Market Size

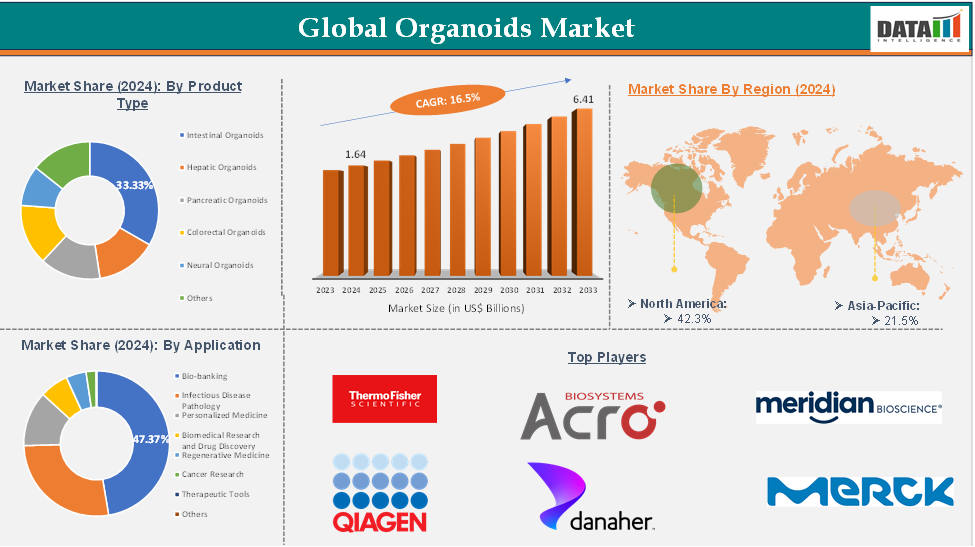

The Organoids Market reached US$ 1.91 Billion in 2025 and is expected to reach US$ 6.41 Billion in 2033, growing at a CAGR of 16.5% during the forecast period (2026–2033).

The global organoids market is growing due to technological advancements, increased research funding, and the demand for accurate and ethical models in biomedical research. Organoids, which are three-dimensional in vitro tissue constructs derived from stem cells, mimic the structure and function of human organs, making them transformative tools in drug discovery, toxicology studies, disease modeling, personalized medicine, and regenerative therapies.

Governments and private organizations are investing heavily in infrastructure and research initiatives, leading to the establishment of dedicated research centers and biobanks. However, the market faces challenges such as high costs, a lack of standardized protocols, and ethical concerns.

However, the North America region witnessing increased adoption of organoid technologies. The integration of organoids with other technologies is opening new frontiers in biomedical research and precision medicine.

Executive Summary

For more details on this report, Request for Sample

Organoids Market Dynamics: Drivers & Restraints

Driver: Rise in the prevalence of chronic diseases

The global organoids market is growing due to the increasing prevalence of chronic diseases like cancer, diabetes, cardiovascular diseases, neurological disorders, and liver and kidney diseases. These diseases are becoming more complex and require personalized treatments. Traditional preclinical models, such as 2D cell cultures and animal testing, have struggled to replicate the intricate physiological and genetic makeup of human tissues, resulting in limited clinical trial outcomes.

Organoids, which mimic the architecture and function of real human organs at a miniaturized scale, offer a revolutionary alternative by providing biologically relevant models that accurately recapitulate the pathophysiology of chronic diseases.

For instance, according to the Centers for Disease Control and Prevention, chronic diseases like heart disease, cancer, and diabetes are the leading causes of death and disability in the US, contributing to $4.5 trillion in annual healthcare costs. Six in 10 Americans have at least one chronic disease, with many preventable diseases caused by risk behaviors like smoking, poor nutrition, physical inactivity, and excessive alcohol use.

Hence, a rise in chronic diseases is driving increased investment in organoids due to the need for accurate, human-relevant disease models. Pharmaceutical and biotech companies are integrating organoids into drug discovery and personalized medicine workflows, accelerating innovation and therapeutic precision.

Restraint: High development costs

The organoids market faces significant challenges due to high development costs, which limit accessibility and scalability, especially for smaller research institutions and startups. The complex, resource-intensive process involves specialized growth media, 3D culture systems, and skilled technical expertise, leading to elevated operational expenses. The need for advanced laboratory infrastructure and continuous monitoring further increases costs. To overcome this, cost-optimization strategies, increased funding, and technological innovations are needed to simplify and streamline organoid development processes.

