Aerospace Aluminum Market Overview

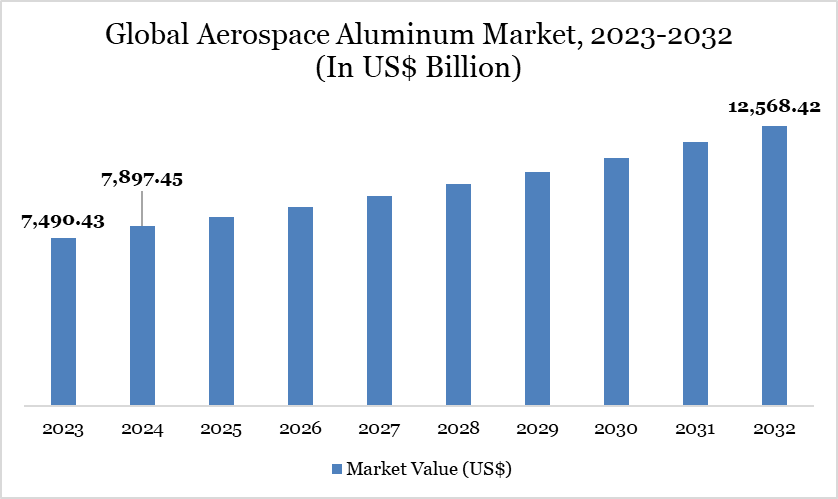

The aerospace aluminum market reached US$ 8,374.50 million in 2025 and is expected to reach US$ 15,119.60 million by 2035, growing at a CAGR of 6.04% during the forecast period 2026-2035.

The global aerospace aluminum market is being driven by the increasing demand for lightweight and high-strength materials in commercial and military aircraft, which enhances fuel efficiency and reduces carbon emissions. This growth is reinforced by the rapid expansion of international air travel, as reported by the International Air Transport Association (IATA), which noted a rise of 11.8% in premium-class passengers in 2024, indicating higher demand for advanced aircraft capable of supporting luxury and long-haul travel. Innovations in aluminum-lithium and other high-performance alloys are enabling manufacturers to produce lighter, stronger aircraft components, meeting the evolving needs of both premium and economy air travel.

The market is further supported by the growth of aerospace infrastructure in regions like Asia-Pacific, where economy class travel surged 28.6% to 500.8 million passengers, highlighting increased aircraft production and modernization. Europe continues to dominate premium travel with 39.3 million passengers, driving demand for robust aluminum components in commercial fleets. Meanwhile, the Middle East’s high share of premium travelers at 14.7% emphasizes the need for durable, lightweight materials in long-haul and luxury aircraft. Overall, rising air travel, technological advancements in alloys, and regional passenger growth are collectively fueling the steady expansion of the aerospace aluminum market.

Key Takeaways

- The market is expected to add more than USD 6.7 billion in new revenue opportunities between 2025 and 2035 due to expanding aircraft manufacturing and replacement programs.

- Commercial aviation remains the largest demand generator as aircraft manufacturers continue increasing the use of lightweight aluminum components in fuselage, wings, and structural assemblies.

- Advanced aluminum-lithium and high-strength alloys are receiving significant investment as aerospace manufacturers seek improved mechanical performance with lower aircraft weight.

- Sustainability initiatives, including recycled aluminum adoption and low-energy production techniques, are influencing procurement decisions across the aerospace value chain.

- Asia-Pacific maintains its leadership position owing to rapid passenger traffic growth, expanding airport infrastructure, and increasing regional aircraft manufacturing capabilities.

- Strategic partnerships between aluminum producers and aerospace companies are accelerating the commercialization of specialized alloys suitable for additive manufacturing and next-generation aircraft programs.

Aerospace Aluminum Market Trend

The aerospace aluminum market is witnessing a strong shift toward lightweight, high-strength alloys to improve fuel efficiency and reduce emissions, driven by increasing air travel demand and stricter environmental regulations. Advanced manufacturing techniques, such as additive manufacturing and precision casting, are gaining traction to enhance material performance and reduce production costs. Additionally, the integration of recycled aluminum and sustainable practices is becoming a key trend, as the industry focuses on circular economy principles. Strategic collaborations between aluminum producers and aerospace manufacturers are also on the rise to innovate next-generation alloys tailored for aerospace applications.

For more details on this report - Request for Sample

Market Scope

| Metrics | Details |

| Market Size in 2025 | USD 8,374.50 million |

| Market Size by 2035 | USD 15,119.60 million |

| CAGR | 6.04% (2026-2035) |

| Historic Years | 2023-2024 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Segments Covered | Alloy Type, Form, Process, End User, Region |

| Leading Region | Asia-Pacific |

| Fastest Growing Region | Asia-Pacific |

Aerospace Aluminum Market Dynamics

Demand for Lightweight Materials in Aircraft

The demand for lightweight materials in aircraft is a major driver of the aerospace aluminum market. Airlines and manufacturers are prioritizing fuel efficiency and emission reduction, which requires materials with a high strength-to-weight ratio. Aluminum alloys are ideal because they provide durability and corrosion resistance while keeping aircraft weight low.

