Durable Carbon Dioxide Remove (CDR) Market Overview

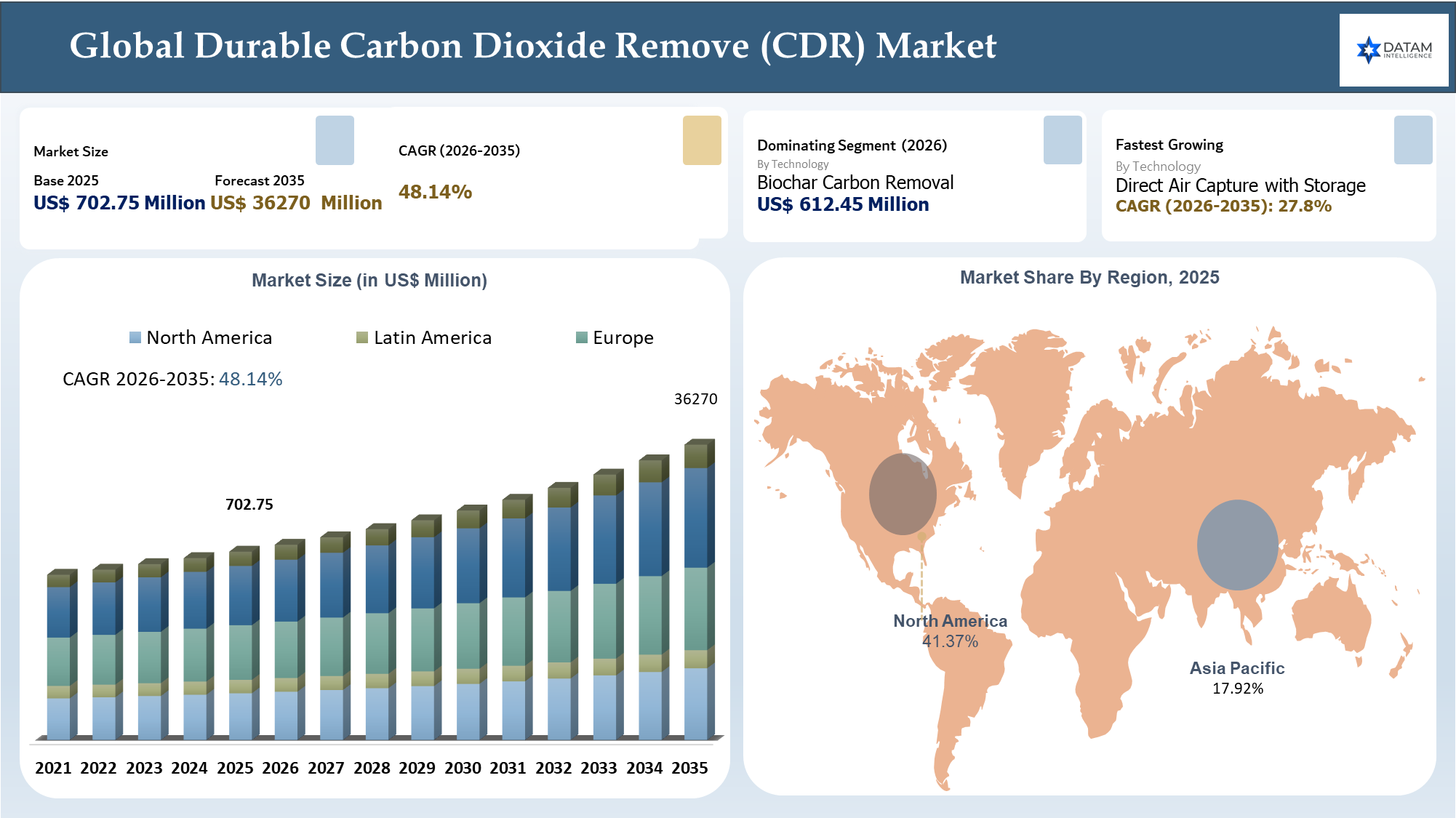

The Global Durable Carbon Dioxide Remove (CDR) Market reached US$ 702.75 million in 2025 and is expected to reach US$36270 million by 2035, growing with a CAGR 48.14% during the forecast period 2026-2035. The Durable Carbon Dioxide Removal Market (CDR) is transitioning from its nascent form as an exotic market for carbon credits to a more established climate infrastructure market. This growth is fuelled by difficult-to-abate industries, tech firms, the airline industry, energy providers, and manufacturers who need sustainable ways of removing remaining carbon dioxide that cannot be reduced through processes in their operations alone.

