North America and Europe Sterile Injectables CMO Market Size & Industry Outlook

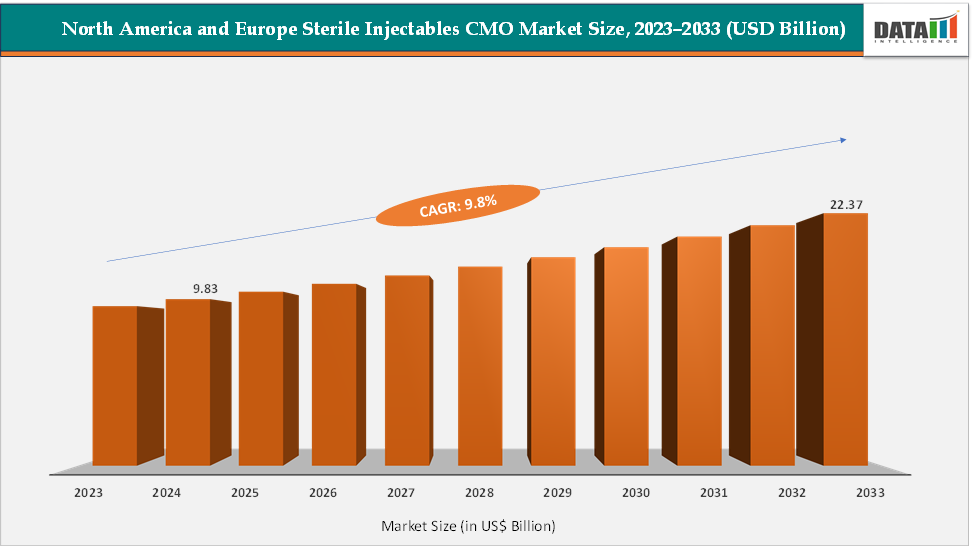

The North America and Europe sterile injectables CMO market size reached US$ 9.83 Billion in 2024 from US$ 9.15 Billion in 2023 and is expected to reach US$ 22.37 Billion by 2033, growing at a CAGR of 9.8% during the forecast period 2025-2033. The North America and Europe sterile injectables CMO market is experiencing robust growth, driven by rising demand for biologics, increasing outsourcing by pharmaceutical companies, and the rapid expansion of prefilled syringe and lyophilized dosage forms. North America leads in technological advancement and biologics production, while Europe offers deep regulatory expertise and a strong mid-sized CDMO presence. Key therapeutic drivers include oncology, which accounts for the largest share due to the injectable nature of most cancer drugs.

Prominent CMOs like Catalent, Lonza, Vetter Pharma, and Thermo Fisher Scientific are expanding their fill-finish and lyophilization capacities, driven by demand for high-value biologics and complex injectables. For instance, Vetter announced plans to expand its capacity in the US & Germany for aseptic injectable filling, while Catalent has invested over $350 million in recent sterile fill-finish expansions across the U.S. and Europe. The shift toward patient-centric drug delivery, including prefilled syringes, auto-injectors, and cartridges, has pushed CMOs to modernize lines with advanced technologies for enhanced sterility assurance.

Moreover, the ongoing shortage of in-house sterile manufacturing capabilities among small and mid-sized pharma, along with the rise of orphan drugs and mRNA-based therapies, has amplified outsourcing demand. Despite challenges such as stringent regulatory scrutiny and capacity constraints, the market is witnessing increased strategic partnerships and long-term supply agreements. This landscape presents a lucrative opportunity for CMOs that offer integrated, flexible, and compliant sterile injectable solutions aligned with evolving clinical and commercial needs.

Key Market Highlights

- North America dominates the sterile injectables CMO market with the largest revenue share of 59.51% in 2024.

