Static Var Compensator Market Overview

The market is experiencing steady growth as utilities, transmission system operators, renewable energy developers, and industrial facilities increasingly invest in advanced reactive power compensation solutions to strengthen grid stability, improve power quality, and support the integration of renewable energy sources. Rising electricity demand, grid modernization initiatives, and expanding high-voltage transmission infrastructure continue to drive market expansion globally.

As there is a fast uptake of renewable energy sources into the electric power generation system, there is a need for the provision of swift responses aimed at balancing the voltage and reactive power in the electric power generation system.

The continued use of electricity from renewable sources, resulting in the need for SVCs to help keep the voltage levels within the electric grid stable. Some of the industries have a high dependency on SVCs including the steel manufacturing industry, the mining sector and the railroad transportation sector since there are constant fluctuations in load levels, which require them to balance their voltage levels. The demand for electricity from industries will rise because of efforts to de-carbonize production methods.

Static Var Compensator Industry Trends and Strategic Insights

- SVC retains commercial viability where rapid, reliable reaction capability and a track record of references and operation are required.

- The transmission network, railways and industrial power networks still offer the most compelling justification for SVCs of utility quality.

- Increasing competition from STATCOMs and hybrids necessitates application-focused communication rather than categorical promotion.

Key Takeaways

- The increasing focus on grid modernization, renewable energy integration, and transmission network stability is emerging as a key industry trend, with utilities deploying static var compensators (SVCs) to enhance voltage regulation, improve power quality, and strengthen overall grid reliability.

