Process Safety Services Market Overview

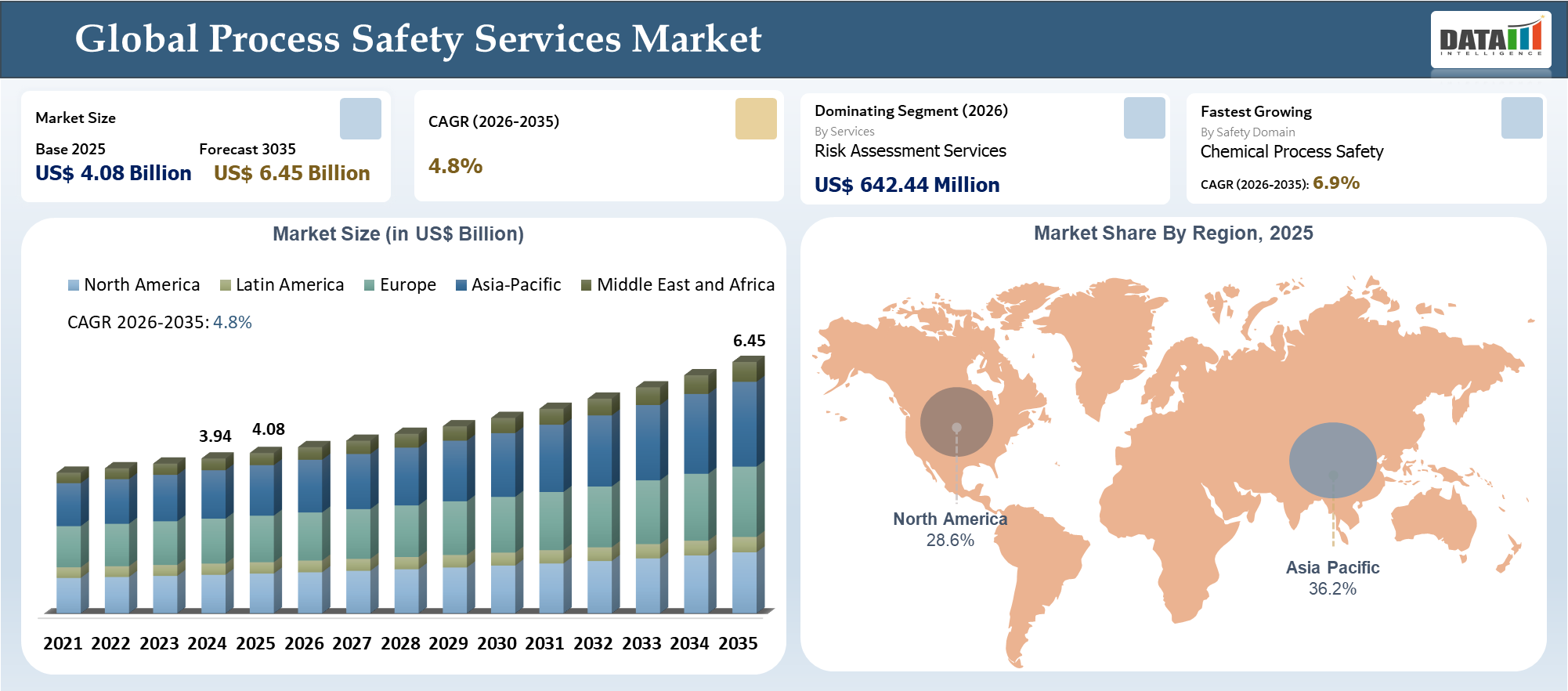

The global process safety services market reached US$ 4.08 billion in 2025 and is expected to reach US$ 6.45 billion by 2035, growing with a CAGR of 4.8% during the forecast period 2026-2035. Management of the hazards associated with fire, explosions and toxic substance leaks has changed from compliance-driven activities to a board-level strategy that focuses on process safety. Process safety services are going through a restructuring period due to increased regulatory pressure, complexity in industries and awareness regarding risk exposure among heavy asset industries.

It has been found by the International Labor Organization that over one billion people work with hazardous materials every year, with one million deaths occurring annually due to exposure to chemicals. The highest number of fatalities happened in developing countries like India and China and this indicates the disparity in the level of development in terms of safety practices. The trend is increasing the need for internationally recognized safety management frameworks and external expertise. A shift is being witnessed in the safety management system from compliance-driven processes to more proactive and risk-based processes. Organizations have begun allocating more resources to hazard identification techniques including HAZOP analysis, Layer of Protection analysis and QRA (Quantitative Risk Assessment).

