Global Data Center Accelerator Market Growth

The economics of AI infrastructure are being rewritten, and data center accelerators sit at the center of this shift. As enterprises move from experimentation to production-scale AI, procurement decisions around GPUs, FPGAs, and ASICs are no longer optional infrastructure upgrades but strategic investments tied directly to revenue growth, cybersecurity resilience, and digital trust.

This market matters now because compute power has become a bottleneck for AI adoption, cybersecurity workloads, and real-time analytics. Enterprises are no longer just buying hardware. They are investing in scalable, secure, and energy-efficient compute ecosystems that can support generative AI, zero-trust architectures, and cloud-native applications.

From an investment timing perspective, the current phase represents early-to-mid cycle expansion. Hyperscalers have already deployed large GPU clusters, but enterprise and sovereign AI infrastructure adoption is still accelerating. This creates a multi-year demand window for accelerator vendors, cloud providers, and infrastructure integrators.

Data Center Accelerator Market Scope

| Metric | Details |

| Market Size (2025) | USD 21.54 Billion |

| Market Size (2035) | USD 270.77 Billion |

| CAGR | 26.47% |

| Historic Years | 2023-2024 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Segments Covered | Processor, Type, Application, Region |

| Leading Region | North America |

| Fastest Growing Region | Asia-Pacific |

Key Takeaways

- The Data Center Accelerator market forecast for 2035 indicates a more than tenfold expansion, signaling sustained capital inflow into AI infrastructure and cloud ecosystems.

- GPUs account for 28.2% share, but ASICs and FPGAs are gaining traction due to workload-specific efficiency and lower long-term cost structures.

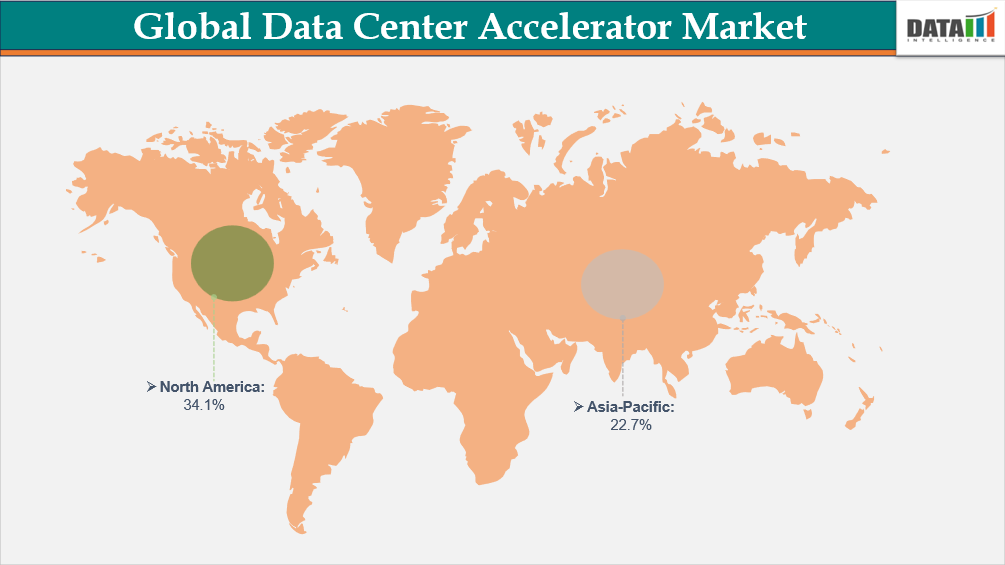

- North America held 34.1% market share in 2025, supported by hyperscaler dominance and early AI adoption.

- Asia-Pacific exceeded 22% share, driven by government-backed digital infrastructure and semiconductor investments.

- Enterprise demand is shifting toward GPU-as-a-service and hybrid deployment models, reflecting evolving pricing and adoption trends.

- Power consumption and cooling costs remain critical constraints, directly influencing procurement strategies and ROI calculations.

Demand Drivers and Enterprise Adoption Patterns

AI Workload Expansion and Digital Trust Requirements

The primary growth driver is the surge in AI and machine learning adoption across industries such as finance, healthcare, and defense. These sectors require low-latency processing for applications like fraud detection, predictive analytics, and autonomous systems. Accelerators enable these workloads at scale while supporting encryption and cybersecurity processing tied to zero-trust frameworks.