While traditional offset projects are based on activities aimed at preventing future emissions, durable CDR emphasizes the tangible removal of carbon dioxide from the atmosphere using approaches like direct air capture, biochar, enhanced rock weathering, carbon mineralization, BECCS, and ocean-based removal. Market trends indicate a move towards higher-integrity credits underpinned by sound metrics, additionality, verifiable permanence, and lifecycle accounting. With improved policy interventions, advance purchase agreements, and carbon removal coalitions, project developers can increase viability and accelerate commercialization efforts. Nonetheless, high costs, low supply of carbon credits, infrastructure deficits, and verification issues will continue to affect market growth.

AI Impact Analysis

AI is playing an increasingly significant role as a market enabler in the Durable Carbon Dioxide Removal business through better project assessment, higher accuracy in measurements, cost reduction opportunities, and increased confidence among buyers. CDR providers are leveraging machine learning capabilities to find optimal locations for DAC, enhanced rock weathering, biochar, mineralization, and geological storage based on available feedstocks, renewable energy sources, suitable land, climate patterns, transportation routes, and storage durability. At the same time, AI is contributing to higher levels of MRV capability through data collection from sensors, satellites, geochemical analyses, and lifecycle measurements for higher accuracy and faster validation process completion. Regarding economics, the application of artificial intelligence could help CDR providers achieve better energy efficiency, plant operation management, sorbent efficacy, biomass transportations, and carbon credit pricing strategy for minimizing costs per ton of CO2 removed. AI will be useful on the consumer side as well due to procurement systems that can evaluate CDR credits in terms of durability, risk, delivery schedule, geographic location, and level of verification.

Durable Carbon Dioxide Remove (CDR) Market Industry Trends and Strategic Insights

- Persisting CDR is critical for reaching net-zero objectives when emission reductions alone cannot achieve this goal, particularly in sectors that are harder to decarbonize.

- Market demand is moving towards permanent, high-integrity carbon removals with robust measurement, reporting, and verification, durable storage, and stringent climate disclosure standards.

- High prices, lack of infrastructure, and low-scale operations present significant challenges to market expansion.

- Government policy support, pre-purchase agreements, and climate commitments from companies are fast-tracking commercialization and future market development.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 702.75 Million | |

