Quantum Photonic Sensors Market Overview

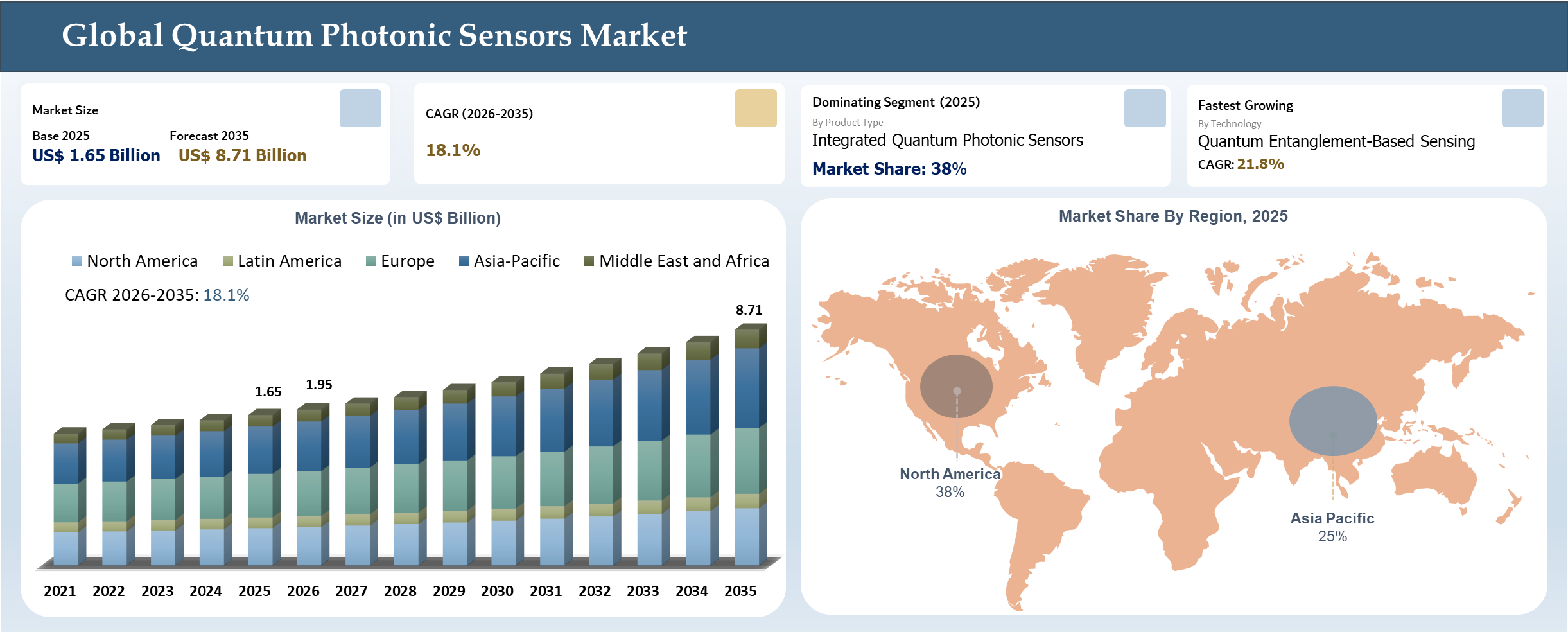

Global Quantum Photonic Sensors Market reached US$ 1.65 billion in 2025 and is expected to reach US$ 8.71 billion by 2035, growing with a CAGR of 18.1% during the forecast period 2026-2035. The global quantum photonic sensors market is expanding due to rising demand for scalable, integrated photonic platforms that support high-precision sensing across defense, aerospace, and industrial applications. Companies and research consortia are actively responding to this trend.

For example, in 2025, Pixel Photonics, a U.S.-based quantum photonics startup, signed an MoU with Aegiq to combine single-photon sources and superconducting nanowire detectors (SNSPDs), accelerating development of scalable photonic quantum sensing platforms. This trend is also reflected in collaborative funding initiatives, such as the 2024 QLASS consortium in Europe, securing €6 million from the European Commission to develop fully integrated quantum photonic circuits, demonstrating that joint R&D and partnerships are strategic for commercializing quantum photonic sensor technology.

