Polylactic Acid (PLA) Market Overview

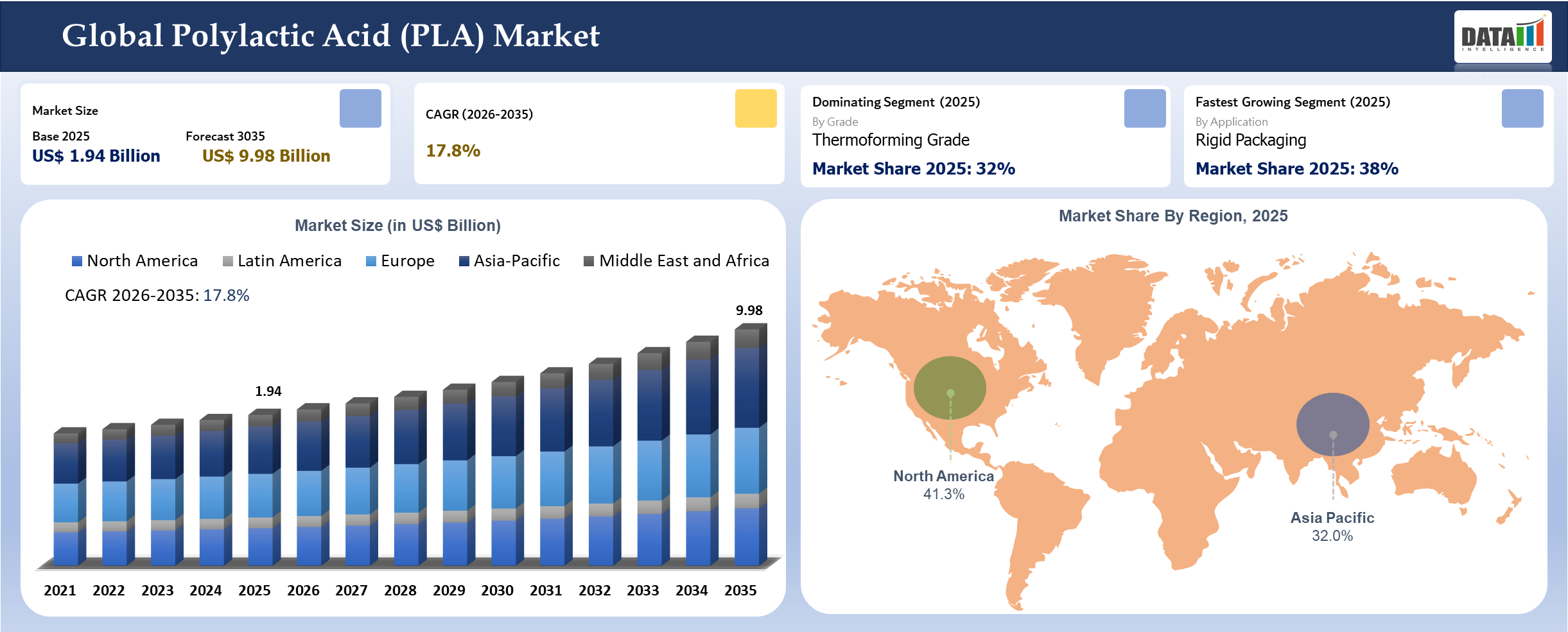

The global polylactic acid (PLA) market reached US$ 1.94 billion in 2025 and is expected to reach US$ 9.98 billion by 2035, growing with a CAGR of 17.8% during the forecast period 2026-2035. The reduction of GHG emissions through bioplastic production such as PLA can go as far as 25% to 70%, according to the International Energy Agency (IEA). Furthermore, there is an increase in the production capacity of bioplastics such as PLA due to the ban on single-use plastics and EPR policy, as stated by European Bioplastics. However, the policy of the government plays a major role in encouraging the use of PLA today. It can be seen in the Circular Economy Action Plan, introduced by the European Commission, whereby the development of bio-based and biodegradable materials in packaging has been prioritized.

The restriction of some single-use plastics by the government of India has encouraged the utilization of alternative products, such as PLA packaging material, in the food service and retail sector. The USDA Bio Preferred Program has been engaging itself in promoting the utilization of bio-based products using different strategies. Poly-lactic acid is gaining momentum due to increased trends regarding policies related to the environment and circular economy, resulting in the transition of plastics from being non-renewable. The acid is obtained from the use of biological materials including corn starch and sugarcane. Poly-lactic acid finds great demand for usage in various sectors such as packaging and textiles because of its biodegradable properties.

