Floor Cleaning Robots Market Size

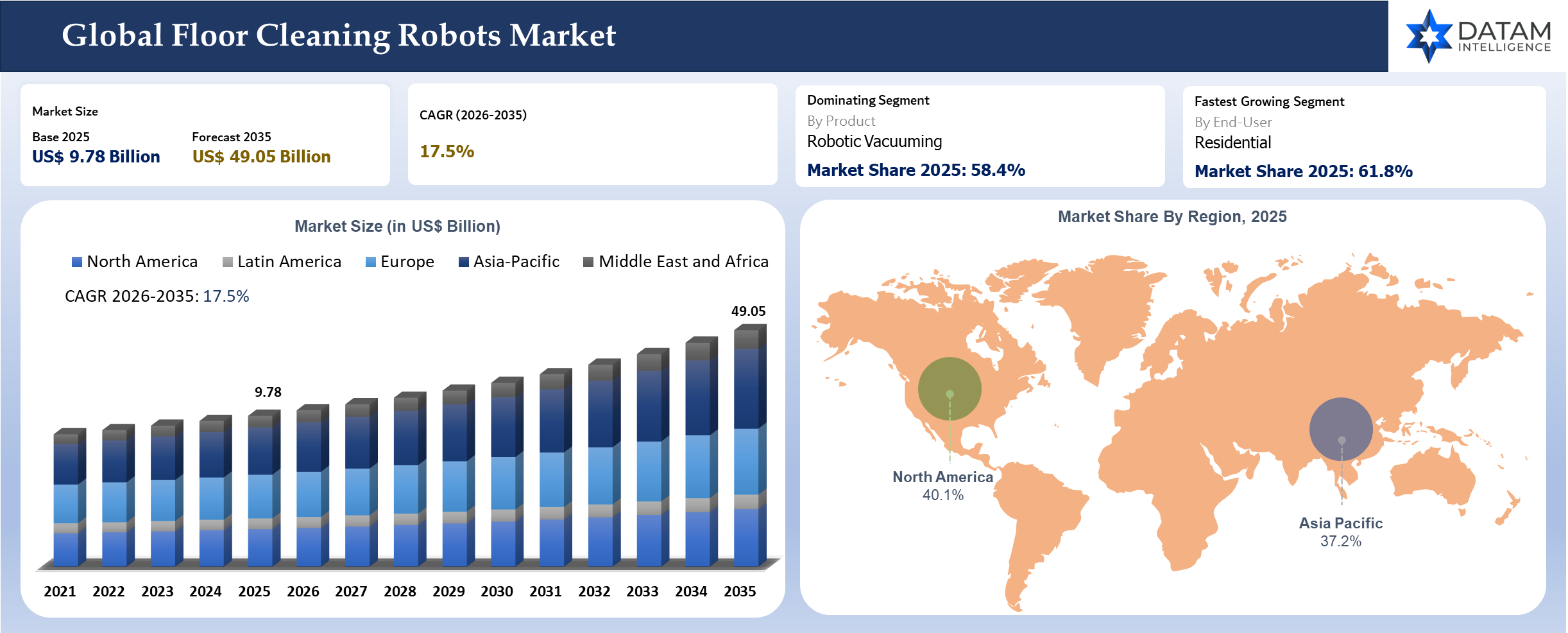

The global floor cleaning robots market reached US$ 9.78 billion in 2025 and is expected to reach US$ 49.05 billion by 2035, growing with a CAGR of 17.5% during the forecast period 2026-2035. Growing urbanization trends, limited residential area size and the increase in number of two-salary families will speed up the growth of need for autonomous cleaning solutions that require less manual labor. Home automation systems have already become common, with connected devices penetrating both developing and advanced countries. As per International Telecommunication Union, over 5.5 billion people in the world used the Internet in 2024, which contribute to the growing popularity of robot cleaners integrated with IoT and AI-controlled home systems using smartphones. In terms of robotization trends, the International Federation of Robotics pointed out continuous development of the application of robots in various sectors, especially the field of domestic service robots owing to improvements in such technologies as sensors, SLAM navigation, LiDAR mapping and edge AI.

The commercial adoption is steadily rising due to the considerable investments by corporations, hospitals, airports, chain stores and hospitality businesses in automation technologies aimed at maintaining hygiene and cutting costs. The lack of labor in the janitorial and facility maintenance sectors of North America, Europe, Japan and South Korea is compelling businesses to implement robots capable of functioning independently without requiring human interaction. Governments and public sector organizations are giving priority to sanitary procedures following their realization about the significance of hygiene and the necessity for infection prevention strategies. For instance, the World Health Organization is always emphasizing the need for appropriate hygiene practices in health institutions and public areas, making sure there is sustainable investment in robot cleaners. Intelligent manufacturing and robotics deployment programs in countries such as China, Japan, Germany and South Korea are stimulating growth in the robotics sector through financial commitment to AI applications and automation endeavors. Robotics industry growth strategies in China and innovations in service robotics in Japan are raising competition among robot floor cleaner manufacturers worldwide in terms of coming up with advanced devices equipped with navigational and voice assistant capabilities.

Floor Cleaning Robots Industry Trends and Strategic Insights

- High-end machines equipped with LiDAR and SLAM systems are able to create real-time indoor maps with millimeter precision, thus reducing collision risks and optimizing cleaning performance. According to WIPO data, the combination of Japan, South Korea and China is responsible for close to 60% of all patents related to domestic robots filed worldwide in 2024, implying the Asia-Pacific superiority in robotics innovation.

- The rise in the commercial application of robotics technology has been witnessed amid efforts by organizations to address growing labor expenses and inefficiencies in their facilities management processes. Large airports, shopping malls, hospitals and warehouses have increasingly favored using self-driven floor scrubbers and robot vacuum cleaners in order to maintain sanitary standards without escalating labor expenditures.