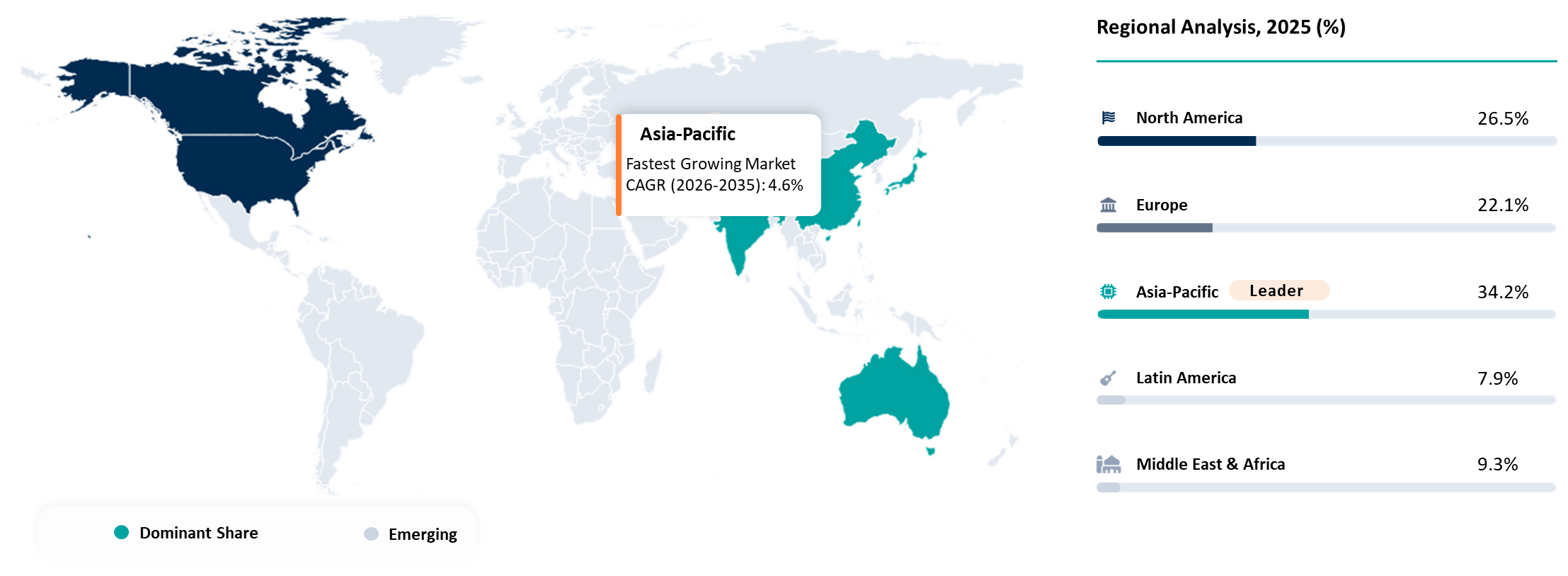

- Asia-Pacific maintains a leading position due to rapid industrialization, expanding power transmission and distribution infrastructure, large-scale renewable energy installations, and rising electricity demand across developing economies.

- North America is projected to record significant growth as aging grid infrastructure modernization, increasing renewable energy integration, expanding utility-scale transmission projects, and investments in smart grid technologies continue to drive demand for advanced reactive power compensation solutions.

- Stringent grid reliability standards, increasing power quality requirements, and the need to maintain voltage stability across high-voltage transmission networks are becoming major factors accelerating the deployment of static var compensators globally.

- The growing integration of wind farms, solar power plants, rail electrification systems, mining operations, and energy-intensive industrial facilities is increasing demand for static var compensators capable of delivering fast and dynamic reactive power compensation.

- Industry participants are increasingly evaluating investments based on technological innovation, digital monitoring capabilities, grid integration expertise, lifecycle service offerings, and operational efficiency rather than focusing solely on equipment installation capacity.

- Rising investments in renewable energy projects, high-voltage transmission corridors, smart grid development, industrial electrification, and cross-border power interconnection networks are creating significant opportunities for static var compensator manufacturers and power system solution providers worldwide.

