AI Accelerator Chip Market Overview

AI Accelerator Chips are powering the next wave of AI innovation. As demand for generative AI, AI data centers, and high-performance computing surges, which companies will dominate this multi-billion-dollar market? Growth the trends, opportunities, and competitive strategies driving growth.

Global governments are making unprecedented investments to secure AI hardware leadership, positioning AI accelerator chips as a cornerstone of future digital economies. In 2025, the US awarded US$ 458 million to SK hynix through the CHIPS and Science Act to establish advanced HBM memory manufacturing and R&D in Indiana, while Samsung secured a US$ 4.74 billion grant for semiconductor fabrication in Texas. China’s Phase III National Integrated Circuit Fund committed ¥344 billion (US$ 47.5 billion) to AI chip and semiconductor advancements. These large-scale public funding programs are expanding manufacturing capacity, reducing foreign dependency, and driving innovation pipelines across AI-specific chip architectures.

Key Takeaways – AI Accelerator Chip Market

- Asia-Pacific accounted for approximately 41.2% of the AI Accelerator Chip Market in 2025 and is expected to register the fastest CAGR through 2035. The region’s growth is being driven by aggressive investments in AI infrastructure, rapid expansion of hyperscale data centers, government-backed semiconductor initiatives, and increasing adoption of generative AI across China, Japan, South Korea, India, and Southeast Asia.

- North America held around 38.5% market share in 2025, supported by the presence of leading AI chip developers, cloud service providers, and technology companies. Large-scale investments in AI training clusters, high-performance computing (HPC), and enterprise AI deployment continue to strengthen regional demand for advanced accelerator chips.

- The competitive landscape is shifting from traditional GPU dominance toward a broader ecosystem of specialized AI accelerators. Custom AI chips, tensor processing units (TPUs), neural processing units (NPUs), and application-specific integrated circuits (ASICs) are gaining traction as organizations seek higher performance and lower power consumption for AI workloads.

- Generative AI is becoming the primary catalyst for accelerator chip demand. The rapid growth of large language models (LLMs), multimodal AI systems, AI copilots, and autonomous AI agents is significantly increasing computing requirements across cloud and enterprise environments.

- Hyperscale cloud providers are increasingly developing proprietary AI accelerators to reduce dependence on third-party suppliers and optimize AI infrastructure costs. Custom silicon strategies are becoming a key competitive differentiator among cloud platforms.

- Energy efficiency has emerged as a critical purchasing criterion. As AI training and inference workloads consume substantial electricity, organizations are prioritizing accelerator architectures that deliver greater performance per watt while reducing total cost of ownership.

- AI accelerator deployment is expanding beyond cloud data centers into edge computing environments. Industries such as automotive, healthcare, manufacturing, telecommunications, retail, and robotics are adopting AI chips for real-time inference, computer vision, predictive analytics, and autonomous decision-making applications.

- Supply chain resilience and semiconductor sovereignty have become strategic priorities. Governments across the United States, Europe, China, Japan, South Korea, and India are investing heavily in domestic semiconductor manufacturing and advanced packaging capabilities to secure AI chip supply.

AI Accelerator Chip Market Trend

A defining trend is the alignment of national industrial policy with AI edge and cloud hardware innovation. The US Department of Commerce has already disbursed over US$ 19 billion of the CHIPS for America program’s funding to accelerate AI chip ecosystem growth. China’s “Big Fund” Phase III is targeting cutting-edge fabrication nodes to capture a greater share of AI accelerator chip production.

Samsung’s Texas expansion is projected to create 12,000 construction jobs and 3,500 manufacturing roles, demonstrating AI chipmaking’s direct economic impact. SK hynix’s Indiana facility, integrated with Purdue University’s R&D network, will boost HBM supply for high-performance AI workloads. This synchronized push shows that government-backed AI chip manufacturing hubs are becoming the new global competitive battleground.