Process Safety Services Industry Trends and Strategic Insights

- Stricter regulations, ageing plant facilities, and increased ESG obligations in the energy, chemicals, and manufacturing industries are impacting the services demand.

- Europe and North America markets will be led by regulatory pressure whereas Asia-Pacific will witness fastest growth owing to increasing levels of industrialization. The focus of industies is moving from reactive services towards digitally enabled predictive services and solutions.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 4.08 Billion | |

| 2035 Projected Market Size | US$ 6.45 Billion | |

| CAGR (2026-2035) | 4.8% | |

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Service | Risk Assessment Services, Process Safety Consulting, Safety Engineering Services, Inspection, Testing & Audit Services, Process Safety Testing & Laboratory Services, Training & Certification Services, Incident Investigation & Forensics, and Software & Safety Lifecycle Services | |

| By Safety Domain | Chemical Process Safety, Fire & Explosion Safety, Toxic Release & Exposure Risk, Electrical & Static Hazard Risk, Mechanical Integrity & Asset Reliability, Environmental & Emission Safety, Human Factors & Ergonomics, Cyber Physical Risk (ICS & OT Security), and Others | |

| By Engagement Model | Project Based Consulting, Annual Retainer Based Services, Managed Safety Services, and Software Subscription Based Services | |

| By Safety Maturity Level | Reactive Safety Services, Proactive Safety Services, and Predictive & Data Driven Safety Services | |

| By Plant Size | Small Scale Facility, Medium Scale Industrial Plant, Large Scale Industrial Complex, and Mega Integrated Refinery or Petrochemical Complex | |

| By Facility Lifecycle Stage | Greenfield Project Phase, Brownfield Expansion Phase, Operational Maintenance Phase, and Decommissioning & Asset Retirement Phase | |

| By Compliance & Regulatory Requirements | North America Framework, Europe Framework, Latin America Framework, Asia Pacific Framework, and Middle East and Africa Framework (National Oil Company Safety Standards). | |

| By Safety Technology | SIS (Safety Instrumented Systems), Process Control Systems (DCS and PLC), SIL Assessment Tools, Risk Modeling Software, Digital Twin Platforms, Real Time Monitoring & Sensors, AI & ML Predictive Risk Analytics, Mobile Safety Apps & Field Tools, Industrial Cybersecurity Tools (ICS and OT), and Others | |

| By End-User | Oil & Gas, Energy & Power, Chemicals & Petrochemicals, Mining & Metals, Process Manufacturing, Pharmaceuticals & Biotechnology, Food & Beverage, Construction & Infrastructure, Utilities, Automotive & Discrete Manufacturing, Government, and Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

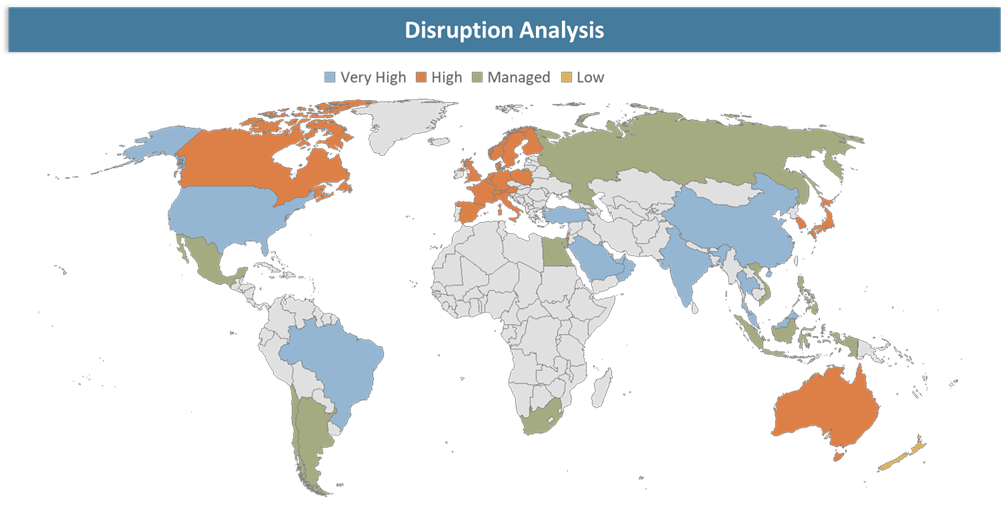

Disruption Analysis

Supply Chain Disruptions for Hardware

Supply chain disruptions is a notable threat affecting the Process Safety Services industry. The threat affects the acquisition and implementation of safety equipment such as sensors, controls, safety instrumented systems (SIS), and monitoring devices. Safety systems require a vast network of global suppliers, making them extremely susceptible to geopolitical conflicts, logistical issues, semiconductor shortages, and vendor disruptions.