| 2035 Projected Market Size | US$ 36270 Million | |

| CAGR (2026-2035) | 48.14% | |

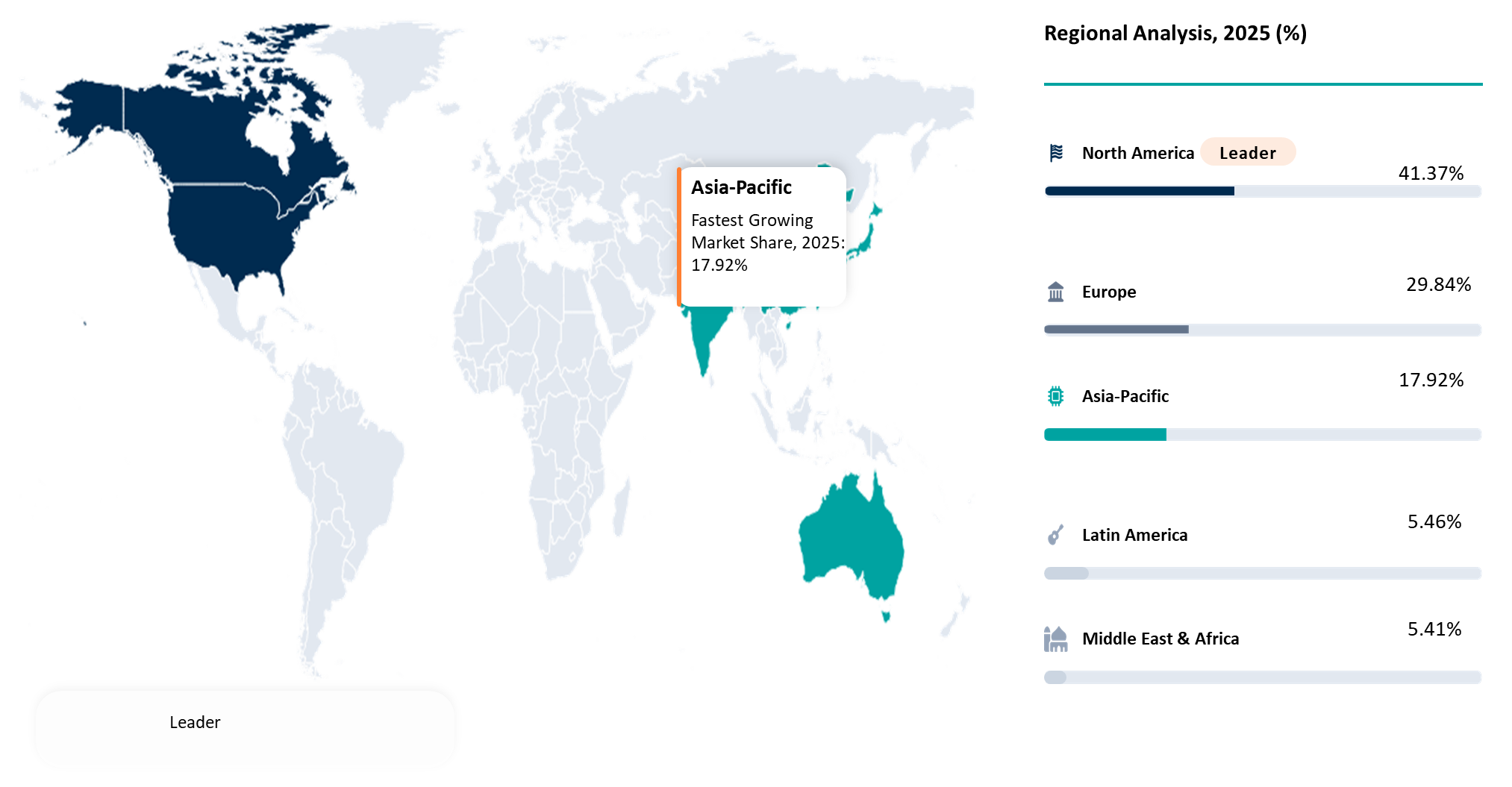

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Technology | Direct Air Capture with Storage, Bioenergy with Carbon Capture and Storage, Biomass Carbon Removal and Storage, Biochar Carbon Removal, Enhanced Rock Weathering, Carbon Mineralization, Ocean Based Carbon Removal, Electrochemical Carbon Removal, Hybrid Removal, and Others | |

| By Storage Pathway | Geological Storage, Mineralization Storage, Soil Carbon Storage, Ocean Storage, Durable Product Storage, and Others | |

| By Durability Period | 100–500 Years, 500–1,000 Years, 1,000–5,000 Years, and Above 5,000 Years | |

| By Feedstock Source | Atmospheric CO₂, Biomass Residues, Agricultural Waste, Forestry Residues, Marine Biomass, Industrial Biogenic CO₂, and Others | |

| By Project Scale | Pilot Scale, Demonstration Scale, Commercial Scale, and Large Scale Deployment | |

| By Business Model | Carbon Credit Sales, Long Term Offtake Agreements, Carbon Removal as a Service, Integrated Capture and Storage Projects, Marketplace and Aggregator Model, and Others | |

| By End User | Technology Companies, Aviation and Aerospace, Energy and Utilities, Industrial Manufacturing, Oil and Gas, Construction and Materials, Consumer Goods Companies, BFSI, Consulting, Government and Public Sector, and Others | |

| By Buyer Type | Voluntary Carbon Market Buyers, Compliance Market Buyers, Corporate Net Zero Buyers, Advance Market Commitment Buyers, and Public Procurement Buyers | |

| By Monitoring Reporting and Verification | Engineering Based Verification, Measurement Based Verification, Life Cycle Assessment Validation, Remote Sensing Verification, Digital Registry and Tracking Systems, and Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

