Healthcare Cybersecurity Market Size

The global healthcare cybersecurity market reached US$23.31 billion in 2025 and is expected to reach US$107.98 billion by 2035, growing at a CAGR of 16.5 % during the forecast period of 2026-2035. The global healthcare cybersecurity market encompasses a wide array of technologies, solutions, and practices aimed at safeguarding sensitive patient data, medical devices, and healthcare IT systems from digital threats such as ransomware, phishing, and data breaches. This sector is vital for hospitals, clinics, pharmaceutical companies, telehealth providers, and other organizations, as it ensures the confidentiality, integrity, and availability of electronic health records (EHRs), medical devices, and critical healthcare infrastructure.

Market growth is being driven by several key factors, including the rapid digitalization of healthcare services, the widespread adoption of EHRs and telemedicine, and the escalating sophistication and frequency of cyberattacks targeting healthcare institutions. Emerging trends in the healthcare cybersecurity market include the integration of artificial intelligence and machine learning for advanced threat detection, the adoption of zero-trust security models, and the increasing use of cloud security solutions.

Opportunities in this market are substantial, as healthcare organizations seek robust solutions to address new and evolving threats, secure remote care platforms, and comply with stricter regulations. The ongoing digital transformation of healthcare, combined with the need to protect against quantum computing threats and supply chain vulnerabilities, positions cybersecurity as a strategic imperative for ensuring patient trust and operational continuity in the global healthcare sector.

Key Takeaways

- The healthcare cybersecurity market size in 2026 is estimated at US$27.15 billion, highlighting sustained investment momentum across healthcare providers.

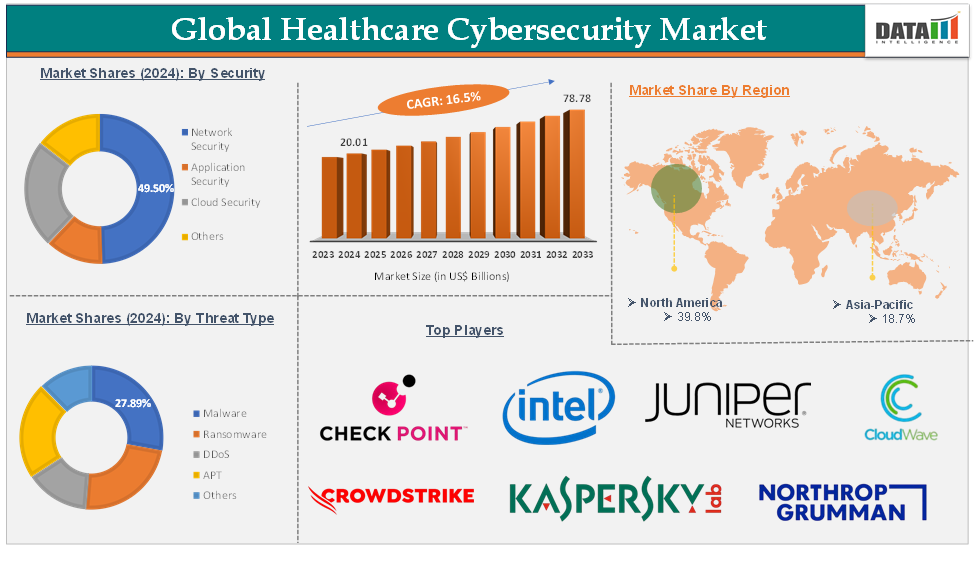

- Network security remains the largest security category, accounting for 49.5% of total market revenue in 2024, reflecting the importance of protecting interconnected healthcare environments.

- North America captured 39.8% of global revenue in 2024 due to strong healthcare digitization, regulatory mandates, and high cybersecurity spending.

- Asia-Pacific accounted for 18.7% of market revenue and represents a major expansion opportunity as healthcare infrastructure modernization accelerates.

- Healthcare organizations experienced an unprecedented cyber threat environment, with approximately 168 million healthcare records exposed or compromised in 2024.

- Compliance requirements are becoming a major purchasing trigger, with healthcare providers investing in cybersecurity to meet HIPAA, HITRUST, NIST, GDPR-inspired frameworks, and emerging regional regulations.

- Enterprise buyers increasingly prefer integrated cybersecurity platforms combining network security, cloud protection, endpoint security, threat intelligence, and AI-driven monitoring capabilities.

