Hole Finishing Tools Market Size & Forecast

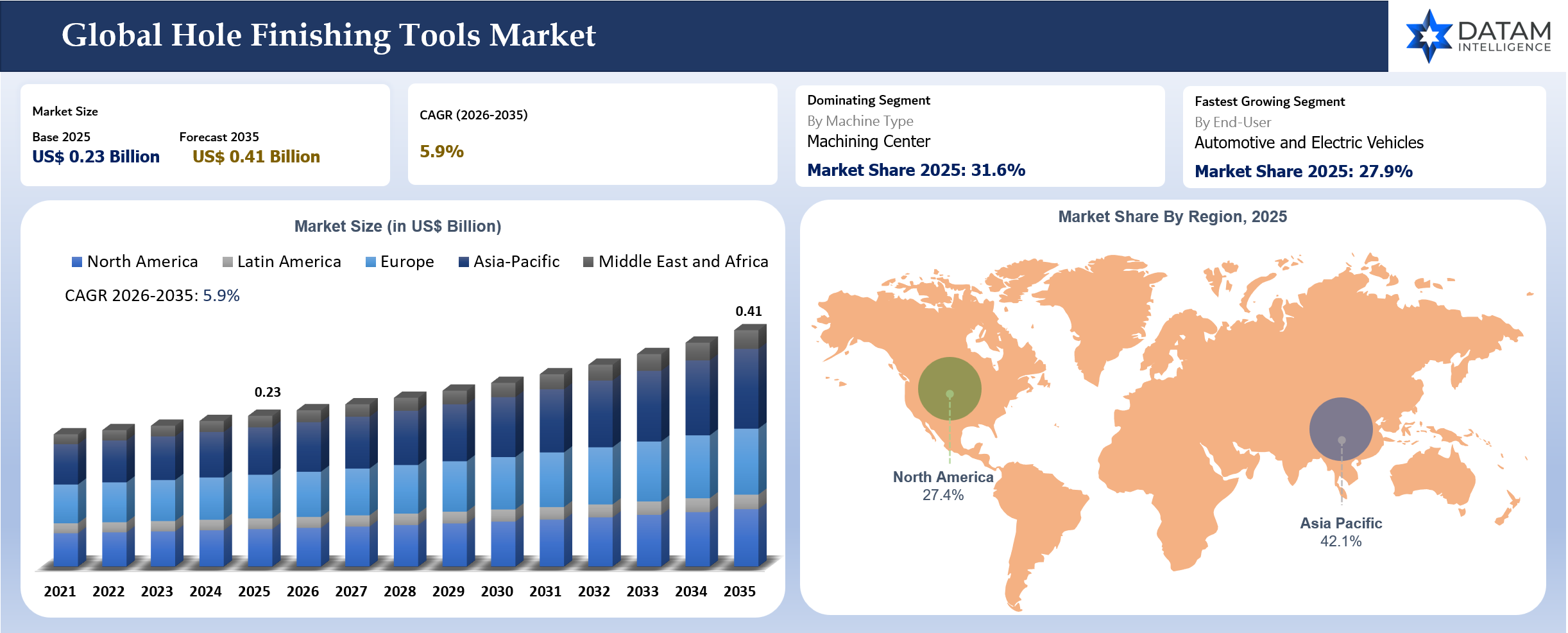

The global hole finishing tools market reached US$ 0.23 billion in 2025 and is expected to reach US$ 0.41 billion by 2035, growing with a CAGR of 5.9% during the forecast period 2026-2035. Hole finishing is becoming a board-level quality issue in precision manufacturing because one rejected bore can scrap a high-value housing, delay an automated assembly cell and trigger a customer quality claim.

EV motor housings, brake bodies, hydraulic manifolds, aircraft brackets, dental implants, medical devices and semiconductor equipment plates all need reliable roundness, surface finish, chamfer geometry and positional stability. Buyers are shifting from catalogue reamer purchasing to bore-assurance programs where the supplier must prove diameter capability, edge life, coolant strategy and repeatability across several machine platforms.

