Low GWP Refrigerants Enter a More Volatile Growth Cycle

U.S. policy is shifting, global cooling demand is rising and refrigerant choice is becoming a strategic equipment decision.

The 2026 U.S. regulatory reversal may slow some near term conversions, while global cooling demand, Kigali led HFC reductions and OEM redesign roadmaps continue to support the low GWP refrigerants market. Explore the DataM Intelligence Low GWP Refrigerants Market report.

A U.S. regulatory reversal changes the timing of the transition

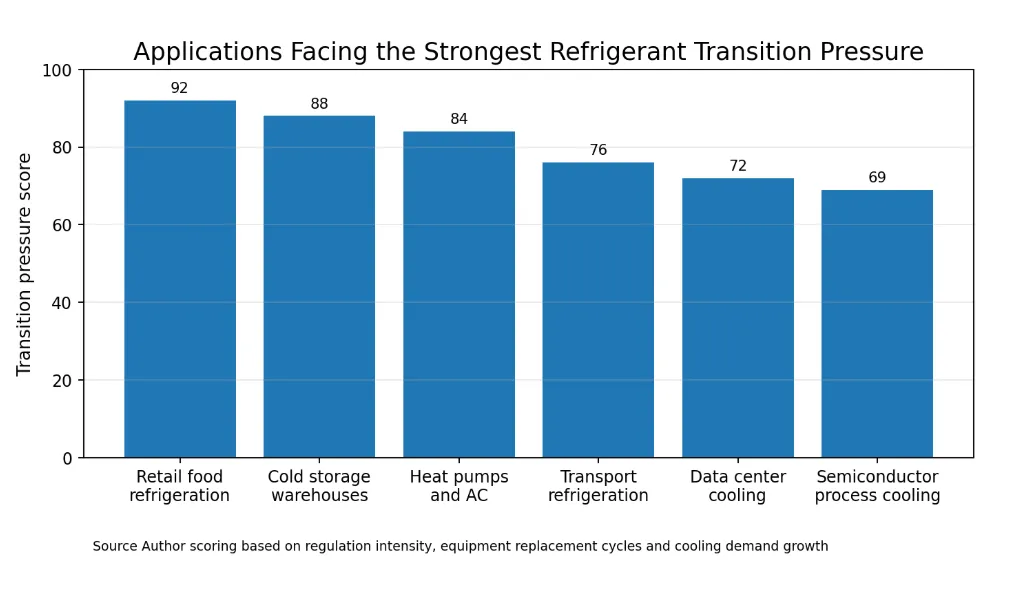

The low GWP refrigerants market entered 2026 with a new layer of uncertainty after the U.S. Environmental Protection Agency moved to relax parts of earlier HFC transition rules. The action was framed by the Trump administration as an affordability measure for grocery stores, food refrigeration operators and air conditioning users. It also extended compliance relief across selected applications such as retail food refrigeration, cold storage warehouses, residential cooling and semiconductor manufacturing.

The policy shift matters because refrigerant regulation is directly tied to capital spending. Grocery chains, cold storage operators and building owners do not buy refrigerant in isolation. They buy new equipment, redesign refrigeration racks, train service teams, update leak management practices and secure long term supply contracts. A delayed compliance date can therefore change project timing, procurement plans and near term demand for low GWP refrigerants.

The reversal has also created a split inside the market. Some food retail groups welcomed the relief because the earlier timeline created cost pressure for stores with large installed refrigeration systems. Equipment and refrigerant industry groups warned that uncertainty can raise service costs because manufacturers have already redesigned products, retooled factories and trained technicians around next generation refrigerant systems.

The market direction still points toward lower climate impact cooling

The U.S. reversal changes the pace of transition more than the long term direction. The American Innovation and Manufacturing Act still requires a national phase down of HFC production and consumption. The Kigali Amendment also continues to push global HFC reductions across developed and developing markets. Europe remains on an aggressive F gas path, while Asia Pacific demand for cooling continues to expand rapidly.