Quantum Photonic Sensors Industry Trends and Strategic Insights

- Quantum photonic sensors are currently moving from lab-based development to actual deployment for defense navigation, biomedical diagnostic, semiconductor metrology, and industrial precision measurement applications. The demand for highly sensitive quantum photonic sensing devices for the detection of magnetic field changes, gravity fluctuations, and optical shifts above and beyond what conventional sensors can do is rising.

- The US, China, Germany, the UK, and Japan governments are investing in quantum technology development in their national quantum strategies, particularly in secure sensing, autonomous navigation, and advanced imaging capabilities. Defense organizations are concentrating on quantum photonic sensors for GPS-denied military missions and submarine detection purposes.

- Quantum sensors commercialization will require integrated photonics and silicon photonics chip production technologies. Businesses are increasingly concentrating on photonic integrated circuits (PICs), which will allow them to build smaller, more energy-efficient, and mobile quantum sensors that may be used in various industries and health care applications.

- The industry is also experiencing cross-over integration with artificial intelligence, edge computing, and quantum photonic sensors. Machine learning algorithms have improved accuracy by enhancing signal interpretation and noise removal, allowing real-time analysis in aerospace, environmental monitoring, and medical imaging applications.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 1.65 Billion | |

| 2035 Projected Market Size | US$ 8.71 Billion | |

| CAGR (2026-2035) | 18.1% | |

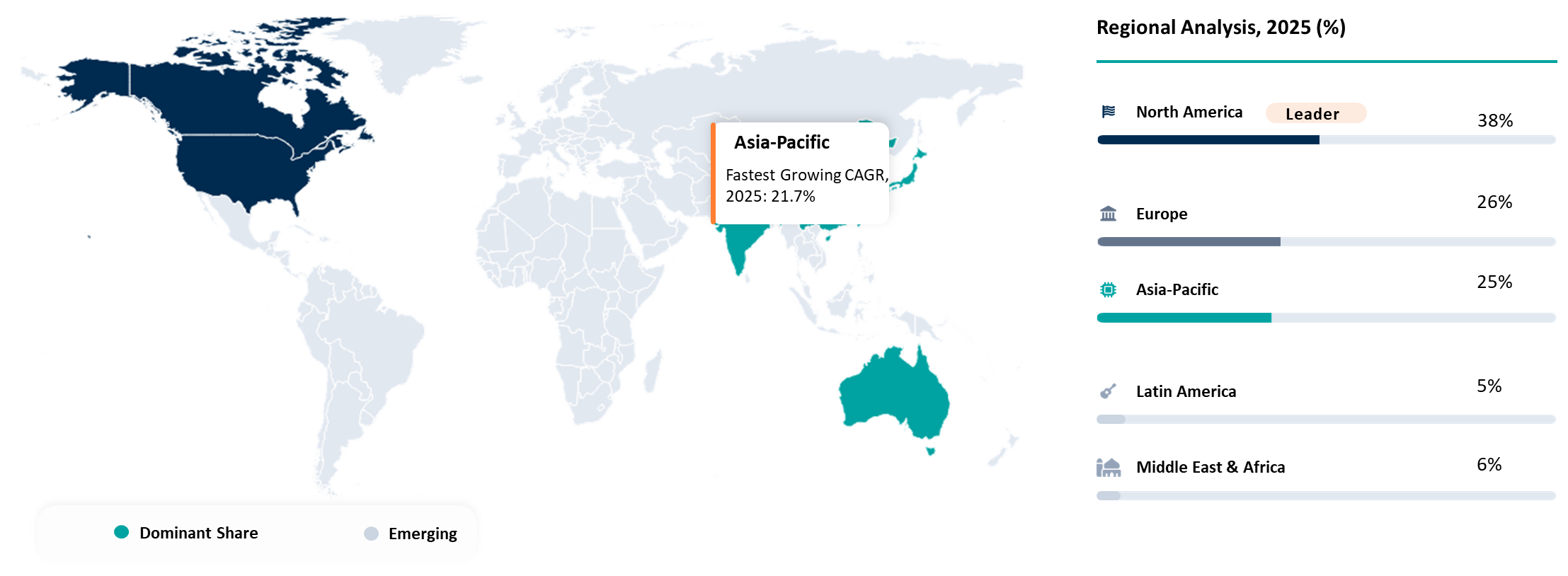

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Product Type | Integrated Quantum Photonic Sensors, Discrete Quantum Photonic Sensors, Others | |

| By Technology | Single-Photon Detection-Based Systems, Quantum Entanglement-Based Sensing, Quantum Interference-Based Sensing, Others | |

| By End-User Industry | Aerospace and Defense, Healthcare, Industrial, Telecommunications, Environmental, Automotive and Transportation, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

