Carbon Capture and Sequestration (CCS) Market Overview

The global Carbon Capture and Sequestration (CCS) Market reached US$ 3.88 billion in 2025 and is expected to reach US$ 26.32 billion by 2035, growing with a CAGR of 21.1% during the forecast period 2026-2035. The concept of CCS is steadily growing in popularity due to the increasing pressure on industries to reduce their emissions in sectors where abatement proves to be difficult, such as cement manufacturing, steel production, refining and the chemical industry. Market is experiencing upward movement owing to several factors, including tougher climate targets, increased use of carbon price mechanisms and large funding projects. According to International Energy Agency, reaching net-zero emissions calls for more than 1 billion tons of captured CO₂ each year up until 2030, which represents a major increase from the current rates. Industries are starting to form alliances across sectors to build common transport and storage infrastructure for CO₂, while oil and gas firms are converting emptied reservoirs into CO₂ sinks.

Further efforts towards the expansion of CCS are being made through government policies and international cooperation by making it an integral part of the national climate roadmaps and transition agendas. CCS has been included in the climate plans of over 40 nations and there are currently more than 40 operational CCS facilities worldwide, along with another 200 that have reached different phases of implementation. Developing countries from Asia-Pacific and the Middle East are developing massive carbon management centers to ensure continued growth in industrial activities with a lower carbon footprint.

Carbon Capture and Sequestration (CCS) Industry Trends and Strategic Insights

- Nearly 90% of all greenhouse gases are emitted due to burning of fossil fuels and industrial processes; hence, the International Governmental Panel on Climate Change claims that it would be more expensive to ensure the temperature rise is kept under 1.5° C without employing CCS technology.

- Globally, the amount of investments made in the CCS sector has exceeded US$80 billion as of 2024, with many CCS centers emerging in North America and Europe due to the availability of government subsidies such as the 45Q tax credits in USA

