Quantum Warfare Market Size

Quantum warfare is becoming a strategic defense priority as militaries prepare for conflict environments where conventional encryption, navigation, sensing and cyber defenses may no longer be sufficient. Quantum technologies are being evaluated for secure communications, post-quantum cryptography, quantum key distribution, precision navigation, submarine detection, GPS-denied operations, cyber defense, electronic warfare and mission simulation.

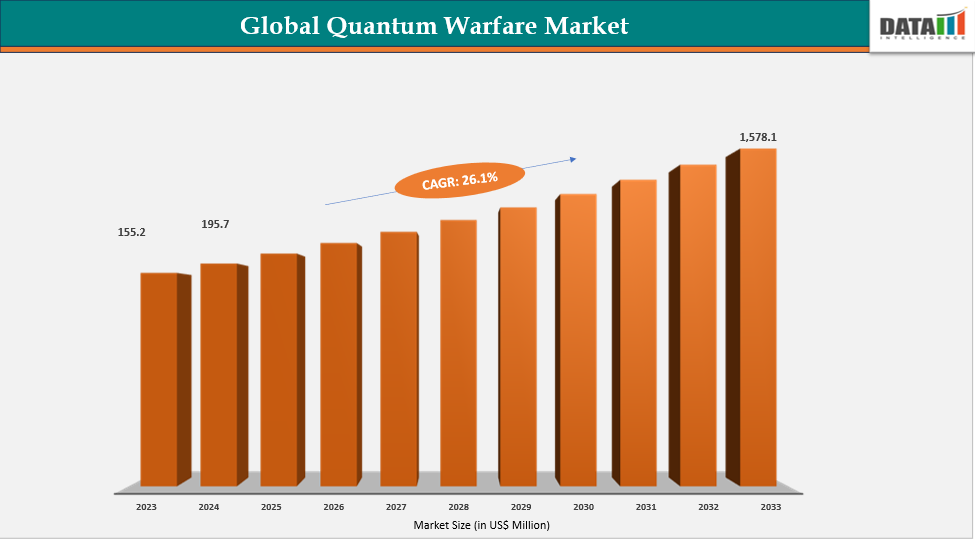

Quantum Warfare Market is valued at US$ 246.78 million in 2025 and is projected to reach US$ 2,508.75 million by 2035, growing at a CAGR of 26.1% during 2026–2035.

The market matters now because defense buyers face a clear timing challenge. Quantum-enabled adversaries could weaken legacy encryption, disrupt command networks and reduce the reliability of satellite-based positioning. This is accelerating procurement interest in quantum-secured communications, quantum sensing, quantum navigation and post-quantum cyber defense.

Key Takeaways

- The Quantum Warfare market size 2026 is recalculated at US$ 311.19 million, supported by defense demand for secure communications, sensing and cyber-resilient systems.

- The Quantum Warfare market forecast 2035 is recalculated at US$ 2,508.75 million, showing strong long-term defense procurement potential.

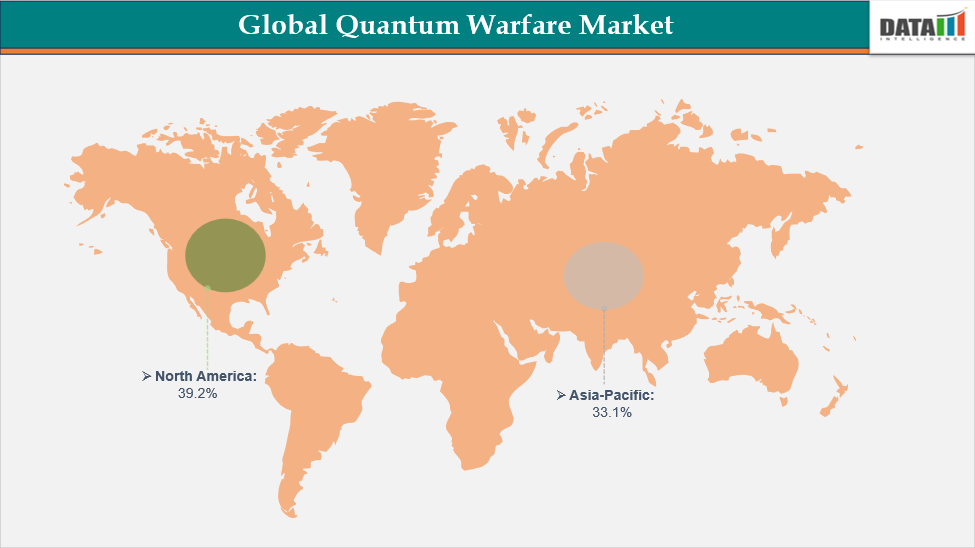

- North America held 39.2% market share in 2024, supported by defense R&D, contractor integration and quantum science funding.