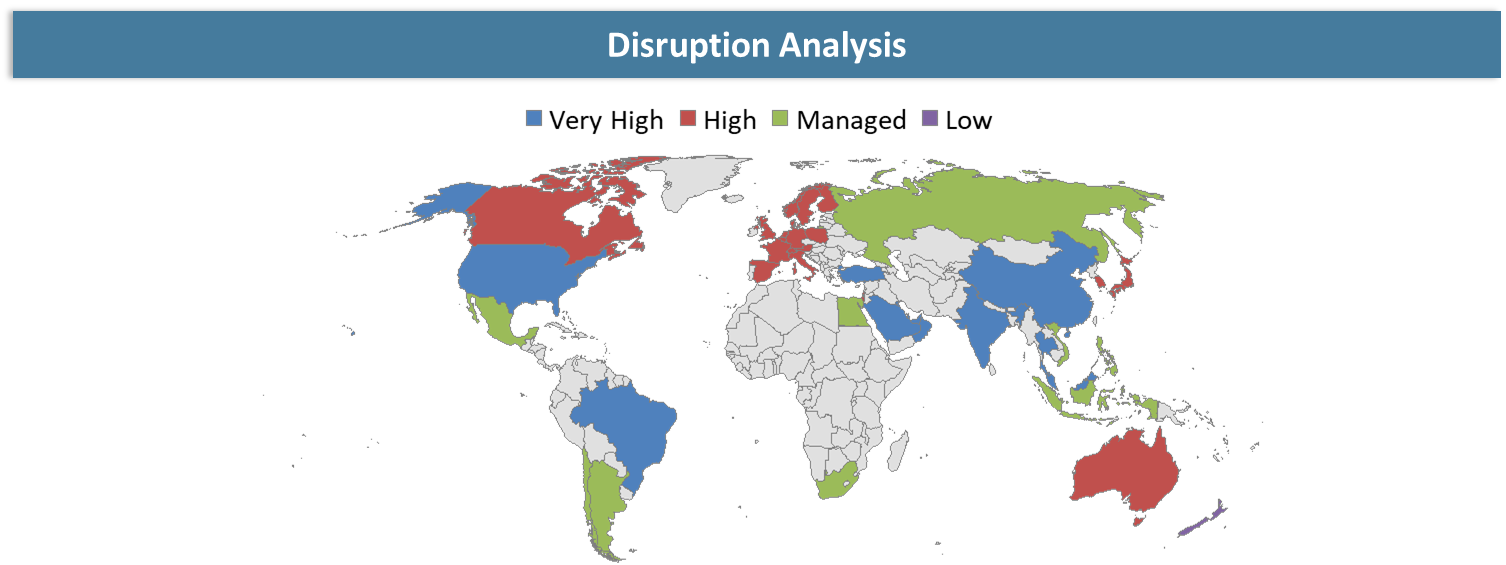

Disruption Analysis

Shift Toward Integrated Photonic-Quantum Architectures Redefining Sensing Platforms

The major disruption is the transition from individual optical systems to quantum integrated photonic systems, which allow the development of compact and effective sensing systems with reliable signals. Such demands are being placed on the industry because of needs for defense navigation, semiconductor inspection, and biomedical sensing. Integrated photonics will reduce system complexity, power usage, and make scalability possible, thus providing an advantage to those companies having photonics on the chip. This change is disrupting existing supply chains and making legacy components become obsolete.

Also, parallel disruption is the development of wafer-level processing and photonic integration, which allows quantum sensor devices to be manufactured in scalable ways. As a consequence of such innovations, cost limitations and barriers for further commercialization of quantum sensor technology will disappear, and technology development will go beyond the laboratory stage and into the industry and even defense field. In addition, the convergence of silicon photonics with quantum sensing technologies enables better integration with artificial intelligence (AI) edge computing.