The intersection of AI and cybersecurity is particularly important. Accelerators are increasingly used for real-time threat detection, anomaly detection, and encrypted data processing, reinforcing their role in digital trust infrastructure.

Hyperscaler and Cloud Ecosystem Expansion

Cloud providers such as AWS, Microsoft Azure, and Google Cloud are driving large-scale deployments. Their demand extends beyond raw compute into integrated ecosystems that combine accelerators, networking, and software stacks.

This shift is influencing enterprise buyer personas. CTOs and CIOs now evaluate accelerators not just on performance but on ecosystem compatibility, developer support, and cloud integration.

Pricing Models and ROI Considerations

Pricing is evolving from capital expenditure-heavy models to consumption-based offerings such as GPU-as-a-service. This shift is lowering entry barriers for enterprises while enabling vendors to generate recurring revenue streams.

However, ROI calculations remain complex. Buyers must balance performance gains against energy costs, cooling infrastructure, and long-term scalability.

Constraints and Risk Factors

Energy Consumption and Thermal Management

Accelerators require significant power, often drawing several hundred watts per unit. This creates operational challenges, particularly in regions with strict environmental regulations or limited renewable energy access.

Cooling technologies such as liquid cooling and immersion systems are becoming essential but add to capital costs, slowing adoption among mid-sized enterprises.

Supply Chain and Geopolitical Pressure

Export restrictions and semiconductor supply constraints are reshaping vendor strategies. Companies are investing in localized manufacturing and alternative chip architectures to mitigate risk.

Compliance and Regulatory Considerations

Data sovereignty laws and AI governance frameworks are influencing deployment strategies. Enterprises must align accelerator infrastructure with regional compliance requirements, especially in sectors handling sensitive data.

Future Technology Roadmap (2026–2035)

The next decade is expected to witness significant advancements in accelerator architectures as organizations seek higher computational performance and improved energy efficiency. AI training infrastructure will continue to drive demand for increasingly powerful processors capable of handling trillion-parameter models and complex machine learning workloads.

Emerging technologies such as chiplet-based processor designs, advanced packaging solutions, photonic interconnects, and next-generation memory architectures are expected to transform accelerator performance capabilities. The industry is also moving toward heterogeneous computing environments where CPUs, GPUs, ASICs, and FPGAs operate together to optimize workload execution.

As AI adoption expands across industries, accelerator technologies will increasingly support real-time inference, autonomous systems, digital twins, scientific simulations, cybersecurity applications, and edge computing environments. This evolution is expected to create new growth opportunities across the broader data center ecosystem.

Market Opportunities and Investment Hotspots

The Data Center Accelerator Market presents substantial investment opportunities as organizations continue to expand AI infrastructure and modernize digital operations. While accelerator hardware remains a critical component of market growth, significant value creation is increasingly occurring across the broader ecosystem supporting advanced computing environments.

One of the most attractive investment areas is AI cloud infrastructure, where cloud providers are rapidly expanding accelerator-enabled platforms to support machine learning, generative AI, and enterprise analytics applications. Growing demand for AI services is creating opportunities across cloud infrastructure, platform services, and accelerator-as-a-service business models.

High-bandwidth memory technologies and advanced interconnect solutions are emerging as strategic growth areas as organizations seek to maximize data transfer speeds and computational efficiency. As accelerator performance continues to increase, memory architecture and system connectivity are becoming critical factors influencing overall infrastructure performance.

Energy-efficient accelerator architectures are attracting significant attention from investors and enterprise buyers as sustainability becomes an increasingly important procurement criterion. Organizations are prioritizing solutions that deliver greater computational performance while reducing power consumption, operational costs, and environmental impact.

Emerging opportunities are also developing within distributed GPU networks that enable decentralized computing environments capable of supporting large-scale AI workloads. Hybrid cloud and on-premise infrastructure models are gaining traction as enterprises seek to balance scalability, security, compliance, and performance requirements.

Edge AI accelerator deployment represents another high-growth opportunity as organizations increasingly require low-latency processing capabilities for real-time applications. Industries such as manufacturing, healthcare, telecommunications, automotive, and retail are investing in edge computing environments that rely on specialized accelerator technologies.