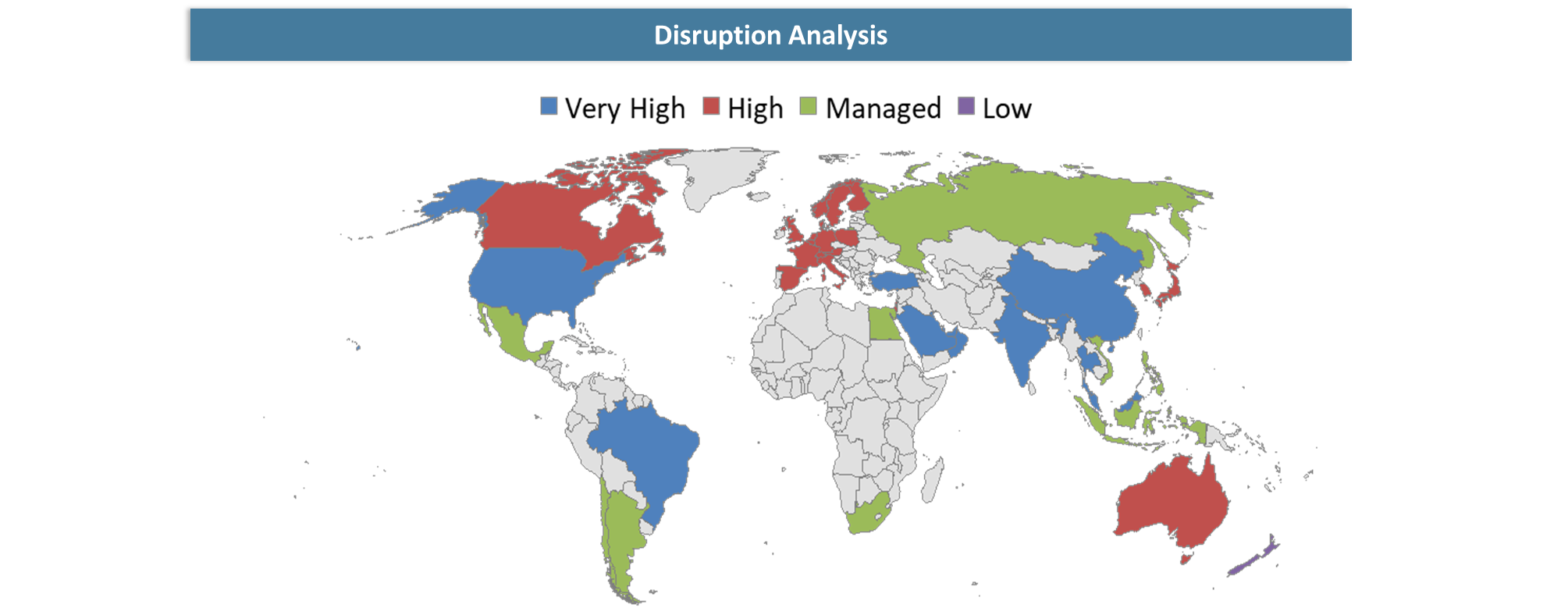

Disruption Analysis

Transition from Traditional Offsets to Permanent Carbon Removal is Reshaping the Carbon Market Landscape

Disruption is occurring within the carbon offsetting ecosystem, driven by the Durable Carbon Dioxide Removal market's move towards buyers' increasing interest in durable, measurable, and verifiable carbon removals over cheap avoidance credits. Companies that have been constructing their net-zero portfolio are now being influenced to consider factors such as durability, additionality, quality of MRV, storage liability, and delivery certainty in their procurement strategy. The use of innovative technologies such as direct air capture, biochar, enhanced rock weathering, mineralization, and oceanic CDR solutions is leading to the emergence of an entirely new asset class, where carbon removal will be considered as climate infrastructure, rather than an expenditure in voluntary ESG metrics. Of course, the involvement of offtake contracts, AMC, and certification regimes supported by policies is promoting commercialization and improving the bankability of projects. On the other hand, advancements in AI-assisted MRV, digitized registries, and lifecycle management of CDR projects are promoting transparency and highlighting shortcomings in the offsets market model.