Polylactic Acid (PLA) Industry Trends and Strategic Insights

- Europe remains the most influential region for demand creation and competitive benchmarking in the current market structure.

- Rigid Packaging is the most commercially important segment because it aligns with current buying behavior, installed base requirements and near term scaling feasibility.

- The strongest growth trigger is brand owner demand for compostable and bio based packaging materials, while the main execution risk is price premium versus fossil based polymers and inconsistent composting infrastructure.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 1.94 Billion | |

| 2035 Projected Market Size | US$ 9.98 Billion | |

| CAGR (2026-2035) | 17.8% | |

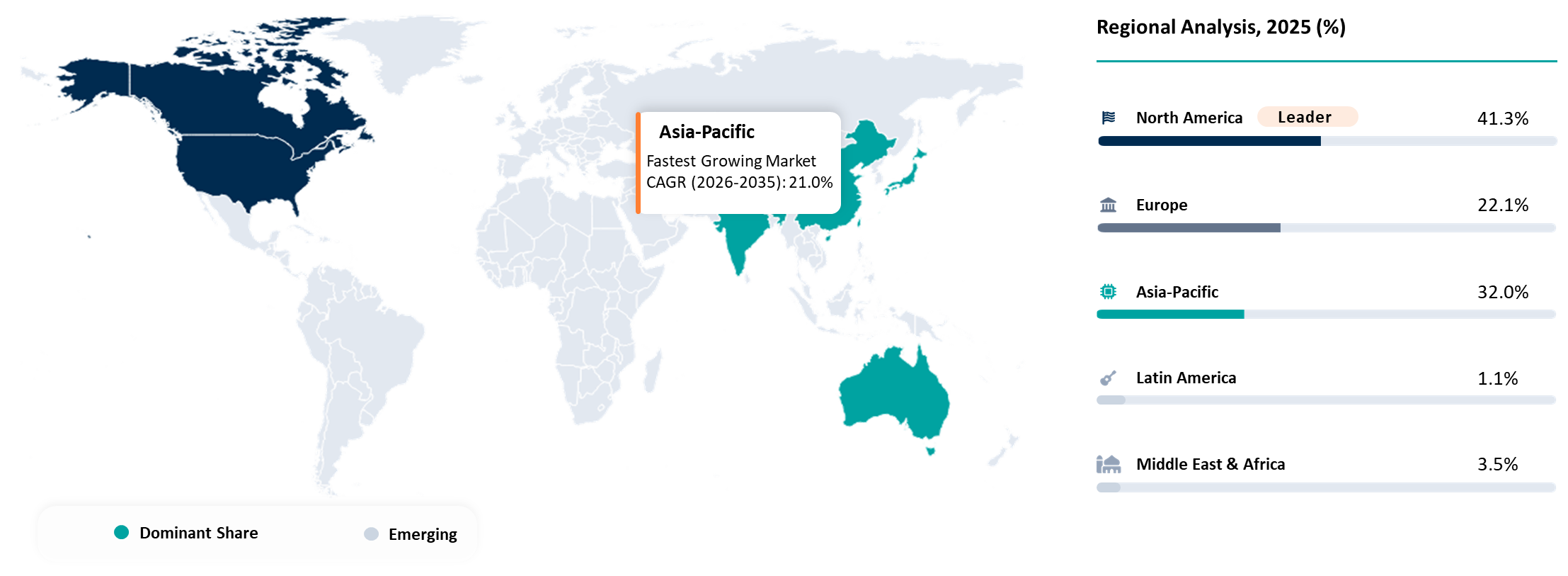

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Grade | Thermoforming Grade, Injection Molding Grade, Extrusion Grade, Fiber Grade, Film Grade Medical Grade | |

| By Raw Material | Corn Starch, Sugarcane, Cassava, Sugar Beet, Other Fermentable Feedstocks | |

| By Form | Pellets, Filament, Sheets and Films, Fibers, Powder | |

| By Processing Technology | Injection Molding, Blow Molding, Extrusion, Thermoforming, 3D Printing, Spinning | |

| By Application | Rigid Packaging, Flexible Packaging, Food Service, Fibers and Textiles, Agriculture, Biomedical, 3D Printing | |

| By End-User | Packaging, Consumer Goods, Agriculture and Horticulture, Textile, Healthcare, Automotive and Electronics | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