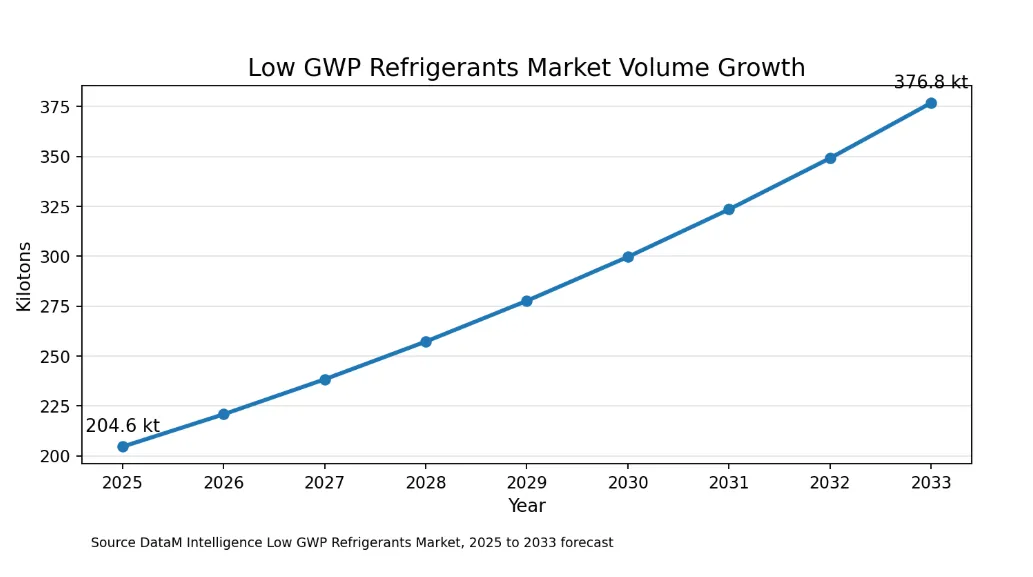

This is why the low GWP refrigerants market remains a growth market even during policy volatility. DataM Intelligence estimates that the global low GWP refrigerants market will expand from 204.6 kilotons in 2025 to 395.8 kilotons by 2035, reflecting a 4.2% CAGR. Asia Pacific is expected to remain the largest and fastest growing region because cooling demand, cold chain expansion and industrial refrigeration investment are rising together.

The regulatory debate should therefore be understood as a sequencing issue. In the near term, some U.S. replacement cycles may slow. Over the medium term, OEM design roadmaps, global refrigerant standards and customer sustainability targets continue to pull the market toward lower GWP alternatives.

Low GWP refrigerant growth depends on HFO blends, natural refrigerants, equipment redesign and regional compliance schedules. Eplore the Low GWP Refrigerants Market report

The climate gap between legacy and next generation refrigerants is too large to ignore