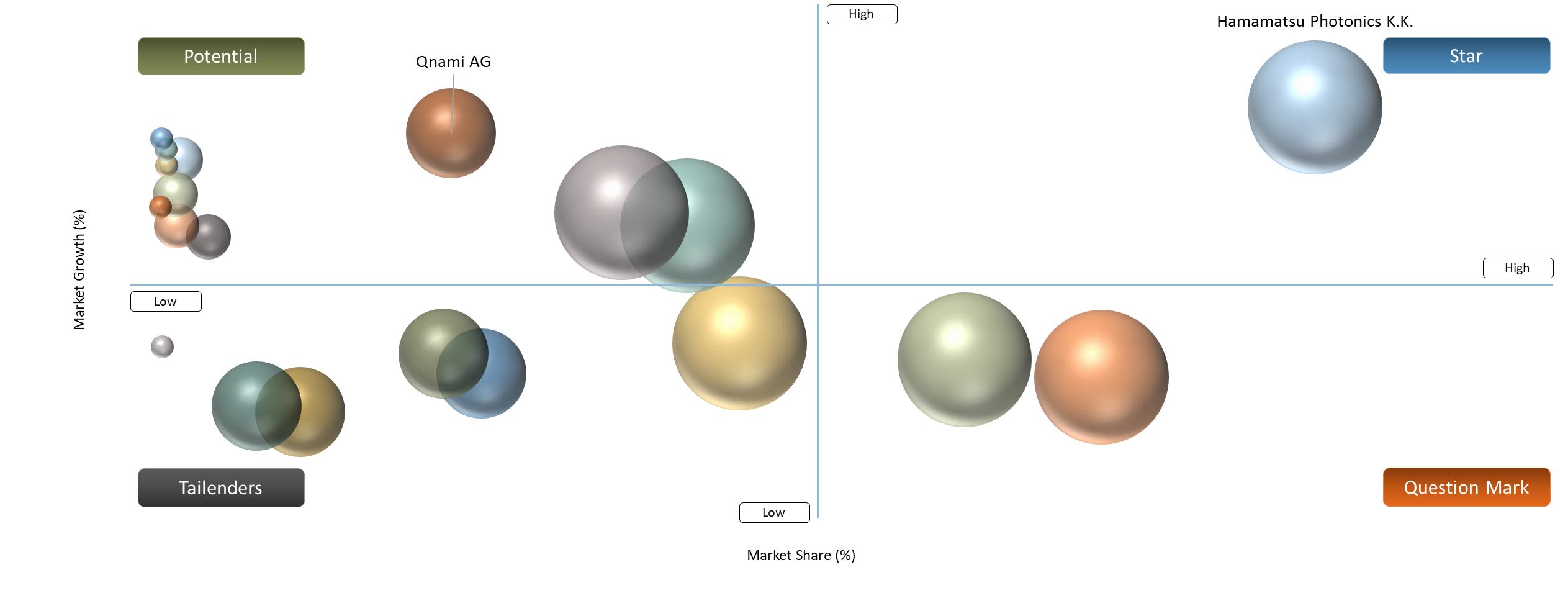

BCG Matrix: Company Evaluation

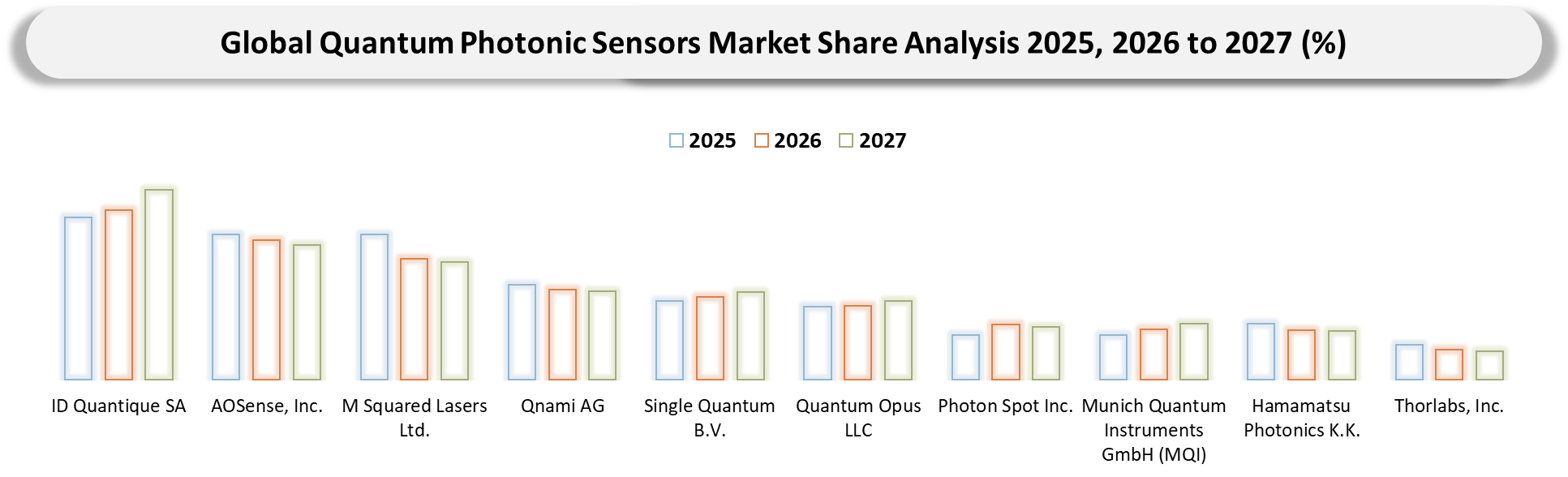

Stars and Question Marks is the grouping that illustrates the balance between high demand and maturity of scale in firms. Examples of stars include Hamamatsu Photonics K.K., Thorlabs Inc. and Single Quantum B.V., because they have high capabilities and positioning in sensing and imaging. Scale and positioning towards industrial and defense demand allow them to grow over time. Firms in the question mark group include AOSense Inc., M Squared Lasers Ltd., ID Quantique SA and Quantum Opus LLC.

Firms in potential players and tailenders groups show specialization and innovation, but restricted market presence in terms of global scale. This is illustrated by companies such as Qnami AG, Photon Spot Inc. and Munich Quantum Instruments GmbH (MQI). They are potential players because they have precise innovations for sensing.

Market Dynamics

Increasing Need for Precision and Security in Critical Applications

The growing demand for ultra‑precise and highly secure measurement systems is driving adoption of quantum photonic sensors across defense, aerospace, navigation, and critical industrial infrastructure. Classical navigation and sensing systems face vulnerabilities such as GPS spoofing and jamming, prompting defense agencies and technology stakeholders to explore quantum alternatives that offer higher accuracy, resilience, and reduced reliance on external references. Government defense innovation units and national quantum programs are investing in compact quantum photonics and integrated sensing architectures to enhance mission‑critical operations such as submarine detection, inertial navigation, and secure timing - use cases where traditional sensors cannot meet performance and security requirements.