Key Takeaways

- Robotic vacuum cleaners continue to dominate the floor cleaning robots market, supported by rising consumer demand for automated home cleaning, smart home integration and growing adoption of AI-powered navigation technologies.

- Artificial intelligence, LiDAR mapping, computer vision and object recognition technologies are becoming major competitive differentiators as consumers increasingly prioritize cleaning accuracy, obstacle avoidance and autonomous operation.

- Residential applications remain the largest revenue contributor, driven by rising urbanization, dual-income households, increasing disposable income and growing preference for time-saving household automation solutions.

- Commercial adoption is accelerating across hotels, healthcare facilities, offices, airports, retail centers and educational institutions, where robotic cleaning solutions help reduce labor dependency, improve operational efficiency and support hygiene standards.

- Asia-Pacific continues to lead global demand due to strong consumer electronics manufacturing capabilities, high smart home adoption rates and expanding middle-class populations in countries such as China, Japan and South Korea.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 9.78 Billion | |

| 2035 Projected Market Size | US$ 49.05 Billion | |

| CAGR (2026-2035) | 17.5% | |

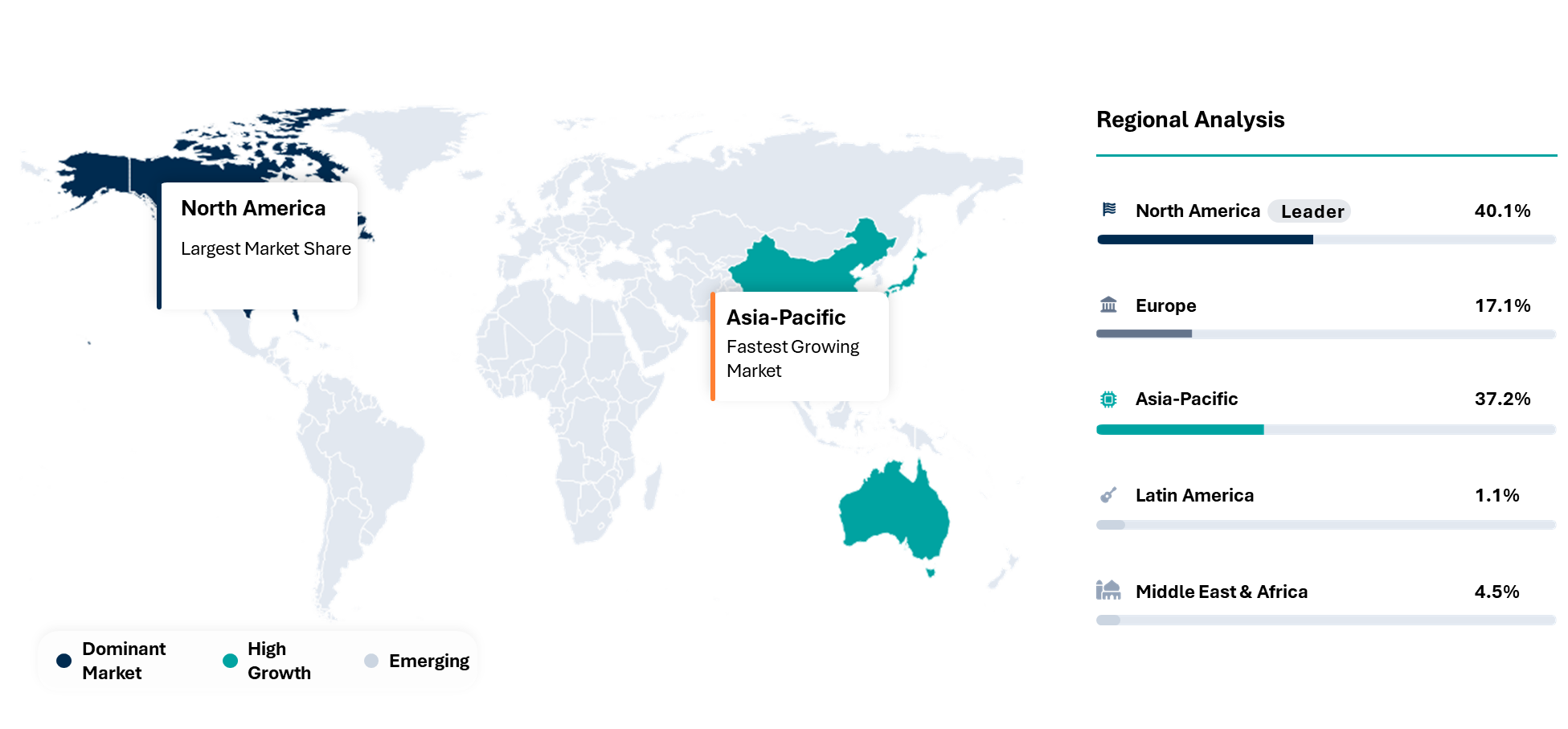

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Product | Robotic Scrubbers, Robotic Sweepers, Robotic Vacuuming | |

| By Cleaning Function | Scrubbing, Sweeping, Vacuuming, Hybrid Cleaning | |

| By Cleaning Area | 1000-2000 ㎡, 2000-5000 ㎡, More than 5000 ㎡ | |

| By Operation Mode | Semi Autonomous Robots, Fully Autonomous Robots, Remote Assisted Robots | |

| By Deployment Model | Ownership Model, Raas, Lease And Managed Service | |

| By Navigation | LiDAR SLAM, Vision AI, Sensor Fusion | |

| By Docking | Manual Charging, Auto Charging, Service Dock | |

| By Floor Type | Hard Floors, Industrial Floors, Carpeted Floors | |

| By Sales Channel | Direct OEM Sales, Distributor Sales, FM Channel, Online Retail | |

| By End-User | Residential, Commercial, Healthcare, Industrial | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Strategic Indicators For Floor Cleaning Robots

High Regulation Impact

The market is under heavy regulation regarding cybersecurity for connected devices, shipping lithium batteries, AI-driven mapping of interiors and data transfer across borders. In 2025, for example, there was an increase in the U.S. compliance requirements in respect of smart home devices that gather spatial data from within households, which directly affected Chinese suppliers, such as Roborock and ECOVACS Robotics. The Cyber Resilience Act and Ecodesign guidelines of the European Union now require changes to firmware update policies, design principles for repairability and energy consumption. The Japanese authorities have tightened regulations regarding household robotics concerning autonomous navigation features, while India has broadened its rules related to the BIS certification scheme for electronics in the realm of imported IoT gadgets.

