Pharma Cloud Services Market Size and Growth

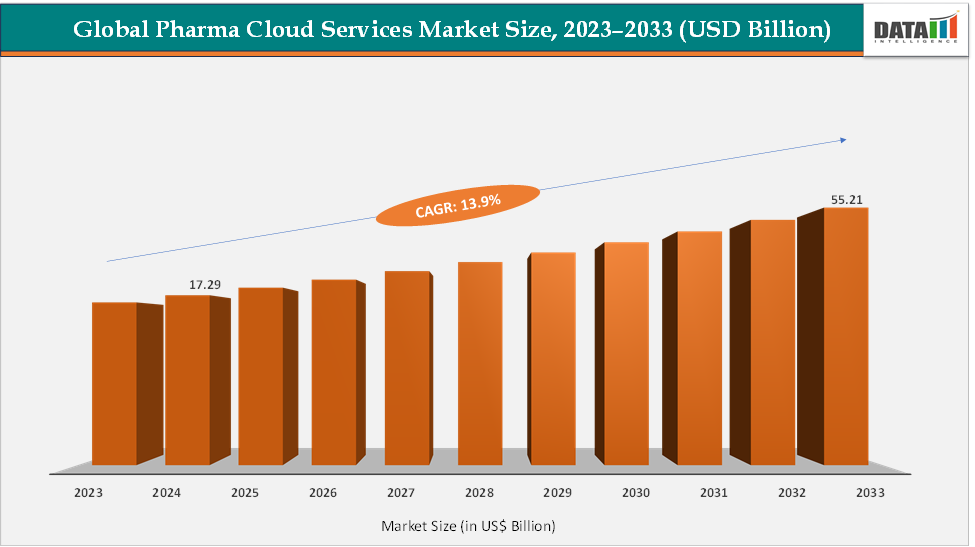

The Pharma Cloud Services Market will reach US$ 22.43 billion in 2026, up from US$ 19.69 billion in 2025, and is projected to reach US$ 80.98 billion by 2035, registering strong growth at a CAGR of 13.9% during the forecast period from 2026 to 2035.

The market is experiencing rapid growth as pharmaceutical and biotech companies increasingly adopt cloud technologies to enhance R&D productivity, clinical trial efficiency, and regulatory compliance. Driven by rising data volumes from genomics, AI-driven drug discovery, and remote trials, cloud platforms such as AWS, Microsoft Azure, and Veeva enable secure, scalable, and GxP-compliant operations. The market’s momentum is further fueled by the shift toward hybrid cloud models, ensuring data sovereignty and compliance with global regulations like GDPR and FDA 21 CFR Part 11. Overall, cloud adoption is transforming pharma operations into agile, data-centric ecosystems that accelerate innovation and reduce time-to-market.

Key Takeaways

- North America accounted for 44.27% of the global Pharma Cloud Services Market share in 2025, driven by advanced digital infrastructure, increasing adoption of cloud-based drug development platforms, and stringent regulatory frameworks supporting digital transformation initiatives across pharmaceutical operations.

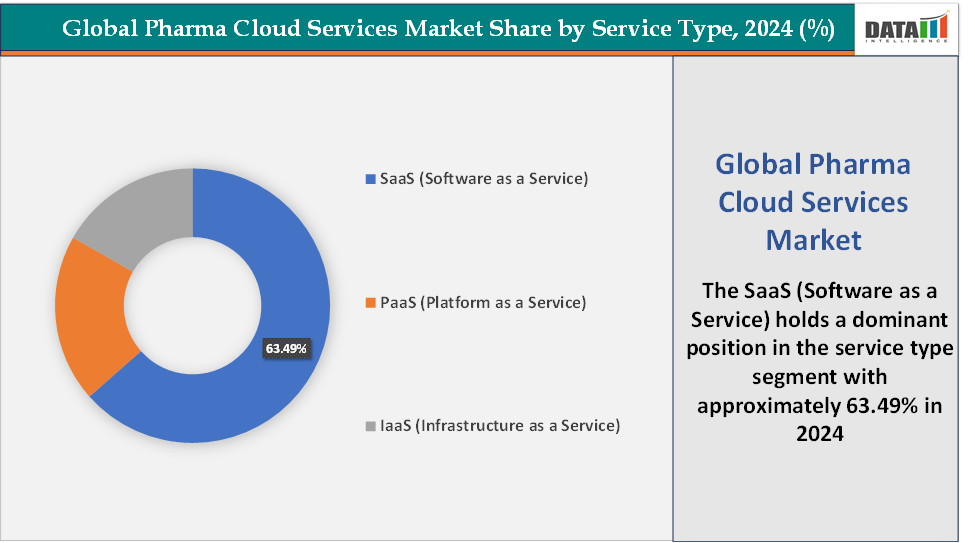

- The Software as a Service (SaaS) segment dominated the market with a 63.49% revenue share in 2025, owing to its scalability, cost-efficiency, and growing adoption across pharmacovigilance, clinical data management, regulatory compliance, and drug development applications.