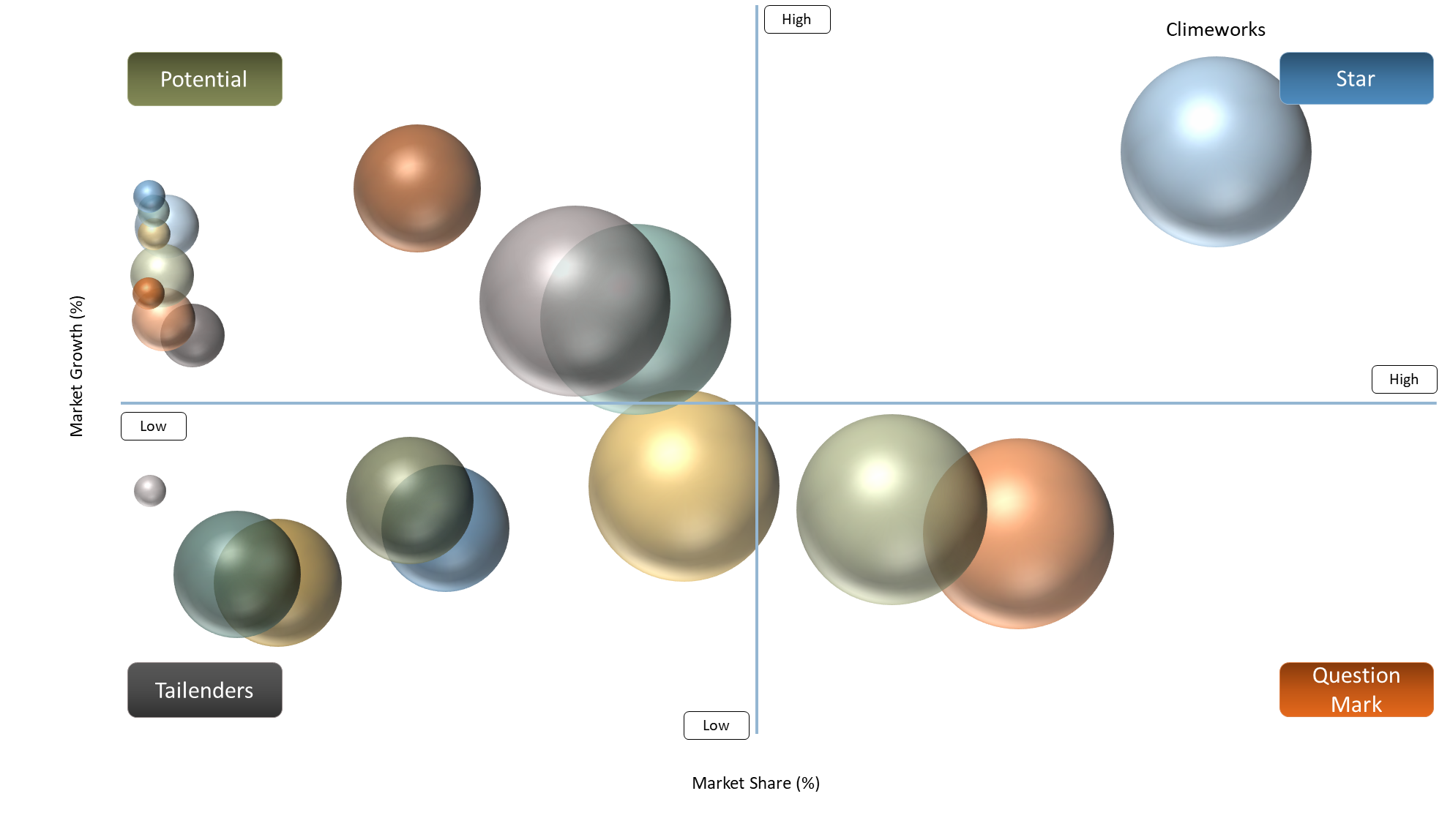

BCG Matrix: Company Evaluation

Positioning in the Durable Carbon Dioxide Removal market may depend on such factors as technological readiness, scale of commercialization, funding, customer acceptance, and carbon removal capabilities for long periods. Climeworks, 1PointFive, Carbon Engineering ULC, Heirloom Carbon Technologies, Inc., and Charm Industrial, Inc. represent stars due to good financing, large-scale projects implementation, offtake agreements between corporations, and robust commercialization pipelines. Such companies influence the future development of the Carbon Removal Technology Market Growth via the creation of high-volume infrastructures and carbon storage capabilities.

Companies like CarbonCure Technologies Inc., Carbfix hf., Planetary Technologies Inc., Deep Sky, Lithos Carbon, and Carbonbuilt, inc could be considered as Pervasive Players as they have good technology differentials and growing partnerships but still work on increasing their penetration into the market.

The list of Emerging Players includes Eion Corp., Undo Carbon Ltd, Captura Corp., CarbonRun, Skytree, Novocarbo GmbH, Exomad Green, Varaha ClimateAg Private Limited, and 8 Rivers Capital, LLC, which implies that they possess significant potential in terms of innovation but lack market penetration at the moment.