This growing focus on lightweight design is particularly strong in commercial aviation, where every kilogram saved can reduce fuel consumption and operational costs. As new aircraft models are developed, aluminum continues to be preferred over heavier metals. Additionally, the push for greener aviation solutions further reinforces the adoption of aluminum alloys in structural components. This trend is expected to sustain strong market growth in the coming years.

High Production and Processing Costs

High production and processing costs significantly restrain the aerospace aluminum market by increasing the overall expenses for manufacturers. Aluminum alloys used in aerospace require advanced technologies, precision equipment, and skilled labor, all of which drive up operational costs.

These elevated costs limit the ability of smaller or emerging players to enter the market and compete effectively. Additionally, high production expenses can make end-products more expensive, reducing demand from cost-sensitive aerospace customers. As a result, growth in the aerospace aluminum sector may be slowed, especially in regions with price-sensitive markets.

Aerospace Aluminum Market Segment Analysis

The global aerospace aluminum market is segmented based on alloy type, form, process, end-user, and region.

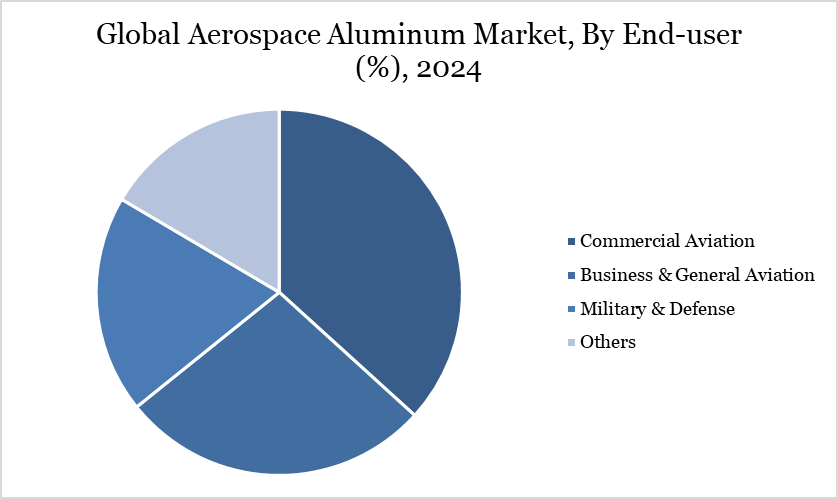

Commercial Aviation Drives Aerospace Aluminum Market for Lightweight, Fuel-Efficient Aircraft Structures

Commercial aviation holds a significant share in the aerospace aluminum market as passenger aircraft extensively rely on lightweight, high-strength aluminum alloys for fuselage, wings, and other structural components. Aluminum’s superior strength-to-weight ratio helps airlines improve fuel efficiency, reduce operating costs, and meet stringent safety standards, making it a preferred material in aircraft manufacturing.

The importance of commercial aviation is further highlighted by the high flight frequency observed from, 30th December 2024, to 17th August 2025, when a total of 24,104,736 one-way flights were scheduled, averaging 104,803 flights per day. This extensive operational demand drives continuous consumption of aerospace-grade aluminum, reinforcing the sector’s pivotal role in market growth and the sustained need for high-performance aluminum alloys.

Aerospace Aluminum Market Geographical Share

Asia-Pacific Dominates Aerospace Aluminum Market Due to Rapid Aviation Growth and Expanding Aircraft Manufacturing Hub

Asia-Pacific commands a significant share in the Aerospace Aluminum market due to its expanding aviation industry and growing investments in aircraft manufacturing. Countries like China, Japan, South Korea, and India are driving demand for lightweight, high-strength aluminum alloys to support both commercial and defense aircraft production. Rising passenger traffic and modernization programs across the region further boost the need for advanced aerospace materials.

According to the IEA, India’s aviation market is rapidly growing, with domestic and international travelers projected to exceed 500 million by 2030, making it a potential global leader by 2047. Passenger traffic surged in 2022, with domestic travel up nearly 50% and international travel over 150%, while the first half of 2023 saw a 32% year-on-year increase. The expansion of airports from 74 in 2014 to 147 in 2022, expected to reach 220 by 2025, highlights the region’s infrastructure development, further reinforcing Asia-Pacific’s strong role in the aerospace aluminum market.

