Agricultural Commodity Market Overview

The global agricultural commodity market encompasses the production, trade, and distribution of essential food and non-food crops such as cereals, oilseeds, sugar, livestock products, and soft commodities. The market is driven by rising global population, increasing food consumption, and growing demand for biofuels and animal feed. Major commodities including wheat, corn, rice, and soybeans dominate global trade flows, supported by large-scale production in regions such as North America, Latin America, and Asia-Pacific. Market dynamics are highly influenced by climatic conditions, input costs such as fertilizers and energy, government policies, and international trade regulations. In recent years, improved crop yields and technological advancements in precision agriculture have supported supply stability. However, volatility persists due to extreme weather events, geopolitical tensions, and supply chain disruptions. Additionally, shifting dietary patterns, sustainability concerns, and increasing focus on food security are reshaping demand trends, encouraging investments in resilient agricultural practices and diversified sourcing strategies across global markets.

Agricultural Commodity Industry Trends and Strategic Insights

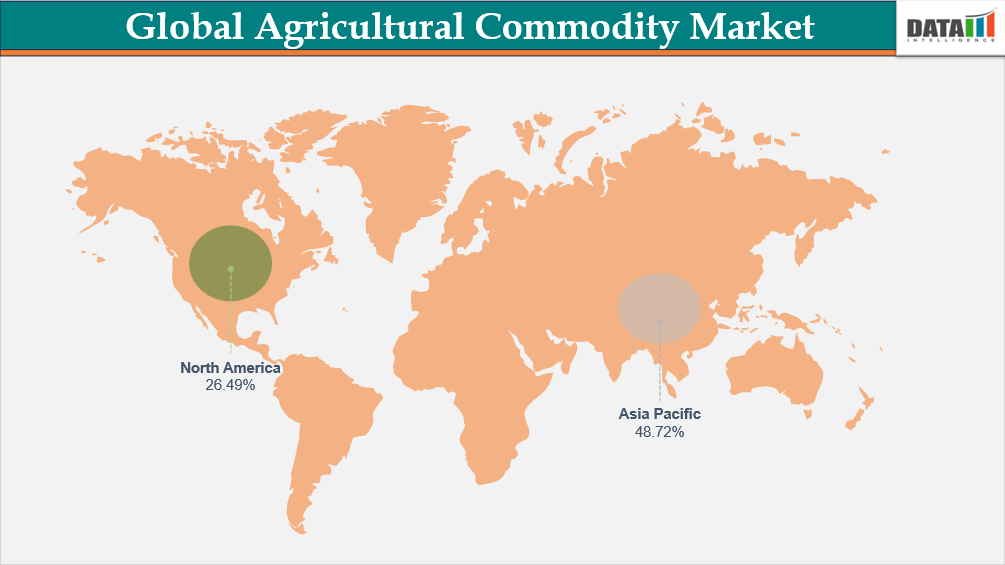

- Asia-Pacific led the global agricultural commodity market in 2025 with a 48.72% revenue share, driven by its large population, strong food demand, expansive agricultural base, and growing exports.

- By commodity type, crops dominated the global agricultural commodity market in 2025 with a 65.4% revenue share, driven by staple food demand, large-scale cultivation, and extensive use in food and bio-based industries.

Global Agricultural Commodity Market Size and Future Outlook

- 2025 Market Size: US$ 1596.85 billion

- 2033 Projected Market Size: US$ 2146.35 Billion

- CAGR (2026–2033): 3.64 %

- Dominating Market: Asia-Pacific

- Fastest Growing Market: North America

Key Takeaways

- The agricultural commodity market is witnessing increasing focus on supply chain resilience, digital trading platforms, and sustainable farming practices, as stakeholders seek to improve productivity, transparency, and long-term food security across global agricultural value chains.

- Asia-Pacific continues to hold a prominent position in the agricultural commodity market due to its large agricultural production base, growing population, expanding food processing industry, and strong demand for staple crops, oilseeds, grains, and livestock feed commodities.

- North America is expected to experience notable growth driven by advanced farming technologies, precision agriculture adoption, increasing export activities, and growing investments in sustainable crop production and agricultural infrastructure modernization.

- Climate variability, changing weather patterns, and evolving trade policies are becoming critical factors influencing agricultural commodity pricing, production planning, and supply-demand dynamics across major producing and consuming regions.

- The growing adoption of precision agriculture, satellite monitoring, data analytics, and farm automation technologies is improving crop yields, resource efficiency, and operational decision-making throughout the agricultural commodity ecosystem.

- Industry participants are increasingly evaluating investments based on supply chain efficiency, sustainability initiatives, commodity diversification strategies, risk management capabilities, and technological advancements rather than focusing solely on production volume expansion.