Market Dynamics

Policy and compliance market interest is strengthening commercial visibility

Compliance and policy market interest is emerging as a crucial enabler for the durable Carbon Dioxide Removal market, as policymakers become aware of the need for more than emission reductions to deliver on the net-zero pathway. The EU passed its first certification scheme for permanently removed carbon emissions in November 2024, providing a roadmap for verifying CDR projects. This is significant because the global carbon removal credit market was valued at US$2.7 billion in 2023 and could potentially grow to US$100 billion yearly by 2030-2035, given improvements in standards, policy backing, and compliance considerations. Moreover, durable CDR is gaining significance in policy discussions surrounding residual emissions in the aviation sector, cement industry, steel production, chemical manufacturing, and power generation. As verifiable CDR enters procurement schemes, tax policies, and compliance regulations, CDR developers benefit from clear revenue streams and improved project viability.

High Cost of Durable Removals Limits Broad Buyer Adoption

Pricing continues to be among the most formidable barriers within the durable Carbon Dioxide Removal industry because many of the technologies employed for permanent removal are significantly more expensive than traditional carbon credits. Technologies such as direct air capture, mineralization, marine removal, and engineered biomass storage all need substantial capital expenditure, clean energy access, advanced technology, transportation, storage infrastructure, and accurate monitoring, reporting, and verification processes. Consequently, durable CDR credits may cost hundreds of dollars per ton, compared to many traditional voluntary carbon credits that can be purchased for relatively low prices. The price difference makes it possible to apply durable CDR only to significant corporate technology, airline, banking, and manufacturing sectors willing to invest in the highest climate budget. Mid-sized organizations are unlikely to consider the adoption of durable CDR unless there is enough budget allocated for sustainability in the short term.

Segmentation Analysis

The Global Durable Carbon Dioxide Remove (CDR) Market is segmented based on the technology, storage pathway, durability period, feedstock source, project scale, business model, end user, buyer type, monitoring reporting and verification, and region/countries.

Direct Air Capture with Storage is Emerging as the Premium Climate Infrastructure Pathway for Durable CDR

The Direct Air Capture with Storage sub-segment is being seen as the most strategic sub-segment in the Durable Carbon Dioxide Removal (CDR) market as it allows for measurable atmospheric CO₂ removals using either long-duration geological or mineral storage. As against the conventional offsets, DACS provides a higher level of additionality, better carbon accounting, and permanent storage, which makes it very appealing for technology players and industries such as aviation, energy, cement, steel, and others that find it challenging to reach net zero status.

The sub-segment is transitioning from demonstration phase to early commercialization. Climeworks has launched the Mammoth plant, which has the capacity to capture 36,000 tons of CO₂ per year in Iceland in May 2024. Also, 1PointFive has announced the sales of its DAC carbon removal credit amounting to 500,000 metric tons of CO₂ from STRATOS project to Microsoft. The U.S. will be developing four direct air capture hubs under its Regional Direct Air Capture Hubs Program that would allow each of the hubs to capture at least 1 million metric tons of CO₂ annually.

From a consulting point of view, DAC with storage is considered a high-end climate infrastructure sector instead of an inexpensive credit option. Growth will be enabled by the push factors such as policies, long-term off-takes, company purchases, and the development of storage centers. Nonetheless, capital intensiveness, clean power needs, and the presence of storage facilities present major challenges. Winners in the future will be organizations that manage to reduce cost per ton, get their hands on renewable power, provide credible MRV, and expand beyond small-scale plants.

Geographical Penetration

North America Dominates Durable CDR Market Growth Through Policy Support, Climate Investment, and Carbon Infrastructure Expansion

North America ranks highest on Durable CDR Market Size across the globe due to the influence of favorable policies, sophisticated climate infrastructure, and early corporate procurements of durable carbon removal. In the region, the United States serves as the primary driver of the market growth thanks to the provision of US$180 per ton of carbon removed under 45Q tax credit scheme.

Such favorable climate policies contribute significantly to Carbon Removal Technology Market Growth as developers receive additional benefits in the form of abundant geological carbon storage resources, mature energy infrastructure, and large investments into DAC hubs development. When examining the Negative Emissions Market Analysis, it becomes evident that technology, aviation, and industrial corporations serve as an important source of early adoption through long-term offtakes and advance purchase agreements.

Carbon Capture Solutions Market Trends observed in North America indicate the transition from small-scale pilots to climate infrastructure developments with multiple large-scale DAC hubs planned in Texas and Louisiana. They are forecasted to remove 2+ million metric tons of CO₂ annually. In terms of Climate Tech Market Forecast, North America should stay a leader in the field due to the presence of favorable policies, project financing options, carbon storage opportunities, and corporate net-zero demand.