- Pharmaceutical and biotechnology companies contributed approximately 48-52% of the overall market demand in 2025, supported by increasing investments in AI-driven drug discovery, decentralized clinical trials, and cloud-enabled research platforms.

- Hybrid cloud deployment models accounted for nearly 38-42% of cloud implementations in 2025, reflecting growing preferences for balancing regulatory compliance requirements, data sovereignty, and operational flexibility across global pharmaceutical organizations.

- Drug development and clinical trial applications represented approximately 35-40% of total cloud service adoption in 2025, driven by increasing adoption of decentralized clinical trials, real-time analytics platforms, and collaborative research ecosystems.

- More than 70% of large pharmaceutical companies globally have accelerated their cloud transformation initiatives, significantly increasing investments in cloud-native platforms supporting clinical operations, manufacturing processes, and regulatory submissions.

- Asia-Pacific is projected to register the fastest regional growth with an estimated CAGR of 13.7% during the forecast period, supported by expanding pharmaceutical R&D investments, government-led healthcare digitalization initiatives, and increasing adoption of cloud-enabled clinical research platforms.

- AI-enabled cloud services are expected to contribute approximately 25-30% of future pharmaceutical cloud investments by 2030, owing to increasing utilization of predictive analytics, machine learning-driven drug discovery, and intelligent clinical trial management solutions.

- Public cloud adoption accounted for nearly 30-35% of deployment models in 2025, primarily among biotechnology companies and emerging pharmaceutical organizations seeking scalable and cost-effective infrastructure solutions.

- The Pharma Cloud Services Market is projected to reach US$ 55.78 billion by 2033, growing at a CAGR of 13.9% during the forecast period, driven by increasing digital transformation initiatives and the growing demand for secure, compliant, and interoperable cloud ecosystems.

Pharma Cloud Services Market Scope

| Metrics | Details | |

| CAGR | 13.9% | |

| Market Size Available for Years | 2023-2035 | |

| Estimation Forecast Period | 2026-2035 | |

| Revenue Units | Value (US$ Bn) | |

| Segments Covered | Service Type | SaaS (Software as a Service), PaaS (Platform as a Service), and IaaS (Infrastructure as a Service) |

| Deployment Mode | Public Cloud, Private Cloud, and Hybrid Cloud | |

| Application | Drug Discovery, Drug Development, Drug Manufacturing, Supply Chain, Regulatory & Quality Compliance, and Others | |

| End-User | Pharmaceutical and Biotechnology Companies, Contract Research Organizations (CROs), Healthcare Providers, and Research & Academic Institutes | |

| Regions Covered | North America, Europe, Asia-Pacific, South America and the Middle East & Africa | |

Pharma Cloud Services Market Dynamics

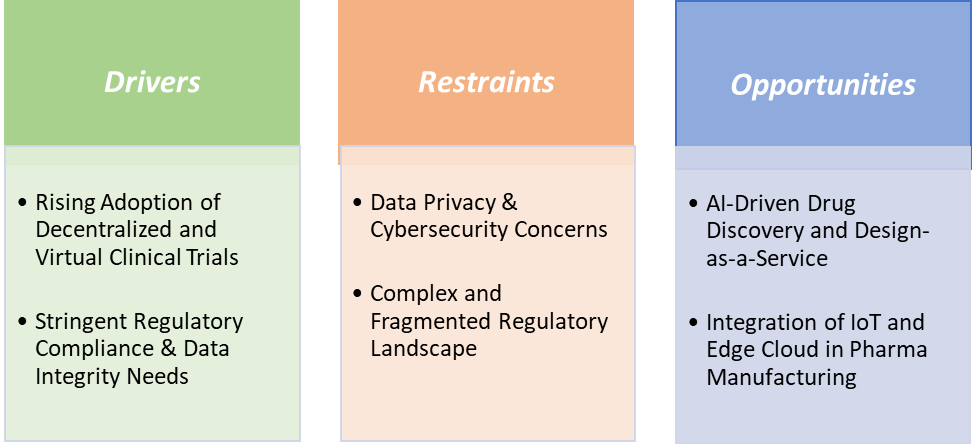

Drivers: Rising adoption of decentralized and virtual clinical trials is significantly driving the pharma cloud services market growth

