Preparing for the Quantum Computing Acceleration

Quantum computing is moving from a distant research topic into a strategic planning issue for enterprises, governments, hyperscalers and advanced industry buyers. Bain’s 2026 analysis argues that quantum systems could begin outperforming classical systems on selected complex problems by 2029, while enterprise capabilities can take three to four years to build. That timing creates a practical problem for leadership teams. Companies that wait for fault tolerant hardware to become fully mature may discover that the skills, use cases, data structures and operating models required for value capture are already several years behind the market.

The opportunity is concentrated rather than universal. Quantum computing will matter most where the business problem involves complex optimization, simulation or cryptography. Healthcare, financial services, logistics, energy, aerospace and advanced manufacturing are likely to see the earliest commercial pressure because these sectors already depend on high complexity modeling and faster decision systems. The market is therefore entering a preparation window where readiness matters more than hardware ownership.

For detailed sizing, segmentation and enterprise adoption trends, see DataM Intelligence’s Quantum Computing Market Report

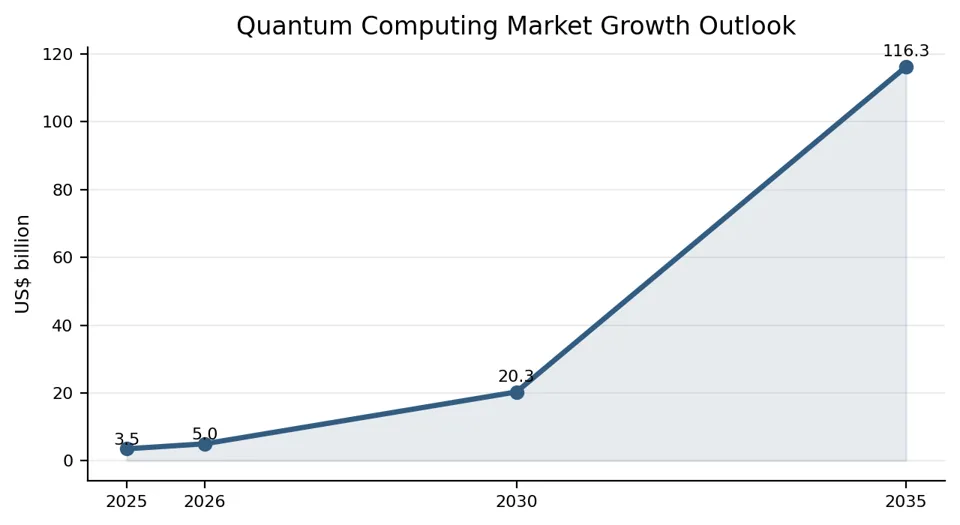

Chart 1. Quantum computing is shifting from early adoption toward a high growth commercial market through 2035.

Quantum Is Becoming a Competitive Readiness Question

The most important shift in 2026 is that quantum computing is no longer only a hardware race. It is becoming a readiness race. Companies need to identify where quantum could create a measurable advantage, design pilots around those problems and build technical fluency before the technology stabilizes. This is different from many generative AI deployments, where companies could start with productivity tools and scale use cases quickly. Quantum requires deeper mathematical framing, specialized talent and integration with high performance computing or cloud based access models.

Bain highlights that use cases can take six to nine months to develop from problem framing to algorithm tuning and impact assessment. That matters because the first wave of commercial advantage may arrive before many companies have finished building internal capability. The companies most exposed are those with complex optimization or simulation problems, because quantum could eventually change how they model risk, discover molecules, design materials and optimize networks.

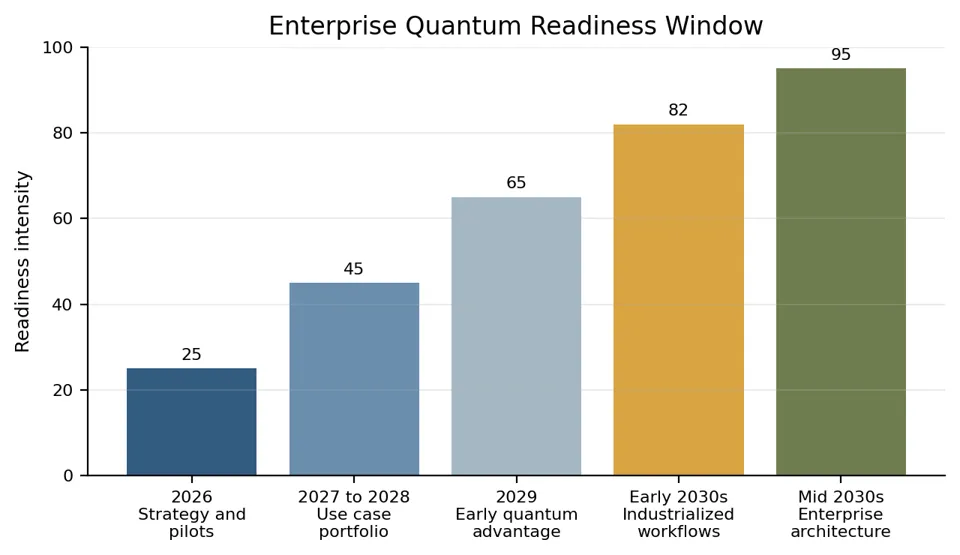

Chart 2. The enterprise preparation window is opening before quantum advantage becomes more visible around the end of the decade.