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 3.88 Billion | |

| 2035 Projected Market Size | US$ 26.32 Billion | |

| CAGR (2026-2035) | 21.1% | |

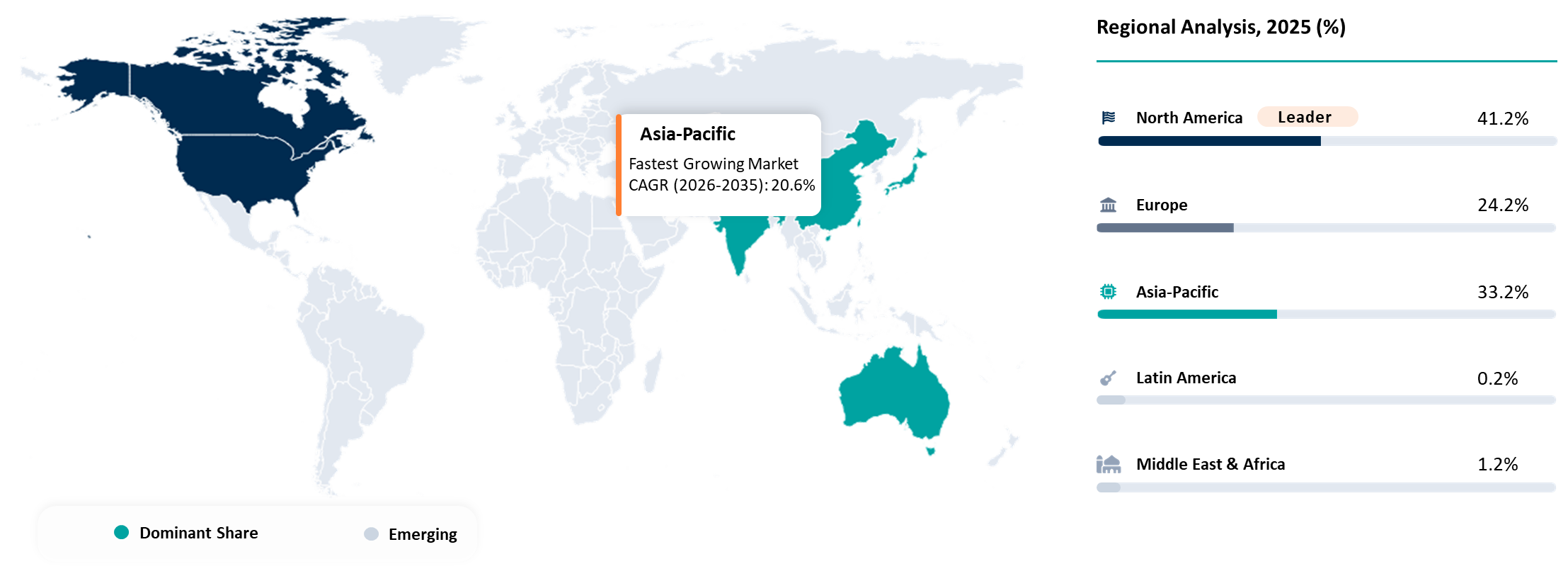

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Service | Capture, Compression and Dehydration, Transportation, Storage | |

| By Capture Technology | Post Combustion Capture, Pre-Combustion Capture, Oxy Fuel Combustion, Industrial Process Capture, DAC Linked to Storage | |

| By Source | Point Source Capture, DAC to Storage | |

| By Transportation Mode | Pipeline, Ship, Rail, Truck | |

| By Storage Type | Saline Aquifers, Depleted Oil Fields, Depleted Gas Fields, EOR Linked Storage, Basalt and Reactive Rock Formations, Unmineable Coal Seams, Other Geological Storage | |

| By Facility Scale | Pilot and Demonstration, Commercial Small Scale, Commercial Large Scale | |

| By Application | Oil and Gas, Power Generation, Natural Gas Processing, Hydrogen, Ammonia and Fertilizers, Cement, Iron and Steel, Chemical and, Petrochemical, Refineries, Pulp and Paper, Waste to Energy, Others | |

| By Project Stage | Announced, Engineering and Design, Under Construction, Operational | |

| By End-User | Emitters, Midstream Transport Operators, Storage Developers, Integrated Carbon Management Developers | |

| By Region | North America | USA, Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Disruption Analysis

Mandates from government, along with incentives in the form of extended tax credits and emissions reduction laws, are changing how investments are being made. Technological advancements in advanced capture processes, like solid sorbents and direct air capture, are lowering the energy requirements and cost associated with carbon capture operations, putting them ahead of existing amine technology. Innovations coming from companies like Svante and Carbon Clean include modular plants that lower costs and disrupt current thinking about CCS. Another development is that applications for utilizing carbon are creating new opportunities through CCUS ecosystems. Advancements in digitalization and artificial intelligence for monitoring and verification are increasing assurance that storage will be successful. Nevertheless, the availability of infrastructure, especially CO₂ transportation and storage networks, remains an essential bottleneck in the system.