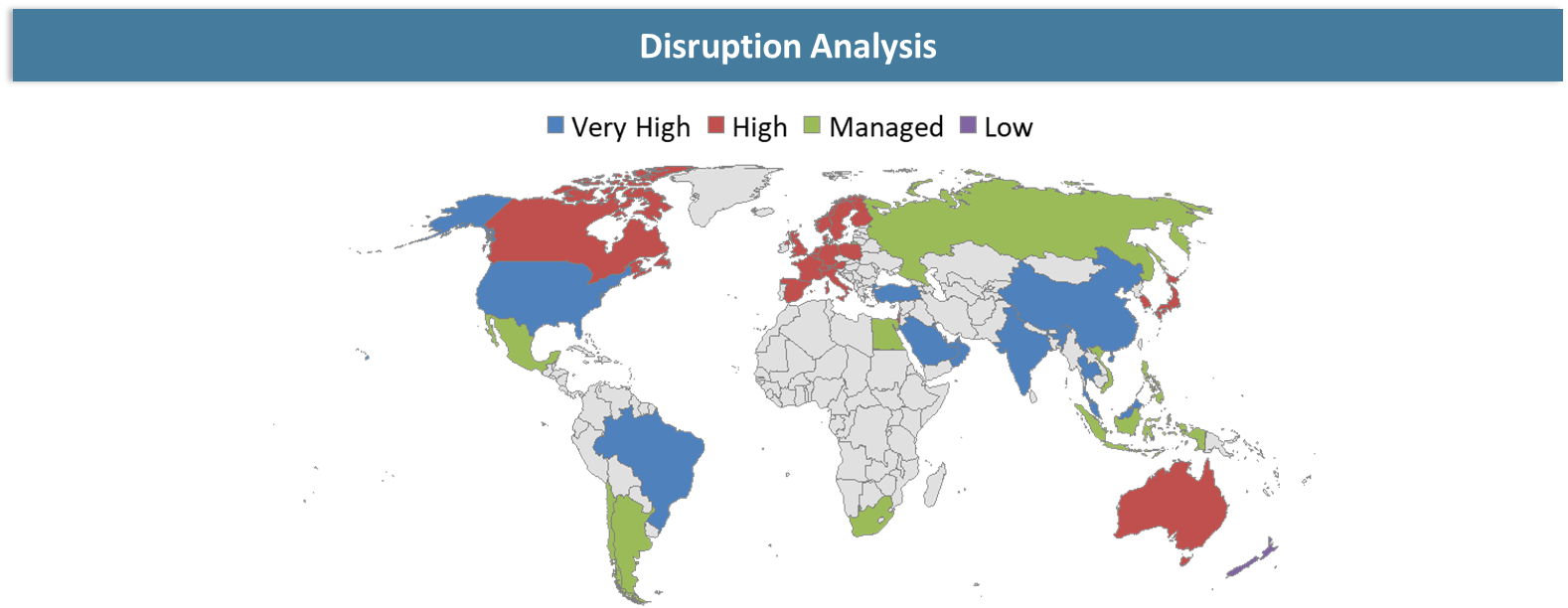

Disruption Analysis

Regulatory bans on conventional plastics across regions are accelerating PLA adoption, fundamentally reshaping demand patterns in packaging and consumer goods. Advancements in polymer engineering, including improved heat resistance and mechanical strength, are expanding PLA’s applicability into durable goods and industrial uses. However, disruptions also arise from cost volatility of feedstocks such as corn and sugarcane, impacting price competitiveness versus fossil-based plastics.

Emerging biopolymers like PHA and PBS pose competitive threats, potentially eroding PLA’s market share in specific applications. Supply chain localization and investments in large-scale biorefineries are transforming production economics, enabling economies of scale. Evolving recycling infrastructure and compostability standards are redefining end-of-life considerations. The disruptions are shifting PLA from a niche sustainable material toward a mainstream industrial polymer, while intensifying competition and innovation cycles.