Market Scope

| Metrics | Details | |

| CAGR | 16.5% | |

| Market Size Available for Years | 2023-2033 | |

| Estimation Forecast Period | 2026-2033 | |

| Revenue Units | Value (US$ Bn) | |

| Segments Covered | Product Type | Intestinal Organoids, Hepatic Organoids, Pancreatic Organoids, Colorectal Organoids, Neural Organoids, Others |

| Application | Bio-banking, Infectious Disease Pathology, Personalized Medicine, Biomedical Research and Drug Discovery, Regenerative Medicine, Cancer Research, Therapeutic Tools, Others | |

| End User | Biopharmaceutical Companies, Contract Research Organizations, Academics, and Research Institutes | |

| Regions Covered | North America, Europe, Asia-Pacific, South America, and the Middle East & Africa | |

Organoids Market Segment Analysis

The global market is segmented based on product type, application, end user, and region.

Product Type

The intestinal organoids segment from the product type is expected to hold 33.33% of the organoids market

Intestinal organoids are miniaturized structures made from stem cells that mimic the human intestine's architecture and function. They contain various intestinal cell types, replicating physiological processes like absorption, secretion, and barrier function. These organoids are useful for studying gastrointestinal diseases, host-microbiome interactions, drug absorption, and personalized medicine applications, providing a more accurate alternative to traditional cell cultures and animal models.

The intestinal organoids segment is gaining momentum due to research into gastrointestinal disorders like IBD, colorectal cancer, and celiac disease. Their high-fidelity modeling of intestinal functions makes them valuable for drug screening, disease modeling, and microbiome research. The demand for personalized treatment and advancements in stem cell and regenerative medicine technologies further boost their adoption.

For instance, in January 2024, HUB Organoids launched its IntegriGut Screen, a screening service using IBD patient-derived organoid monolayers (PDO Monolayers) to accelerate the development of novel IBD therapies. The service uses high-quality human data on epithelial barrier function, addressing the pressing need for faster, more physiologically relevant models. With 40% of IBD patients failing to respond to mainstay therapies, IntegriGut Screen enables rapid evaluations of epithelial barrier function and integrity, addressing the pressing need for faster, more relevant models.

Organoids Market - Geographical Analysis

North America dominated the global organoids market

The North American organoids market is fueled by significant investments in biotechnology and life sciences research, government funding, and private sector initiatives. The presence of leading pharmaceutical companies and advanced healthcare infrastructure accelerates the adoption of organoid technologies for drug discovery, personalized medicine, and disease modeling. The growing awareness of limitations of traditional preclinical models and the prevalence of chronic diseases further drive demand.

Asia-Pacific is the global organoids market

The Asia-Pacific organoids market is experiencing rapid growth due to improved healthcare infrastructure, research capabilities, and government support for biotechnology initiatives. The rising prevalence of chronic diseases in the region necessitates advanced disease models and personalized therapies. The growing biopharmaceutical industry and clinical trials also contribute to market expansion. Lower operational costs and skilled researchers attract investments, making the Asia-Pacific an attractive market for organoid technologies.

For instance, in April 2025, Researchers at Keio University developed long-lasting, functional human liver organoids from frozen hepatocytes, marking a huge moment in organoid science.

Organoids Market - Key Players

The major global players in the organoids market include Thermo Fisher Scientific Inc, Merck KGaA, QIAGEN N.V, MERIDIAN BIOSCIENCE Inc, New England Biolabs, Mirus Bio LLC, ACROBiosystems, Danaher Corporation, ATCC, and AxoSim among others.

Recent Developments

In March 2026, STEMCELL Technologies expanded its organoid culture platforms with advanced 3D cell models for disease research. The innovation focuses on improving reproducibility and scalability. This supports drug discovery and personalized medicine.

In February 2026, Thermo Fisher Scientific introduced new organoid growth media and tools for complex tissue modeling. The development enhances experimental accuracy and efficiency. This benefits pharmaceutical and academic research.

In January 2026, Merck KGaA (MilliporeSigma) strengthened its organoid solutions with optimized reagents and culture systems. The focus is on high-throughput screening applications. This supports precision medicine advancements.