Asia-Pacific remains the largest and fastest-growing regional opportunity through automotive, electronics, job shop, precision machinery and semiconductor equipment clusters. The U.S. remains attractive where aerospace, defense, medical manufacturing and reshoring programs require traceability and local support. Japan remains a premium market because machine tool builders, automotive suppliers, bearing producers and precision component makers favor process stability and long-term supplier relationships.

Buyer attention is shifting toward cost per accepted hole, reconditioning economics, local technical support, material-specific tooling and proof that a premium reamer, countersink, burnishing tool or honing tool can reduce scrap and inspection delays. Investment is concentrated in precision grinding, coating access, PCD capability, digital ordering, tool-life tracking and application engineering rather than broad catalogue expansion.

Key Takeaways

- Asia-Pacific led the global hole finishing tools market with 42.1% share in 2025, supported by large automotive, electronics, semiconductor equipment, precision parts, medical device and industrial machinery manufacturing clusters across China, Japan, India, South Korea and ASEAN.

- North America accounted for 27.4% share in 2025, driven by aerospace, defense, medical devices, semiconductor equipment, EV component machining and reshoring-led demand for high-precision bore finishing solutions.

- Europe held 19.9% share in 2025, supported by premium automotive engineering, aerospace machining, industrial machinery, medical technology and strong adoption of advanced reaming, honing, deburring and burnishing tools.

- Machining centers remained the largest machine type with 31.6% share in 2025 as manufacturers increasingly rely on flexible CNC platforms for accurate reaming, counterboring, countersinking, deburring and finishing use cases across mixed production environments.

- Automotive and electric vehicles represented the fastest-growing end-user segment with 27.9% share in 2025, as EV motor housings, brake components, battery thermal plates, aluminum castings and precision drivetrain parts require stable bore quality and repeatable surface finish.

- Solid carbide, PVD coated carbide, PCD and diamond-coated tools are gaining attention where customers need longer tool life, lower diameter drift, stronger edge stability and reduced cost per accepted hole.

- Supplier differentiation is shifting from unit price toward lifecycle economics, including regrind planning, material-specific recommendations, tool availability, application support, bore-quality proof and cost per accepted hole.

Hole Finishing Tools Industry Trends and Strategic Insights

- Hole finishing suppliers are competing on process confidence, service depth and lifecycle economics. Buyers increasingly want evidence that a tool will protect bore quality, reduce downtime and maintain surface finish across production shifts.

- Commercial opportunity is strongest where the finished hole affects assembly, sealing, noise, fluid flow, safety or inspection time. Premium suppliers should frame value around cost per accepted hole and documented process stability.

- Regional strategy should separate high-volume Asian production from premium Japanese, German and U.S. programs where documentation, supplier trust and local technical support drive purchasing decisions.

- EV and semiconductor equipment demand is redirecting hole finishing toward aluminum castings, thermal plates, precision manifolds, vacuum components, and complex multi-axis use cases.

Hole Finishing Tools Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 0.23 Billion | |

| 2035 Projected Market Size | US$ 0.41 Billion | |

| CAGR (2026-2035) | 5.9% | |

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| Largest Machine Type | 5-Axis Machining Center | |

| Fastest Growing End-User | Automotive and Electric Vehicles | |

| By Tool Grade | High Speed Steel (HSS), Solid Carbide, Cermet, Diamond Tools | |

| By Machine Type | 5-Axis Machining Center, Machining Center, CNC Turning Machines (Turning Center), Swiss Type Automatic Lathes (Sliding Head Lathes), Multi-Tasking Machines (Mill Turn Machines), Other | |

| By Workpiece Detail | P Steel, M Stainless Steel, K Cast Iron, N Non Ferrous Metals, S Super Alloys and Titanium, H Hardened Materials, Composites, Plastic, Wood | |

| By End-User | Automotive and Electric Vehicles, Aerospace and Defense, General Machining, Job Shops, Die and Mold, Industrial Machinery, Construction and Agriculture Equipment, Energy and Power Generation, Oil and Gas, Mining, Rail, Marine and Shipbuilding, Electronics and Consumer Appliances, Semiconductor Equipment and Precision Parts, Medical Devices, Dental, Bearing Manufacturing, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Why this report matters in 2026?