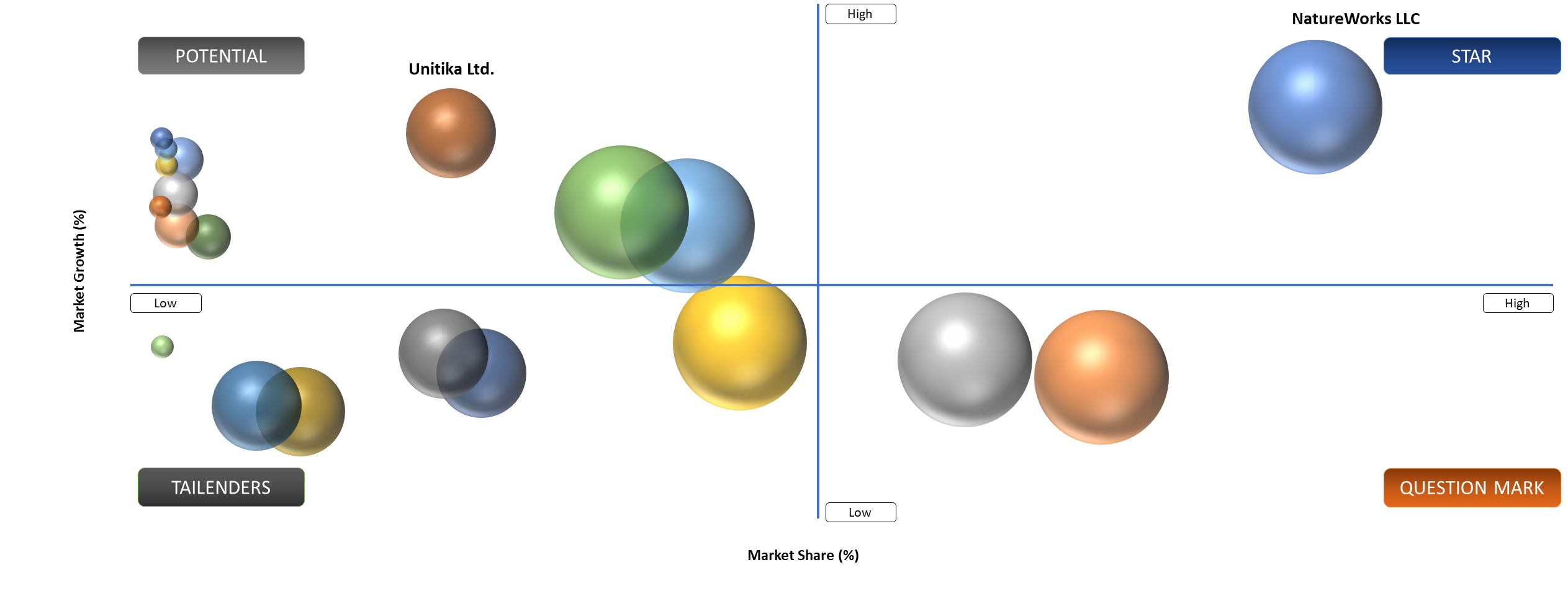

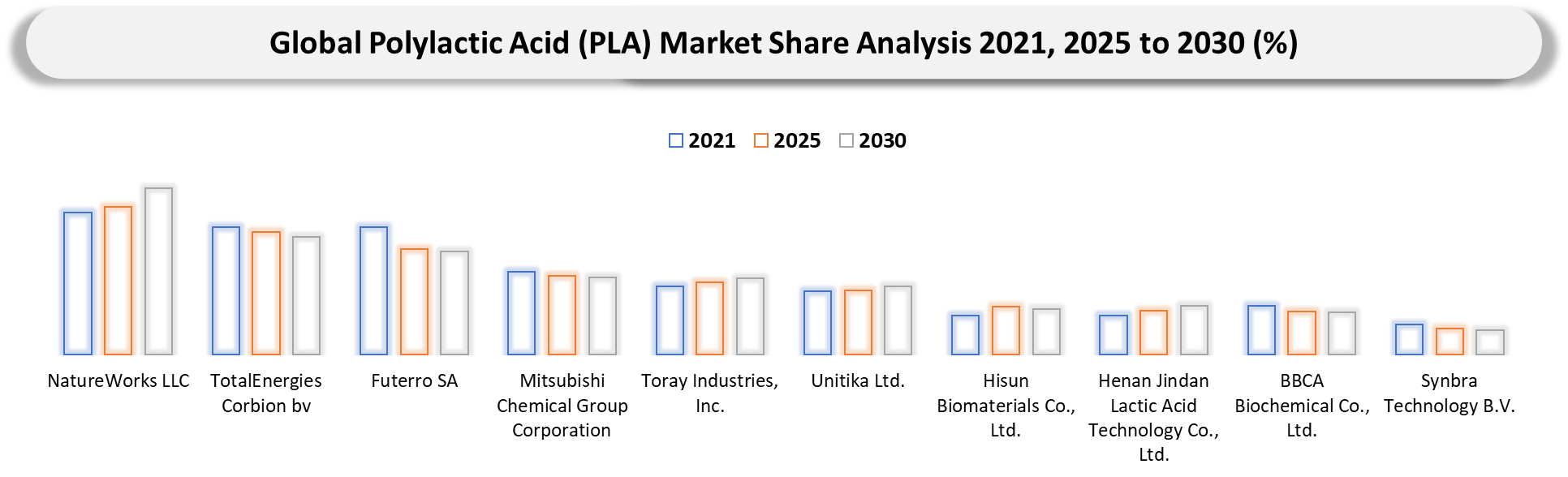

BCG Matrix: Company Evaluation

In BCG terms, the most likely Stars in the polylactic acid market are vendors that combine visible revenue momentum with a strong technology or channel position. The lead group includes NatureWorks LLC, TotalEnergies Corbion bv and Futerro SA because these companies influence product standards, customer qualification cycles and investment direction.

Market Dynamics

Brand owner demands compostable and bio-based packaging materials

The use of traditional petroleum-based plastic products is being substituted with innovative materials, such as polylactic acid, which uses renewable feedstocks, including corn starch and sugarcane and emits less carbon dioxide than their traditional counterparts. Consumers have shown a preference for compostable products in the food and beverage industry, thus increasing the adoption rates in this domain. In the Global Polylactic Acid (PLA) Market, one of the major factors responsible for driving growth is the availability of compostable products using PLA, enabling the adoption of circular economic models. Moreover, brands promote the renewable nature of PLA and its capability to reduce greenhouse gases (by up to 50%-70%) in comparison to other products, thus contributing towards the sustainability narrative.

Price premium versus fossil-based polymers and inconsistent composting infrastructure

While PLA may be a bio-based and biodegradable polymer, it is also subject to a hefty premium compared to traditional polymers such as polyethylene and polypropylene that are made from fossil sources, due to the energy-intensive manufacturing process and variable cost of the agricultural raw materials used for production, making PLA between 20% and 50% more expensive. It poses a hurdle in the expansion of PLA into price-sensitive applications, including packaging and consumer goods. On another note, the green credentials of PLA are hampered by the lack of composting facilities available to enable degradation under controlled composting conditions. However, only about 30% of places around the world have access to this facility, resulting in improper disposal of PLA products in landfills and recycling streams.