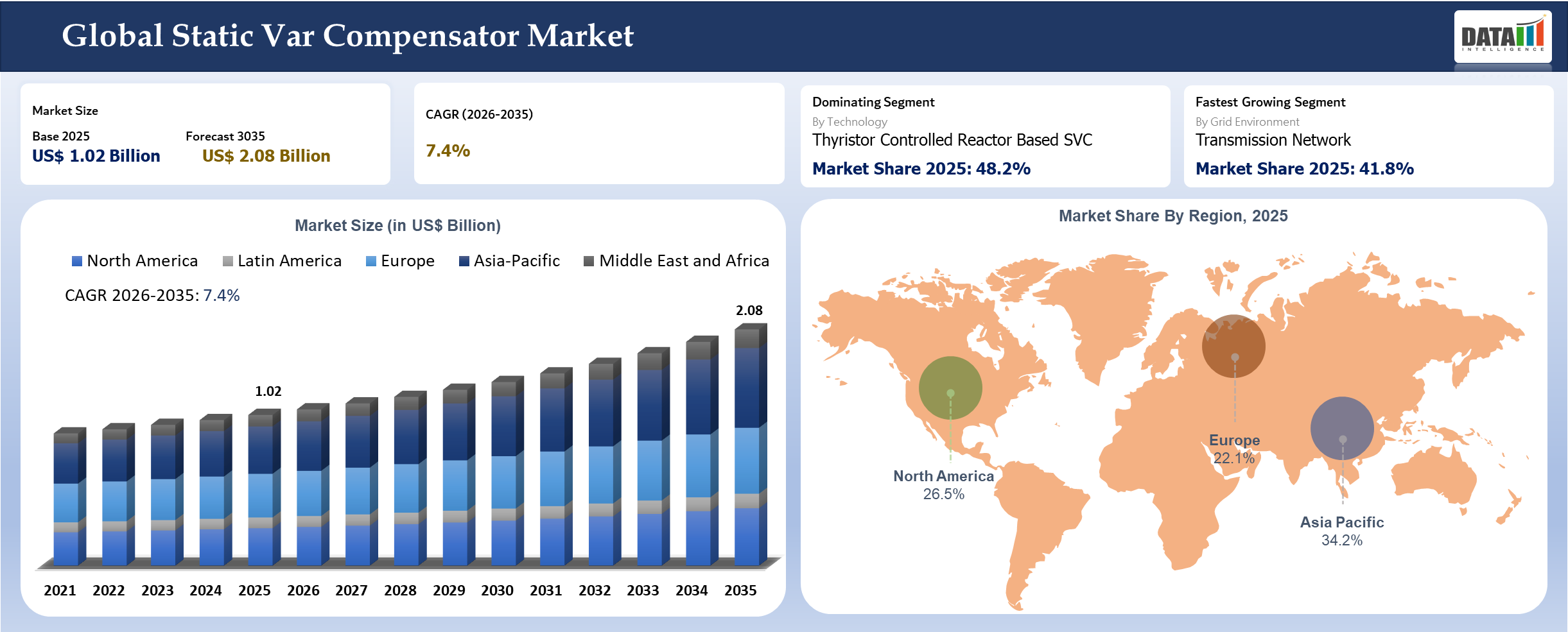

Static Var Compensator Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 1.02 Billion | |

| 2035 Projected Market Size | US$ 2.08 Billion | |

| CAGR (2026-2035) | 7.4% | |

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Technology | Thyristor Controlled Reactor Based SVC, Thyristor Switched Capacitor Based SVC, Hybrid SVC, Utility SVC with Harmonic Filters | |

| By Voltage Class | Medium Voltage, High Voltage, Extra High Voltage | |

| By Grid Environment | Transmission Network, Sub Transmission Network, Industrial Power System, Railway Electrification, Renewable Interconnection Point | |

| By Compensation Need | Voltage Stability Support, Flicker Mitigation, Power Factor Correction, Fault Ride Through Support, Reactive Power Balancing | |

| By Installation Model | Greenfield Grid Project, Brownfield Substation Upgrade, Industrial Process Retrofit | |

| By Region | North America | USA, Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