- Rising global food consumption, increasing demand for biofuel feedstocks, expanding livestock production, and growing requirements for high-quality agricultural raw materials are creating significant opportunities for producers, traders, processors, and agribusiness companies worldwide.

Agricultural Commodity Market Scope

| Metrics | Details | |

| By Commodity Type | Crops, Livestock & Animal Products | |

| By Nature of Product | Conventional, Organic | |

| By Processing Level | Raw / Unprocessed, Semi-Processed, Processed / Value-Added | |

| By Production System | Rainfed Agriculture, Irrigated Agriculture, Controlled Environment Agriculture | |

| By Distribution Channel | Direct Sales, Wholesalers & Traders, Commodity Exchanges, Retail Channels, Online Trading Platforms | |

| By End-User | Food & Beverages, Animal Feed, Biofuels, Industrial Applications, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Norway, Netherlands, Sweden, Denmark, Belgium, Switzerland, Austria, Poland, Finland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Egypt, Turkey, Qatar, Kuwait, Oman, Bahrain | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Market Share, Market Growth | |

For More Detailed Information, Request for Sample

Agricultural Commodity Market Dynamics

Government Food Security Programs are Intensifying Cross-Border Trade and Market Activity

Government interventions in food security are increasingly affecting commodity markets. Programs such as the Global Agriculture and Food Security Program (GAFSP), which aim to provide financial support to small-scale farmers and agribusiness in developing nations, have begun guaranteeing a steady market and supply. By providing these assurances, the food security programs encourage active engagement in the markets or trade groups, which helps to enhance liquidity.

The infusion of resiliency into food systems also fuels border trade, as countries attempt to strike a balance between internal security and inter-country demands. The fact that GAFSP has helped fund over 323 projects and programs across 55 countries, helping almost 32 million people, is indicative of how effective programs can increase trade routes, bring commodities to global markets, and bolster resiliency for citizens. All of this helps ensure food security for those who need it, but also increases trading activity within commodity systems.

Agricultural Commodity Market Segmentation Analysis

The global Agricultural Commodity market is segmented based on commodity type, nature of product, processing level, production system, distribution system, end-user and region.

Crops Dominate Global Agricultural Commodities Market Due to Their Central Role in Food and Industrial Supply

Under commodity type, crops are a substantial contributor to the global share of agricultural commodities due to their importance as the backbone of global food supplies and trade. According to FAO, global production levels of primary crops in 2023 recorded 9.9 billion tons, which signifies a growth of 3% from 2022 levels and a growth of 27% from levels experienced in 2010. Hence, it indicates that crops are a fundamental contributor to meeting increased demand. Due to large supplies and consumption levels, crops are still the dominant type of agricultural commodity.

In this category, cereals take the lead in terms of production, which increases by 2% in 2023, mainly contributed to by maize. In fact, maize, wheat, and rice, which are crucial crops in a global context, contribute a collective total of 91% to the production of all cereals. In this context, a remarkable increase has also been noted in the production of sugar crops like sugar cane, along with fruits, vegetables, roots, and tubers. The rise of oil crops such as oil palm fruit, soybeans, and rapeseed, reaching 893 million tons, further strengthens the commanding market share of crops worldwide.

Agricultural Commodity Market Geographical Penetration

DOMINATING MARKET:

Asia-Pacific’s Market Dominance Driven by Large Population, High Crop Production, and Favorable Farming Conditions.

Asia-Pacific is considered to be one of the highest contributors to the share of the world market in agricultural commodities due to a number of factors like its large population, agro-climatic conditions, large agricultural production base, and high agricultural productivity. Also, countries like China and India are considered to be among the largest propellers and consumers of agricultural commodities like rice, wheat, and sugar; they possess large agricultural availability and high per capita labor. Besides, there is an increase in modern technology.

India Agricultural Commodity Market Outlook

The country possesses a higher share in Asia-Pacific agricultural commodity markets owing to its large agricultural land and the number of farmers. The positivity has been seen in foodgrains that now total higher production compared to 265.05 million tons in 2014-15. The production of foodgrains is now increased to an estimate of 347.44 million tons in 2024-25. The favorable climatic conditions make India produce various crops through different seasons. The list of crops includes rice, wheat, pulses, and spices. To increase agricultural commodity exports further, the Bharati initiative was launched in September 2025. The initiative is to provide support to 100 agri food and agri-tech startups.

China Agricultural Commodity Market Trends

China holds a significant share in the APAC agricultural commodity market due to its sheer capacity and export participation. For instance, the export volume figure for Chinese agricultural products, from the beginning of the 14th five-year plan (from 2021 to 2025), rose from 544.34 billion yuan or US$77.83 billion in 2021 to 732.75 billion yuan in 2024, which is an increase of 34.6% over the previous year to demonstrate the strong foothold for the production and export demand. At the end of the first 11 months of 2025, the export volume for agricultural products from China had encompassed 224 countries and regions, which demonstrates the key position held by China on its territory regarding the APAC market.