Cybersecurity threats are directly resulting in supply chain disruptions. The attack by ransomware on logistics services or component providers has resulted in operational disruptions. Cybersecurity attacks on logistics platforms caused disruptions within retail and supply chains. Order fulfillment was halted during these attacks, preventing deliveries in different geographic locations.

Manufacturing companies depend on production cycle, and any disruption during safety systems integration will expose the business to greater risk and compliance issues. Industries such as oil & gas and petrochemical heavily depend on safety systems to monitor the production process. Supply chain disruptions in acquiring equipment will cause a delay in project implementation, downtime, and capital expenditure.

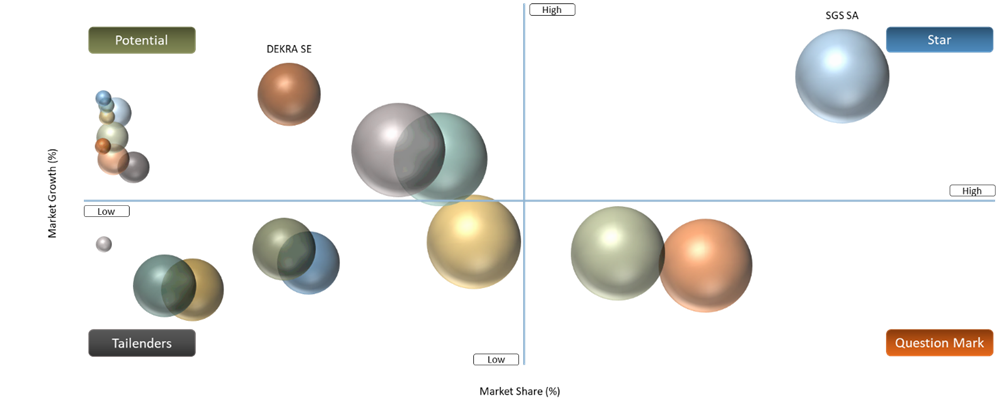

BCG Matrix: Company Evaluation

The companies may be classified as Stars, Potential, Question Mark, and Tailender Participants according to their digital capabilities and service range. The established TIC and global engineering companies work as 'Potential' players with the advantage of good client relations and demand due to compliance.

The technology-based companies providing predictive and digital safety services become 'Stars' for their fast-growing business prospects. In contrast, smaller consultancy companies that conduct risk assessments and start-up AI-based safety analytics players become 'Tailender' Participants.

Market Dynamics

Tightening Regulatory & Compliance Regimes

The authorities and regulators have steadily become stricter regarding regulation, owing to disasters and other environmental problems, alongside the need for safety in society. As an example, there exist OSHA PSM regulations in U.S., which require organizations to adopt procedures aimed at risk identification, hazard assessment and avoidance of incident occurrence.

In terms of enforcement, regulatory scrutiny is still intense but constrained in resources, making it increasingly incumbent upon organizations to take initiative regarding compliance. For example, according to OSHA statistics, there are about 1,850 inspectors who monitor over 130 million employees in eight million workplaces, equating to one inspector for roughly 70,000 employees. The implication here is that regulators are becoming increasingly dependent on self-compliance systems, audits and external safety services, which drive demand for process safety consulting, auditing and digital compliance tools.

Fines for violations of regulations, mandatory shutdowns and even criminal charges have become more frequent, especially where governments implement more stringent ESG policies. Hence, firms are allocating more resources to implementing state-of-the-art safety management solutions, HAZOP analysis and quantitative risk assessment. The move towards continuous monitoring through the use of digital twins, artificial intelligence for identifying risks and real-time safety analysis makes the involvement of process safety services even more imperative.

Fragmented Market & Differing Standards

The process safety management (PSM) model varies significantly depending on the location. For example, the OSHA model consists of 14 components, while other models from Europe and other parts of the world differ in terms of structure, nomenclature and implementation strength. The disparity in standards and regulations creates challenges such as duplicity of work required, benchmarking inconsistencies and scalability challenges of standardized services globally.