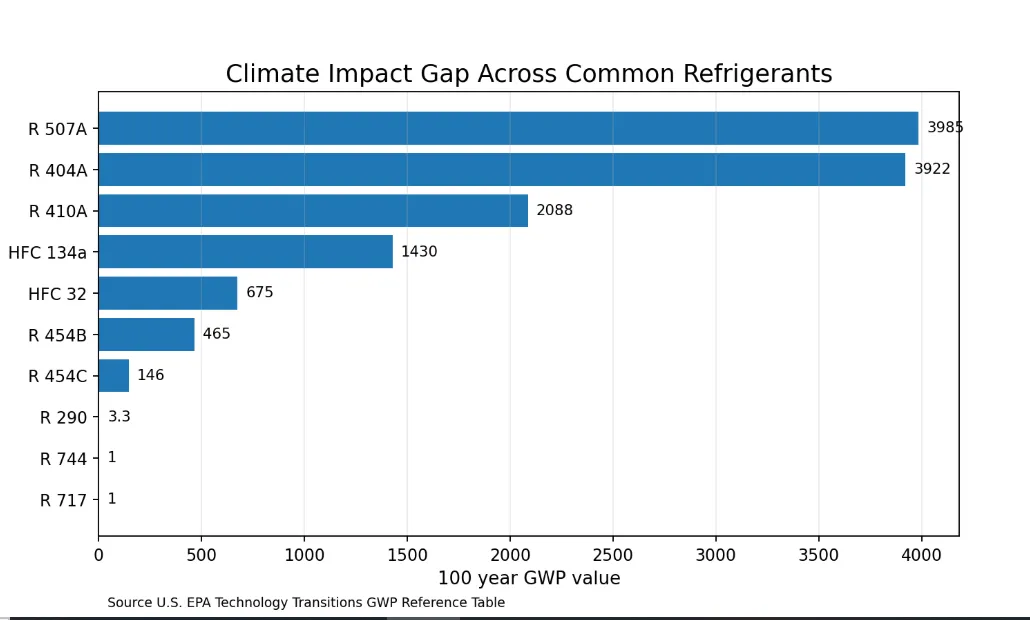

The core reason low GWP refrigerants remain strategically important is the size of the climate impact gap. EPA reference values show that common legacy blends such as R 404A and R 410A carry GWP values far above newer options. R 404A has a 100 year GWP of 3,922, while R 410A has a GWP of 2,088. By comparison, R 454B has a GWP of 465, R 454C has a GWP of 146 and natural refrigerants such as CO2, ammonia and propane have very low GWP values.

This difference is reshaping equipment design. Refrigeration and HVAC buyers increasingly evaluate refrigerants through four lenses. They examine climate impact, safety classification, equipment efficiency and lifecycle service cost. A refrigerant that works well in one application may be unsuitable in another because pressure, flammability, toxicity or charge size can change the economics of the full system.

Refrigerant choice is now an equipment architecture decision

Low GWP adoption is difficult because the transition often requires new equipment architectures. HFO blends can support familiar system designs, but many are mildly flammable and require updated safety procedures. CO2 systems can be attractive in commercial refrigeration, but they operate at high pressure and require specialized components. Ammonia remains powerful in industrial refrigeration, while safety and location requirements limit where it can be deployed. Hydrocarbons can deliver strong efficiency in smaller systems, although charge limits and flammability rules shape adoption.

This means the market is moving from refrigerant substitution toward system redesign. Compressor suppliers, valve makers, controls companies, leak detection providers and service contractors all become part of the refrigerant transition. The companies that benefit most will be those that help customers lower GWP while improving energy efficiency, reliability and serviceability.

Retail food and cold storage are the most exposed commercial battlegrounds

Food retail is at the center of the U.S. policy debate because refrigeration is a large and unavoidable operating cost for supermarkets. Stores often run complex rack systems, refrigerated display cases, walk in coolers and freezers. Replacing or retrofitting those assets can be expensive, disruptive and difficult to schedule without affecting store operations.

The 2026 U.S. policy shift gives some retailers more time, but it also creates a planning challenge. Chains that already invested in lower GWP systems may now face competitors with extended use of older assets. Smaller grocers may gain breathing room, although they still need to prepare for future refrigerant availability and service cost changes. Refrigerant supply will become more constrained as HFC phase down allocations continue, which means older systems could become more expensive to maintain even when compliance deadlines move.

Cold storage warehouses face a similar issue. Demand for frozen food, pharmaceutical storage and temperature controlled logistics is rising, but operators must balance system reliability with refrigerant compliance. For many facilities, the best return will come from pairing refrigerant transition with energy efficiency upgrades, leak reduction and digital monitoring.