Sustainability Analysis

The Aerospace Aluminum market is increasingly focusing on sustainability through the adoption of lightweight, fuel-efficient aluminum alloys that reduce aircraft emissions. Manufacturers are investing in recycling programs and secondary aluminum use to minimize environmental impact and conserve resources. Innovations in production processes, such as energy-efficient casting and extrusion techniques, further lower the carbon footprint of aluminum components. Regulatory pressures and industry standards are pushing aerospace companies toward greener supply chains and eco-friendly material sourcing.

Aerospace Aluminum Market Major Players

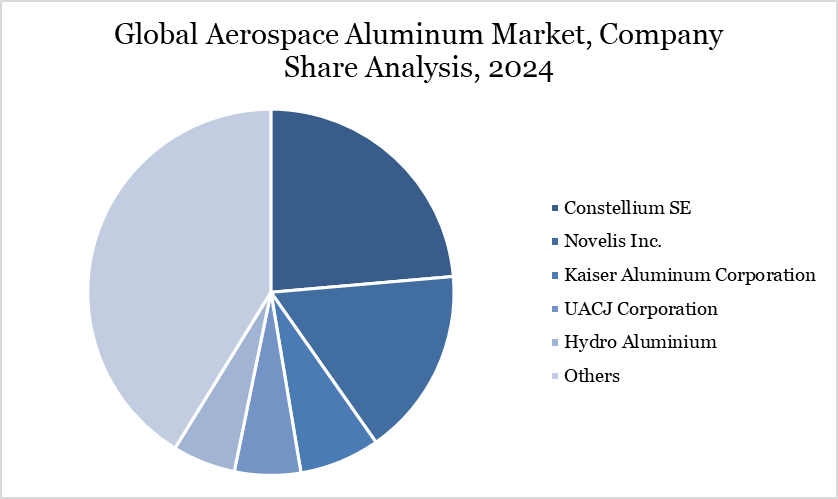

The major global players in the market include Constellium SE, Novelis Inc., Kaiser Aluminum Corporation, UACJ Corporation, Hydro Aluminium, China Zhongwang Holdings Limited, Arconic Corporation, SAPA Group, Gulf Extrusions Company, Alcoa Corporation.

Recent Developments:

- On April 24, 2026, Kaiser Aluminum reported stronger aerospace and high-strength aluminum shipments in Q1 2026, driven by recovering commercial aerospace demand and recently completed capacity expansion projects. The company raised its 2026 aerospace outlook, reflecting growing demand for lightweight aluminum plate and extrusion products used in next-generation aircraft manufacturing.

- On January 26, 2026, Century Aluminum Company announced participation in a major U.S. aluminum smelter project alongside Emirates Global Aluminium (EGA), marking the first new primary aluminum smelter planned in the United States in nearly five decades. The project is expected to strengthen domestic aluminum supply for aerospace, defense, and transportation applications while supporting long-term lightweight material demand.

- On January 30, 2026, industry reports highlighted cautious but improving sentiment across the U.S. aluminum extrusion sector, supported by aerospace and defense demand despite ongoing raw material cost pressures and tariff uncertainties. Aerospace applications remained one of the strongest growth segments for advanced aluminum extrusions and specialty alloys.

- On February 20, 2026, Kaiser Aluminum projected a return to aerospace aluminum shipment growth in 2026 following inventory normalization and renewed aircraft production activity. The company emphasized rising demand for high-strength aerospace plate and extrusion products as global aircraft manufacturing continues recovering.

- On December 18, 2025, market analysts reported that Europe’s aluminum sector entered 2026 under pressure from tightening supply conditions, Carbon Border Adjustment Mechanism (CBAM) implementation, and rising energy costs. These developments are expected to influence aerospace aluminum pricing and accelerate investments in sustainable and low-carbon aluminum production.

- On October 23, 2025, Lockheed Martin Corporation partnered with NioCorp Developments Ltd. under a Pentagon-funded initiative to develop scandium-enhanced aluminum alloys for aerospace and defense applications. The collaboration supports next-generation lightweight materials offering improved strength, corrosion resistance, and additive manufacturing capabilities.

- On July 2025, Constellium SE expanded investments in advanced aerospace aluminum alloys and recycling technologies to support future aircraft programs. The company focused on lightweight, recyclable aluminum solutions and friction stir welding technologies aimed at reducing aircraft weight and improving manufacturing efficiency.

- On April 30, 2025, Airbus subsidiary APWORKS partnered with Equispheres to strengthen North American production of Scalmalloy, a high-performance aluminum-magnesium-scandium alloy designed for aerospace additive manufacturing. The partnership supports growing adoption of advanced aluminum alloys in lightweight aircraft structures and next-generation aerospace components.

Why Choose DataM?

Data-Driven Insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. This approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. This personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. These insights complement and go beyond what is typically available in generic databases.

Target Audience

Manufacturers/ Buyers

Industry Investors/Investment Bankers

Research Professionals

Emerging Companies