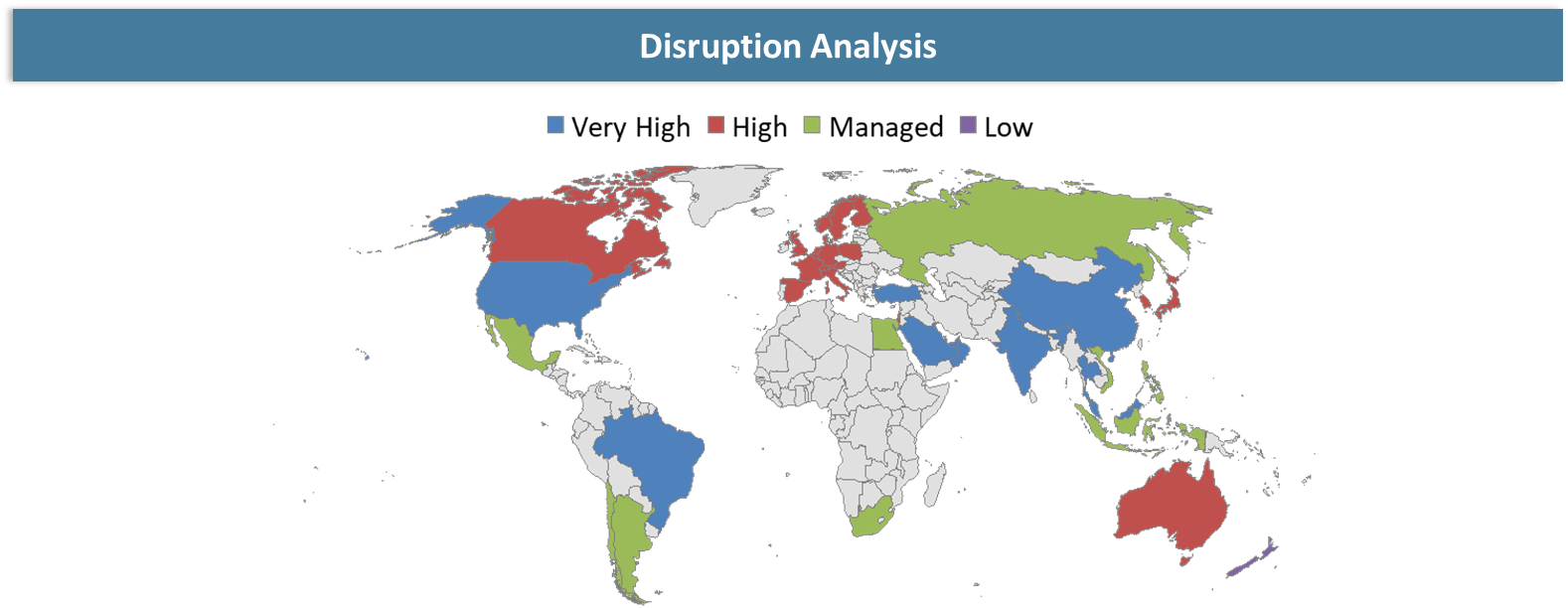

Static Var Compensator Market Disruption Analysis

The disruption relates to SVC having to defend its value proposition more clearly relative to STATCOM and hybrid solutions. Customers are not buying from one FACTS perspective. It considers response time, voltage characteristics, harmonic design, footprint, cost and lifecycle performance among various dynamic compensation solutions. Another disruption involves the changing locus of the creation of compensation value. Traditionally, voltage support on the transmission system was the primary consideration.

Applications include renewable energy interconnection, data center adjacent power quality, electrified railways and industrial activities in weak grids. It expands the market potential but also means more customized sales pitches. Utility buyers seek more compelling rationale and sometimes favor incremental investment strategies. It might benefit SVC manufacturers that integrate their solutions within larger stories about substation enhancement projects or power quality initiatives. In some cases, customers will appreciate digital capabilities that allow SVC providers to prolong the commercial viability of their products in an established product category.