High Investment Activity

The rate of investment witnessed an exponential growth in 2025 due to Chinese robotics manufacturers leveraging their aggressive research and development, implementation of AI-navigation technology and localization of manufacturing processes to improve their market share. China continued to be the top destination for investment, thanks to the vertically-integrated ecosystems of electronics in Shenzhen and Suzhou that allowed the rapid scaling of LiDAR and AI object recognition platforms. South Korea and Japan increased investment in premium automation ecosystems aimed at the elderly and labor shortages for home maintenance. Investment in North America moved away from hardware manufacturing towards intelligent cleaning software.

Supply Chain Disruption

Motor production, LiDAR units, sensor technology, printed circuit board assembly and battery parts were all dominated by Chinese suppliers, thereby increasing reliance risk on North American and European brands. The rise in tariffs imposed by the United States on Vietnam's robotic equipment shipments interrupted earlier efforts made to circumvent China-based import taxes, thereby significantly impacting iRobot. On the other hand, difficulties with the Red Sea route extended delivery times for electronics shipped to Europe. Both Japan and South Korea experienced supply issues for semiconductors caused by growing server demands for AI, which limited sensor access for robotics companies.

Pricing Volatility

Roborock and ECOVACS Robotics brands reduced prices in North America and Europe via online-to-customer platforms, compelling established companies to offer discounts on their stock. At the same time, rising logistics costs, lithium battery shipment fees and higher prices for chip components raised manufacturing costs. Tariff vulnerability for Vietnamese-related goods in the U.S. caused uncertainty in the price levels of high-end robotic vacuum cleaners. Promotional discounts were more prevalent in Germany and France, while Japan witnessed stable premium prices owing to greater smart home implementation.

Procurement Pressure

The push for procurement became significantly heightened in 2025 due to the competition among robotics suppliers for more advanced semiconductors, LiDAR sensors, brushless electric motors and battery management units. The Chinese robotics suppliers enjoyed an advantage in the sourcing process due to their own electronic industry clusters and consolidation of suppliers, whereas suppliers from the United States and Europe had extended procurement cycles and lower bargaining power. It was also a growing trend among premium cleaning robot suppliers for processors that were capable of running artificial intelligence to perform object recognition and navigation tasks, which further strained their availability. Semiconductor suppliers from South Korea and Taiwan focused on maximizing profits by supplying semiconductors to AI servers rather than robotics consumers.

New Technology Adoption

Adoption was at its peak during 2025 due to technology adoption in terms of integrating AI perception sensors, LiDAR mapping technology, self-cleaning mop technology and interoperable Matter-based smart home compatibility. Roborock launched innovative technology of robotic arm-based obstacle navigation, whereas iRobot decided to adopt LiDAR navigation technology due to the dependency on cameras for mapping the environment. Asia, particularly China, is considered as the hub of innovative development owing to commercial cycles of development and availability of components. Japan is concentrating on indoor navigation and small scale robotic engineering. The United States is adopting AI-based customization of machines along with voice assistant capability.

Regional Expansion Opportunity

Asia-Pacific continues to be the most attractive region for business expansion because of the manufacturing supremacy of China, the aging population of Japan and growing use of premium smart homes in South Korea and India. The companies operating in the region take advantage of localized supply chain networks, fast innovation and robotics proliferation in urban areas through the use of e-commerce channels.

The European market offers substantial opportunities for business expansion based on energy efficiency laws, high-end appliances and consumer inclination towards home-cleaning robots. Germany, France and Nordic countries have started adopting AI-powered cleaning robots according to their sustainable smart home renovation programs.

Government Policy Support

Robotic automation received considerable encouragement from governments during 2025 through smart manufacturing, semiconductor localization and AI commercialization initiatives. China further developed robotics automation by means of provincial manufacturing subsidies and intelligent appliance development funds that aided its homegrown leaders, such as ECOVACS Robotics and Roborock. Automation-support measures in Japan were aimed at tackling labor and elderly care issues in the domestic market through automation technologies. Tax benefits to facilitate the export of AI-enabled consumer electronics were offered in South Korea. The government in India incentivized electronics assembly in production-linked incentive schemes to encourage investments in local appliances manufacturing. The EU backed energy-efficient robotic appliances under green transition, although the same had added cybersecurity concerns for multinationals.

Import Export And Pricing Intelligence

The international export flows of robotic floor cleaning devices show an increasing trend towards Chinese centricity for exports, with Vietnam and Malaysia joining as second-level assemblers. The USA and Germany continue to be lucrative markets for imports, whereas regional distributors tend to broaden their supply chain to diminish geopolitical risks.

| Proxy Code | Reporter | Trade Flow | 2024 Trade Value | Interpretation |

| HS 850811 | China | Export | US$ 5.8 Billion | China dominates robotic and smart vacuum exports through vertically integrated electronics manufacturing ecosystems |

| HS 850811 | United States | Import | US$ 2.1 Billion | U.S. demand remains premium-driven despite tariff pressure and supplier diversification initiatives |

| HS 850811 | Germany | Import | US$ 1.3 Billion | Germany leads European smart appliance imports supported by high automation adoption |

| HS 850811 | Vietnam | Export | US$ 980 Million | Vietnam strengthened assembly-based exports benefiting from China-plus-one manufacturing strategies |

| HS 850811 | Japan | Import | US$ 740 Million | Japan’s imports reflect rising smart-home penetration and premium robotics adoption |

Price segregation in premium robotic floor cleaning machines has increased in 2025 due to robust pricing power shown by the most expensive models powered by artificial intelligence. Chinese competitors have increased competition in mid-premium products through the inclusion of automation capabilities in their machines, compelling western firms to adopt promotion-driven pricing tactics.