Hole finishing buyers enter 2026 with a practical challenge: precision assemblies are becoming less tolerant of bore variation while plants are under pressure to reduce inspection time and labor content. A low-cost finishing tool can become expensive if it creates oversize bores, burrs, poor cylindricity or unstable surface finish.

The decisive shift is the movement from catalogue tool buying to bore-risk management. Tungsten, cobalt, PCD supply, coating capacity, skilled grinding labor and freight uncertainty make lead-time confidence and reconditioning support as important as initial tool price.

Decision-makers need visibility into suppliers that can support material-specific reamers, countersinks, deburring tools, honing tools, burnishing tools, custom specials and local service before a production launch. A clear view of supplier capability helps customers reduce scrap, avoid assembly delays and capture opportunities in EV, aerospace, medical and semiconductor equipment programs.

Strategic Indicators For Hole Finishing Tools

High Regulation Impact

Hole finishing suppliers are now being judged on compliance paperwork as much as dimensional performance. Aerospace, medical device and semiconductor equipment buyers increasingly request tool data packs, coating declarations, batch traceability and recommended safe-use limits before approving a reamer or counterbore for a validated process. Chemical compliance is becoming more practical because hole finishing is sensitive to coolant and surface chemistry. A small change in friction can shift bore size, roundness and surface finish. Suppliers that can prove REACH, RoHS and PFAS-aware process choices have a stronger case with European medical, electronics and aerospace customers.

High Investment Activity

Investment in hole finishing is strongest where customers need bore accuracy without adding secondary inspection time. Automotive transmission housings, EV motor casings, aircraft hydraulic blocks, medical implants and semiconductor precision plates are pushing toolmakers toward higher-accuracy grinding, edge preparation, coating chambers and application engineering.

Capacity investment is also moving closer to regional manufacturing clusters. North American customers increasingly want shorter lead times for engineered tools rather than waiting for European or Asian production slots.

New Product Launches

Recent product activity is concentrated around advanced reamers, exchangeable-head drills, solid-carbide tools, digital tool-supply systems and higher-productivity hole making portfolios. Suppliers are positioning around longer tool life, better inventory visibility, faster tool changeovers and stronger hole-quality consistency.

Supply Chain Disruption

Supply-chain disruption is visible in carbide blanks, PCD supply, coating queues, specialty steel, long custom grinding cycles and international logistics. A small delay in one input can delay the full tool because precision tooling depends on sequential operations. Suppliers with regional warehouses, local regrind partners and transparent lead-time systems can convert disruption into an advantage.

Pricing Volatility

Pricing pressure is no longer a simple annual surcharge conversation. Tungsten carbide powder, cobalt powder, PVD coating capacity, precision grinding wages and air freight affect hole finishing tools differently. Buyers should separate standard catalogue tools, modified specials, engineered specials, coating premium, reconditioning value and emergency lead-time premiums.

Procurement Pressure

Procurement teams are under pressure to reduce tooling spend while production teams need better hole quality and fewer stoppages. A shared cost-per-accepted-hole model helps reduce the gap between purchase price and production economics. Large plants want fewer suppliers but deeper technical coverage, including material-specific recommendations and local service.

New Technology Adoption

Technology adoption includes digital tool configuration, AI-assisted quotation, process simulation, tool vending, connected inventory, automated inspection feedback and predictive regrind planning. The highest-value use cases reduce wrong ordering, stockouts, scrap and downtime.

Regional Expansion Opportunity

Asia-Pacific should remain the strongest expansion region because China, India, Japan, South Korea and ASEAN concentrate automotive, electronics, semiconductor equipment and precision machining demand.

Mexico, Eastern Europe and India offer localized-service opportunities as manufacturers expand EV, aerospace, rail and medical component programs close to end customers.

Government Policy Support

Policy support for hole finishing comes through the industries that need controlled bores and clean edge quality. Semiconductor incentives, defense production, aerospace investment, EV localization and medical manufacturing expansion create recurring demand for accurate hole finishing in stainless steel, aluminum, titanium, copper alloys and engineered plastics.