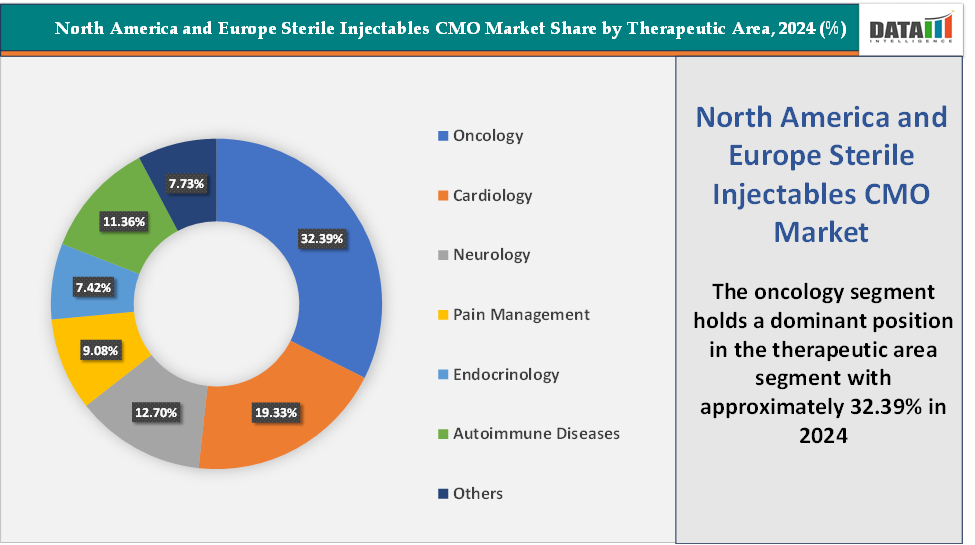

- Based on therapeutic area, the oncology segment led the market with the largest revenue share of 32.39% in 2024.

- The major market players in the North America and Europe sterile injectables CMO market are Catalent, Inc, Lonza, Vetter Pharma, Thermo Fisher Scientific Inc., Recipharm AB, Jubilant HollisterStier, Grand River Aseptic Manufacturing, and Afton Scientific, among others.

Market Dynamics

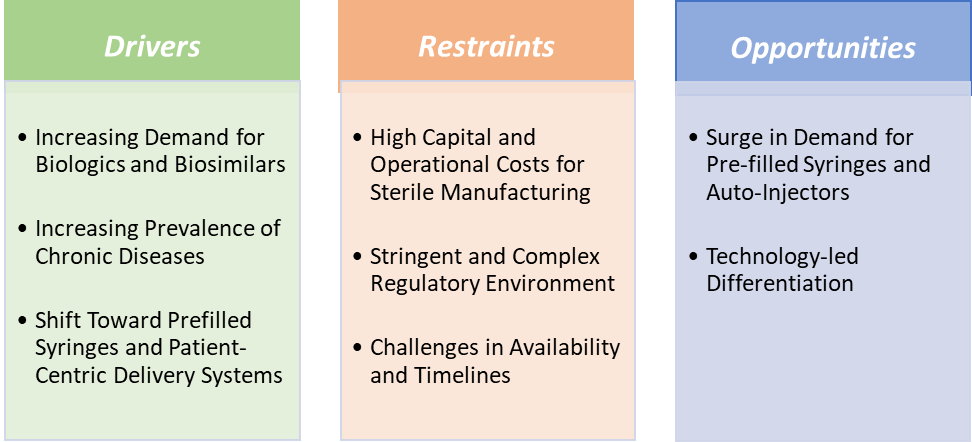

Drivers: Increasing demand for biologics and biosimilars is significantly driving the North America and Europe sterile injectables CMO market growth

The North America and Europe sterile injectables CMO market is growing due to the increasing demand for biologics and biosimilars. Pharmaceutical companies are turning to specialized contract manufacturers for advanced expertise and regulatory know-how, enabling faster development and commercialization of innovative therapies while reducing operational costs and capital investment in specialized manufacturing facilities.

Moreover, product launches, approvals, in biologics and biosimilars, which often require precise dosing and ease of administration, propel demand for prefilled formats. The shift supports the rise of outpatient treatments and home-based therapies, providing greater convenience for patients. For instance, in April 2025, the approval of Argenx’s VYVGART Hytrulo prefilled syringe supports the growing Sterile Injectables CMO market, as it drives demand for high-quality prefilled syringe production to enable self‑injection and home‑based therapy.

Furthermore, major contract manufacturing organizations (CMOs) in the USA and Europe are investing in advanced sterile fill-finish and large-scale biologic drug production facilities. For instance, in January 2024, Enzene Biosciences opened its first US manufacturing site 2024, offering both continuous manufacturing and flexible fed-batch processes aimed at supporting novel biologic and biosimilar pipelines destined for injectable use. Additionally, the UK and Germany are leading in biosimilar adoption due to their robust biomanufacturing infrastructure and innovative manufacturing techniques, under MHRA oversight.

Restraints: High capital and operational costs for sterile manufacturing are hampering the growth of the market

The production of sterile injectables requires significant investment in state-of-the-art facilities, advanced technology, and highly trained personnel. These costs can be prohibitive, especially for smaller manufacturers, making it a significant challenge to scale operations while maintaining the necessary levels of quality and sterility. Operational expenses remain high due to continuous quality assurance, extensive sterility testing, and skilled labor for maintaining aseptic conditions. These costs can reach hundreds of millions of dollars.