Segmentation Analysis

The global polylactic acid (PLA) market is segmented based on the grade, raw material, form, processing technology, application, end-user and region.

Packaging Applications Still Decide Where PLA Converts into Real Demand

The rigid packaging category remains the most approachable segment since converters can utilize the material in consumer-focused applications that allow them to easily promote their biobased position and their industrial composability message. Therefore, cups, trays, clamshells and service ware have emerged as the ideal playgrounds for PLA introduction.

The need for rigid packaging has become less a matter of consumer preference and more of one of regulatory compliance. As debates continue to unfold in Europe regarding compostable plastics, consumers will grow more selective in determining when PLA use is necessary, opting for instances where there is a clear means of disposal. From a business perspective, the rigid packaging classification enjoys the benefit of ease in making decisions. It is up to the brand owner to consider aesthetics, rigidity, printability and renewability before deciding if PLA could have an edge over its competitors.

Geographical Penetration

Europe Leads Industrial Carousel Market Evolution Through Precision Engineering, Regulatory Discipline and Application-Specific Innovation

In Europe, PLA retains its highest priority since regulation, packaging development and end-of-life issues are currently being developed at the highest commercial level. Consumers in the region have become disillusioned with mere 'bio-based' marketing claims and are looking for an exact fit between material properties, end-of-life options and regulatory language.

Another factor contributing to the relevance of Europe as a PLA market is the skill of converters. European packaging manufacturers are testing combinations, coatings and material structures tailored to specific applications, thus taking PLA beyond the realm of simple replacement and into engineering applications. Finally, there is the discipline of legislation. The guidelines set by the EU regarding biobased, biodegradable and compostable plastics are forcing the market to determine where PLA is useful and where it could be misleading.