Company Coverage Preview

The Roborock company has established itself as the world leader in the floor cleaning robot segment, based on quick commercialization of artificial intelligence applications, advanced products and vertical optimization of production processes. Roborock further enhanced its global dominance in 2025 through increasing the usage of LiDAR navigation, artificial intelligence detection of obstacles, robotic manipulation techniques and efficient mopping mechanisms. In contrast to conventional appliance firms, Roborock uses a software-focused product model combining artificial intelligence vision systems, autonomous navigation and IoT interoperability features in high-end user experiences. China is Roborock's primary production base and center for R&D initiatives, while Europe is an essential growth market for premium robotic vacuum adoption.

AI Impact Analysis

Modern AI-assisted navigation systems incorporate functionalities such as obstacle identification, room-based cleaning adjustment, dirt prediction and behavior learning. Companies like Roborock, ECOVACS Robotics and iRobot are focusing more on machine vision capability and less on suction efficiency. The use of AI technology has led to higher operational efficiency by way of predictive maintenance, energy management and accurate mapping. AI-generated data collection has also brought about greater scrutiny regarding household privacy, cybersecurity regulations and data governance in North America and Europe.

Disruption Analysis

Chinese companies such as Roborock, Ecovacs Robotics and Dreame Technology together account for a significant share of global shipment volumes through innovation cycle strategies, aggressive pricing and artificial intelligence technology in product differentials. Sophisticated innovations like robotic arms, self-cleaning docks, edge expansion mops, multiple sensor obstacle detection systems and LiDAR navigational technology are revolutionizing the product functionalities beyond that of a vacuum cleaner. Bankruptcy issues facing companies like iRobot are indicative of the fierce competitive pressures being generated by old players failing to keep up with software-led innovations and lower costs.

The growing consumer expectation towards an entire ecosystem of self-governing cleaning machines that can operate via voice assistants, internet of things and predictive maintenance. In addition, there are other market disruptors such as security issues arising from the use of artificial intelligence, cybersecurity threats and dependency on the cloud which have become important. Emerging markets such as India, Southeast Asia, Eastern Europe and the Middle East are set to become new drivers of growth owing to rapid urbanization, rise in disposable incomes and higher penetration of smart homes.

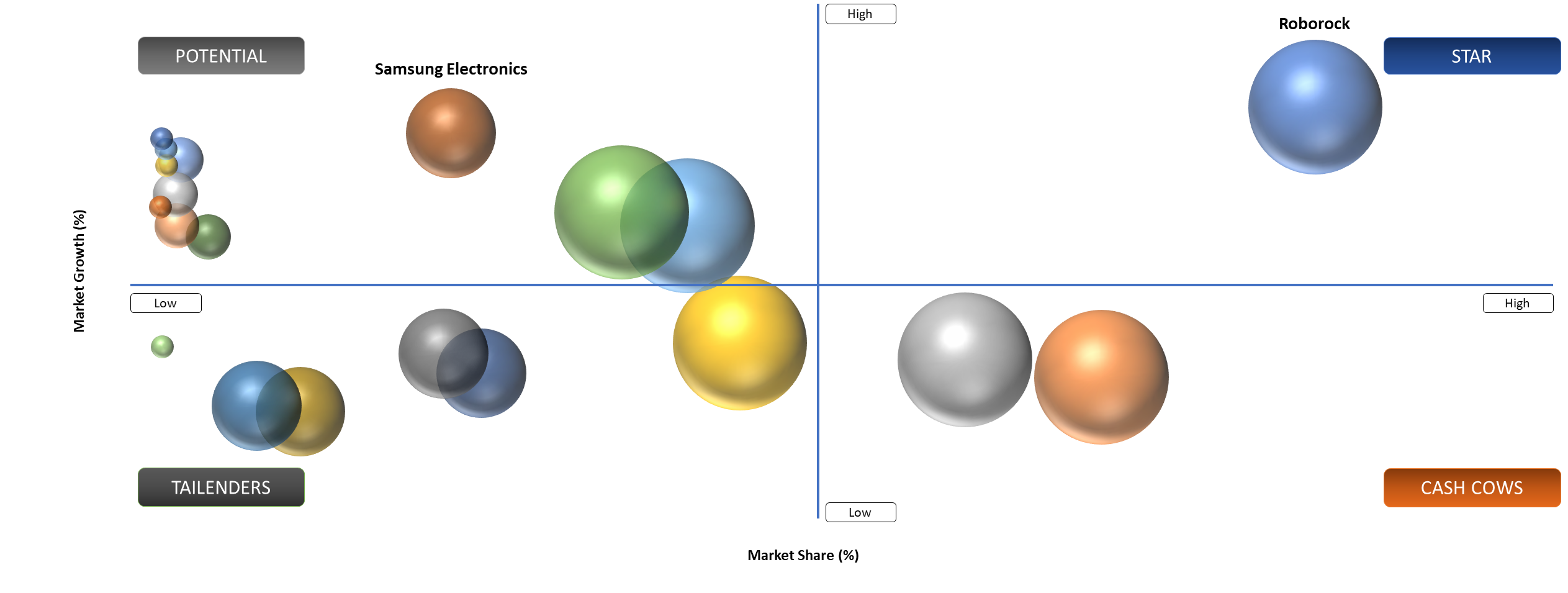

BCG Matrix: Company Evaluation

STAR

The stars players are characterized by advanced technology, high market share and revenues. Roborock holds dominance in the global smart cleaning robot business, thanks to advanced artificial intelligence navigation, robotic arm, LiDAR mapping and high-end docking station features. Ecovacs Robotics has managed to penetrate all corners of the globe using its multifunction vacuum mop products and quick expansion into Europe and Asia. Dreame Technology has become one of the growth leaders due to premium innovations, solid performance on e-commerce platforms and intelligent automation solutions. It has been helped by increasing adoption of smart homes, premium consumerism and artificial intelligence cleaning capabilities.