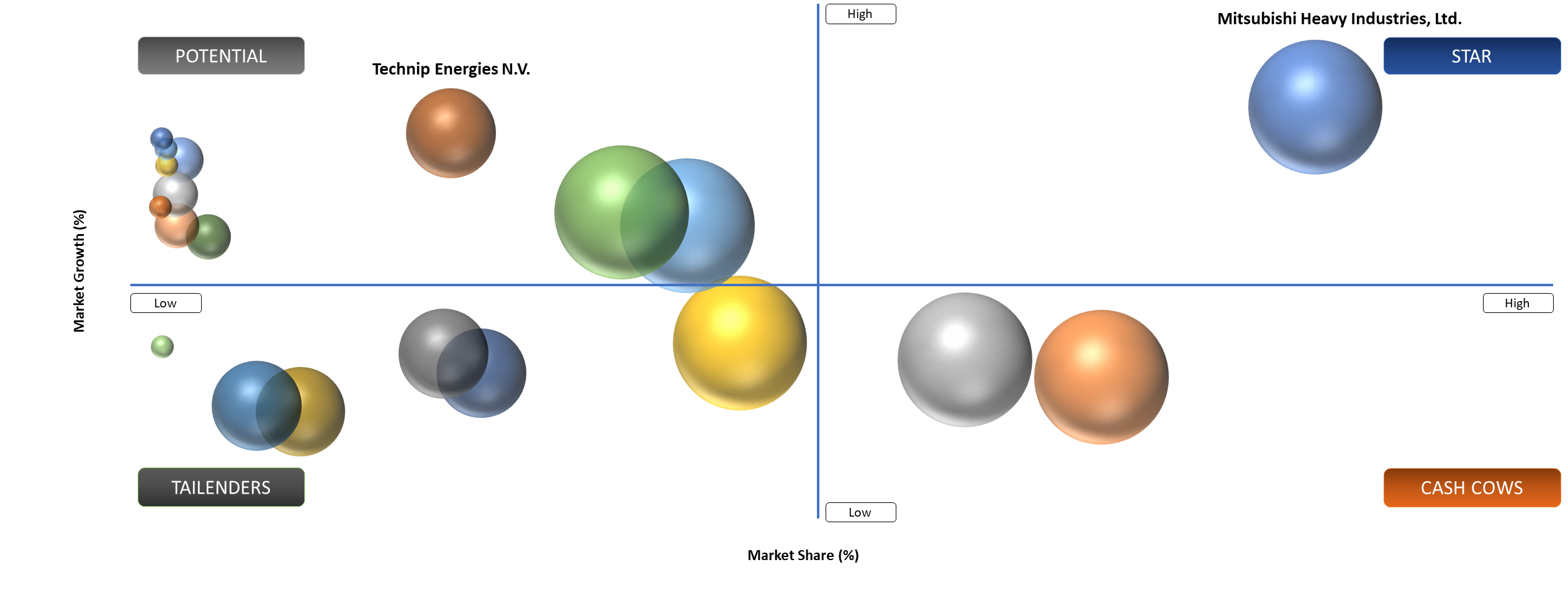

BCG Matrix: Company Evaluation

The stars are actively making significant investments in large-scale CCS centers, which receive governmental inducements such as tax incentives and carbon taxes. The companies have a high market position and tremendous potential, especially in North America and Europe. The potential includes young DAC and modular capture companies such as Carbon Engineering and Climeworks, whose scalability and costs are still not determined because they receive much financing. The cash cows are mature industrial gases companies such as Air Liquide and Linde plc, which use their constant income from capture technologies in hydrogen and ammonia production.

Market Dynamics

Rising Deployment Across Industrial Decarbonization

CCS has been gaining momentum owing to its wide applicability in the heavy industries sector, including cement, steel and chemical manufacturing, that cannot switch completely to renewable energy in their operations and hence require CCS solutions. Heavy industries contribute more than 30% to total global CO₂ emissions and are thus the main beneficiaries of CCS. As of 2024, more than 40% of all future CCS projects will be aimed at serving industrial processes and not power production. Also, there has been an increased use of hydrogen production from natural gas along with CCS (blue hydrogen). It is most prevalent in Europe and the Middle East, where governments are actively involved in the creation of hydrogen clusters. An example includes the Norwegian Longship CCS project supported by the Norwegian government that aims at capturing about 0.8 Mt of CO₂ annually from cement production.

High Capital Costs and Infrastructure Constraints

Even with such a promising outlook, the implementation of CCS encounters various obstacles linked to its high capital cost, intricate licensing procedure and demand for large-scale CO₂ transport and storage networks. The cost of capture might vary anywhere from US$50 to US$150 per tonne, making the technology economically unfeasible without any form of policy intervention. Most developing countries fail to have the regulatory system and geological evaluation of storage sites needed for the adoption of CCS technologies. The issue of long-term security and accountability of CO₂ storage also remains unresolved in many places.

Segmentation Analysis

The global Carbon Capture and Sequestration (CCS) market is segmented based on the service, capture technology, source, transportation mode, storage type, facility scale, application, project stage, end-user and region.

Power Generation and Hydrogen Applications Lead Adoption

Installing CCS technology into existing coal and gas power plants is under consideration to prolong the life of these assets while reducing carbon footprints. On the other hand, the use of CCS alongside the production of hydrogen is becoming another growth opportunity. According to the International Renewable Energy Agency, annual demand for hydrogen may exceed 500 million tonnes by 2050, with a considerable part derived through low-emission processes, such as CCS-based hydrogen production. There have been developments on USA Gulf Coast, along with Humber in UK, of CCS combined with hydrogen hubs to benefit from cost-saving opportunities.