AI Accelerator Chip Market Scope

| Metrics | Details |

| By Processing Type | Cloud, Edge |

| By Chip Type | Graphics Processing Unit (GPU), Application-Specific Integrated Circuit (ASIC), Field-Programmable Gate Array (FPGA), Central Processing Unit (CPU), Others |

| By Technology | Natural Language Processing (NLP), Computer Vision, Network Security, Others |

| By End-User | Consumer Electronics, Automotive, Healthcare, IT & Telecom, Retail, Others |

| By Region | North America, South America, Europe, Asia-Pacific and Middle East and Africa |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth |

For more details on this report - Request for Sample

AI Accelerator Chip Market Dynamics

Rising Integration of AI Accelerator Chips in Edge Devices for Real-Time Processing

The integration of AI accelerator chips into edge devices is revolutionizing real-time data processing. For instance, the US Department of Energy's Fermilab has developed real-time edge AI systems that enhance the efficiency of particle accelerators by processing data locally, reducing latency and improving operational accuracy . Similarly, MIT researchers have introduced a photonic processor capable of performing deep learning tasks at the speed of light, enabling edge devices to analyze data in real-time with minimal energy consumption . These advancements underscore the growing reliance on edge AI accelerators to meet the demands of time-sensitive applications across various sectors.

Supply Chain Vulnerabilities in Advanced Semiconductor Manufacturing Nodes

The global semiconductor supply chain faces significant vulnerabilities, particularly in advanced manufacturing nodes. The Organization for Economic Co-operation and Development (OECD) reports that the top five semiconductor-producing economies account for approximately three-quarters of global semiconductor value added. This high concentration means that disruptions in any of these key regions can have widespread effects on global supply. Additionally, the semiconductor industry is highly upstream, meaning that any disruptions can impact a broad range of industries that rely on semiconductors, including information and communications technology (ICT), electronics, and automotive sectors.

AI Accelerator Chip Market Segment Analysis

The global AI accelerator chip market is segmented based on processing type, chip type, technology, end-user and region.

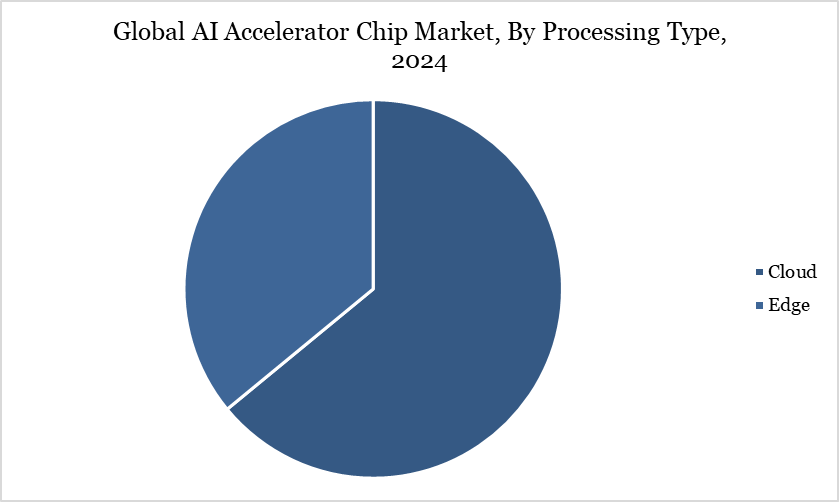

Cloud Segment Driving AI Accelerator Chip Market

The cloud processing segment is the primary driver of growth in the global AI accelerator chip market. In 2024, it accounted for approximately 55% of the market revenue. This dominance is attributed to the increasing demand for high-performance computing capabilities required to support AI workloads in data centers. Hyperscale cloud providers such as Google, Amazon Web Services (AWS), and Microsoft are at the forefront of this trend, investing heavily in AI infrastructure to meet the needs of AI-driven applications. For instance, Cisco reported receiving over US$2 billion in AI infrastructure orders in fiscal 2025, more than double its initial expectations, driven by increased investments from major cloud providers.

Why AI Accelerator Chip Market Matters in 2026

The global artificial intelligence industry is entering a new phase of accelerated computing demand.

AI accelerator chips are becoming the foundation of modern AI infrastructure by enabling faster model training, lower inference latency, improved energy efficiency, and scalable deployment of generative AI, machine learning, and high-performance computing applications.