POTENTIAL

In the quadrant of potential players organizations have good technology competency and expanding distribution systems; however, they have comparatively less global market presence in robotic floor cleaning. Samsung Electronics and LG Electronics have good smart-home environments and AI capabilities along with good appliances brand names which allow these organizations to grow rapidly in terms of robotic cleaning. Dyson keeps developing innovations related to intelligent suction and home cleaning, specifically for the premium residential market segments. SharkNinja has made efforts in growing the robotic vacuum business by using mid-premium pricing and omnichannel marketing. In the case of Xiaomi, the company utilizes the concept of ecosystem and Internet of Things (IoT) for entry into the emerging market segments.

Floor Cleaning Robots Market Dynamics

Rising Smart Home Adoption Accelerates Market Growth

The growth in the number of smart homes worldwide is increasing the demand for robot vacuum cleaners compatible with the IoT platform and its various components such as virtual assistants and smartphone apps. Consumers desire appliances that have the ability to schedule themselves, perform remote monitoring operations and conduct customized cleaning operations. GSMA reports that there were over 18 billion IoT connections globally in 2025, where home gadgets formed a significant portion of the connected consumer electronics.

In China, smart home appliance penetration is expanding rapidly because of the development of the country's digital infrastructure with the support of the government and the capacity of local firms to produce electronic devices. According to figures from the China Household Electrical Appliances Association, the shipment of AI-integrated smart home appliances was up over 20% in 2024, aided by rising income levels among urban consumers and enhanced 5G coverage.

Robotic cleaning machines have also been widely adopted in America owing to an increase in the number of families with dual income earners. In 2024, the number of such families was estimated at over 63% by the U.S. Census Bureau, thus giving rise to greater consumer interest in domestic appliances and devices that automate tasks within the household.

High Product Costs and Maintenance Complexity Restrain Adoption

AI-driven premium robotic floor-cleaning systems that are able to perform such tasks as autonomous navigation, automatic emptying and effective mopping usually cost more compared to traditional vacuum cleaners, restricting their affordability among mid-income consumers. Replacing batteries, calibrating sensors and performing software upgrades further elevate the overall cost of owning robotic cleaners for both individual and business clients.

Cleaning robots encounter certain challenges in functioning within intricate indoor conditions featuring irregular floors, stairs, extensive clutter or inadequate Wi-Fi connection. As per the United States Consumer Product Safety Commission, consumer grievances about robotic vacuum defects and battery overheating issues surged in 2024 due to the rising volume of robot usage worldwide. The potential risks of cyberattacks on smart home devices prevent some people from using internet-connected robotic systems capable of gathering indoor mapping data.

Commercial operators will encounter integration problems when installing automated cleaning solutions within expansive buildings needing integration with building management systems and worker coordination systems. Software upgrades, training of technical personnel and regular maintenance agreements will increase the cost of operation, especially for small enterprises lacking sufficient funds for automation.

Floor Cleaning Robots Market Segmentation Analysis

The global floor cleaning robots market is segmented based on the product, cleaning function, cleaning area, operation mode, deployment model, navigation, docking, floor type, sales channel, end-user.

Residential Segment Leads Market Deployment

The residential category is expected to lead in terms of deployments in 2025 because of increasing usage of smart homes, urbanization trends and consumers’ need for convenient appliances. Small robotic vacuum cleaners that can mop floors have been gaining traction among urban apartment dwellers and office workers who prefer automated devices for performing their chores. As per the estimates by the United Nations Department of Economic and Social Affairs, more than 57% of the world population was living in urban areas in 2025, which would drive the demand for compact and effective devices for household automation.

Robotics manufacturers are concentrating on urban customers with their multi-purpose products such as vacuuming, mopping, UV sterilization and self-cleaning functions. Several top robotics companies released their artificial intelligence-based floor cleaning robots in 2025, which can detect carpets, pet excrements, cords and furniture layout with their computer vision algorithms.

Aging demographics have also been contributing towards demand for residential robots. WHO suggests that the world population of individuals above the age of 60 years will go beyond 1.4 billion by 2030. As such, there has been growing interest in home automation devices that ease the physical burden on older adults. Countries like Japan, Germany and Italy have shown notable growth in adoption of robotic vacuum cleaners among other home care robots by their seniors.

Commercial and Industrial Applications Gain Momentum

Commercial establishments, including airports, hospitals, hotels, shopping centers and schools, have embraced robotic floor cleaning technologies to improve their efficiency. Hospitals have considerably increased their budget allocations towards robotic floor cleaners because of their greater concern about controlling infections due to the coronavirus pandemic.

According to the World Health Organization, there are millions of cases annually of health care associated infections globally, pushing hospitals to embrace autonomous cleaning robots that will enable them to control the infections. In 2025, several hospital networks in Europe and North America have embraced autonomous floor cleaners equipped with ultraviolet light technology to control infections.

Robotics cleaning solutions are being used in industrial warehouses as well as in logistics operations in conjunction with warehousing automation technology. E-commerce fulfillment centers are growing at an incredible rate, thereby making there a need for robotic floor cleaning solutions that can work round the clock in huge industrial settings. Mobile robotics installations in logistics settings grew tremendously in 2024 according to the International Federation of Robotics.