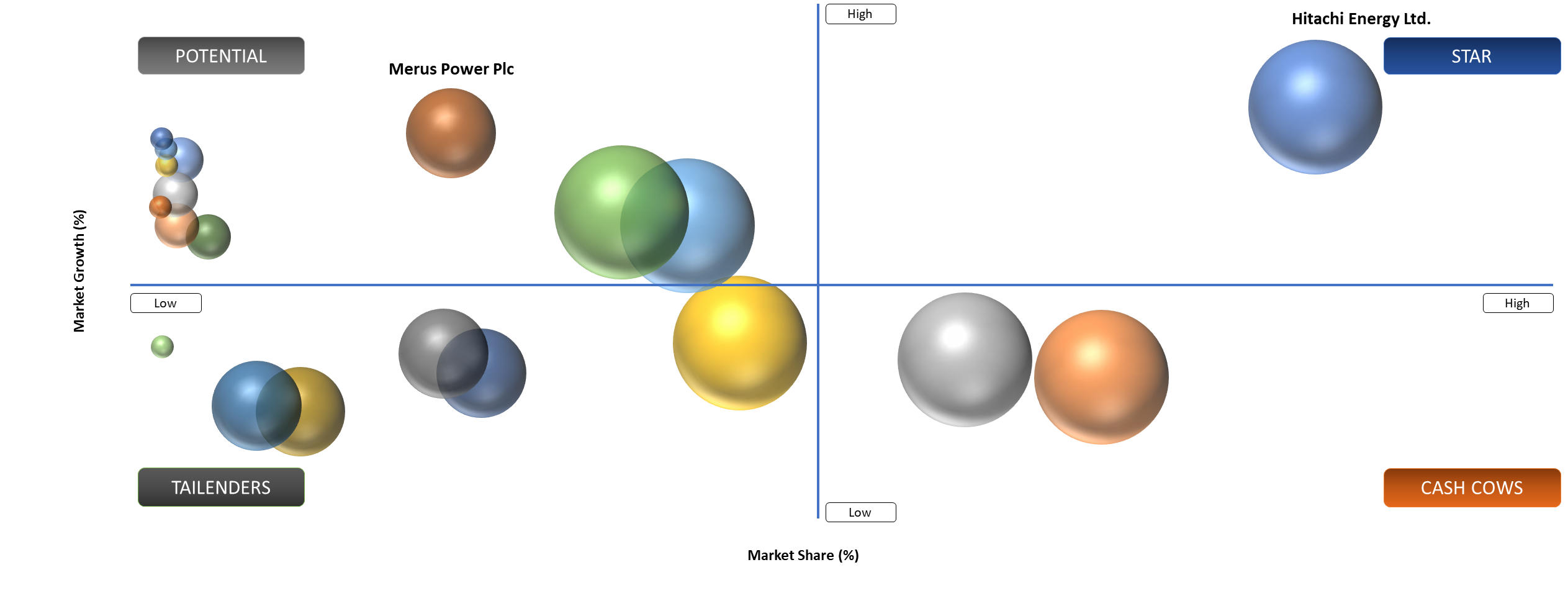

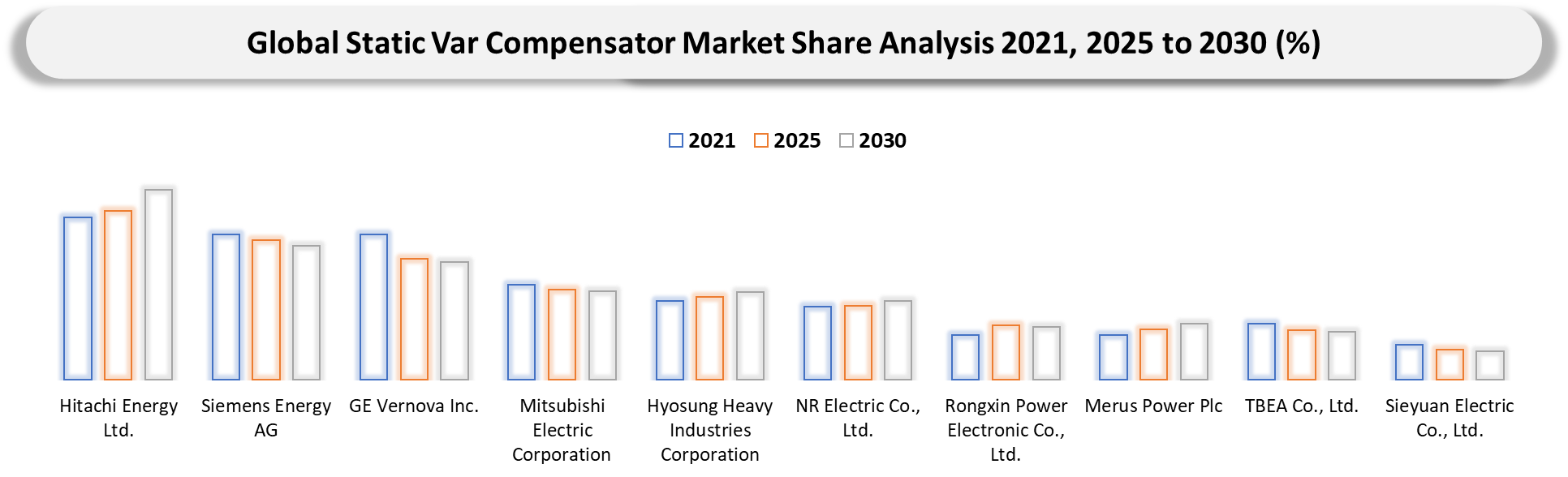

BCG Matrix: Company Evaluation

Hitachi Energy Ltd., Siemens Energy AG and GE Vernova Inc. make up Stars due to their combination of reference bases, utility credentials and technical capacity to locate SVC properly within a greater portfolio context. In other words, what distinguishes these vendors from others is not merely availability but rather the customers' trust in how these products will be integrated into a project and sustained throughout their lifecycle. For Cash Cows vendors, the existing reputation of their power system solutions and solid connections with regional utilities in projects where reliability of delivery is valued by the purchaser is very advantageous. For Question Marks, there is more room to grow in technically driven or cost-conscious projects.