The rising adoption of decentralized and virtual clinical trials is a major catalyst driving the growth of the pharma cloud services market, as it fundamentally transforms how trials are conducted. By enabling remote patient participation through telemedicine, wearable devices, ePROs, and home-based data collection, decentralized clinical trials rely heavily on secure, scalable, and compliant cloud infrastructures to capture, store, and analyze real-time patient data. Cloud platforms facilitate seamless collaboration between sponsors, CROs, investigators, and patients, reducing site visits, improving data accuracy, and enhancing patient diversity.

Recent developments exemplify this shift. For instance, in April 2025, Clinical ink, a global leader in life science technology, launched TrialLensTM, a fully integrated, AI-powered analytics dashboard that transforms how clinical trial eCOA data is visualized, queried, and interpreted. TrialLens delivers real-time, actionable insights into study operations, participant behavior, and digital biomarker metrics across decentralized and hybrid clinical trials. As a result, demand for cloud-based platforms with interoperability and advanced analytics is surging, positioning cloud technologies as the backbone of next-generation, patient-centric clinical research.

Restraints: Data privacy & cybersecurity concerns are hampering the growth of the market

Data privacy and cybersecurity concerns are major factors hampering the growth of the pharma cloud services market, as pharmaceutical companies manage vast volumes of highly sensitive data including clinical trial results, patient health records, and proprietary drug formulations. The sector has become a prime target for cyberattacks. Cloud misconfigurations, hybrid IT ecosystems, and third-party integrations often create vulnerabilities that malicious actors exploit.

Such incidents not only disrupt R&D operations but also expose companies to regulatory penalties under laws like HIPAA, GDPR, and 21 CFR Part 11.In the year to August 31, 2024, there have been 491 data breaches of 500 or more records, and at least 58,668,002 records are known to have been breached. The average breach size in 2024 is currently 119,487 records and the median breach size is 4,109 records.

For more details on this report - Request for Sample

Pharma Cloud Services Market Segment Analysis

The global pharma cloud services market is segmented based on service type, deployment mode, application, end-user, and region.

Service Type: The SaaS (Software as a Service) segment is dominating and the fastest-growing in the pharma cloud services market with a 63.49% share

The Software as a Service (SaaS) segment is dominating and emerging as the fastest-growing area of the pharma cloud services market, driven by its scalability, cost-efficiency, and compliance-ready architecture. SaaS enables pharma firms to access validated, cloud-hosted applications for functions such as clinical data management, pharmacovigilance, manufacturing, and commercial operations without heavy infrastructure investment.

Recent developments underscore this momentum by launching various advanced products into the market. For instance, in October 2025, GE HealthCare launched CareIntellect for Perinatal, a cloud-first Software-as-a-Service (SaaS) application designed to deliver clear, actionable insights that help clinicians improve maternal and fetal care. CareIntellect for Perinatal supports clinicians by integrating information from disparate clinical sources in a single place, making it fast and easy for clinicians to monitor status, annotate clinical events, search historical data, and remotely monitor patients, with the aim of providing timely patient insights. This is the second application within GE HealthCare’s CareIntellect family of clinical and operational applications, built to help healthcare systems quickly and easily deploy and scale new applications.

Similarly, in March 2025, Carrier Global Corporation launched Carrier Lynx FacTOR, a revolutionary software-as-a-service (SaaS) solution designed to transform product release processes in the pharmaceutical industry. Lynx FacTOR automates end-to-end product release evaluations, minimizing manual processes and safely accelerating product movement in the cold chain. The name FacTOR represents the critical impact of 'time out of range' in supporting product quality and patient safety.

Pharma Cloud Services Market Geographical Share

North America is expected to dominate the global pharma cloud services market with a 44.27%

North America is expected to dominate the global pharma cloud services market due to its advanced digital infrastructure, presence of major market players, strong regulatory support, and high concentration of leading pharmaceutical and technology companies. The region's growth is driven by early adoption of cloud-based R&D, manufacturing, and clinical solutions.

US Pharma Cloud Services Market Trends

The U.S. Food and Drug Administration (FDA) has played a pivotal role in encouraging this shift through initiatives like precisionFDA, a cloud-based platform that enables secure collaboration and high-performance genomic data analysis among researchers and regulators. The FDA has also transitioned several internal systems, such as its Advanced Laboratory Information System (ALIS), to cloud environments, signaling confidence in compliant cloud frameworks.