Carbon Utilization and Storage Hubs Gain Traction

The establishment of CCS hubs and clusters on a large scale is revolutionizing the market because these hubs allow several emission sources to benefit from common transport and storage infrastructure. Hubs decrease expenses and simplify the process of implementation. In 2023, the Northern Lights CCS hub in Norway, one component of the Longship project, started the development of open access CO₂ transport and storage infrastructure with a capacity of 1.5 million tons per annum (Mtpa), expandable up to 5 Mtpa. Additionally, there have been plans for the implementation of regional DAC and CCS hubs within USA that will be financed by the government. Hubs play an essential role in efficient deployment of CCS technology, particularly in areas characterized by a high concentration of industrial activities.

Geographical Penetration

North America Leads in Enterprise Adoption and Platform Investment

North America has become the dominant force in the CCS industry because of favorable policies, the presence of existing oil and gas infrastructure and the implementation of early CCS projects. In fact, USA boasts the highest number of active CCS projects globally, thanks to higher tax breaks provided by the 45Q program, which gives up to US$85 per tonne of CO₂ captured and stored. As stated by the EPA, more U.S. CCS projects are now geared towards industrial capture and saline storage as opposed to enhanced oil recovery. Canada is making substantial investments as well, including Alberta’s carbon trunk line, which can transport 14.6 million tonnes of CO₂ each year.

USA Carbon Capture and Sequestration (CCS) Market Trends

Over US$ 12 billion of government funds (2021-2025) have been dedicated to CCS projects through bipartisan infrastructure laws that will finance CCUS hubs, DAC plants and storage pilots by USA Department of Energy. The new enhanced 45Q tax credit allows developers to earn up to US$85 per ton of captured CO₂ and US$ 180 per ton of direct air capture, greatly boosting the financial incentives for such ventures. According to the International Energy Agency, over 50% of current world CCS capacity belongs to USA in the form of projects implemented in the fields of hydrogen production, ethanol manufacturing and natural gas processing. Furthermore, there are more than 5,000 miles of pipelines dedicated to transporting CO₂, offering a strong basis for further development in sequestration technology. The Gulf Coast industrial complexes are transforming into carbon management centers thanks to collaboration between oil companies and cleantech.

Canada Carbon Capture and Sequestration (CCS) Market Trends

The investment tax credit system has been introduced in Canada, whereby 50% of the expenses required to establish the CCS project will be covered, resulting in a marked rise in its adoption. According to the website of Natural Resources Canada, CCS is essential in ensuring that Canada achieves its goal of zero emissions, especially with the help of Alberta in the form of transportation and storage of the captured carbon. Several projects related to CCS are taking place in Canada, mainly focusing on the production of blue hydrogen and fertilizers.

Competitive Landscape

- The global CCS market features a mix of energy majors, engineering firms and emerging technology providers competing across capture technologies, transport logistics and storage solutions.