Global Healthcare Cybersecurity Market – Executive Summary

Global Healthcare Cybersecurity Market Dynamics: Drivers

Increasing cyberattacks and concerns related to security and privacy

The surge in cyberattacks and mounting privacy concerns are key drivers fueling the growth of the global healthcare cybersecurity market. As healthcare organizations increasingly adopt digital technologies and connected devices, they face escalating threats from sophisticated cybercriminals targeting sensitive patient data and critical IT systems.

In 2024, the industry experienced a record-breaking 168 million healthcare records exposed, stolen, or improperly disclosed, representing a dramatic rise from previous years. This included 26 data breaches, each affecting over 1 million records, with the largest single incident impacting more than 11 million individuals.

The majority of these breaches involved hacking incidents often linked to ransomware or extortion attempts, though some stemmed from unauthorized disclosures, such as the use of tracking pixels on healthcare websites. High-profile cases, like the breach at Kaiser Permanente, underscored the risks associated with online technologies, as personal information was inadvertently shared with third parties when patients accessed digital services.

In 2024, while the number of reported healthcare data breaches showed a slight decline, the total number of compromised records soared, driven by unprecedented incidents such as the Change Healthcare ransomware attack that affected an estimated 190 million individuals.

These trends highlight the urgent need for advanced cybersecurity measures in healthcare, as organizations must not only defend against increasingly complex attacks but also address regulatory requirements and protect patient trust in an environment where privacy risks are rapidly evolving.

Global Healthcare Cybersecurity Market Dynamics: Restraints

Lack of a cybersecurity policy framework in healthcare organizations

A lack of a comprehensive cybersecurity policy framework in healthcare organizations acts as a significant restraint on the growth and effectiveness of the global healthcare cybersecurity market. Without standardized policies and structured frameworks, healthcare providers often struggle to implement consistent security controls, risk management practices, and incident response protocols across their operations.

This inconsistency leaves organizations vulnerable to cyber threats, increases the likelihood of data breaches, and makes it difficult to comply with evolving regulatory requirements such as HIPAA, HITRUST, and the NIST Cybersecurity Framework. The absence of a unified policy framework also hampers interoperability and secure data exchange within increasingly digital and interconnected healthcare environments, as highlighted by studies on health data spaces and cross-border data sharing.

Furthermore, when technology and service providers supporting healthcare infrastructure are not held to uniform cybersecurity standards, it creates gaps in protection and accountability across the supply chain. These challenges not only expose healthcare organizations to greater cyber risks but also slow the adoption of advanced cybersecurity solutions, ultimately restraining market growth and undermining efforts to safeguard patient data and critical healthcare services.

Strategic Takeaways for Decision-Makers

Healthcare remains one of the most targeted sectors globally due to the high value of patient data and the critical nature of healthcare operations. Cybercriminals increasingly exploit ransomware, malware, advanced persistent threats (APTs), distributed denial-of-service (DDoS) attacks, and supply chain vulnerabilities.

The threat landscape is evolving beyond traditional perimeter attacks. Connected medical devices, cloud-hosted applications, telemedicine platforms, third-party software providers, and healthcare IoT networks have expanded the attack surface significantly.

The Change Healthcare ransomware incident demonstrated how attacks against a single healthcare technology provider can create operational disruptions across the broader healthcare ecosystem. As healthcare organizations continue integrating digital services, cybersecurity spending is increasingly linked to business continuity, patient safety, and operational resilience.

Growth Catalysts Reshaping Market Demand

Escalating Ransomware and Data Breach Incidents

Healthcare organizations continue to experience some of the highest cybersecurity risks among all industries. The exposure of approximately 168 million healthcare records during 2024 highlights the growing scale of cyber threats facing hospitals, clinics, insurers, and digital health providers.

The increasing sophistication of attackers is encouraging organizations to invest in advanced monitoring, threat intelligence, security operations centers (SOCs), and automated response capabilities.

Expansion of Digital Healthcare Infrastructure

The adoption of electronic health records, telehealth services, connected medical devices, remote patient monitoring systems, and cloud-based healthcare applications continues to expand globally.

Every new digital touchpoint creates additional cybersecurity requirements, driving demand for comprehensive security platforms capable of protecting data across multiple environments.

Rising Compliance Requirements

Healthcare cybersecurity compliance requirements are becoming more stringent worldwide. Organizations are under pressure to comply with frameworks such as HIPAA, HITRUST, NIST Cybersecurity Framework, and emerging healthcare-specific regulations across Asia-Pacific and Europe.