Import Export And Pricing Intelligence

HS 820760 is the closest trade code for boring and broaching tools and can be used for reamers where customs lines do not split every hole finishing product. Shipment-level keyword filters, supplier names, unit values and destination industries are required to isolate relevant reamers, countersinks, counterbores, honing tools and burnishing tools.

| HS Code | Reporter | Trade Flow | 2025 Trade Value (US$) | Interpretation |

| HS 820770 | Japan | Export | 173,993,222 | Global leader; high-value precision tooling exports dominate |

| HS 820770 | USA | Import | 322,225,489 | Internal demand for reallocation of precision machining tools |

| HS 820770 | Italy | Export | 153,075,036 | Scale-driven exports with competitive pricing advantage |

| HS 820770 | Japan | Import | 61,881,461 | Strong industrial dependency on imported high-precision tools |

| HS 820770 | China | Export | 12,013,811 | Automotive and electronics-driven exports demand for premium milling tools |

Company Coverage Preview

Sandvik Coromant is the largest player to cover because its hole making, boring, reaming and digital machining ecosystem gives it reach across automotive, aerospace, medical, energy and general machining accounts. The company’s USP is its ability to combine grade development, application engineering, distributor reach and digital customer workflow. A buyer can source a standard reamer, discuss a custom solution, build an assembly and access machining knowledge within the same ecosystem.

AI Impact Analysis

AI impact in precision tooling is most useful when it supports engineering judgement rather than replacing it. Tool drawings, workpiece material, machine type, coolant condition and past failure records can be converted into better recommendations. Predictive service is another practical use case. Tool wear, regrind frequency, coating life and customer rejection records can be analyzed to detect patterns before a production stoppage. Many tooling failures show early signals through burr formation, surface change or dimensional drift.

Disruption Analysis

Disruption is coming through process integration, digital ordering, tighter quality gates, sustainability expectations and localized supply-chain strategies. Buyers want fewer surprises at launch and more proof before committing to a supplier. Tool suppliers are moving closer to machine builders, CAM providers, inspection companies and distributors with inventory visibility. A tool sale is becoming part of a broader process package. Suppliers unable to support trials, regrind planning or technical documentation risk being pushed into low-margin catalogue orders.

BCG Matrix: Company Evaluation

STAR

Star players include Sandvik Coromant, Kennametal, MAPAL, OSG, Guhring and Mitsubishi Materials because they combine broad holemaking portfolios, local application engineers, coating knowledge and support for custom programs. Buyers do not only ask whether a supplier has a reamer. Buyers ask whether the supplier can hold bore size after tool wear, support a trial on the customer machine and provide a realistic cost per accepted part calculation.

POTENTIAL

Potential companies include NACHI-FUJIKOSHI, ISCAR, Seco Tools, regional PCD specialists and reconditioning-focused tool rooms that serve EV, aerospace and medical clusters. Smaller specialists can win by owning difficult materials, offering quick recoating loops and building relationships with job shops that large suppliers may not service closely.

Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

EV and precision aluminum programs increase bore-quality demand | 5.5% | Asia-Pacific, Europe and North America | Motor housings, thermal plates, brake bodies and aluminum castings | Supports demand for PCD, diamond-coated and coated carbide tools that stabilize diameter and finish. |

Aerospace, medical and semiconductor equipment require validated hole finishing | 5.0% | U.S., Japan, Germany and South Korea | Hydraulic blocks, implants, vacuum plates and precision fixtures | Raises demand for documentation, traceability and material-specific process support. |

Automation increases the value of repeatable finishing processes | 4.6% | High-volume machining plants globally | Automated cells, 5-axis machining centers and Swiss-type lathes | Improves economics for premium tools where stable bore quality reduces inspection queues. |

Localized manufacturing strengthens service-led supplier selection | 4.2% | U.S., Mexico, India, Eastern Europe and Southeast Asia | Local regrinding, custom specials and launch assistance | Rewards suppliers with nearby engineering and repair capability. |

Bore Capability Audits Are Replacing Simple Tool Buying

Automated assembly lines are no longer tolerant of hole variation because robots, gauges and press-fit operations cannot correct ovality, burrs or chamfer inconsistency after the fact. A rejected bore can push an entire batch into inspection and rework. EV component plants show the shift clearly. Motor housings, inverter cases and battery thermal parts can contain cast surfaces, thin walls and long-reach holes. Hole finishing tools must control chatter and chip evacuation while maintaining cycle time.