Static Var Compensator Market Market Dynamics

Grid instability from variable generation and weak-network conditions is keeping demand for proven dynamic voltage support intact

Renewable energy production, long-distance transmissions, industrial electrification and off-grid operations provide an environment in which static compensation alone is not adequate and dynamic compensation becomes economically viable. SVC retains its appeal in such circumstances because it is a known entity. Power utilities and their industrial counterparts know its behavior, requirements and application. It becomes important when dealing with substantial projects that cannot accommodate any surprises during installation. It becomes even more important in situations involving substations, railway feeds, mining facilities and industries were poor quality of electricity impacts performance. In such situations, voltage compensation has tangible consequences on productivity, protection and the life of equipment.

Buyers increasingly compare SVC against STATCOM and hybrid alternatives before committing capital

Comparison pressure is perhaps the greatest constraint. SVC is no longer operating in isolation. Buyers increasingly do a better job of making a comparison of what can be achieved by STATCOMs, FACTS and power quality systems with digital technology, particularly where there are rapid voltage changes or space requirements become an issue. Even in instances where SVC still makes economic sense, it can hinder its adoption. It is about more than just demonstrating what SVCs offer.

Static Var Compensator Market Segmentation Analysis

The global static var compensator market is segmented based on technology, voltage class, grid environment, compensation need, installation model and region.

Static VAR Compensators Emerge as Critical Assets for Grid Stability and High-Load Transmission Networks

Utility operators employ SVC for voltage stability control and reactive power management as well as improving reliability in heavily loaded and weak lines. The transmission application is the area of network where network operators require reliable and proven compensators with considerable experience and utility level support. Large utilities will tend towards technologies that have a considerable field history when they are developing new substations. It would be another strength of the SVC application given its ability to incorporate harmonic filtering and grid code requirements in the wider context of station development.

Railway Electrification is significant commercially due to the ability of traction systems to impose unstable reactive loads on networks and to generate observable power quality problems. SVC has an important role to play here in improving network stability and reducing disturbance such as flickers associated with changing traction loads. The segment is significant because, for railway authorities, the question of compensation is not one of technology but of operation, which is whether the system can provide more stable performance against traction variations.

Static Var Compensator Market Geographical Penetration

Asia Pacific Leads Growth in Static Var Compensator Market Amid Grid Modernization and Renewable Expansion

Asia Pacific emerges as the most dynamic SVC market due to its aggressive renewable energy capacity additions, widespread electrification programs and robust transmission networks. In view of this, power companies and grid managers are relying on SVC equipment to ensure stability of voltage levels, minimize losses in power transmission and improve the quality of power. At the same time, governments in the Asia Pacific region have made grid modernization their main priority, whereby China has committed to building UHV grids, while India plans to build Green Energy corridors utilizing FACTS technologies, including SVC technology.

China Static Var Compensator Market Trends

China leads in SVC installation in the Asia-Pacific region owing to its immense power generation and renewable energy capacity. According to National Energy Administration, during the period from 2020 to 2024, the country commissioned more than 300 GW of renewable energy capacity, leading to the need for voltage regulation systems such as SVCs. With China having the most extensive UHV transmission system globally, FACTS technologies play an essential role in ensuring that electricity is transmitted effectively from one point to another across great distances. By 2024, the total power capacity of the country had risen to above 2,900 GW, with much of the capacity needing reactive power control. The state-run energy companies have been installing SVCs and STATCOMs in response to the unstable conditions caused by renewables.