Regulatory compliance increasingly influences procurement decisions, making cybersecurity investments essential for both risk management and legal compliance.

Adoption Maturity Across Healthcare Organizations

Healthcare cybersecurity enterprise adoption by sector varies considerably.

Large hospital networks and integrated healthcare systems are typically in advanced adoption stages, deploying AI-driven security platforms, zero-trust frameworks, and cloud security architectures.

Pharmaceutical and biotechnology companies are increasing investments in intellectual property protection and research data security.

Telehealth providers and digital health platforms are prioritizing application security and identity access management due to growing volumes of patient interactions.

Smaller clinics and outpatient facilities often remain in earlier adoption stages due to budget constraints and limited cybersecurity expertise, creating substantial future market opportunities.

Pricing and Adoption Trends

Healthcare cybersecurity pricing and adoption trends are shifting from hardware-centric models toward subscription-based and managed security services.

Cloud-delivered security platforms, Security-as-a-Service (SECaaS), managed detection and response (MDR), and endpoint protection subscriptions are gaining traction because they reduce upfront capital expenditure and provide continuous protection.

Healthcare organizations increasingly evaluate cybersecurity investments based on measurable outcomes, including reduced breach risk, regulatory compliance readiness, operational uptime, and incident response effectiveness.

Zero-Trust Architecture Gains Strategic Importance

Zero-trust architecture is becoming a foundational cybersecurity strategy within healthcare organizations.

Rather than assuming users or devices are trusted within a network perimeter, zero-trust frameworks continuously verify identities, access permissions, device health, and behavioral patterns before granting access to critical healthcare systems.

The growing use of remote work environments, telemedicine services, cloud applications, and connected medical devices is accelerating healthcare adoption of zero-trust security models.

Organizations implementing zero-trust architectures are better positioned to mitigate insider threats, ransomware attacks, credential theft, and unauthorized access incidents.

Market Opportunities

Healthcare cybersecurity opportunities extend well beyond traditional hospital environments.

Outpatient care facilities are rapidly adopting healthcare IT systems, creating substantial demand for scalable cybersecurity solutions designed for decentralized care delivery models.

Medical device manufacturers can benefit from rising demand for embedded cybersecurity capabilities as regulators and healthcare providers place greater emphasis on device security.

Technology vendors offering AI-powered threat detection, cloud-native security platforms, identity access management solutions, and healthcare-specific compliance tools are positioned to capture significant market share through 2035.

Regional providers in emerging markets have opportunities to address unmet cybersecurity needs among healthcare institutions undergoing digital transformation while operating with limited internal security resources.

Segmentation Analysis

Segmented by Threat Type (Malware, Ransomware, DDoS, APT, Others), by Solution (IAM, Antivirus/Antimalware, Firewall, Encryption, Tokenization, Others), by Security (Network Security, Application Security, Cloud Security, Others), by Deployment (On-Premises, Cloud-Based), by End User (Hospitals, Ambulatory Surgical Centers, Specialized Clinics and Others), and by Region, Share, Trends, and Forecast to 2035.

By Security

Network security accounted for the largest market share of 49.5% in 2024. Healthcare providers continue to prioritize investments in network visibility, firewall technologies, endpoint protection, VPN encryption, and threat monitoring to protect increasingly connected healthcare environments.

Application security and cloud security are expected to record strong growth as healthcare organizations migrate critical workloads to cloud platforms and expand digital patient engagement services.

By Solution

Identity and Access Management (IAM), encryption technologies, firewalls, tokenization solutions, and antivirus platforms remain core components of healthcare cybersecurity strategies.

IAM solutions are becoming increasingly important as organizations adopt zero-trust architectures and seek tighter control over access to sensitive patient data.

By Deployment

Cloud-based cybersecurity solutions are gaining momentum due to scalability, lower implementation costs, centralized management capabilities, and continuous security updates.

On-premises deployments continue to serve organizations with strict regulatory or operational requirements but face increasing competition from cloud-native platforms.

By End User

Hospitals remain the largest cybersecurity buyers due to their extensive digital infrastructure, patient data volumes, and exposure to cyber threats.

Telehealth providers, healthcare facilities, pharmaceutical companies, biotechnology firms, and insurance providers are also increasing cybersecurity investments to support digital operations and regulatory compliance.