Restraint Impact Analysis

| Restraint | Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

Custom finishing tool cost can slow purchase approval | 4.2% | Prototype and low-volume programs | Special reamers, counterbores, stepped tools and long-reach tools | Delays investment until volume and design stability are clear. |

Raw material and coating cost volatility raises quote risk | 3.8% | Carbide, PCD, cobalt and tungsten-exposed supply chains | Solid carbide, PCD and diamond-coated tools | Shortens quote validity and increases forecast-backed purchasing. |

Skilled grinding and application-engineering shortages limit service speed | 3.6% | Custom toolmakers and regional repair providers | Regrind planning, tool repair and emergency specials | Creates lead-time pressure and favors suppliers with trained tool-room capacity. |

Legacy machining habits slow premium-tool adoption | 3.3% | Job shops and cost-sensitive plants | Catalogue reamers, manual deburring and separate inspection loops | Requires clearer cost-per-accepted-hole justification. |

Custom Tool Lead Times Can Slow Production Launches

Custom hole finishing tools require precise design work because small geometry errors can create oversize bores, poor cylindricity or chatter. Special diameters, stepped features, long reaches and coolant delivery routes need engineering review. Lead-time pressure is highest in EV, aerospace and medical projects where part designs change close to validation. Suppliers can reduce risk through modular shanks, replaceable-head programs, local regrind centers and early design-for-manufacturability support.

Segment Analysis

The global hole finishing tools market is segmented based on tool grade, machine type, workpiece detail, end-user and region.

Solid Carbide and PVD Coated Carbide Are Becoming the Workhorse Premium Choice

Solid carbide provides rigidity and dimensional control for many precision bores. PVD coatings improve wear behavior in stainless steel, alloy steel and harder ferrous workpieces where uncoated carbide can lose edge quality too quickly. Supplier differentiation comes from geometry, coolant delivery and coating selection rather than carbide alone. Sales teams should position coated carbide through accepted bore cost.

PCD and Diamond Coated Tools Are Becoming Strategic in Aluminum Use Cases

PCD and diamond-coated tools serve high-volume non-ferrous programs where abrasive aluminum-silicon alloys and long runs create severe wear. EV housings, compressor parts and high-precision aluminum plates can justify the price premium. Application engineering becomes part of the product because PCD performs well when the process is stable but poor fixturing or interrupted cuts can damage the edge.

Automotive and Electric Vehicles Lead Bore-Quality Demand

Automotive and electric vehicles remain a priority end-user base because bore quality affects motor housings, brake bodies, e-drive systems, thermal plates and precision aluminum castings. Suppliers with material-specific tool recommendations can protect cycle time and reduce inspection delays.

Legacy Hobbing Assets Slow New Process Adoption

Many gear shops already own depreciated hobbing and shaping machines. Existing operators, fixtures, inspection routines and resharpening relationships support those assets. New skiving capability can be difficult to justify unless the program has the right volume and complexity. Suppliers need to show payback through fewer operations, lower work-in-process, shorter cycle time and quality gains. A complete process proposal with machine builders and inspection providers gives customers more confidence than a standalone tool quotation.

Geographical Penetration

U.S. Hole Finishing Tools Market Landscape

The U.S. market is attractive because customers value documentation, local support and production continuity. Defense, aerospace, medical devices, semiconductor equipment and heavy machinery buyers cannot afford long downtime when a critical bore moves out of specification. Tariff and shipping risk have made local inventory, quick servicing and domestic repair partners more important in supplier selection.

Japan Hole Finishing Tools Market Outlook

Japan should be treated separately because buyer behavior is different from pure volume markets. Precision machinery, automotive suppliers, bearings, robotics and machine tool builders reward consistency, long-term support and trusted engineering relationships. Low price alone rarely wins if it increases uncertainty inside a precision production environment.

Asia-Pacific Hole Finishing Tools Market Trends

Asia-Pacific remains central because manufacturing scale is spread across automotive, electronics, industrial machinery, construction equipment, shipbuilding and precision component ecosystems. China offers volume and price competition, India is investing in mobility and defense, Japan values accuracy and South Korea links tooling demand with EVs, shipbuilding and electronics. Suppliers should avoid one broad Asia-Pacific strategy. Hole finishing demand must be mapped by machine type, material group, customer sector and local service expectations.