When considering practical implications, fragmentation creates isolated safety systems and varying data classification structures, thus making it hard for companies to incorporate hazard identification, reporting and risk control processes into their operations. Evidence from practice shows that many of the PSM processes continue to be fragmented and reactive, failing to create integrated systems of risk management and real-time monitoring. The fragmentation challenges faced by service providers include methodology differences required in various jurisdictions.

Inconsistencies in process safety data and information also play a significant role in making things difficult. Research in academic settings shows that industrial plants contain several inconsistencies between the documentation of safety measures (such as piping diagrams) and the reality of the plant itself. Moreover, hazards associated with unintended chemical reactions are not sufficiently addressed.

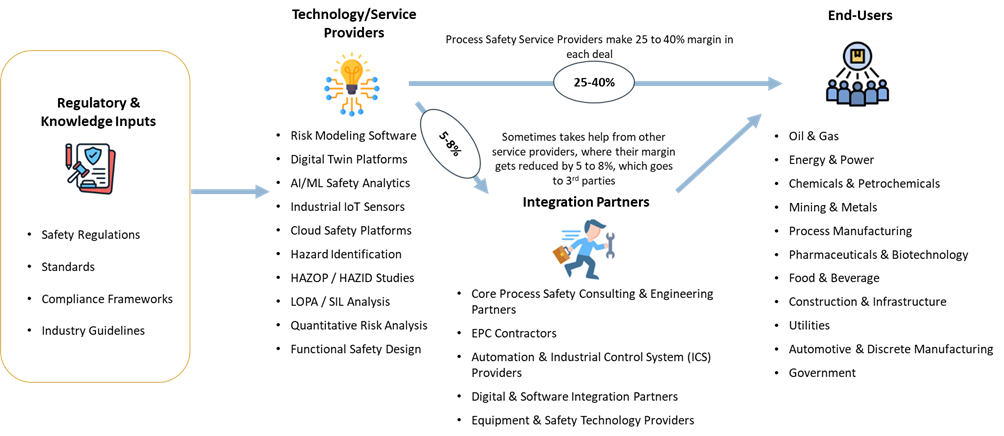

Supply Chain Analysis

The supply chain for process safety services includes end-users, service/technology providers, integration partners and regulators, thereby developing an interdependent ecosystem. Service providers make use of various inputs like engineering knowledge, regulatory requirements, and digitization capabilities to provide safety assessment, audit, and life cycle services.

Input factors for upstream activities consist of data, plant design information, and operating information, while value from downstream activities is created through risk reduction, compliance, and sustained operations. Growing digitalization is impacting the supply chain by allowing real-time data communication and integrated safety management.

Regulatory Impact Index

The regulatory environment is an important component in determining the market attractiveness with variations being present in terms of how strictly regulations are applied, how rigorously enforced and how exposed a country’s industry is to regulatory controls. In areas where strict regulations like OSHA, Seveso III, and IEC are present, there is greater demand for process safety services because of mandatory compliance requirements.

However, regulatory influence is not always evident since many companies in Middle East and Asian countries implement international standards like EPA, API, and IEC in lieu of lacking stringent regulations.

Segment Analysis

The global process safety services market is segmented based on services, safety domain, engagement model, safety maturity level, plant size, facility lifecycle stage, compliance & regulatory requirements, safety technology, end-user and region.

Increasing renewable energy, modernization of the grid and increasing rate of electrification

The energy and power sector, including thermal, nuclear and renewable energy power plants, relies on process safety services to ensure system stability and prevent system failures. The utility sector is facing new challenges to the operation and safety of the power generation and energy sectors due to significant growth in renewable energy production.

The requirements for safety are changing to respond to new risks such as battery storage, hydrogen and grid instability risks. DNV is one of the key players involved in the energy transition process and its safety, especially when it comes to hydrogen and renewable infrastructure safety analysis. The Skylark Joint Industry Project by DNV was established at the end of 2024 to enhance the safety requirements associated with the operation of CO2 pipelines, considering emerging safety issues related to decarbonization and electrification.