Floor Cleaning Robots Market Geographical Penetration

U.S. Floor Cleaning Robots Market Landscape

The United States is the most advanced country when it comes to technology and commercial readiness of floor cleaning robots. Automation is prevalent in retail stores, healthcare centers, logistics operations, hotels and educational institutions. Lack of sufficient manpower in janitorial and facilities management services is promoting he use of self-operated cleaning robots that can function round-the-clock without requiring human intervention. According to the Bureau of Labor Statistics of the U.S., there are over 2.1 million janitors and building cleaners in the nation. The escalating trend of wage increases and turnover rates is adding up to the cost of doing business for facilities management organizations. It has driven companies to install robotic floor scrubbing devices and intelligent vacuuming technologies in their warehouses, airports, grocery stores and hospitals.

Market players are prioritizing development efforts towards LiDAR guidance systems, computer vision-based obstacle recognition, self-docking systems and cloud-based fleet management solutions in order to boost efficiency. Universities and robotic start-ups are engaging in research collaborations geared toward developing autonomous navigation and man-machine interaction solutions that can be implemented in commercial cleaning environments. Current research efforts related to autonomous floor scrubbers in large commercial spaces have focused on increased spending on multi-modal perception systems incorporating 3D LiDAR, RGB-D cameras and AI-powered spatial mapping in order to navigate safely in cluttered environments. Furthermore, warehouse managers and facility operators throughout the U.S. have quickly adopted the use of industrial robotic floor scrubbers that can work autonomously for long periods of time in large commercial premises. Discussions held between warehouse managers have increasingly centered on the profitability associated with employing autonomous robotic scrubbers in facilities measuring more than 50,000 square feet, particularly in concrete-floored logistics centers that require constant dust control and floor scrubbing.

Japan Floor Cleaning Robots Market Outlook

Japan emerges as one of the most innovative markets for automated floor cleaning robots because of its serious shortage of labor force, aging population and heavy investments made by the nation in automating service robots. The use of autonomous cleaning robots by commercial firms, shopping centers, railway stations, hotels and manufacturing plants is becoming increasingly common because of their potential to cut the need for manpower while ensuring high levels of cleanliness. Japan’s well-developed robotics industry, fueled by efforts by governments and corporations to embrace automation technologies, has hastened the adoption of artificial intelligence-based floor cleaning robots by both public and private organizations.

Japanese companies that develop floor cleaning robots are moving towards incorporating intelligent facility automation, which includes cloud-based analytical software and robotics-as-a-service (RaaS). In 2026, for instance, SoftBank Robotics held the top market share position as the biggest domestic manufacturer in Japan's commercial cleaning robot market, based on the autonomous mobile robot industry analysis conducted by Fuji Keizai. Cleaning robot demand in Japan has surged, particularly in airports, railway infrastructures, retail chains, universities and medical institutions due to labor shortages. In addition, the robotics manufacturers are making investments in AI perception technologies, collision detection and avoidance and human-machine interaction innovations to improve robot performance in crowded interior spaces. There is an increasing interest among researchers and engineers in Japan in the application of autonomous cleaning, motion adjustment and situational awareness for the operation of service robots in proximity to pedestrians. In parallel, cleaning robots are incorporated into smart building management systems along with energy management and facility analytics. Japan is expected to continue its dominance in terms of advanced autonomous floor cleaning and service robotics technology worldwide.

China Floor Cleaning Robots Market Trends

China has emerged as the leading producer of innovations in robotics, especially floor cleaning robots in the Asia-Pacific due to the country’s strong electronics manufacturing, artificial intelligence and smart home penetration. In addition, China produces more floor cleaning robot vacuums than any other competitor while aggressively venturing into manufacturing autonomous robots used in cleaning malls, airports, high-rises, hospitals and factories. Manufacturers in China have been fast in making advancements such as LiDAR navigation, AI obstacle detection, robotic arms, self-cleaning docks and multiple-purpose sweeping and mopping systems. The availability of an efficient semiconductors supply chain, battery manufacturing capabilities and software engineering in AI have allowed local firms in China to launch floor cleaners that are highly competitive not only within domestic but even export markets.

Autonomous cleaning robots have become common in subway stations, airports, logistics hubs and factories where work optimization and automation are key considerations. Chinese robotics manufacturers are spending a lot of time working on embodied AI, autonomous navigation standards and human-machine cooperative technologies to develop their next-generation cleaning robots. The CleanUpBench project is developing AI-powered mobile cleaning machines that can sweep and grasp and interact with their environment adaptively. At the same time, robot development projects like SCCRUB have focused on soft robotic brushing technology to create high cleaning force in human-inhabited areas. High local demand for premium robotic vacuum cleaners, increasing adoption of smart home appliances and the international push by Chinese robotics companies are keeping China among the leading nations influencing the global floor cleaning robot market.

Competitive Landscape

- The global floor cleaning robots market features intense competition among consumer electronics manufacturers, robotics specialists and AI-driven smart appliance companies focused on technological innovation, autonomous navigation accuracy and ecosystem integration.