For instance, in 2025, Nexus Photonics, a U.S.‑based quantum photonics company, was awarded a contract by the U.S. Defense Innovation Unit (DIU) to advance photonic integration for quantum sensing systems, aiming to drastically reduce size, weight, power, and cost (SWaP‑C) while enabling field‑ready navigation and anomaly detection platforms. Another example: in 2026, IonQ, a U.S. quantum technology firm, acquired Vector Atomic, a California‑based quantum sensor developer, to expand its portfolio into precision atomic clocks and photonic inertial sensors for secure navigation and timing - technologies critical in defense and aerospace environments where signal integrity and measurement precision are paramount.

Challenges in Commercialization and Supply Chain Maturity

Despite strong demand, commercialization of quantum photonic sensors faces hurdles related to complex hardware, high R&D costs, and limited manufacturing capacity. Quantum photonic systems require precise optical alignments, cryogenic compatibility in some cases, and highly specialized components - factors that contribute to long development cycles and higher unit costs compared with conventional sensors. These barriers slow down large‑scale adoption in price‑sensitive segments such as consumer electronics and mass automotive applications.

Smaller suppliers and startups also encounter supply chain constraints for key components like high‑efficiency photon detectors, specialized PIC substrates, and ultra‑low loss waveguide materials. Extended lead times and limited vendor ecosystems make scaling production difficult, particularly for companies lacking strong manufacturing partnerships. As a result, many organizations are cautious about adopting nascent quantum photonic systems for mission‑critical operations until hardware reliability and supply continuity improve.

Segmentation Analysis

The global quantum photonic sensors market is segmented based on product type, technology, end-user industry, and region.