Several macroeconomic and technological factors are driving market growth:

- Growing demand for large language models (LLMs) and foundation models

- Expansion of hyperscale data centers worldwide

- Rising investments in AI cloud infrastructure

- Increasing deployment of edge AI applications

- Growing demand for high-performance computing (HPC) solutions

- Advancements in semiconductor manufacturing technologies

- Government initiatives supporting domestic semiconductor production

- Increasing focus on energy-efficient AI processing architectures

Analyst View

DataM Intelligence Analyst Perspective

The AI accelerator chip market is evolving from a specialized computing segment into a critical pillar of the global digital economy.

The long-term success of the AI accelerator chip market will depend on:

- Semiconductor manufacturing advancements

- AI model complexity and scalability requirements

- Power efficiency improvements

- Supply chain resilience and chip availability

- Data center expansion strategies

- Edge AI deployment growth

- Software-hardware ecosystem optimization

- Strategic partnerships across semiconductor and cloud industries

The United States continues to lead AI chip innovation through strong investments in advanced semiconductor design, cloud computing, and AI research. China is accelerating domestic AI chip development to strengthen technological self-sufficiency and reduce dependence on foreign suppliers. Japan and South Korea remain key players through advanced semiconductor manufacturing capabilities and strategic investments in next-generation chip technologies. India is emerging as a promising AI accelerator market, driven by digital transformation initiatives, expanding data center investments, government-backed semiconductor programs, and increasing enterprise adoption of AI solutions.

AI Accelerator Chip Market Geographical Share

North America Drives the Global AI Accelerator Chip Market

North America led the global AI accelerator chip market with a substantial revenue share of approximately 30% in 2024. The United States, in particular, is at the forefront of this sector, driven by robust investments from both government and private entities. The U.S. Department of Energy (DOE) has been instrumental in advancing AI chip technologies.

For instance, in December 2024, the DOE announced a US$ 285 million award to establish a CHIPS Manufacturing USA Institute, aiming to bolster domestic semiconductor manufacturing capabilities. Additionally, the DOE has allocated $68 million to support 11 multi-institution projects focused on developing AI models for scientific research

Major deployment hubs include:

- Silicon Valley

- Austin

- Seattle

- Phoenix

- Santa Clara

Asia-Pacific AI Accelerator Chip Market

Asia-Pacific is expected to register the fastest CAGR during the forecast period.

China leads regional expansion through aggressive investments in AI semiconductor development, data center infrastructure, and government-backed AI initiatives.

Japan, South Korea, and Taiwan are rapidly strengthening their AI chip ecosystems through advanced semiconductor manufacturing capabilities and strategic investments.

India represents a major future growth opportunity due to:

- Expansion of AI data centers

- Government semiconductor incentive programs

- Growing AI startup ecosystem

- Increasing enterprise AI adoption

Europe AI Accelerator Chip Market

Europe is witnessing growing adoption supported by increasing investments in AI sovereignty, high-performance computing infrastructure, and semiconductor innovation.

Germany, France, and the United Kingdom are leading AI accelerator deployment across manufacturing, automotive, healthcare, and research sectors.

The Netherlands and Ireland are emerging as important markets due to expanding cloud infrastructure and semiconductor investments.

Latin America AI Accelerator Chip Market Outlook

Latin America is gradually increasing AI infrastructure investments as enterprises accelerate digital transformation and cloud adoption.

Brazil, Mexico, and Chile are emerging as key markets driven by growing demand for AI-powered analytics, financial services, and enterprise automation applications.

Middle East & Africa AI Accelerator Chip Market Outlook

The Middle East & Africa region is expected to create significant long-term opportunities through national AI strategies, smart city projects, and digital economy initiatives.

The UAE and Saudi Arabia are actively investing in AI data centers, sovereign AI platforms, and advanced computing infrastructure, positioning themselves as regional AI innovation hubs.

South Africa is also witnessing increased adoption of AI technologies across financial services, telecommunications, and public sector applications.

Technological Advancement Analysis

The global AI accelerator chip market is experiencing significant technological advancements, driven by both private sector innovation and public sector initiatives. Companies like Intel and AMD are at the forefront, with Intel's Gaudi 3 chip offering 40% improved power efficiency and 50% faster inference speeds compared to its predecessor, the H100 GPU. Similarly, AMD's MI450 chip is poised to challenge Nvidia's dominance with its upcoming MI400 series, particularly the MI450, marking AMD's first rack-scale AI server platform.