Software-defined orchestration platforms are becoming increasingly important as enterprises seek centralized management and optimization of accelerator resources across distributed computing environments. These solutions help improve infrastructure utilization, workload scheduling, and operational efficiency.

Additionally, growing cybersecurity requirements are creating opportunities for specialized accelerators designed to support encryption, secure processing, threat detection, and zero-trust security architectures. As digital infrastructure becomes more complex, hardware-based security acceleration is expected to emerge as an increasingly important market segment throughout the forecast period.

Segmentation Insights and Strategic Positioning

The Data Center Accelerator Market is segmented by processor, type, application, and region, reflecting the diverse requirements of modern computing environments. As artificial intelligence, machine learning, cloud computing, and high-performance computing workloads continue to expand, each segment is evolving to address specific performance, efficiency, and scalability requirements.

Processor Landscape

Graphics Processing Units (GPUs) currently account for the largest share of the market due to their exceptional parallel processing capabilities and widespread use in artificial intelligence and machine learning applications. GPUs have become the preferred choice for training large language models, generative AI systems, and high-performance computing workloads that require substantial computational power.

Application-Specific Integrated Circuits (ASICs) are gaining significant traction as organizations seek highly optimized solutions for specific AI and inference workloads. These processors offer improved energy efficiency, lower operating costs, and enhanced performance for dedicated applications, making them increasingly attractive for hyperscale cloud providers and large enterprises.

Field Programmable Gate Arrays (FPGAs) represent one of the fastest-growing segments due to their flexibility and ability to adapt to changing workloads. Their low-latency processing capabilities make them particularly valuable for real-time analytics, networking applications, telecommunications infrastructure, and edge computing environments.

Central Processing Units (CPUs) continue to play a foundational role within accelerator-enabled data centers, serving as the primary control and orchestration layer while working alongside specialized accelerators to optimize workload distribution and overall system performance.

Application-Level Demand

Deep learning training remains the largest and fastest-growing application segment within the Data Center Accelerator Market. The growing adoption of generative AI, large language models, computer vision systems, and advanced analytics platforms is creating substantial demand for high-performance accelerator infrastructure capable of supporting increasingly complex training workloads.

Enterprise interface applications are also witnessing strong growth as organizations integrate artificial intelligence into business operations, customer engagement platforms, cybersecurity solutions, and enterprise software environments. Accelerators are enabling faster data processing, improved automation, and more intelligent decision-making across multiple industries.

Public cloud interface applications continue to expand as cloud service providers invest in accelerator-rich infrastructure to support AI-as-a-Service, machine learning platforms, and high-performance computing services. The increasing availability of cloud-based AI resources is further accelerating market growth and enabling broader access to advanced computing capabilities.

Deployment Models

Cloud data centers currently represent the largest deployment segment due to their scalability, flexibility, and cost-efficiency advantages. Hyperscale cloud providers are investing heavily in accelerator-enabled infrastructure to meet growing demand for AI workloads, analytics applications, and cloud computing services.

At the same time, hybrid deployment models are gaining popularity as enterprises seek greater control over sensitive data, regulatory compliance requirements, and workload management. By combining cloud-based infrastructure with on-premise computing resources, organizations can optimize performance while maintaining operational flexibility and security.

Regional Analysis and Demand Outlook

North America

North America leads the Data Center Accelerator regional analysis with over 34% share.North America continues to dominate the global Data Center Accelerator Market, accounting for a significant share of overall revenue. The region benefits from the presence of leading hyperscale cloud providers, semiconductor manufacturers, artificial intelligence innovators, and advanced research institutions. Strong investments in AI infrastructure, cloud computing, and high-performance computing are driving accelerator adoption across both public and private sectors.

The United States remains the primary growth engine within the region, supported by increasing investments in generative AI, advanced semiconductor technologies, and next-generation data center infrastructure. Government-backed research initiatives, defense modernization programs, and growing enterprise AI adoption are further strengthening market expansion. Additionally, the presence of major technology companies and cloud service providers continues to accelerate innovation and infrastructure deployment.

Asia-Pacific

Asia-Pacific is projected to be the fastest-growing regional market during the forecast period. Rapid digital transformation, expanding cloud infrastructure, increasing AI adoption, and substantial investments in semiconductor manufacturing are creating strong growth opportunities across the region.