Geographical Penetration

Strengthening of regulatory landscape and government action plans supporting process safety services requirements

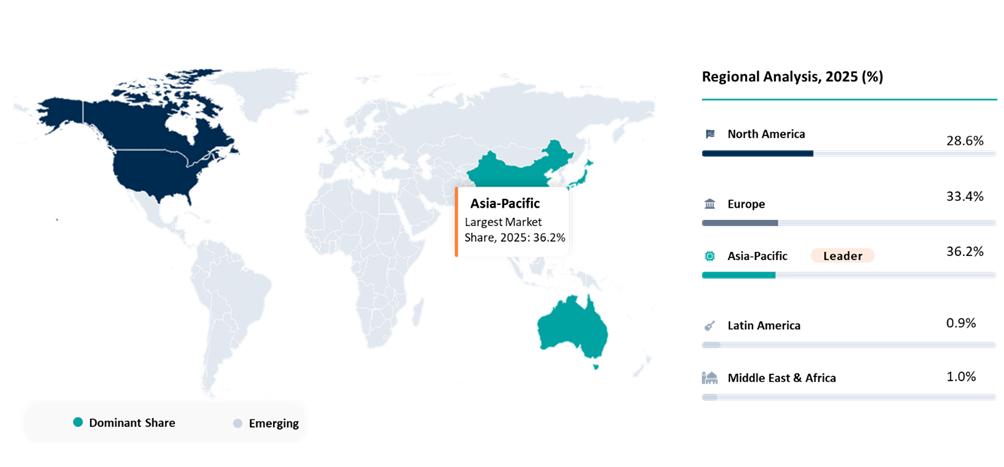

Asia-Pacific process safety services market is the fastest-growing market globally, accounting for around ~36% of the total market in 2025.

China Process Safety Services Market Trends

China’s process safety services market is being reshaped by the 3-year (2024-2026) national action plan, which mandates stricter inspection of hazardous chemical permits and licenses. It is driving demand for compliance audits, licensing support and regulatory advisory services, while reinforcing a shift toward continuous compliance monitoring across chemical and petrochemical industries.

Integration of Process Safety Management (PSM) into national standards and alignment with global frameworks from Center for Chemical Process Safety is transforming the market into a structured, auditable and capability-driven ecosystem.

Demand is expanding from basic safety studies to end-to-end PSM implementation, advanced risk engineering (HAZOP, QRA) and competency-based training services. Digitalization and the chemical industrial park model are driving rapid growth, including real-time risk monitoring and safety prediction technologies. Gaps in capabilities of SMEs, inadequate regional enforcement, and workforce shortages still drive the reliance on outsourcing, ensuring continued growth of technology-based process safety services.

India Process Safety Services Market Outlook

India is gradually entering into the initial stages of formalization, with regulatory pressure and training drives starting to result in structured demand for services. In December 2024, the Department of Chemicals and Petrochemicals (DCPC) organized its first drive aimed at training professionals on chemical and petrochemical industrial safety (the drive held between November 28-29, 2024, in Ahmedabad), which marks the initiation of structured national efforts to bolster process safety skills among MAH facilities.

In September 2025, the Gujarat Institute of Disaster Management organized a one-day capacity building drive on PSM implementation, which is part of efforts at the state level aimed at enhancing process safety management skills in hazardous industries. The drive emphasized the basics of PSM, gap analysis, safety culture, and implementing PSM through tools recommended by global authorities like OSHA and Center for Chemical Process Safety.

The market is highly fragmented but growing, owing to the growth of industries and lack of in-house capability in most firms, resulting in a high dependence on external sources and adoption of integrated training, consultancy & compliance programs as per frameworks like Center for Chemical Process Safety.

Competitive Landscape

- The market for global process safety services is characterized by an average consolidation within the competitive environment, where traditional TIC firms compete with leading industrial automation companies to offer complete safety solutions.

- SGS SA, Siemens AG, Intertek Group plc, Schneider Electric SE and Bureau Veritas SA together hold more than 54% market share. Market leaders are able to gain a competitive advantage due to their size, regulatory know-how, and capability of incorporating digital safety solutions within the industrial ecosystem.

- SGS SA and Intertek Group plc benefit from their global network of testing centers to offer superior safety auditing and safety certification services. On the other hand, Siemens AG and Schneider Electric SE thrive by offering safety services within their own hardware and software platforms.

- High-end participants such as Honeywell International Inc., ABB Ltd and DEKRA SE are able to create a niche for themselves through the provision of specialized safety services within critical industrial sectors including oil and gas, chemicals, and renewable energy initiatives.

- Leading firms such as Emerson Electric Co. and Rockwell Automation, Inc. have been expanding their presence in Europe and North America through their shift towards functional safety and cybersecurity safety services.