- Asia-Pacific held 33.1% market share in 2024 and is expected to grow fastest, supported by China, India, Japan, South Korea and Australia.

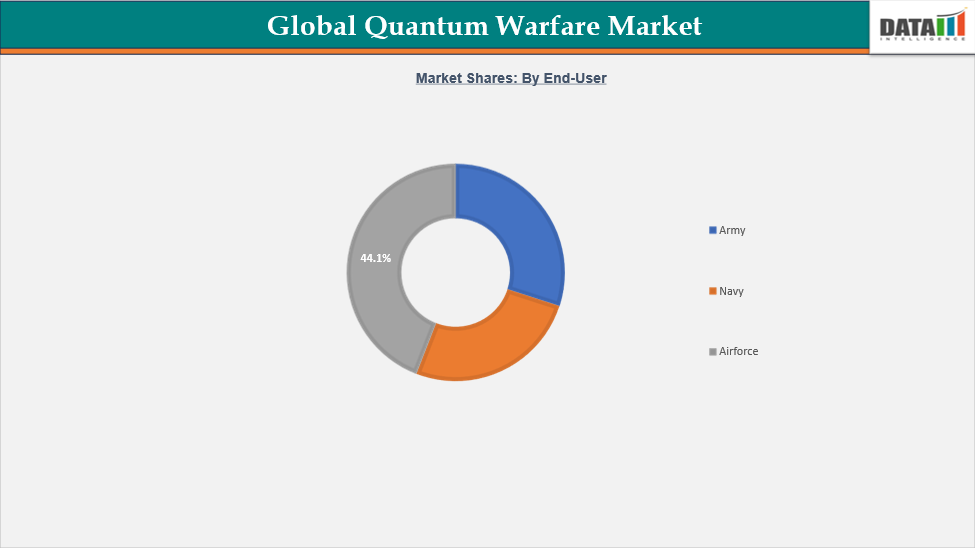

- The Air Force segment is estimated to hold 44.1% market share, driven by secure air links, GPS-denied navigation and advanced airborne sensing.

- The US Department of Defense invested over US$ 700 million in quantum information science between 2019 and 2023, while North American quantum defense R&D investment reached over US$ 844 million in 2023.

- Quantum Warfare top companies include Northrop Grumman Corporation, Lockheed Martin Corporation, RTX Corporation, BAE Systems plc, Thales Group, L3Harris Technologies, IBM, Google LLC, IonQ, Inc. and Quantinuum.

Quantum Warfare Market Scope

| Metric | Details |

| Market Size in 2025 | US$ 246.78 million |

| Market Size by 2035 | US$ 2,508.75 million |

| CAGR | 26.10% |

| Historic Years | 2023 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Segments Covered | By Deployment, Application, End-User and Region |

| Leading Region | North America |

| Fastest Growing Region | Asia-Pacific |

Quantum Warfare Growth Drivers

Quantum-Secured Communications Are Becoming a Defense Modernization Priority

Quantum-secured communications are one of the strongest Quantum Warfare growth drivers. Military satellite, radio and data networks face growing cyber and electronic warfare risks. Quantum key distribution supports highly secure encryption by detecting interference or interception attempts, making it attractive for command-and-control networks.

China demonstrated quantum-encrypted communication between ground stations and satellites in 2020, while Europe is advancing quantum communication infrastructure through EuroQCI. The US Department of Defense invested US$ 140 million in DARPA’s Quantum Network Challenge to support scalable battlefield quantum networks.

GPS-Denied Navigation and Stealth Detection Are Expanding Use Cases

Defense forces need alternatives to GPS-dependent systems in contested environments. Quantum clocks, accelerometers and sensors can support precision navigation when satellite signals are jammed or denied. This is especially relevant for aircraft, submarines, missiles, dronesand naval platforms.

Quantum sensing also creates interest in submarine detection and stealth asset identification. The US Navy is testing quantum sensors for submarine detection with MIT Lincoln Laboratory, while Canada invested CAD 40 million, or US$ 28.9 million, in quantum radar development for Arctic surveillance.

Defense Alliances Are Accelerating Quantum Deployment

Cross-border defense collaboration is strengthening the market. The US, UK and Australia under AUKUS are exploring joint quantum technology applications for secure naval and aerospace operations. Japan and South Korea are also piloting defense quantum communications with domestic telecom partners.