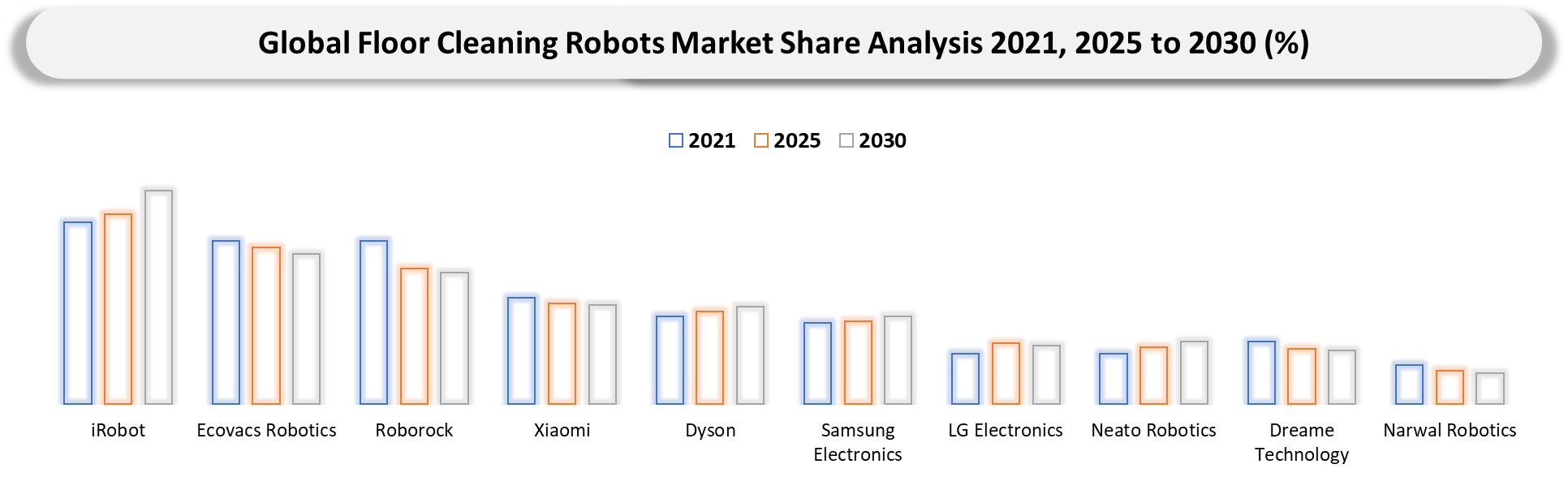

- Key players include iRobot, Ecovacs Robotics, Roborock, Xiaomi, Dyson, Samsung Electronics, LG Electronics, Dreame Technology, Narwal Robotics and Panasonic Holdings.

- Companies are increasingly competing through AI-enabled navigation systems, self-cleaning docking stations, obstacle recognition technologies, advanced suction efficiency and integrated smart home connectivity.

- Strategic investments in edge AI chips, computer vision, lithium battery optimization and autonomous mobility software are becoming essential as manufacturers attempt to differentiate products in a rapidly evolving intelligent appliance ecosystem.

Major Pain Points

- High upfront costs limiting adoption across price-sensitive residential and commercial consumers.

- Limited battery life disrupting cleaning cycles in large residential and commercial spaces.

- Navigation failures in cluttered environments reducing cleaning efficiency and customer satisfaction.

- Difficulty cleaning carpets, corners, thresholds and uneven floor surfaces effectively.

- Frequent maintenance requirements increasing ownership complexity and long-term operating costs.

- Privacy and cybersecurity concerns surrounding connected robots with cameras and mapping systems.

- Software dependency and firmware update failures impacting operational reliability and performance.

- Weak after-sales service and spare parts availability in emerging regional markets.

- Consumer skepticism regarding durability, cleaning precision and autonomous decision-making capabilities.

- Intense low-cost competition pressuring profit margins and accelerating product commoditization globally.

Key Developments

- May 2026 - Dreame Technology unveiled futuristic household robotics ecosystem, highlighting advanced robotic vacuum and AI-powered cleaning concepts at Dreame Next 2026.

- April 2026 - Ecovacs Robotics introduced DEEBOT X12 OmniCyclone featuring FocusJet stain-treatment, roller mopping and enhanced autonomous floor-cleaning performance.

- April 2026 - iRobot launched DEEBOT-style Roomba Mini and expanded AI-driven floor-cleaning ecosystem after Picea acquisition restructuring.

- September 2025 - Dyson showcased Spot+Scrub AI robot cleaner using stain-detection technology and autonomous deep-scrubbing capabilities for premium households.

- September 2025 - LG Electronics showcased hidden furniture-style robotic vacuum docking concepts and AI-enabled cleaning innovations during IFA 2025 exhibition.

- September 2025 - SharkNinja continued expanding AI-enabled robotic vacuum portfolio amid intensifying premium floor-cleaning competition across North American retail markets.

- September 2025 - Xiaomi expanded smart-home robotics portfolio through upgraded AI-powered robot vacuum integration showcased across Asian consumer-electronics exhibitions.

- March 2025 - Samsung Electronics expanded Bespoke AI appliance ecosystem, integrating smarter AI Home connectivity across robotic and cordless floor-cleaning products.

- January 2025 - Narwal Robotics introduced Flow Series robotic vacuums featuring rolling-pad mopping systems and enhanced autonomous floor-cleaning automation at CES.

- January 2025 - Neato Robotics had no major publicly disclosed floor-cleaning robot launch or strategic development announcements during 2025-2026 period.

- January 2025 - Roborock unveiled Saros Z70 robotic-arm vacuum at CES, enabling autonomous obstacle removal during cleaning operations.

Analyst View/Opinion

- AI-powered navigation and LiDAR mapping technologies are accelerating premium floor cleaning robot adoption across residential and commercial sectors globally.

- Rising labor shortages in hospitality, healthcare and facility management industries are increasing demand for autonomous cleaning robotics solutions.

- Multifunctional robots integrating vacuuming, mopping, self-emptying and self-cleaning capabilities are strengthening consumer replacement cycles and premiumization trends.

- China continues dominating manufacturing and innovation ecosystems through cost-efficient production, advanced sensor integration and aggressive export expansion strategies.

- Subscription-based maintenance, consumables and smart-home ecosystem integration are emerging as critical recurring revenue opportunities for market participants.

- Commercial floor cleaning robots are witnessing accelerated deployment across airports, warehouses, retail malls and healthcare facilities to reduce operational expenses.

- Advancements in computer vision, obstacle avoidance and edge AI processing are significantly improving cleaning efficiency and real-time navigation accuracy.

- Intense price competition among Asian manufacturers is pressuring margins while simultaneously expanding adoption across price-sensitive emerging economies.

- Sustainability-focused consumers are increasing demand for energy-efficient robots utilizing recyclable materials, water-optimized cleaning systems and low-noise operations.