- Key players include SGS SA, Bureau Veritas SA, Intertek Group plc, DNV AS, DEKRA SE, TÜV SÜD AG, TÜV Rheinland AG, TÜV NORD GROUP, UL Solutions Inc., Lloyd’s Register Group Limited, RINA S.p.A., ABS Group of Companies, Inc., Applus+, Honeywell International Inc., Siemens AG, Emerson Electric Co., Yokogawa Electric Corporation, ABB Ltd, Schneider Electric SE, Worley Limited, Jensen Hughes, ioMosaic Corporation, BakerRisk, Rockwell Automation, Inc., Jacobs Solutions Inc., Fluor Corporation, KBR, Inc., AECOM, Becht Engineering Co., Inc., Aspen Technology, Inc., dss+ (dss+ Group), Sphera Solutions, Inc., John Wood Group PLC, JGC Holdings Corporation and Chiyoda Corporation

Key Developments

- March, 2026: ABB introduced improvements in its industrial control solutions (such as Symphony Plus DCS) and entered into a collaboration with NVIDIA to integrate digital twin within automation tools, focusing on the advancement of safety-oriented monitoring and prediction of operations in industrial processes and facilities.

- February 2026: DNV rolled out Industrial Services, transforming its inspection business line into a specialized quality control, inspection, and risk management services for highly sophisticated industrial and energy infrastructures.

- February 2026: DEKRA expanded its offerings in terms of process safety training through new courses on Process Safety Management, HAZOP Analysis, Chemical Reaction Hazard Safety, Functional Safety Training Program, and Electrostatic Ignition Risk Assessment for the development of competencies to mitigate operational risks.

- December 2025: ABB India launched the ACS380-E industrial drive for advanced machinery automation, featuring better connectivity, flexibility, and security capabilities, which contribute to industrial process automation.

- October 2025: Applus+ collaborated with Fuvex in applying long-distance drones for the monitoring of power installations, facilitating remote inspections, identification of hazards, and mitigation of risks in industrial sites.

Why Choose DataM?

- Technological Innovations: Explores the latest advancements in process safety services design, including improved hydraulic systems, advanced operator controls, telematics integration, electric and hybrid powertrains and enhanced attachment versatility that are driving higher productivity and lower operating costs across construction and industrial applications.

- Product Performance & Market Positioning: Evaluates how different OEMs perform in real-world construction, landscaping, agriculture and municipal environments. The analysis compares lifting capacity, breakout force, fuel efficiency, durability, operator comfort and attachment compatibility, highlighting how leading manufacturers differentiate themselves globally.

- Real-World Evidence: Highlights practical use cases of process safety Services across infrastructure development, road maintenance, warehouse handling and smart city projects. It demonstrates measurable improvements in jobsite efficiency, reduced labor dependency, faster material handling and optimized equipment utilization.

- Market Updates & Industry Changes: Tracks important industry developments such as new product launches, electrification initiatives, localized manufacturing expansions, tightening emission standards (Stage V, Tier 4 Final) and shifts in construction spending across major regions, including North America, APAC, China and India.

- Competitive Strategies: Analyzes how leading manufacturers are expanding their footprint through dealer network strengthening, localized production, electric model introductions, strategic partnerships and technology-driven differentiation such as AI-enabled monitoring and autonomous-ready platforms.

- Pricing & Market Access: Explains pricing structures across standard, high-capacity and electric skid steer models, including outright purchase, leasing and rental models. It also reviews regional availability, distribution networks and financing strategies that enhance market penetration.

- Market Entry & Expansion: Identifies growth opportunities in emerging economies driven by infrastructure development, urbanization, smart city programs and expanding rental ecosystems. It also outlines strategies for OEMs to scale operations globally through regional manufacturing hubs and after-sales service optimization.

Target Audience 2026

- Construction & Infrastructure Companies: EPC contractors, real estate developers, road construction firms and urban infrastructure agencies utilizing compact equipment for site preparation, excavation and material handling.

- Rental & Leasing Companies: Equipment rental providers expanding fleets to meet growing demand for compact, versatile machinery with high utilization rates.

- Agricultural & Landscaping Operators: Farm operators, orchard managers, landscaping firms and municipal maintenance departments using process safety Services for multipurpose operations.

- Government & Municipal Authorities: Public works departments, urban development authorities and smart city mission teams responsible for infrastructure upgrades and maintenance.

- OEMs & Equipment Manufacturers: Global and regional construction equipment manufacturers seeking competitive intelligence, innovation benchmarking and regional expansion strategies.

- Investors & Private Equity Firms: Investment groups tracking growth in construction equipment manufacturing, rental markets and electrification of compact machinery.

- Dealers & Distribution Networks: Authorized distributors, service providers and aftermarket suppliers involved in sales, financing, spare parts and maintenance services.