Agricultural Commodity Regulatory Analysis

Agricultural commodity markets are regulated by country and international bodies to ensure transparency in the respective commodity markets and the prices charged in the market. Such bodies include the Food and Agriculture Organization and the World Trade Organization that stipulate the regulations that characterize the global commodity market. On the country level, the US Department of Agriculture or the Ministry of Agriculture for a given country may be the governing body.

The quality control and trade compliance are done by various agencies such as the Codex Alimentarius Commission, the APEDA of India, and the EU Food Safety Authority, among others. They implement standards about food grading, safety, storage, and export certification. Sanitary and Phytosanitary (SPS) regulations need to be implemented for international trade. The regulations are indeed important, but increase operational costs for producers/exporters as well.

Agricultural Commodity Competitive Landscape

- The agricultural commodity market is a highly fragmented market with many global and regional players in the grains, oilseeds, and livestock segments

- Major companies include Cargill Inc., Archer Daniels Midland (ADM), Bunge Limited, CHS Inc, Louis Dreyfus Company (LDC), COFCO International, Olam Group, Wilmar International, Marubeni Corporation, Tyson Foods, JBS S.A., Marfrig Global Foods, BRF S.A., Fonterra Co-operative Group, Danone, Bayer AG, and Amaggi

- Market forces are shaped by fluctuations due to demand and supply, nature, and geopolitics. Price volatility is an essential factor that differentiates market forces. They are also characterized by global consumption patterns and value chain speculation. Increased technological innovation, like precision farming, is providing opportunities for establishing differentiation.

Key Developments of the Agricultural Commodity Market

- In January 2026, Avendus Capital advised Arya.ag on its INR 7.25 billion Series D investment led by GEF Capital Partners. The funding is aimed at scaling Arya.ag’s climate-smart agricultural solutions, strengthening post-harvest infrastructure, and enhancing digital platforms for efficient agricultural commodity trading and supply chain management.

- In July 2025, Bunge Global SA completed its merger with Viterra, creating a major global agribusiness and commodity trading powerhouse. The merger significantly enhanced global grain sourcing, processing, and export capabilities, strengthening supply chain integration across key agricultural markets.

Why Choose DataM

- Latest Data & Forecasts – Comprehensive, up-to-date insights and projections through 2033. Coverage includes global value by commodity type, nature of product, processing level, production system, distribution system, end-user and region. Scenario forecasts with region-level splits (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa) and sensitivity to factors such as regulatory reclassification and raw-material costs.

- Regulatory Intelligence – Actionable analysis of regulatory frameworks that materially affect Agricultural Commodity commercialization, revenue by country, allowable label claims, permitted doses, import/export controls and advertising restrictions.

- Competitive Benchmarking – Standardized profiling and benchmarking of leading pharma and nutraceutical players, contract manufacturers and e-commerce specialists active in the market.

- Geographic & Emerging Market Coverage – Region-by-region market sizing, growth drivers, reimbursement dynamics, cultural/consumer behavior and market access considerations. Focus on high-growth or regulatory-uncertain markets.

- Actionable Strategies – Identify opportunities for launching innovative products, while leveraging strategic partnerships and supply chain integration for maximum ROI.

- Pricing & Cost Analysis – In-depth assessment of price trends, raw material costs and sustainability-driven cost efficiencies across regional markets.

- Expert Analysis – Insights from industry experts such as product specialists, regulatory affairs professionals and key manufacturing companies.

Target Audience

- Agribusiness Enterprises– Large-scale farming corporations, agribusiness conglomerates, food processors and vertically integrated producers relying on data-driven operations, supply chain efficiency and yield optimization.

- Commodity Traders & Market Operators – Commodity trading firms, exchanges, brokers and risk management desks involved in agricultural commodities such as grains, oilseeds, livestock, soft commodities and agri-derivatives.

- Regulatory & Policy Bodies– Government ministries of agriculture, food safety authorities, trade regulators and environmental agencies overseeing agricultural policy, commodity standards, sustainability and trade compliance.

- Agritech & Innovation Leaders – Agritech startups, precision agriculture providers, AI and data analytics firms, IoT solution developers and climate-tech innovators building next-generation farming and commodity intelligence platforms.

- Investors & Financial Institutions – Venture capital firms, private equity funds, hedge funds, banks and development finance institutions investing in agriculture, commodities, food security and sustainable farming technologies.

- Supply Chain & Logistics Providers – Storage operators, grain elevators, cold chain providers, shipping companies, port operators and logistics firms enabling efficient movement of agricultural commodities from farm to market.

- Research & Academic Institutions– Agricultural universities, research institutes and policy think tanks focused on crop science, climate impact, yield modeling, commodity forecasting and food system resilience.