For instance, in a recent analysis by NCBI the cost of manufacture of vaccines, which estimated the cost of sterile formulation as an ampoule to be around $0.12/unit, and as a vial to be around US$0.35/unit, with these values including raw materials (ie, the vial or ampoule itself), labour, facility and equipment costs, and overheads.

Moreover, the market faces multi-million-dollar capital outlays and operational costs, limiting market expansion and innovation. Contract manufacturers must balance investment in advanced technology and regulatory compliance with cost-effective production strategies to remain competitive in North America and Europe. Thus, sterile injectable manufacturing requires significant capital investment and operational expenses, but these are crucial for product safety and regulatory compliance. Smaller manufacturers face financial barriers, emphasizing strategic planning and innovation. Balancing these challenges is essential for market expansion and innovation.

Opportunities: Technology-led differentiation is expected to create a market opportunity

The North America and Europe Sterile Injectables CMO Market is dominated by technology-led differentiation, offering advanced capabilities like high-speed fill-finish lines, lyophilization, and ready-to-use formats. Innovative technologies, such as isolator-based manufacturing, single-use systems, and real-time quality monitoring, improve production efficiency, reduce contamination risks, and meet regulatory requirements. This leads to increased growth and competitive advantage in mature markets.

For instance, in 2025, major companies like Amneal Pharmaceuticals are expanding domestic sterile injectable production capacity through collaborations with medical technology firms such as Apiject Systems. The expansion includes the use of advanced Blow-Fill-Seal (BFS) technology for producing sterile, prefilled injectors at scale with superior efficiency, speed, and reduced supply chain complexity.

Moreover, in September 2024, Norbrook in Northern Ireland upgraded its sterile injectable manufacturing suite with a £1.3 million investment for a new modular cleanroom and improved HVAC systems, ensuring compliance with the latest EU GMP Annex 1 guidelines. The facility manufactures key sterile injectable veterinary products.

North America and Europe are seeing increased investments in digitalized quality control, robotics-assisted packaging, and AI-driven predictive maintenance, helping CMOs reduce downtime and meet client demands for flexibility. As biopharmaceutical pipelines shift towards injectable biologics and personalized medicines, technology-led differentiation is positioned to capture a larger market share.

For more details on this report – Request for Sample

Sterile Injectables CMO Market, Segment Analysis

The North America and Europe sterile injectables CMO market is segmented based on product type, dosage form, therapeutic area, CMO service type, and region.

Therapeutic Area: The oncology segment is dominating the North America and Europe sterile injectables CMO market with a 32.39% share in 2024

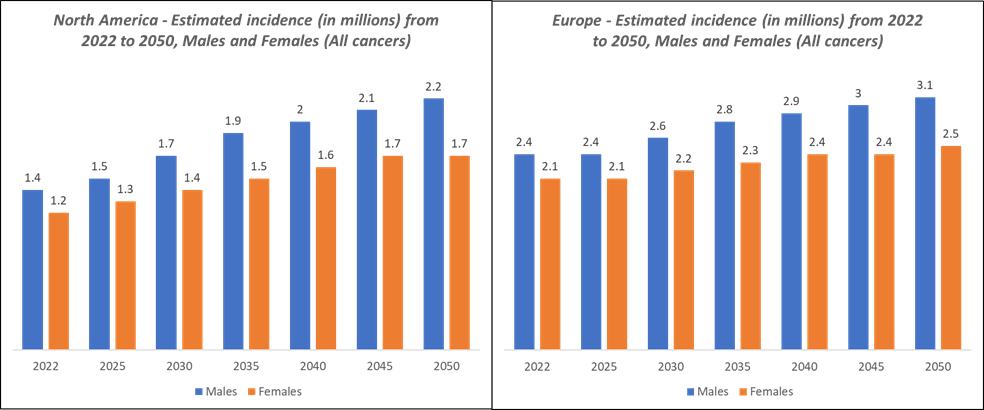

The oncology segment is one of the strongest growth drivers in the North America and Europe sterile injectables CMO market, propelled by the rising prevalence of cancer, the increasing complexity of oncology therapeutics, and the growing demand for specialized injectable delivery formats. Cancer remains a leading cause of death globally, with over 2.8 million new cancer cases expected annually in North America alone by 2025, according to the World Health Organization. Many of the novel therapies, including monoclonal antibodies, antibody-drug conjugates (ADCs), checkpoint inhibitors, and cell & gene therapies, require highly sterile injectable formats for safe and effective delivery. These biologics often have short shelf lives and demand strict temperature and contamination controls, making outsourced sterile manufacturing to experienced CMOs a strategic necessity.