Major and emerging market players are developing various technologies, which are boosting the market growth in the US. For instance, EVERSANA, a leading provider of commercialization services to the global life sciences industry, launched a groundbreaking pharmaceutical marketing AI agency running on an end-to-end AI-powered delivery platform built on Google Cloud technology. The AI Agency, actively deployed and validated for multiple pharmaceutical brands, is 80% AI-powered and automated, reducing marketing costs and rapidly accelerating traditional agency operations.

Furthermore, the US SaaS providers like Veeva Systems continue to expand their cloud portfolios for eClinical, regulatory, and commercial operations, supported by frequent FDA approvals for digital therapeutics and AI-assisted trials. Combined with heavy R&D spending, a strong CRO network, and a mature compliance ecosystem (HIPAA, 21 CFR Part 11), the US ecosystem positions itself as the global hub for cloud-driven pharmaceutical innovation and growth.

The Asia Pacific region is the fastest-growing region in the global pharma cloud services market, with a CAGR of 13.7%

The Asia-Pacific (APAC) region is emerging as the fastest-growing market in the global pharma cloud services industry, driven by rapid digital transformation, expanding pharmaceutical R&D, and strong government initiatives to modernize healthcare infrastructure. Countries like China, India, Japan, and South Korea are investing heavily in cloud-enabled pharma ecosystems to enhance drug discovery, manufacturing efficiency, and clinical research.

The adoption of cloud services has been accelerated by the region’s expanding biotech sector and regulatory modernization, for instance, India’s CDSCO and Singapore’s HSA are aligning more closely with global data integrity and GxP standards, fostering cloud adoption in validated environments. The rise of regional CROs and biotech startups adopting SaaS-based clinical and regulatory tools like ArisGlobal’s LifeSphere and Medidata Rave Cloud further accelerates adoption. Combined with the growing volume of clinical trials and government-backed digital health programs (such as India’s Ayushman Bharat Digital Mission), APAC’s strong demand for scalable, compliant cloud infrastructure positions it as the fastest-growing and most dynamic region in the pharma cloud services landscape.

Europe Pharma Cloud Services Market Trends

The European pharma cloud services market is experiencing steady and robust growth, fueled by digital transformation initiatives, stringent data compliance standards, and strong collaboration between pharmaceutical companies and cloud technology providers. The implementation of the EU General Data Protection Regulation (GDPR) has encouraged cloud providers to develop highly secure, compliant platforms tailored for life sciences.

The European Medicines Agency (EMA) also rolled out cloud-supported initiatives under its Regulatory Science to 2025 roadmap, promoting data interoperability and digital submissions via cloud-based eCTD platforms. Meanwhile, Europe’s growing biotech hubs such as Switzerland, Denmark, and Ireland are rapidly adopting SaaS-based solutions for eClinical and pharmacovigilance operations, exemplified by Veeva Systems’ expanding customer base across these regions. Collectively, the region’s emphasis on regulatory compliance, sustainability, and digital innovation positions Europe as a mature and fast-evolving market within the global pharma cloud services landscape.

Pharma Cloud Services Market Competitive Landscape Analysis

The competitive landscape of the Pharma Cloud Services Market is characterized by strategic collaborations between cloud technology providers and pharmaceutical organizations seeking to accelerate digital transformation initiatives. Market participants are increasingly focusing on expanding their life sciences cloud portfolios through investments in regulatory compliance capabilities, cybersecurity enhancements, and AI-enabled analytics platforms. Product innovation, geographic expansion strategies, and strategic partnerships continue to remain key differentiating factors influencing competitive dynamics across the market.

Pharma Cloud Services Market Companies

Top companies in the pharma cloud services market include IBM Corporation, Oracle, Google, Amazon Web Services, Inc., Microsoft, Veeva Systems Inc., Siemens, and Körber AG, among others.

Recent Developments in Pharma Cloud Services Market

- June 2026: IBM Corporation expanded its AI-powered hybrid cloud capabilities for life sciences and pharmaceutical companies, enhancing secure data management, clinical research, and regulatory compliance solutions.

- June 2026: Microsoft Corporation strengthened its healthcare and life sciences cloud offerings by advancing Azure-based solutions that support pharmaceutical research, drug development, and intelligent data analytics.

- May 2026: Amazon Web Services (AWS), Inc. continued expanding its cloud services portfolio for pharmaceutical organizations through enhanced generative AI, data lakes, and scalable computing solutions for clinical and R&D applications.