Rapid Growth in Integrated Quantum Photonic Sensors Driven by Commercial Adoption

Integrated quantum photonic sensors are projected to account for 38% market share in 2025, making them the dominant product segment due to increasing demand for compact, scalable, and power-efficient sensing systems. Demand is fueled by the need for miniaturized, high-precision sensors across telecommunications, aerospace, and industrial manufacturing applications, where smaller form factors reduce deployment costs and improve performance at scale. Advances in photonic integration have enabled real-world usage in both laboratory and field environments, bridging the gap between research prototypes and operational systems. Investments in foundry-scale photonics and standard process technologies further support this shift toward integrated solutions.

Integrated sensing momentum is supported by real-world company developments that emphasize product readiness and commercialization. For instance, in 2026, Monarch Quantum, a U.S.-based quantum photonics provider, launched integrated photonics engines designed to consolidate discrete optical components into commercial modules that accelerate market adoption. Such developments demonstrate how scalable, factory-aligned photonic systems are enabling broader deployment beyond research labs, helping industries such as defense, navigation, optical communications, and environmental monitoring benefit from quantum precision at practical scales.

Customization and High-Precision Performance Sustaining Demand for Discrete Quantum Photonic Sensors

Discrete quantum photonic sensors have experienced strong growth due to their demand for high-precision, customizable sensing platforms in aerospace, oil and gas exploration, and advanced research laboratories. Bulk optics and fiber-based architectures provide superior flexibility for precision gravimetry, spectroscopy, and environmental monitoring applications. Research laboratories and defense programs continue to rely on discrete systems for experimental validation and mission-critical sensing tasks. Their modular design supports rapid prototyping and customization for specialized industrial requirements.

For instance, in 2024, Menlo Systems, a Germany-based photonics company, introduced enhanced optical frequency comb systems enabling ultra-precise interferometric measurements. These product advancements highlight ongoing innovation within discrete quantum photonic sensing platforms.

Geographical Penetration

Rising Government Investments Accelerating Quantum Sensor Adoption in Asia-Pacific

Asia‑Pacific remains one of the fastest‑growing regions in the quantum photonic sensors market with an estimated 25% share in 2025, driven by significant government funding, national quantum missions, and expanding research infrastructure. Governments are prioritizing quantum technology to support high‑precision navigation, defense sensing, industrial metrology, and environmental monitoring, accelerating commercialization efforts beyond purely academic research. China continues scaling local sensor ecosystems with increased installations of quantum testbeds and prototype facilities, while Japan and South Korea integrate quantum sensing into aerospace and robotics research.

For instance, in 2026, IBM, a U.S.–based technology company, announced plans to open a quantum computing facility in Amaravati, India, under India’s National Quantum Mission to support local research and talent development in quantum technologies, including sensing platforms. India’s National Quantum Mission itself has allocated over ₹6,000 crore (USD 730 million) through 2030 to foster quantum R&D and industry collaboration, supporting India’s position in the global quantum photonic sensors landscape.

India Quantum Photonic Sensors Market Outlook

India’s quantum photonic sensors market is accelerating on the back of strategic government initiatives under the National Quantum Mission (NQM), which aims to build a robust quantum hardware ecosystem, including sensing and metrology technologies, securing economic and defense advantages. The expansion of quantum fabrication and sensor development hubs at top institutions like IIT Bombay and IISc Bengaluru is expected to strengthen local production of quantum sensors and integrated photonic components, boosting industry‑academia collaboration and commercialization prospects.

For instance, in 2026, QpiAI, an India‑based deep tech startup, launched India’s first indigenous 25‑qubit quantum computer architecture in Bangalore, laying the groundwork for adjacent sensor technologies that rely on quantum readout and coherent detection for navigation, imaging, and timing applications. Additionally, innovations such as the PhotonSync technology from Indian research teams are enabling conventional optical fibre to act as quantum communication channels, a key enabler for distributed quantum sensing networks across the country.

China Quantum Photonic Sensors Market Trends

China continues to position itself as a global leader in quantum photonic technologies by leveraging concentrated state R&D funding and coordinated national strategy to advance quantum‑grade photonic hardware and sensing systems. Large‑scale quantum research infrastructure, coupled with military and civilian collaborations, is accelerating the development of integrated quantum sensors for precision navigation, environmental monitoring, and communications applications across industrial and defense sectors.

For instance, in 2025, CHIPX, a China‑based photonics and quantum technology firm, introduced a next‑generation photonic quantum chip integrating thousands of optical components capable of massively enhancing computation and sensing tasks, which is seen as a foundational step toward commercial‑scale photonic sensor production for aerospace, finance and industrial analytics markets.