CMOs like Lonza, Vetter, Recipharm, Siegfried and Thermo Fisher Scientific have responded with large-scale investments. For instance, in North America, Thermo Fisher has expanded operations in Greenville, NC, to support large-scale oncology product manufacturing and packaging. The highly potent nature of oncology APIs further necessitates isolator-based systems and dedicated containment zones, infrastructure that only a select group of CMOs can offer at scale.

As more targeted and personalized therapies enter the market requiring smaller batch production, cold-chain management, and high-mix low-volume manufacturing, CMOs are uniquely positioned to meet these complex requirements. Altogether, the oncology segment’s dynamic growth, technical demands, and regulatory urgency are significantly driving CMO engagement and sterile injectable infrastructure expansion in both regions.

The cardiology segment is the fastest-growing in the North America and Europe sterile injectables CMO market with 10.1% CAGR over the forecast period

The cardiology segment is steadily contributing to the growth of the North America and Europe sterile injectables CMO market, driven by a combination of rising cardiovascular disease prevalence, the critical need for rapid drug administration, and increased adoption of injectable biologics and biosimilars. Cardiovascular diseases remain the leading cause of death globally, accounting for over 17.9 million deaths per year according to the World Health Organization, with a significant burden in the U.S. and European countries due to aging populations and lifestyle-related risk factors.

These rising cases create consistent demand for fast-acting injectable drugs such as antithrombotics, vasodilators, antiarrhythmics, and biologic agents, which require sterile formulations to ensure immediate therapeutic effect in acute care and hospital settings. These innovations require CMOs with robust aseptic processing and advanced fill-finish capabilities.

In both Europe and North America, the cardiology segment’s focus on sterile, life-saving therapies combined with the shift toward ready-to-administer injectable formats is ensuring sustained CMO demand and capacity expansion in this area. This trend is expected to continue as more advanced injectable drugs targeting complex cardiovascular conditions enter the pipeline and require compliant, scalable production.

Sterile Injectables CMO Market, Geographical Analysis

North America is expected to dominate the North America and Europe sterile injectables CMO market with a 59.51% in 2024

The North American sterile injectable CMO market is being fueled by significant factors such as real-world investments, expansion, product innovation, and strategic partnerships. For instance, in July 2025, Simtra BioPharma Solutions, a leading global contract development and manufacturing company specializing in injectable medicines, acquired a 65-acre property from Cook Group, providing over 300,000 square feet of space for expansion near its Bloomington, Indiana, manufacturing facility.

Furthermore, in February 2024, Simtra BioPharma Solutions, formerly Baxter BioPharma, invested over $250 million to expand its sterile fill-finish capacity in Bloomington, Indiana, in response to increasing demand for biologics and injectable therapies. Moreover, in April 2024, Baxter launched ten new injectable pharmaceutical products in critical-therapy areas, highlighting the need for advanced sterile injectable manufacturing in the U.S.

Additionally, North America is the largest and most strategically important market for sterile injectables CMOs due to its fast FDA regulatory approvals, advanced technologies, and high concentration of venture-funded biotech's. This allows for quicker commercialization for clients and provides a competitive advantage in handling high-potency APIs and pre-filled syringe formats. The region's high concentration of venture-funded biotechs also relies heavily on outsourcing due to limited in-house capacity.

Competitive Landscape

Top companies in the North America and Europe Sterile Injectables CMO Market are Catalent, Inc, Lonza, Vetter Pharma, Thermo Fisher Scientific Inc., Recipharm AB, Jubilant HollisterStier, Grand River Aseptic Manufacturing, and Afton Scientific, among others.

Market Scope

| Metrics | Details | |

| CAGR | 9.8% | |

| Market Size Available for Years | 2022-2033 | |

| Estimation Forecast Period | 2025-2033 | |

| Revenue Units | Value (US$ Bn) | |

| Segments Covered | Product Type | Small Molecules and Large Molecules |

| Dosage Form | Liquid Injectables, Pre-filled Syringes, Lyophilized Injectables, and Others | |

| Therapeutic Area | Oncology, Cardiology, Neurology, Pain Management, Endocrinology, Autoimmune Diseases, and Others | |

| CMO Service Type | Manufacturing Services, Development Services, Packaging Services, and Others | |

| Regions Covered | North America and Europe | |

The North America and Europe sterile injectables CMO market report delivers a detailed analysis with 49 key tables, more than 48 visually impactful figures, and 159 pages of expert insights, providing a complete view of the market landscape.

Suggestions for Related Report

For more medical devices-related reports, please click here