India Static Var Compensator Market Trends

The SVC market in India is experiencing strong growth as a result of a sharp rise in the use of renewable energy sources and large transmission projects. According to the Ministry of New and Renewable Energy, the cumulative capacity of India's renewable energy installations has already exceeded 180 GW (as of 2024), resulting in high requirements for reactive power compensation to ensure stable functioning. The development of new technological solutions under the Green Energy Corridor initiative is aimed at integrating renewable energy sources through the application of SVC technology. Moreover, the Indian transmission system is characterized by more than 470,000 km of circuits, thus requiring voltage control in power delivery. FACTS devices, including SVCs, are being actively introduced into the power grids managed by state-owned companies such as the Power Grid Corporation of India Limited.

Static Var Compensator Market Competitive Landscape

- The rivalry for SVC supply in FACTS is led by grid-technology providers that can position SVCs among other FACTS products and substation equipment. Such companies as Hitachi Energy Ltd., Siemens Energy AG, GE Vernova Inc., Mitsubishi Electric Corporation and Hyosung Heavy Industries Corporation continue to play an important role since customers generally value integrated solutions providers.

- Regional rivalry plays a much bigger role than general talk about global market shares might imply. Chinese and Asian competitors may well be very competitive at home and in neighboring countries, while the Europeans and the Japanese still dominate if utilities favor experience in reference projects and comprehensive product range.

Key Developments of the Static Var Compensator Market

- March 2026: Eaton Corporation plc enhanced grid modernization portfolio with reactive power compensation technologies supporting SVC integration for utilities and industrial customers.

- February 2026: Schneider Electric SE integrated digital grid and automation platforms with SVC-compatible solutions, enabling real-time monitoring and predictive maintenance capabilities.

- February 2026: NR Electric Co., Ltd. strengthened smart grid solutions with advanced reactive power compensation systems, enhancing SVC-based voltage stability in utility networks.

- January 2026: Siemens Energy AG expanded SVC deployments globally to enhance grid stability, supporting renewable integration and improving voltage regulation capabilities.

- January 2026: GE Vernova Inc. increased SVC installations for grid modernization, enhancing reactive power compensation and supporting renewable energy integration projects globally.

- January 2026: CG Power and Industrial Solutions Limited strengthened transmission and distribution portfolio, supporting SVC deployment in grid modernization and industrial power quality applications.

- December 2025: Hitachi Energy Ltd. expanded U.S. grid manufacturing investments exceeding US$ 650 million, strengthening supply of SVC-related high-voltage equipment for renewable integration.

- December 2025: Bharat Heavy Electricals Limited advanced FACTS solutions including SVC systems for Indian grid stability and renewable energy integration projects.

- November 2025: Hyundai Electric & Energy Systems Co., Ltd. expanded power grid equipment manufacturing supporting SVC deployment and high-voltage transmission infrastructure upgrades globally.

Why Choose DataM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

Target Audience

- Transmission Utilities and Grid Operators: Utilities seeking voltage stability, reactive power support and dynamic compensation in heavily loaded or weak-grid corridors.

- Railway Electrification Authorities and Traction Power Teams: Operators managing flicker, voltage fluctuation and reactive imbalance in rail networks with changing traction loads.

- Renewable Interconnection Developers and EPCs: Project teams evaluating compensation needs at wind, solar and hybrid energy connection points where weak-grid behavior can slow commissioning.

- Industrial Power Users: Mining, metals, process-industry and heavy-manufacturing operators needing dynamic power-quality support to protect throughput and equipment stability.

- Substation EPC Contractors and Power System Integrators: Companies responsible for engineering, integrating and commissioning utility-grade compensation assets.

- Utility Asset Managers and Service Teams: Stakeholders comparing refurbishment, replacement and digital-support strategies for long-life reactive power assets.

- Regulators and Grid-Planning Institutions: Policy and planning stakeholders assessing how dynamic compensation supports reliability, renewable integration and network reinforcement.

- Infrastructure Investors and Strategic Industrial Buyers: Capital providers tracking how grid-stability and power-quality investments shape utility and industrial modernization.