High Adoption of Quantum Photonic Sensing Technologies Across North America

North America remains the dominant region, capturing an estimated 38% market share in 2025, supported by extensive federal funding, defense innovation programs, and integration of quantum sensors into navigation and industrial testbeds. The region leads in patent filings, academic–industry partnerships, and early commercial deployments. The United States drives most of this growth with substantial investments into sensor integration for aerospace, defense, and precision metrology, while Canada focuses on environmental and geoscience applications backed by research‑industry collaboration.

For instance, in 2026, Cisco Systems, a US networking company, partnered with quantum startup Qunnect to build a real‑world quantum network over existing fiber infrastructure in New York, marking significant progress toward quantum communication ecosystems that support distributed sensing and advanced measurement applications across critical infrastructure.

U.S. Quantum Photonic Sensors Market Insights

The U.S. leads regional quantum photonic sensor adoption, driven by defense programs, navigation projects, and strong private‑public partnerships. Federal initiatives such as the National Quantum Initiative and substantial R&D investment continue to fuel early commercial use cases. Quantum sensors are increasingly deployed in prototype navigation systems, defense platforms, and high‑precision instrument clusters at research labs and industrial testbeds.

For instance, in 2026, IonQ, a U.S.‑based quantum technology company, completed acquisitions of firms including Vector Atomic to bolster its position in quantum sensor and positioning technologies, reflecting strategic moves to integrate photonic and atomic quantum sensing into broader technology offerings.

Canada Quantum Photonic Sensors Market Growth

Canada’s quantum photonic sensors market is expanding steadily, supported by collaborative research initiatives and innovation funding that targets environmental monitoring, geoscience, and precision metrology. Universities and research institutes are key adoption hubs for quantum sensor prototypes, and national modernization programs encourage commercialization partnerships.

For instance, in 2025, researchers at the Institute for Quantum Computing (IQC) at the University of Waterloo secured funding to develop a quantum entanglement‑based sensing system linking remote observation stations, showcasing Canada’s growing innovation footprint in real‑world quantum sensor applications.

Sustainability Analysis

The global quantum photonic sensors market has a developing but increasingly sustainable profile, as integrated photonic circuits and compact sensor architectures enable higher measurement efficiency, reduced energy consumption, and minimized material waste compared to traditional bulky optical or atomic sensing systems. By leveraging silicon, silicon nitride, and lithium niobate platforms, quantum photonic sensors reduce reliance on scarce or high-energy materials while maintaining ultra-precise measurements for applications in aerospace, defense, healthcare, and industrial monitoring.

The primary environmental impact arises from the fabrication of photonic chips, specialized substrates, and high-precision optical components, which require cleanroom environments, rare materials, and energy-intensive processes. However, sustainability initiatives are advancing across the industry. Measures such as energy-efficient photonic chip design, modular manufacturing, and low-power single-photon detection modules are lowering environmental footprints. For instance, in 2025, Veeco Instruments deployed energy-optimized deposition systems for quantum photonic fabrication, while in 2024, Aeluma developed compact, low-power quantum dot photonic integrated circuits for NASA applications, demonstrating how sustainability and performance co-evolve in the market.

Competitive Landscape

- The global quantum photonic sensors market is characterized by a competitive landscape that includes both established and regional players.

- Key players include ID Quantique SA, AOSense, Inc., M Squared Lasers Ltd., Qnami AG, Single Quantum B.V., Quantum Opus LLC, Photon Spot Inc., Munich Quantum Instruments GmbH (MQI)., Hamamatsu Photonics K.K., Thorlabs, Inc.

Key Developments

- In 2025, Rydberg Technologies, a U.S.–based quantum sensing firm, launched Rydberg Photonics GmbH in Berlin to deliver micro‑integrated photonic engines designed to support global quantum systems, strengthening photonic hardware innovation across research and commercial sectors.

- In 2026, Renishaw, a UK‑based precision technology company, launched a Time‑Resolved Raman Spectroscopy (TRRS) module with an integrated single‑photon avalanche diode (SPAD) sensor, advancing optical quantum sensing capabilities for materials, biological, and environmental analysis.

Why Choose DataM?

- Data-Driven Insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. This approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. This personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. These insights complement and go beyond what is typically available in generic databases.

Target Audience

- Manufacturers/ Buyers

- Industry Investors/Investment Bankers

- Research Professionals

- Emerging Companies