Competitive Landscape

- Competition is fragmented at product level but more concentrated for global accounts and technically demanding applications. Large suppliers win where they offer breadth, application engineers, coatings, digital infrastructure and cross-regional support.

- Specialist suppliers win where they solve difficult materials faster or provide local service that large companies cannot match. Emergency regrinding, quick custom turnaround and strong coolant or chip-evacuation guidance can outweigh brand scale in customer clusters.

- Distributor influence remains strong for standard reamers and countersinks. Direct manufacturer relationships become more important for custom tools, high-value production programs and sensitive materials.

- Competitive benchmarking should track custom quote speed, local regrind capability, coating access, drawing support, machine compatibility knowledge, inventory transparency and ability to provide trial evidence.

MAJOR PAIN POINTS

- Gap between tool selection and production performance when procurement compares price while production carries the cost of scrap, rework, downtime and inspection queues.

- Long lead times for custom geometry, coating, inspection and precision grinding when customer drawings change late in the program.

- Weak visibility into replacement timing because many plants service high-value tools only after bore quality begins drifting.

- Shortage of skilled grinding labor and application engineers capable of diagnosing chatter, chip evacuation, coolant delivery and machine-condition issues.

- Raw material and coating cost volatility that makes quotation validity difficult for custom solid carbide, PCD and diamond-coated tools.

- Limited local repair and reconditioning options in fast-growing manufacturing clusters.

- Difficulty comparing catalogue reamers, custom specials, replaceable-head systems and secondary finishing routes without a cost-per-hole model.

RECENT DEVELOPMENTS

- April 2026: Sandvik Coromant launched GC1240 milling grade, enabling higher-speed stainless-steel finishing with reduced coolant consumption and longer predictable tool life.

- March 2026: Sandvik Coromant introduced CoroMill MR20, delivering stable profiling, improved tool life and enhanced finishing performance in difficult aerospace materials.

- January 2026: Sandvik Coromant launched CoroPlus Tool Supply, improving tooling inventory visibility, automation and machining productivity for precision hole-finishing operations.

- October 2025: Mitsubishi Materials launched DXAS exchangeable-head carbide drills within TRISTAR series, supporting versatile and efficient deep-hole drilling use cases.

- October 2025: Walter AG launched 1,600 machining products, including advanced drilling and hole making solutions enhancing productivity and process reliability.

- July 2025: Mitsubishi Materials introduced TRISTAR DVAS solid-carbide drills up to 20mm, strengthening high-precision drilling and hole-finishing capabilities.

- June 2025: OSG Corporation highlighted environmentally friendly tooling technologies and advanced drilling solutions within global SHAPE it manufacturing magazine edition.

KEY PROCUREMENT PRIORITIES AND BUYER EVALUATION CRITERIA

- Buyers are evaluating suppliers on tool-design support, material-specific recommendations, expected tool life, regrind economics, local service response and proof of bore-quality stability.

- Automotive and EV manufacturers prioritize cycle time, diameter control, burr reduction, stable supply and tooling economics for motor housings, brake bodies, thermal plates and aluminum casting use cases.

- Aerospace, medical and semiconductor equipment buyers prioritize traceability, documentation, process control, inspection records and repair discipline because tool failure can affect safety-critical or high-value components.

- Procurement teams increasingly require a cost-per-accepted-hole view that separates new tool cost, grinding, coating, inspection, trial support, repair, regrind and emergency special premiums.

- Preferred suppliers are those that can support both engineering and procurement conversations, converting price discussions into production-risk and lifecycle-value decisions.

ANALYST VIEW / OPINION

- DataM expects the strongest suppliers to behave like process partners rather than tool sellers. Customers are paying for confidence that bore quality will remain stable at production speed.

- Regional service depth will become a stronger differentiator as tariffs, shipping uncertainty and shorter product launches make local sharpening, repair and application support commercially important.

- Market winners will combine technical evidence, digital customer convenience and lifecycle economics. Suppliers that can prove cost per accepted hole and maintain service records will have a stronger argument with engineering and procurement teams.