- May 2026: Oracle Corporation advanced its cloud infrastructure and healthcare platforms by strengthening solutions for clinical trial management, pharmacovigilance, and pharmaceutical supply chain operations.

- April 2026: Google LLC enhanced its cloud-based AI capabilities designed to accelerate drug discovery, precision medicine initiatives, and pharmaceutical data interoperability across healthcare ecosystems.

- April 2026: Veeva Systems Inc. expanded its cloud applications portfolio by strengthening solutions for regulatory affairs, quality management, and clinical operations within the pharmaceutical industry.

- March 2026: Siemens AG continued advancing its digital transformation technologies by enhancing cloud-enabled industrial and life sciences solutions that improve pharmaceutical manufacturing efficiency and compliance management.

- March 2026: Körber AG strengthened its pharmaceutical software capabilities by expanding cloud-based supply chain and manufacturing execution solutions for the global life sciences sector.

- February 2026: IBM Corporation introduced enhancements to its enterprise AI and cloud technologies that support secure pharmaceutical data integration and accelerate innovation across drug development workflows.

Emerging Technology Trends

Emerging technologies including artificial intelligence, machine learning, predictive analytics, digital twins, blockchain-enabled data security, and generative AI are transforming pharmaceutical cloud services globally. AI-powered cloud platforms are increasingly supporting drug target identification, clinical trial optimization, pharmacovigilance activities, and personalized medicine initiatives. Furthermore, cloud-native architectures are enabling pharmaceutical organizations to achieve greater interoperability across clinical, operational, and commercial data ecosystems while improving regulatory compliance capabilities.

Investment Opportunity Analysis

Growing investments in cloud-enabled pharmaceutical innovation continue to create substantial market opportunities across multiple service segments. Pharmaceutical organizations are increasingly allocating resources toward cloud-based clinical trial management systems, advanced analytics platforms, cybersecurity solutions, and AI-driven drug discovery technologies. Emerging markets are also witnessing significant investments in healthcare digitalization programs that are expected to accelerate cloud adoption across pharmaceutical operations. Strategic investments in secure cloud infrastructures are anticipated to remain a key market growth driver through 2033.

Who Should Buy This Report?

This report is designed for pharmaceutical and biotechnology companies seeking to accelerate their digital transformation initiatives and optimize cloud adoption strategies across drug discovery, clinical development, manufacturing, and regulatory operations. Cloud service providers and healthcare technology companies can leverage the report to identify emerging market opportunities, evaluate evolving customer requirements, and strengthen their competitive positioning within the pharmaceutical ecosystem. Contract Research Organizations (CROs) and Contract Development and Manufacturing Organizations (CDMOs) can utilize the insights to enhance their cloud-enabled service capabilities and improve operational efficiencies across clinical and commercial activities. Additionally, healthcare consulting firms, institutional investors, venture capital organizations, and regulatory stakeholders can benefit from the report's comprehensive analysis of market trends, investment opportunities, technology advancements, and regional growth dynamics. The report also serves as a valuable strategic resource for Chief Information Officers (CIOs), Chief Technology Officers (CTOs), and digital transformation leaders responsible for implementing secure, compliant, and scalable cloud infrastructures within pharmaceutical organizations.

Why Should You Buy This Report?

This report provides comprehensive market intelligence on the Pharma Cloud Services Market, delivering actionable insights into emerging technologies, cloud deployment models, regulatory developments, and investment trends shaping the future of pharmaceutical digital transformation. It enables stakeholders to identify high-growth opportunities across cloud-enabled drug discovery, clinical trial management, pharmacovigilance, and pharmaceutical manufacturing applications while evaluating evolving cloud adoption patterns across major global markets. The report offers an in-depth assessment of competitive strategies adopted by leading market participants, helping organizations benchmark their capabilities and develop informed business strategies. Furthermore, it provides valuable insights into data security requirements, regulatory compliance frameworks, regional market dynamics, and future technological innovations expected to influence the market through 2033. By supporting strategic decision-making related to partnerships, investments, product development, capacity expansion, and market entry initiatives, this report serves as an essential resource for organizations seeking to strengthen their position within the rapidly evolving pharma cloud services ecosystem.

The global pharma cloud services market report delivers a detailed analysis with 64 key tables, more than 64 visually impactful figures, and 159 pages of expert insights, providing a complete view of the market landscape.

Suggestions for Related Report

For more healthcare IT-related reports, please click here