China remains a major contributor to regional growth due to its focus on domestic semiconductor development, AI innovation, and large-scale data center expansion projects. India is emerging as an important growth market supported by data localization initiatives, digital economy development, cloud adoption, and government programs aimed at strengthening domestic technology infrastructure. Other countries including Japan, South Korea, Singapore, and Australia are also investing heavily in advanced computing infrastructure to support future digital growth.

Europe

Europe is experiencing steady growth as organizations prioritize digital sovereignty, sustainability, and regulatory compliance. The region is increasingly investing in advanced data center infrastructure that aligns with environmental objectives while supporting AI and cloud computing adoption.

Growing emphasis on green data centers, energy-efficient computing, and responsible AI governance is influencing accelerator deployment strategies across the region. Countries such as Germany, France, the United Kingdom, and the Netherlands are leading investments in next-generation computing facilities, while regulatory frameworks related to data protection and digital sovereignty continue to shape market development.

Competitive Landscape and Vendor Positioning

The Data Center Accelerator top companies include NVIDIA Corporation, Advanced Micro Devices, Inc., Intel Corporation, IBM Corporation, Dell Inc., Lenovo Ltd., Marvell Technology Inc., Qualcomm Incorporated, NEC Corporation, and Microchip Technology Inc.

Competition is shifting from hardware performance to ecosystem control. NVIDIA leads with its CUDA software ecosystem, while AMD and Intel are expanding their accelerator portfolios. Companies like Google are advancing custom ASICs such as TPUs to optimize internal workloads.

Server manufacturers like Dell and Lenovo are focusing on integrated AI-ready systems, while networking and chip companies like Marvell are enhancing data throughput and interconnect efficiency.

Vendor comparison increasingly depends on:

- Software ecosystem strength

- Power efficiency

- Integration with cloud platforms

- Support for zero-trust and secure computing frameworks

Recent Developments

- June 2026- NVIDIA and AMD expanding next-generation AI accelerator deployments

NVIDIA Corporation and Advanced Micro Devices (AMD) accelerated shipments of advanced AI accelerators designed to support large language models, generative AI workloads, high-performance computing (HPC), and cloud infrastructure applications. - May 2026- Intel and Marvell advancing data center processing technologies

Intel Corporation and Marvell Technology Inc. expanded investments in AI-optimized processors, networking accelerators, and data center infrastructure solutions to enhance computing efficiency and workload performance. - In May 2026, NVIDIA Corporation expanded its data center accelerator portfolio with next-generation GPUs optimized for AI and high-performance computing workloads. The initiative focuses on improving processing speed and energy efficiency. This supports advanced data center operations.

- April 2026- Dell Technologies and Lenovo strengthening AI-ready server portfolios

Dell Inc. and Lenovo Ltd. introduced enhanced AI server platforms integrating advanced accelerator technologies to support growing enterprise demand for machine learning, analytics, and cloud computing applications. - April–June 2026- Growing focus on AI infrastructure and high-performance computing

Companies including IBM Corporation, Qualcomm Incorporated, NEC Corporation, and Microchip Technology Inc. expanded development of specialized accelerator architectures, energy-efficient processing technologies, and next-generation data center solutions to address rapidly increasing AI computing

Impact Analysis: Infrastructure and Policy

The push toward sustainable data centers is influencing accelerator design and deployment. Integration with renewable energy sources and battery storage systems is becoming more common, particularly in hyperscale environments.

At the same time, regulatory pressure around data privacy and AI governance is encouraging localized infrastructure investments, reshaping global supply chains.

How This Report Supports Decision-Makers

This report provides actionable insights for:

- Manufacturers evaluating product strategy and innovation focus

- Investors identifying high-growth segments and timing entry points

- Technology companies aligning with AI and cloud infrastructure trends

- Procurement teams optimizing pricing and vendor selection

- Strategy teams assessing competitive positioning and market entry

Why Choose DataM?

Data-Driven Insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. This approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. This personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. These insights complement and go beyond what is typically available in generic databases.

Target Audience

- Semiconductor and hardware manufacturers

- Cloud service providers and hyperscalers

- Enterprise IT and infrastructure leaders

- Investment firms and venture capitalists

- AI and cybersecurity solution providers

- Data center operators and integrators