Healthcare Cybersecurity Regional Analysis

North America

North America held approximately 39.8% of global market revenue in 2024 and continues to represent the largest regional market.

The region benefits from mature healthcare infrastructure, widespread EHR adoption, extensive use of connected medical devices, and strong regulatory oversight. The high frequency of cyberattacks has further accelerated cybersecurity spending among healthcare organizations.

Government initiatives, advanced cybersecurity vendor ecosystems, and increasing AI adoption continue to support market expansion across the United States and Canada.

Europe

Europe maintains a strong position due to growing regulatory oversight, cross-border health data initiatives, and increasing investments in healthcare digitalization.

Healthcare providers across major European countries are expanding cybersecurity budgets to address privacy requirements, ransomware risks, and secure health information exchange frameworks.

The European Commission's cybersecurity action plan for hospitals and healthcare providers reflects the region's focus on strengthening healthcare cyber resilience.

Asia-Pacific

Asia-Pacific is emerging as one of the most dynamic markets for healthcare cybersecurity.

Rapid digital transformation across China, India, Japan, South Korea, Singapore, and Southeast Asia is increasing demand for advanced security solutions. Government-led healthcare modernization programs and stricter data protection regulations are encouraging healthcare providers to strengthen cybersecurity capabilities.

The introduction of cybersecurity guidelines for medical devices and healthcare systems across several countries is expected to further stimulate investment through 2035.

Global Healthcare Cybersecurity Market – Competitive Landscape

The major global players in the healthcare cybersecurity market include Checkpoint Software Technologies Inc., Intel Corporation, Juniper Networks Inc., Cloudwave Sensato Cybersecurity, CrowdStrike Holdings, Kaspersky Labs, Northrop Grumman Corporation, Palo Alto Networks, Broadcom, and Sophos Ltd., among others.

Key Developments

April 2026: The United States increased investments in healthcare cybersecurity infrastructure and digital health protection initiatives, supporting stronger defenses against ransomware, data breaches, and cyber threats targeting healthcare organizations.

March 2026: Japan strengthened healthcare data security regulations and cybersecurity frameworks, encouraging hospitals and healthcare providers to adopt advanced security solutions for protecting patient information and connected medical systems.

February 2026: Palo Alto Networks, Inc. expanded its healthcare cybersecurity capabilities through advanced threat detection, cloud security, and network protection solutions designed for healthcare environments.

January 2026: Healthcare organizations increased investments in zero-trust security architectures, identity management platforms, and endpoint protection technologies to safeguard sensitive patient data and clinical systems.

December 2025: Cybersecurity vendors accelerated development of AI-powered threat intelligence and security monitoring solutions to help healthcare providers identify, prevent, and respond to evolving cyber threats.

November 2025: CrowdStrike Holdings, Inc. strengthened its healthcare-focused cybersecurity offerings through enhanced endpoint protection and threat hunting capabilities for hospitals and healthcare networks.

October 2025: Industry participants expanded deployment of cloud security, data encryption, and security information and event management (SIEM) solutions to support secure digital healthcare operations.

September 2025: India increased investments in healthcare IT modernization and cybersecurity infrastructure, supporting protection of electronic health records, telehealth platforms, and connected medical devices.

July 2025: Fortinet, Inc. advanced integrated cybersecurity solutions designed to improve network security, operational resilience, and regulatory compliance across healthcare organizations.

May 2025: Healthcare providers accelerated adoption of cybersecurity training programs and risk management frameworks to strengthen organizational preparedness against phishing, ransomware, and insider threats.

March 2025: Strategic collaborations between healthcare institutions, cybersecurity firms, and government agencies expanded efforts to improve cyber resilience, incident response capabilities, and protection of critical healthcare infrastructure.

Global Healthcare Cybersecurity Market – Scope

| Metric | Details |

| Market Size (2025) | US$ 23.31 Billion |

| Market Size (2035) | US$ 107.98 Billion |

| CAGR (2026-2035) | 16.50% |

| Historic Years | 2023-2024 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Segments Covered | Threat Type, Solution, Security, Deployment, End User |

| Leading Region | North America |

| Fastest Growing Region | Asia-Pacific |

The global healthcare cybersecurity market report delivers a detailed analysis with 78 key tables, more than 80 visually impactful figures, and 173 pages of expert insights, providing a complete view of the market landscape.

Suggestions for Related Report

For more healthcare IT-related reports, please click here