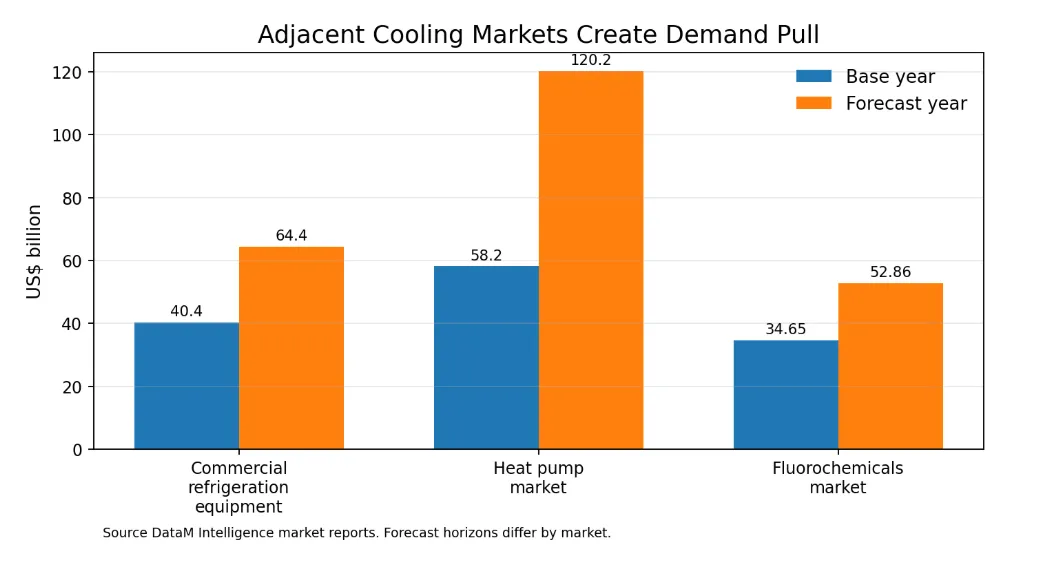

Commercial refrigeration is at the forefront of the refrigerant transition, where evolving regulations directly influence capital investment, equipment upgrades, and operational planning. Explore the Commercial Refrigeration Equipment Market report for in-depth insights into technology trends, regulatory developments, and growth opportunities shaping the industry.

Cooling demand makes the transition global

The refrigerant market is being pulled by a much larger trend. Cooling demand is rising globally as urbanization, income growth, heat exposure, data center buildout and cold chain expansion increase demand for air conditioning and refrigeration. The International Energy Agency has estimated that air conditioners and electric fans already account for around 10 percent of global electricity consumption, with cooling demand expected to rise sharply in coming decades.

This creates a double challenge. The world needs more cooling, but it needs cooling systems with lower direct refrigerant emissions and better energy efficiency. Low GWP refrigerants solve only part of the problem. System efficiency, insulation quality, building design and maintenance also determine the real emissions footprint of cooling.

Heat pumps add another layer to the market. As governments promote electrified heating, heat pump deployment increases demand for refrigerants that can support efficient heating and cooling across different climates. Heat pumps increase the importance of safe, efficient and lower GWP refrigerants in buildings. Explore the Heat Pump Market report.

Who benefits as old and new refrigerant systems coexist

The strongest beneficiaries are likely to be suppliers that can operate across transition complexity. Refrigerant producers with low GWP portfolios benefit as OEMs redesign equipment around HFO blends, natural refrigerants and lower GWP alternatives. Component makers benefit because compressors, valves, sensors and heat exchangers often need to be optimized for new refrigerant properties.

Reclaimers and service networks also stand to gain. As HFC supply tightens and old systems remain in operation, reclaimed refrigerant becomes more important for maintenance. Contractors with A2L training, CO2 system expertise and leak management capabilities may gain pricing power because customers will need qualified service during a mixed equipment cycle.

End users with disciplined transition programs could also benefit. Grocers, cold storage companies and industrial users that manage equipment replacement before emergency failure can lower retrofit costs and reduce stranded asset risk. The best positioned buyers will treat refrigerant strategy as part of capital planning rather than a last minute compliance exercise.

Fluorochemical producers remain central because HFO blends, refrigerant recovery and specialty chemistry determine transition availability. Explore the Fluorochemicals Market report.

Where the low GWP refrigerants market is headed

The next phase of the market will be shaped by four priorities. First, companies will need transition plans that can survive policy swings. Second, energy efficiency will become as important as GWP because electricity cost is often the largest lifetime cooling cost. Third, reclaimed refrigerant supply will become more valuable as legacy HFCs become tighter. Fourth, application specific refrigerant selection will matter more than universal substitution.

This creates a more segmented market. Retail food may lean toward CO2 and selected HFO blends. Residential air conditioning and heat pumps may move toward A2L refrigerants. Industrial refrigeration may continue using ammonia and CO2 where safety and scale support the economics. Smaller equipment categories may use hydrocarbons where charge limits allow.

The U.S. reversal slows parts of the compliance timetable, but it also highlights why the market needs more clarity. Refrigerant transitions involve factories, contractors, stores, warehouses and homeowners. When policy signals change, the entire equipment chain absorbs the uncertainty.

Even so, the direction of travel remains clear. Cooling demand is rising, high GWP refrigerants face long term pressure and equipment makers are already designing around lower climate impact alternatives. The low GWP refrigerants market is entering a more volatile phase, while the long term investment case remains tied to efficient, safe and lower emission cooling.