Asia-Pacific should remain the volume center while Japan, Germany and the U.S. remain premium markets for high-confidence tools and documented reconditioning programs.

TARGET AUDIENCE

| INDUSTRY | WHO SHOULD BUY THIS REPORT? | REASON TO BUY THIS REPORT |

Automotive & EV Manufacturers | Engine Machining Teams, Production Engineers, Manufacturing Heads | Analyze hole finishing tool demand for engine blocks, EV housings and precision bore use cases. |

Aerospace & Defense Companies | Aerospace Machining Engineers, Tooling Specialists, Precision Manufacturing Teams | Evaluate advanced reaming, honing and boring solutions for aerospace-grade alloys and tight tolerances. |

Industrial Machinery Manufacturers | Plant Operations Managers, CNC Programming Teams, Industrial Engineers | Optimize hole finishing operations, machining precision and tool lifecycle management. |

General Engineering & Metal Fabrication Companies | Workshop Supervisors, Production Planning Teams, Fabrication Managers | Identify efficient hole finishing tools for large-scale precision machining and metalworking operations. |

CNC Machine Tool Manufacturers | Product Development Teams, Automation Engineers, Strategic Alliance Teams | Understand demand trends for CNC-compatible hole finishing solutions and smart machining integration. |

Oil & Gas Equipment Manufacturers | Heavy Machining Teams, Reliability Engineers, Procurement Managers | Assess wear-resistant hole finishing tools for valves, drilling systems and pipeline equipment manufacturing. |

Medical Device Manufacturers | Precision Component Engineers, Micro-Machining Teams, R&D Departments | Study ultra-precision hole finishing technologies for surgical instruments and miniature medical components. |

Industrial Automation & Smart Factory Companies | Industry 4.0 Teams, Automation Integration Engineers, Smart Manufacturing Consultants | Evaluate integration opportunities between hole finishing tools, CNC systems and automated machining platforms. |

Contract Manufacturing & Job Shops | CNC Workshop Owners, Production Supervisors, Cost Optimization Teams | Assess profitable precision machining segments and tooling investments for high-accuracy hole finishing use cases. |

Investors, Private Equity & Consulting Firms | Investment Analysts, Industrial Consultants, Market Intelligence Teams | Evaluate market growth opportunities, competitive landscape and technology adoption trends in hole finishing tools. |

WHY CHOOSE DATAM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

WHAT DATAM UNIQUELY PROVIDES

- Client-ready views that connect tooling demand with part programs, machine type, workpiece material, region, trade flows and supplier capability.

- Bottom-up market modeling using customer interviews, distributor checks, HS trade codes, machine installation patterns, tool-grade mapping and end-equipment analysis.

- Supplier scorecards covering quote speed, regrind capability, coating access, machine compatibility knowledge, service depth and lifecycle support.

- Procurement intelligence covering cost-per-hole economics, pricing trackers, sourcing risk, lead-time benchmarks and reconditioning models.

- Regional opportunity mapping for automotive, EV, aerospace, defense, semiconductor equipment, medical, rail and precision machinery demand clusters.

- Application-fit matrices that help clients compare catalogue tools, engineered specials, replaceable-head systems, honing, burnishing and deburring routes on economic and operational grounds.

- Risk-mitigation roadmaps covering raw material exposure, coating queues, local repair capacity and backup supplier options.

QUESTIONS THIS REPORT ANSWERS

- What is the current and forecast market size of the global hole finishing tools market through 2035?

- Which regions will dominate by 2030 and why does Asia-Pacific remain the leading growth engine?

- Which machine types, tool grades and end-user use cases are scaling fastest?

- How are EV, aerospace, medical and semiconductor equipment programs changing demand for precision bore quality?

- Which companies are best positioned in custom tooling, service, repair and lifecycle support?

- How should buyers compare catalogue reamers, engineered specials, replaceable-head systems, honing, burnishing and secondary finishing alternatives?

- What regulatory, quality and documentation expectations are accelerating supplier qualification requirements?

- What is the investment outlook for precision grinding, reconditioning, coating and regional service capacity?

- Where can DataM support supplier scorecards, pricing trackers, opportunity mapping and procurement strategy?