These partnerships show that quantum warfare is moving from isolated research programs toward allied defense architecture.

Buyer Pain Points

| Buyer Group | Key Pain Point | Quantum Warfare Relevance |

| Defense ministries | Future encryption vulnerability | Post-quantum cryptography and QKD reduce cyber risk |

| Air forces | GPS-denied operations and contested airspace | Quantum clocks, sensors and secure data links improve mission resilience |

| Navies | Submarine detection and secure naval command | Quantum sensing and encrypted communication support maritime operations |

| Army commands | Secure battlefield networking | Quantum networks improve tamper-resistant communications |

| Intelligence agencies | Faster analysis and secure data protection | Quantum computing and cryptography support intelligence operations |

| Defense contractors | Need for next-generation platform differentiation | Quantum-enabled subsystems support higher-value defense programs |

Regulatory and Policy Drivers

Quantum warfare adoption is being shaped by national security policy, defense modernization programs and secure communication mandates. Governments are funding quantum programs because future quantum computers could weaken today’s encryption systems.

The EU is supporting EuroQCI with Euro 90 million, or US$ 105 million, in funding between 2021 and 2027. India’s National Quantum Mission is valued at US$ 730 million, with defense-focused quantum encryption projects supporting air and naval command systems. South Korea allocated US$ 60 million in 2023 for military-grade quantum communications.

These policy signals show that quantum warfare is becoming part of sovereign technology strategy.

Substitute Analysis

| Current Alternative | Strength | Limitation Compared With Quantum Technologies |

| Conventional encryption | Widely deployed and mature | Vulnerable to future quantum-enabled decryption |

| Classical radar | Proven defense sensing capability | May face limits against stealth and low-signature targets |

| GPS and satellite navigation | Global coverage and operational familiarity | Vulnerable to jamming, spoofing and signal denial |

| Classical cyber defense tools | Established across networks | May not protect against quantum-era encryption threats |

| Traditional secure radio links | Operationally mature | Can be intercepted, jammed or disrupted in contested environments |

Quantum warfare solutions will not replace all current systems immediately. They are more likely to be adopted first in mission-critical communications, strategic sensing and high-value platforms.

Quantum Warfare Market Segmentation Analysis

Segmented by Deployment (on-premises and cloud based), by Application (intelligence, surveillance, and reconnaissance, precision navigation and timing, target acquisition and guidance, communications, electronic warfare, cyber warfare and others), by End-User (army, navy and air force), and by Region - Share, Trends, and Forecast to 2035.

By Deployment

On-premises deployment is important for defense agencies that require strict control over sensitive quantum systems, classified algorithms and secure communication infrastructure. Cloud-based deployment is relevant for quantum computing access, simulation, algorithm development and defense R&D workflows.

By Application

Communications is one of the most important applications because quantum-secured networks address cyber espionage and interception risks. Precision navigation and timing are also gaining importance as militaries prepare for GPS-denied environments.

Intelligence, surveillance and reconnaissance applications are growing as quantum sensors improve detection possibilities. Cyber warfare is another critical area because post-quantum cryptography is becoming necessary to protect military networks from future quantum-enabled attacks.

By End-User

The Air Force segment holds 44.1% market share, supported by demand for encrypted command links, advanced sensing and GPS-independent navigation. Army applications focus on battlefield communications and cyber resilience. Navy applications are linked to submarine detection, secure naval communications and maritime surveillance.

Practical Use Cases

| Use Case | Defense Value |

| Satellite-enabled QKD | Secures long-range military communication |

| Quantum navigation | Supports operations in GPS-denied environments |

| Quantum radar and sensing | Improves detection of submarines and stealth assets |

| Post-quantum cryptography | Protects defense networks from future quantum cyber threats |

| Quantum computing simulations | Supports logistics optimization and mission planning |

| Quantum-secured air data links | Improves resilience of air-to-air and air-to-ground communication |

Regional Analysis

North America

North America leads the market with 39.2% share in 2024. The region benefits from defense funding, advanced research universities, public-private partnerships and strong defense contractor participation. The US and Canada are investing in quantum communications, sensing and computing to retain defense technology leadership.

IBM, Honeywell, Rigetti and IonQ are collaborating with defense agencies on deployable quantum systems. Lockheed Martin’s contract with D-Wave focuses on quantum computing for logistics and mission simulation, while DARPA’s Quantum Apertures program targets advanced airborne sensing.