U.S. Durable Carbon Dioxide Remove (CDR) Market Trends

The United States holds a pivotal position within the Durable CDR Market Size, backed by an extensive network of climate technology developers, carbon buyers, infrastructure providers, and regulatory facilitators. America has emerged as a leading hub for Carbon Removal Technology Market Growth, fueled by massive investments in direct air capture, biomass carbon sequestration, enhanced rock weathering, and carbon mineralization solutions.

Regarding the U.S. Negative Emissions Market Analysis, corporate buying stands out as a critical market driver, with several prominent technology firms, airlines, and manufacturing industries entering into multiyear carbon removal purchase contracts to ensure decarbonization objectives are achieved. In addition, America has access to abundant geological carbon storage sites, well-developed pipeline networks, and a robust energy industry equipped to integrate carbon removal systems on an industrial level.

Carbon Capture Solutions Market Trends reveal a rise in regional carbon management clusters, increasing investment in monitoring, reporting, and verification technologies, and enhanced cooperation between carbon removal vendors and industrial carbon emitters. As far as Climate Tech Market Forecast goes, the United States will continue its dominant position owing to robust private equity flows, climate-friendly policies, and a thriving commercial carbon landscape.

Canada Durable Carbon Dioxide Remove (CDR) Market Outlook

Canada is becoming an increasingly significant player in the Durable CDR Market Size, due to the presence of promising geological storage sites, abundant sources of clean energy, and increasing capital flows towards carbon management infrastructure. Canada’s Carbon Removal Technology Market Growth will be driven by investments in direct air capture, biomass carbon removal, biochar, mineralization, and carbon capture solutions related to industrial decarbonization.

In the Negative Emissions Market Analysis of Canada, the best chance for success exists through utilizing forestry waste, agriculture biomass, clean energy, and sedimentary basin storage to build scalable durable removal projects. Major Carbon Capture Solutions Market Trends involve carbon hubs in Alberta, financial incentives encouraged by policy, and increased cooperation between energy companies, climate tech businesses, and industrial emissions companies.

From a Climate Tech Market Forecast viewpoint, Canada will be poised to capitalize as buyers become increasingly interested in high-quality North America-based durable CDR credits.

Competitive Landscape

- The Durable Carbon Dioxide Removal industry is very innovation-focused, where competitive advantage lies in permanence, scalability, robustness of MRV system, economic feasibility, and trustworthiness of the buyers. Climeworks, 1PointFive, Carbon Engineering ULC, Heirloom Carbon Technologies, Inc., and Charm Industrial, Inc. are regarded as the major competitors because of their strong technology foundations, commercialization efforts, and long-term collaborations in carbon removal projects.

- CarbonCure Technologies Inc., Carbfix hf., Carbonbuilt, inc, and Planetary Technologies Inc. offer a mineralization solution along with concrete-based carbon storage and durable storage routes for enabling an industrialized process.

- Exomad Green, Novocarbo GmbH, Varaha ClimateAg Private Limited, Lithos Carbon, Eion Corp., Undo Carbon Ltd, Captura Corp., CarbonRun, Skytree, 8 Rivers Capital, LLC, and Deep Sky represent emerging competitors via biochar, enhanced weathering, oceanic removal, DAC technology components, and carbon removal hubs.

- Cost efficiency, verifiable permanence, scalable infrastructure, credit provision reliability, and robust corporate customer relationships will determine future competitive advantage.

Key Developments

- January 2026 - Varaha ClimateAg Private Limited signed a carbon removal agreement with Microsoft for 100,000 tonnes of biochar carbon removal credits over three years, strengthening India’s position as an emerging durable CDR supply hub.

- January 2026 - 1PointFive and Bain and Company announced an agreement for Direct Air Capture carbon removal credits, expanding enterprise adoption of durable CDR among consulting and corporate sustainability buyers.

- September 2025 - 1PointFive and NYK announced a carbon removal agreement, supporting the use of Direct Air Capture credits for hard-to-abate maritime sector decarbonization.

- August 2025 - Planetary Technologies Inc. signed a US$31.3 million offtake agreement with Frontier buyers to remove more than 115,000 tons of CO₂ between 2026 and 2030 through ocean alkalinity enhancement.

- August 2025 - Deep Sky Alpha began operations in Alberta, marking the start of carbon removal operations and North America’s first CO₂ storage from Direct Air Capture.