- Strategic collaborations between robotics manufacturers and smart-home platform providers are strengthening interoperability and enhancing long-term customer retention.

Target Audience

| INDUSTRY | WHO SHOULD BUY THIS REPORT? | REASON TO BUY THIS REPORT |

| Residential Robotics Manufacturers | Product Development Teams, Smart Home Engineers, Innovation Managers | Analyze demand trends for autonomous floor cleaning robots across residential smart home applications |

| Commercial Cleaning Service Providers | Facility Operations Managers, Procurement Heads, Cleaning Technology Teams | Evaluate robotic cleaning adoption for offices, malls, airports and commercial infrastructure maintenance |

| Hospitality & Hotel Chains | Housekeeping Operations Teams, Facility Managers, Automation Consultants | Assess robotic floor cleaning solutions for labor optimization and improved guest experience standards |

| Healthcare Facilities & Hospitals | Hospital Administration Teams, Infection Control Specialists, Facility Engineers | Understand demand for robotic cleaning systems supporting hygiene compliance and contamination reduction |

| Retail & Shopping Mall Operators | Mall Operations Teams, Facility Maintenance Departments, Procurement Managers | Identify efficient robotic cleaning technologies for large retail spaces and high-footfall environments |

| Industrial & Warehouse Operators | Warehouse Automation Teams, Plant Facility Managers, Operations Engineers | Evaluate autonomous floor cleaning robots for industrial facilities, warehouses and logistics centers |

| Smart Home Technology Companies | IoT Product Teams, Connected Device Engineers, Strategic Partnership Departments | Analyze integration opportunities between floor cleaning robots and smart home ecosystems |

| Consumer Electronics Manufacturers | Product Strategy Teams, Robotics Engineers, Market Intelligence Departments | Benchmark robotic vacuum technologies, AI navigation systems and competitive product positioning |

| Educational Institutions & Universities | Campus Facility Teams, Maintenance Supervisors, Smart Infrastructure Departments | Assess robotic cleaning solutions for large educational campuses and operational cost optimization |

| Airports & Transportation Hubs | Infrastructure Operations Teams, Facility Automation Engineers, Procurement Departments | Evaluate robotic cleaning deployment for terminals, stations and high-traffic transportation facilities |

| Corporate Offices & Commercial Real Estate Companies | Building Operations Managers, Facility Management Teams, Sustainability Officers | Optimize cleaning efficiency and reduce labor dependency through robotic floor maintenance solutions |

| Robotics Software & AI Companies | AI Development Teams, Autonomous Navigation Engineers, R&D Departments | Study advancements in AI-powered mapping, obstacle detection and robotic cleaning intelligence |

| Battery & Component Suppliers | Energy Storage Teams, Component Engineering Departments, Supply Chain Managers | Analyze future demand for batteries, sensors, motors and robotic cleaning system components |

| E-commerce & Retail Distribution Platforms | Category Managers, Consumer Electronics Sales Teams, Market Analysts | Identify high-growth consumer segments and purchasing trends for robotic floor cleaning products |

| Facility Management Service Providers | Integrated Facility Teams, Smart Building Consultants, Operations Directors | Evaluate robotic cleaning adoption trends across commercial and institutional facility management contracts |

| Industrial Automation & Smart Building Companies | Automation Engineers, Industry 4.0 Consultants, Smart Infrastructure Teams | Assess integration opportunities between cleaning robots, IoT systems and building automation platforms |

| Research Institutes & Universities | Robotics Research Teams, AI Researchers, Engineering Faculties | Study innovations in autonomous navigation, robotic vision systems and cleaning automation technologies |

| Government & Public Infrastructure Organizations | Municipal Facility Departments, Smart City Authorities, Public Procurement Teams | Support smart infrastructure modernization and automation initiatives in public facilities management |

| Investors, Venture Capital & Consulting Firms | Investment Analysts, Market Intelligence Teams, Strategy Consultants | Evaluate market growth opportunities, competitive dynamics and technology adoption trends in cleaning robotics industry |

| Semiconductor & Sensor Manufacturers | Embedded Systems Teams, Sensor Development Engineers, Robotics Component Specialists | Understand sensor demand growth for LiDAR, cameras and intelligent robotic navigation systems |

Why Choose DataM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

What DataM Unquely Provides

- DataM delivers SKU-level benchmarking of robotic vacuum technologies across LiDAR, AI vision and autonomous mopping architecture competitive landscapes globally.

- DataM provides tariff-sensitive supply-chain intelligence tracking China-plus-one manufacturing transitions affecting robotic appliance sourcing economics and margin structures.

- DataM analyzes real-time semiconductor dependency exposure impacting robotic navigation systems, AI chip allocation and advanced sensor procurement strategies.

- DataM benchmarks country-wise smart-home adoption trends influencing premium robotic floor-cleaning penetration across residential and commercial customer segments.

- DataM delivers granular competitive intelligence on AI-enabled object recognition, autonomous navigation and predictive maintenance feature commercialization pipelines.

- DataM tracks cross-border regulatory developments involving cybersecurity, IoT compliance, repairability mandates and household data-governance implications for robotics manufacturers.

- DataM provides strategic market positioning analysis covering premiumization trends, direct-to-consumer pricing dynamics and innovation-led competitive disruption across global robotics ecosystems.

Qestions This Report Answers

- What is the current and forecast market size of the global floor cleaning robots market through 2035?

- Which end-users are driving demand growth and why?

- Which regions and product categories present the highest growth and investment opportunities in the global floor cleaning robots market?

- How are investments in AI-enabled navigation, self-cleaning docking systems and autonomous mobility reshaping competitive dynamics and consumer adoption?

- How do regulatory frameworks, data privacy standards and geopolitical supply chain risks affect floor cleaning robot manufacturing and deployment globally?

- Which technologies are shaping next-generation floor cleaning robots manufacturing?