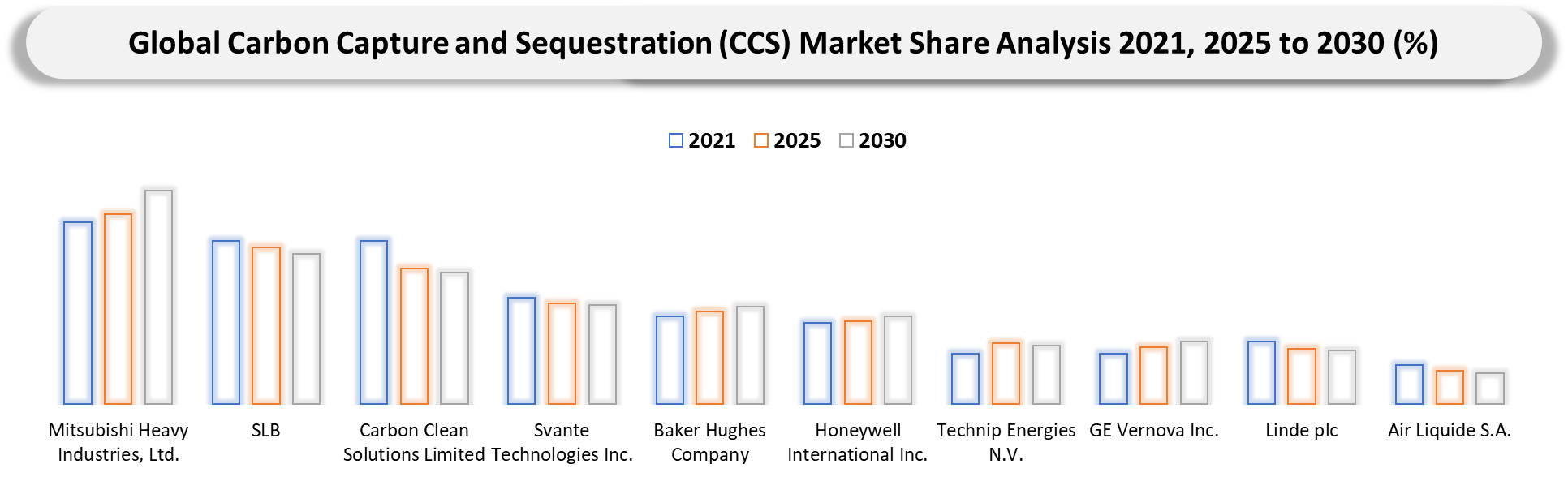

- Key players include ExxonMobil, Shell plc, Chevron Corporation, Equinor, Siemens Energy, Aker Carbon Capture, Fluor Corporation and Mitsubishi Heavy Industries.

- Companies are differentiating through advanced capture technologies such as solvent-based, solid sorbent and direct air capture systems, along with integrated project development capabilities.

- Strategic partnerships between governments and private firms, along with investments in CO₂ transport infrastructure and digital monitoring technologies, are becoming critical to scaling CCS deployment globally.

Key Developments

- April 2026: Halliburton Company expanded its CCS services portfolio, including subsurface storage evaluation and well integrity solutions for long-term carbon sequestration projects.

- March 2026: GE Vernova Inc. demonstrated 100% ammonia combustion in gas turbines, enabling CCS-integrated low-carbon power generation pathways.

- March 2026: Mitsubishi Heavy Industries, Ltd. advanced proprietary CO₂ capture technology for large-scale steel and chemical applications, strengthening industrial decarbonization deployment globally.

- February 2026: Baker Hughes Company partnered with Giammarco Technologies to commercialize hot potassium carbonate capture systems for large-scale industrial decarbonization projects.

- February 2026: TotalEnergies SE strengthened CCS partnerships across Europe, focusing on offshore storage and industrial cluster decarbonization initiatives.

- January 2026: SLB expanded its CCS portfolio, integrating digital subsurface modeling and carbon storage monitoring solutions to optimize sequestration efficiency across global energy projects.

- January 2026: Equinor ASA accelerated Northern Lights CCS project expansion, increasing CO₂ transport and offshore storage capacity for European industries.

- December 2025: Calix Limited scaled low-emissions calcination technology, enabling direct CO₂ separation in cement and lime industries.

- October 2025: Honeywell International Inc. launched advanced solvent-based carbon capture technology integrated with digital optimization tools to improve efficiency and reduce energy consumption.

September 2025: Fluor Corporation delivered FEED services for multiple CCS projects, enhancing carbon capture integration across power and industrial sectors globally.

Why Choose DataM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

Target Audience 2026

- Energy & Industrial Companies: Oil & gas operators, power generation utilities, cement, steel and chemical manufacturers implementing CCS technologies to reduce emissions and meet decarbonization targets.

- Technology Providers & Engineering Firms: CCS technology developers, EPC contractors and engineering consultancies specializing in capture systems, transport infrastructure and storage solutions.

- Carbon Management & Storage Operators: Companies involved in CO₂ transportation, geological storage and utilization, including pipeline operators and subsurface storage developers.

- Government & Regulatory Authorities: Environmental agencies, energy ministries and policymakers driving carbon reduction frameworks, incentives and large-scale CCS project approvals.

- Research Institutions & Academia: Universities, climate research organizations and innovation hubs focused on advancing capture efficiency, storage safety and carbon utilization pathways.

- Investors & Financial Institutions: Private equity firms, infrastructure funds and climate-focused investors tracking CCS project financing, carbon markets and long-term decarbonization opportunities.

- Carbon Market Participants & Corporates: Corporations participating in carbon trading schemes, offset programs and sustainability initiatives leveraging CCS to achieve net-zero commitments.

- Equipment Manufacturers & Supply Chain Players: Manufacturers of capture units, compressors, pipelines, monitoring systems and other critical CCS infrastructure components.

- Environmental Organizations & NGOs: Climate advocacy groups and non-profits monitoring CCS deployment, environmental impact and alignment with global climate goals.