- January 2025 - Google signed long-term purchase agreements with Varaha ClimateAg Private Limited and Charm Industrial, Inc. to buy 100,000 tons of biochar carbon removal from each company by 2030, strengthening commercial demand for durable biochar-based CDR.

- December 2024 - Breakthrough Energy Catalyst committed US$40 million to Deep Sky to support the Deep Sky Alpha Direct Air Capture test facility in Alberta, helping accelerate DAC technology testing and scale-up.

- December 2024 - Heirloom Carbon Technologies, Inc. closed a US$150 million Series B financing round to support Direct Air Capture scale-up, project development, and commercialization.

- October 2024 - CarbonCure Technologies Inc. announced that its carbon mineralization technology had achieved 500,000 metric tons of cumulative carbon savings, reinforcing concrete mineralization as a scalable durable carbon storage pathway.

- July 2024 - 1PointFive announced an agreement to sell 500,000 metric tons of Direct Air Capture carbon removal credits to Microsoft over six years from its STRATOS facility in Texas.

- June 2024 - Heirloom Carbon Technologies, Inc. announced plans to build two Direct Air Capture facilities in Northwest Louisiana, with the first phase expected to remove 100,000 tonnes of CO₂ per year once operational.

- May 2024 - Climeworks launched Mammoth in Iceland, its largest Direct Air Capture and Storage facility, designed to capture up to 36,000 tons of CO₂ annually for permanent storage.

White Space Opportunities

White spaces present themselves in Durable Carbon Dioxide Removal (CDR) Market beyond just carbon credits to DataM. As most businesses have become occupied with direct air capture and premium offtakes, other segments such as enhanced rock weathering, biochar produced from agri-residue, biomass carbon storage, carbon mineralization in construction materials, ocean-based CDR, and even regional CDR Hubs still present a huge scope of growth.

One major area of white space would include a business that would be able to provide a full-fledged solution that covers project development, raw material acquisition, access to storage facility, MRV, registration and issuing credits, as well as obtaining buyers' contracts. Organizations that can drive down their cost per ton and demonstrate their durability and infrastructure along with verifying their process will fare well in the market. The best possible way is by creating durable CDR as infrastructure solutions.

DMI Opinion

As per DataM, the growth of the Durable Carbon Dioxide Removal (CDR) Market will depend not only on the availability of carbon removal solutions but also on the effectiveness of the solutions to produce verifiable, durable, and scalable carbon removals. There is a shift from conventional inexpensive offsetting to high-quality removal credits that come with reliable measurement, verification, and reporting, durability of storage, additionality, and comprehensive lifecycle accounting.

In accordance with the research from DataM, the highest potential for commercialization will be found in DACS, biochar carbon removal, enhanced rock weathering, mineralization of carbon dioxide, BECCS, and biomass carbon removal and storage. Businesses which prove their capability to achieve cost-effectiveness per ton, verifiable performance, offtake agreements for decades, and delivery capability will be in a competitive position. Thus, the proper approach to this market should consider it as an infrastructure market for carbon removal, not merely a voluntary carbon credits one.

Why Choose DataM?

- Innovative Durable CDR Technology: Includes direct air capture, biochar, enhanced rock weathering, carbon mineralization, BECCS, biomass carbon sequestration, ocean carbon removal, and electrochemical CDR.

- Positioning of Competing Firms: Analyzes major firms according to their technology approach, pipeline, ability to deliver credits, durability claims, MRV effectiveness, partnerships, and degree of commercialization.

- Market Trends and Dynamics: Discusses durable carbon removals, procurement for corporate net-zero, advanced purchasing arrangements, regulatory backing, compliance market involvement, and transition from offsets to high-integrity removals.

- Business Strategies by Competitors: Analyzes offtake contracts, project financing, storage deals, registry approval, scaling technology, geographic expansion, and partnerships with corporate purchasers.

- Carbon Removal Credits Pricing: Examines pricing and cost-per-ton, durability premium, willingness to pay by buyer, delivery risk, and barriers to adoption in key markets.

Target Audience 2026

- Carbon removal technology developers

- Direct Air Capture and carbon mineralization companies

- Biochar and biomass carbon storage providers

- Carbon credit marketplaces and registries

- Corporate net-zero and sustainability teams

- Energy, utilities, and industrial decarbonization companies

- Aviation, shipping, and hard-to-abate industry operators

- Climate technology investors and venture capital firms

- Government climate agencies and regulatory bodies

- Environmental consulting and carbon advisory firms

- Carbon accounting and MRV platform providers

- Infrastructure developers and geological storage operators