The advancements are complemented by government-backed initiatives such as the US CHIPS and Science Act, which provides US$ 50 billion to bolster semiconductor research and manufacturing, aiming to enhance the nation's position in AI hardware development. Additionally, the US Department of Energy's AI testbeds are facilitating the exploration of novel hardware, software, and algorithms to accelerate AI capabilities. These combined efforts are propelling the AI accelerator chip market toward more efficient, powerful, and scalable solutions, meeting the growing demands of AI applications across various sectors.

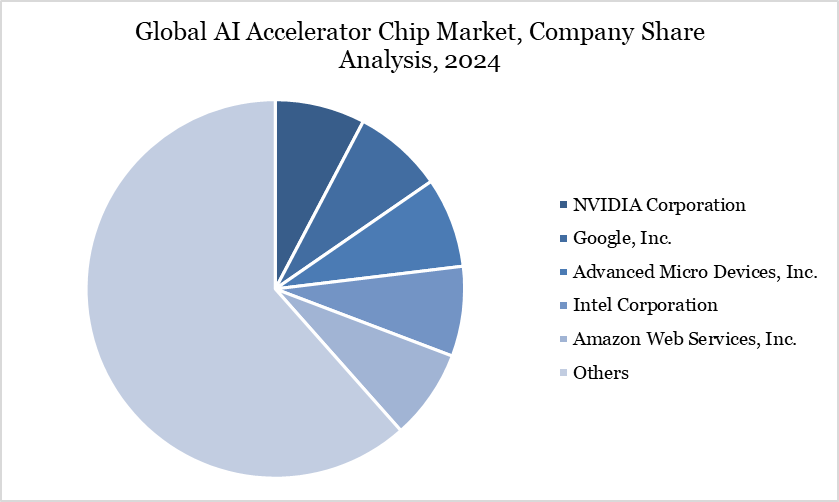

AI Accelerator Chip Market Competitive Landscape

The major global players in the market include NVIDIA Corporation, Google Inc., Advanced Micro Devices Inc., Intel Corporation, Amazon Web Services Inc., Huawei Technologies Co. Ltd., Cerebras Systems Inc., Graphcore Limited, Qualcomm Incorporated, and SambaNova Systems Inc.

Key Developments

- On April 27, 2026, Cadence Design Systems raised its annual revenue forecast following strong demand for AI chip design tools, driven by increasing investments from major technology companies such as NVIDIA, Google, and Amazon. The company also completed the acquisition of Hexagon AB’s design and engineering division, strengthening its capabilities in AI-driven chip development and simulation technologies.

- On April 1, 2026, reports indicated that Chinese AI chipmakers significantly expanded their market presence, capturing around 41% of the domestic AI accelerator server market, intensifying competition against global leaders like NVIDIA. This shift reflects growing regional innovation and supply chain diversification in the AI accelerator ecosystem.

- On June 12, 2025, Advanced Micro Devices unveiled its next-generation AI accelerator platform and open AI ecosystem strategy, introducing scalable rack-level infrastructure designed to compete with leading GPU-based AI systems and support large-scale generative AI workloads.

- On October 27, 2025, Qualcomm Technologies announced the launch of new AI accelerator chips (AI200 and AI250 series) targeting data center applications, marking its strategic entry into the high-performance AI infrastructure market and intensifying competition with established players.

- On September 18, 2025, NVIDIA announced a $5 billion strategic investment in Intel Corporation to co-develop advanced AI computing platforms integrating CPUs and GPUs. This collaboration represents a significant industry consolidation move aimed at accelerating next-generation AI accelerator architectures.

- On August 2025, Advanced Micro Devices expanded its AI capabilities through acquisitions of AI software and compiler startups, including Brium, and by onboarding engineering talent from Untether AI. These moves enhance AMD’s AI accelerator performance optimization and strengthen its competitive position in inference and data center markets.

- On April 2025, Tenstorrent introduced its Blackhole series AI accelerators featuring advanced RISC-V architecture and high-performance tensor processing capabilities, targeting next-generation AI workloads and data center applications.