Asia-Pacific

Asia-Pacific held 33.1% market share in 2024 and is the fastest-growing region. China, India, Japan, South Korea and Australia are investing in quantum technologies due to geopolitical tensions and the need for secure military communications in the Indo-Pacific.

Europe

Europe remains a major quantum defense region, supported by EuroQCI and defense alliance priorities. The region is focused on building integrated quantum communication infrastructure to protect government and military networks.

European defense demand is likely to concentrate on secure communications, alliance interoperability, cyber resilience and quantum-safe infrastructure.

Company Product Mapping and Vendor Landscape

| Company | Quantum Warfare Positioning |

| Northrop Grumman Corporation | Defense systems integration, sensing and mission technologies |

| Lockheed Martin Corporation | Quantum computing applications for logistics and mission simulation |

| RTX Corporation | Defense electronics, sensing and aerospace systems |

| BAE Systems plc | Defense platforms, secure systems and electronic warfare relevance |

| Thales Group | Secure communications, defense electronics and cryptography |

| L3Harris Technologies, Inc. | Tactical communications, ISR and mission systems |

| IBM | Quantum computing platforms, post-quantum cryptography and defense algorithms |

| Google LLC | Quantum computing R&D and advanced computing capabilities |

| IonQ, Inc. | Quantum computing systems and cloud-accessible quantum platforms |

| Quantinuum | Quantum computing, cryptography and enterprise-grade quantum software |

IBM is a key technology enabler through its IBM Quantum program, which offers over 20 quantum systems accessible through the cloud. Its roadmap toward 1,000-plus qubit processors by 2025 strengthens its positioning in cryptography, defense simulation and quantum algorithm development.

Pricing and Adoption Trends

Quantum Warfare pricing and adoption trends are shaped by high R&D cost, specialized infrastructure, cryogenic cooling, error correction, talent scarcity and defense-grade validation requirements. Building a quantum communication network can cost hundreds of millions of dollars, limiting early adoption to countries with large defense budgets.

Adoption will likely start with high-priority defense networks, strategic communications, aerospace platforms, naval sensing and cyber protection programs. Wider deployment will depend on cost reduction, engineering maturity, workforce availability and operational proof.

Recent and Historical Developments

- May 2026 – Northrop Grumman advances quantum sensing technologies for defense applications

Northrop Grumman continued investing in quantum-enabled sensing, navigation, and secure communications technologies to improve military situational awareness, GPS-independent navigation, and resilient defense systems for future operational environments. - May 2026 – IBM expands quantum computing capabilities for national security research

IBM enhanced its quantum computing ecosystem by advancing quantum hardware, software, and hybrid computing technologies that support defense research, cryptography, optimization, and secure communications. - April 2026 – Lockheed Martin strengthens quantum-enabled defense research

Lockheed Martin expanded collaborations with government agencies and research institutions to accelerate the development of quantum computing, quantum sensing, and quantum networking technologies for next-generation defense systems. - April 2026 – Quantinuum advances quantum cybersecurity and secure communications

Quantinuum introduced new quantum cybersecurity capabilities focused on quantum-resistant encryption, secure key generation, and trusted communication technologies to address emerging national security requirements. - March 2026 – RTX Corporation expands quantum technology investments

RTX continued developing quantum sensing and advanced computing technologies for defense applications, including intelligence, surveillance, electronic warfare, and resilient positioning, navigation, and timing (PNT) systems. - March 2026 – Google LLC advances fault-tolerant quantum computing research

Google continued improving quantum computing architectures and error-correction technologies, supporting long-term applications in defense modeling, cryptography, and optimization for complex military operations. - February 2026 – Thales Group strengthens quantum communication initiatives

Thales expanded research into quantum-secure communication systems and post-quantum cryptography to enhance cybersecurity and protect critical defense and government communication networks.

Report Benefits

This report helps defense agencies evaluate quantum warfare investment timing, procurement priorities and mission-critical use cases.

It supports investors by quantifying the Quantum Warfare market forecast 2035 and identifying demand signals across secure communications, sensing, navigation and cyber defense.

It helps technology companies assess product opportunities in QKD, post-quantum cryptography, quantum sensors, quantum computing and mission simulation.

It supports defense contractors in mapping platform integration opportunities across air, naval, land and cyber domains.

It helps strategy teams compare regional funding, vendor positioning, adoption barriers and long-term defense modernization priorities.

Target Audience

The report is designed for defense ministries, military procurement agencies, aerospace and defense contractors, quantum technology companies, cybersecurity vendors, telecom infrastructure providers, intelligence agencies, investors, policy teams, defense strategy leaders and R&D organizations.

Suggestions for Related Report