Germany Polylactic Acid (PLA) Market Outlook

Germany represents an essential PLA market due to the intersection of material advancements, innovations in packaging design and regulations. The country wields significant influence on purchasing practices within Europe, particularly when converters and brand owners require assurance that performance claims can survive regulatory assessment. In Germany, PLA purchases are not driven by general green marketing, but rather by practical applications of the technology. Buyers are concerned with the integration of PLA into current recycling networks and converting facilities, as well as its ability to provide a sustainable alternative to legacy products. Labor and productivity considerations also play a role in the German PLA market. The conversion of materials to finished goods relies on production lines, which makes reliability in the production process highly desirable for converters.

Italy Polylactic Acid (PLA) Market Trends

Italy is a key market for compostable packaging since the latter holds unique significance in the nation, culturally and commercially speaking, especially when it comes to organics collection-related foodservice applications and controlled-use formats. The Italian market has traditionally been more receptive to stories on composability than most of its competitors. Demand for packaging in Italy usually considers PLA and other bioplastics as a factor in consumer behavior about municipal waste, as opposed to environmentally friendly marketing angles. In the area where organic collection and food contact materials overlap, the plastic material finds its true calling from a business perspective.

Competitive Landscape

- The competitive landscape is led by a mix of global leaders and focused specialists, with NatureWorks LLC, TotalEnergies Corbion BV, Futerro SA and Mitsubishi Chemical Group Corporation shaping category standards. Market positioning depends on portfolio breadth, application depth, route to market strength and the ability to support customers after the initial sale.

- The strongest companies are using product upgrades, partnerships, regional manufacturing and selective vertical focus to defend share. As the market matures, leadership is likely to concentrate further around suppliers that can translate technical capability into faster commercialization and stronger customer retention.

Key Developments

- April 2026: Futerro SA strengthened its global PLA expansion roadmap, supporting large-scale polylactide capacity growth aligned with rising packaging and textile demand.

- March 2026: TotalEnergies Corbion bv expanded PLA commercialization strategy, focusing on circular bioplastics and advanced recycling integration across European packaging applications.

- January 2026: Mitsubishi Chemical Group Corporation accelerated bio-based polymer portfolio integration, enhancing PLA-based sustainable materials for automotive and electronics sectors.

- September 2025: Henan Jindan Lactic Acid Technology Co., Ltd. strengthened lactic acid integration for PLA production, improving upstream efficiency and supporting biodegradable plastics market expansion.

- August 2025: Hisun Biomaterials Co., Ltd. increased PLA production capacity in China, focusing on cost competitiveness and large-scale supply for packaging and 3D printing industries.

- July 2025: BBCA Biochemical Co., Ltd. expanded fermentation-based lactic acid output to support PLA manufacturing growth and enhance bio-based polymer supply chains globally.

- June 2025: Unitika Ltd. expanded its biomass plastic product line, integrating PLA into textile fibers to meet sustainability requirements in apparel and industrial materials markets.

- March 2025: Toray Industries, Inc., advanced development of high-performance PLA fibers targeting durable textile and industrial applications with improved mechanical properties.

February 2025: NatureWorks LLC announced a joint venture with Cargill to build a next-generation fermentation facility, strengthening PLA feedstock supply chain globally.

Why Choose DataM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

Target Audience 2026

- Packaging & Consumer Goods Companies: FMCG manufacturers, food & beverage brands and sustainable packaging firms adopting PLA for biodegradable and compostable packaging solutions.

- Bioplastics Manufacturers & Compounders: Producers of PLA resins, blends and compounds focusing on innovation, cost optimization and performance enhancement for diverse applications.

- Agriculture & Horticulture Operators: Farm owners, greenhouse operators and agro-based companies utilizing PLA-based films, mulch sheets and biodegradable agricultural inputs.

- Healthcare & Biomedical Companies: Medical device manufacturers, pharmaceutical firms and biotech companies leveraging PLA for applications such as sutures, implants and drug delivery systems.

- Textile & Fiber Manufacturers: Apparel brands, nonwoven fabric producers and industrial textile companies integrating PLA fibers for sustainable and eco-friendly product lines.

- Government & Regulatory Authorities: Environmental agencies, sustainability councils and policymakers promoting bioplastics adoption through regulations, bans on single-use plastics and circular economy initiatives.

- OEMs & Product Manufacturers: Companies in 3D printing, electronics and consumer goods sectors using PLA as a preferred material for prototyping and end-use applications.

- Investors & Private Equity Firms: Investment entities tracking growth in the bioplastics sector, sustainable materials innovation and circular economy-driven business models.

- Distributors & Supply Chain Participants: Raw material suppliers, distributors and logistics providers supporting PLA market penetration across global and regional markets.