AI Accelerator Chip Market Investment & Funding Analysis

Global investments in AI computing infrastructure continue to increase significantly.

Major funding areas include:

- AI accelerator chip development

- Data center AI infrastructure

- High-bandwidth memory (HBM) technologies

- Edge AI processors

- Generative AI hardware platforms

- Advanced semiconductor manufacturing

- Chiplet architecture innovation

- AI cloud computing infrastructure

Strategic Recommendations

For Semiconductor Manufacturers

- Increase investment in advanced AI chip architectures

- Expand partnerships with hyperscale cloud providers

- Strengthen packaging and manufacturing capabilities

For Investors

- Focus on high-growth AI hardware innovators

- Monitor AI infrastructure spending trends

- Evaluate long-term demand from generative AI workloads

For Governments

- Support domestic semiconductor manufacturing initiatives

- Strengthen AI and chip R&D programs

- Develop resilient semiconductor supply chains

Why Buy This AI Accelerator Chip Market Report?

This report helps organizations:

- Understand future AI hardware trends

- Identify high-growth investment opportunities

- Benchmark competitors effectively

- Analyze technology adoption patterns

- Optimize market entry strategies

- Evaluate emerging AI chip innovations

- Assess regional growth potential

- Track next-generation computing developments

What’s Included in the AI Accelerator Chip Market Report?

The report provides:

- Market size & forecast analysis

- Regional growth outlook

- Competitive intelligence

- Technology benchmarking

- Pricing analysis

- Supply chain assessment

- Market share analysis

- Investment landscape analysis

- Strategic recommendations

- Emerging trends analysis

- Company profiling

- Demand and adoption analysis

Who Should Buy This Report?

This AI Accelerator Chip Market report is ideal for:

- Semiconductor manufacturers

- AI accelerator chip developers

- Cloud service providers

- Data center operators

- Technology companies

- Venture capital firms

- Institutional investors

- Electronics manufacturers

- Research institutions

- Government agencies

- Market intelligence teams

- System integrators

Key Benefits for Stakeholders

Gain actionable market intelligence:

- Understand future AI computing disruptions

- Analyze global semiconductor investment trends

- Evaluate AI hardware innovation strategies

- Identify strategic growth opportunities

- Benchmark market competitors

- Improve investment decision-making

- Assess evolving AI infrastructure demand

- Monitor next-generation chip technology developments

- Understand regional competitive dynamics

- Support long-term business planning and expansion strategies

Related Reports

The AI Accelerator Chip Market is closely connected to broader advancements in artificial intelligence infrastructure, high-performance computing, cloud data centers, and next-generation semiconductor technologies. As enterprises accelerate AI adoption and demand greater computing efficiency, specialized accelerator chips are becoming critical for training, inference, and real-time AI workloads. Explore the following related reports for deeper insights into the technologies shaping the future of AI computing.

Photonic AI accelerators market are emerging as a transformative technology for next-generation artificial intelligence systems by leveraging light-based computing to achieve higher processing speeds and lower energy consumption. As AI models become increasingly complex, photonic architectures are gaining attention for their ability to overcome the performance and power limitations of conventional electronic processors, enabling faster and more efficient AI workloads.

Data center accelerators market play a crucial role in optimizing AI training, machine learning, deep learning, analytics, and high-performance computing applications. With hyperscale cloud providers and enterprises investing heavily in AI infrastructure, accelerator technologies such as GPUs, TPUs, FPGAs, and custom AI processors are becoming essential for improving computational efficiency, reducing latency, and supporting large-scale AI deployments.

AI training chip market are specifically designed to handle the intensive computational requirements of training advanced neural networks and foundation models. The growing adoption of generative AI, large language models (LLMs), and enterprise AI applications is driving demand for high-performance training processors that deliver enhanced parallel processing capabilities, memory bandwidth, and scalability across data center environments.

Quantum chip market represent the next frontier in computing innovation, enabling quantum systems to perform complex calculations beyond the capabilities of classical processors. Advances in superconducting, trapped-ion, photonic, and other quantum architectures are accelerating research and commercial development, creating new opportunities for optimization, cryptography, materials science, and future AI computing applications.