Why the First Advantage Will Come From Specific Use Cases

Quantum computing should be viewed as a specialized accelerator for a defined set of problems. It will not replace classical computing across enterprise technology stacks. Its early value will likely come from areas where classical systems struggle with vast combinations or highly complex simulations. That includes molecule discovery in healthcare and pharmaceuticals, portfolio risk modeling in financial services, route optimization in logistics and battery chemistry modeling in energy.

This use case discipline is important because the market is still early. Many quantum pilots will not translate into near term economic value. The better strategy is to start with business problems where the value of improved computation is clear. A pharmaceutical company may focus on molecular simulation. A bank may focus on risk models and optimization. A logistics operator may focus on routing and capacity planning. An energy company may focus on grid optimization or materials discovery.

For industry specific use cases in banking, risk modeling and quantum safe finance, see DataM Intelligence’s Quantum Computing in Financial Services Market Report

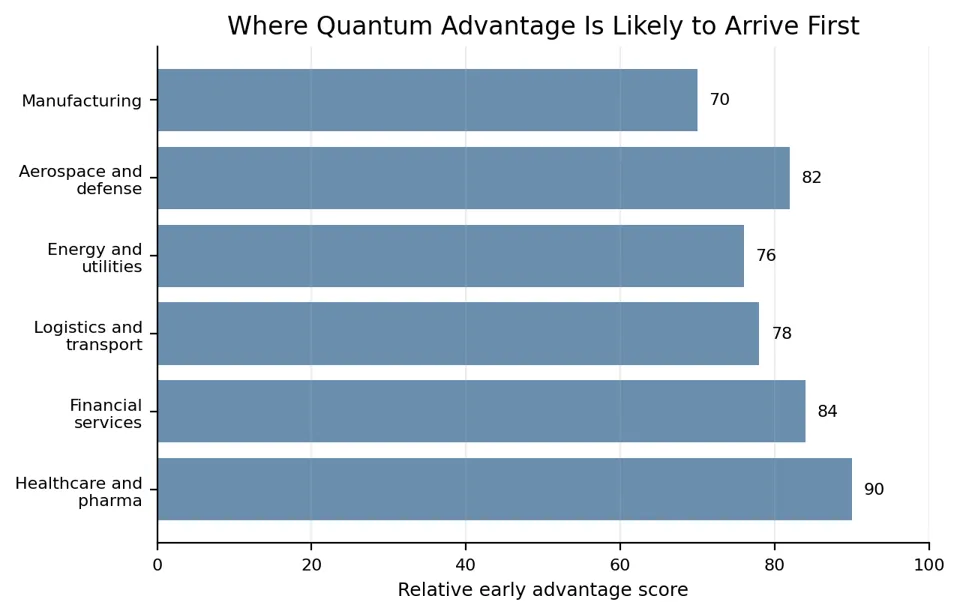

Chart 3. Early quantum advantage is expected to concentrate in sectors with simulation, optimization and cryptography heavy problems.

Hardware Progress Is Accelerating, but Cloud Access Will Shape Adoption

Quantum hardware is improving across superconducting qubits, trapped ions, neutral atoms, photonic systems and silicon spin approaches. Bain notes that progress in error correction and device engineering is moving the industry toward systems with usable logical qubits by the end of this decade. DataM Intelligence estimates the global quantum hardware market reached US$ 2.29 billion in 2025 and could reach US$ 33.31 billion by 2035, supported by government funding, hyperscaler investment and enterprise experimentation.

Most enterprises will not own quantum hardware in the early adoption phase. They will access quantum resources through cloud platforms and hybrid quantum classical architectures. This lowers the adoption barrier because companies can test algorithms without building specialized infrastructure. It also shifts competition toward software, APIs, algorithm libraries and partner ecosystems. The most practical question for many enterprises is therefore which provider relationships and cloud access models should be developed before quantum workloads become commercially relevant.

For hardware technology trends, qubit platforms and procurement priorities, see DataM Intelligence’s Quantum Hardware Market Report

Cybersecurity Is the Most Immediate Quantum Risk

Even before broad quantum advantage arrives, cybersecurity risk is already becoming more urgent. The central issue is the possibility that encrypted data captured today could be decrypted later when quantum systems become powerful enough. This threat is especially important for banks, defense agencies, healthcare companies, telecom operators and any organization that stores long life sensitive data.

The immediate action is post quantum cryptography readiness. Enterprises need to inventory cryptographic assets, understand where vulnerable algorithms are used and build crypto agility so systems can migrate to quantum resistant standards. This work can take years because encryption is embedded across applications, identity systems, certificates, hardware devices and third party platforms. For many companies, quantum cybersecurity will become the first serious budget line before quantum computing creates direct business advantage.

For quantum safe security, quantum key distribution and post quantum encryption demand, see DataM Intelligence’s Quantum Cryptography Market Report

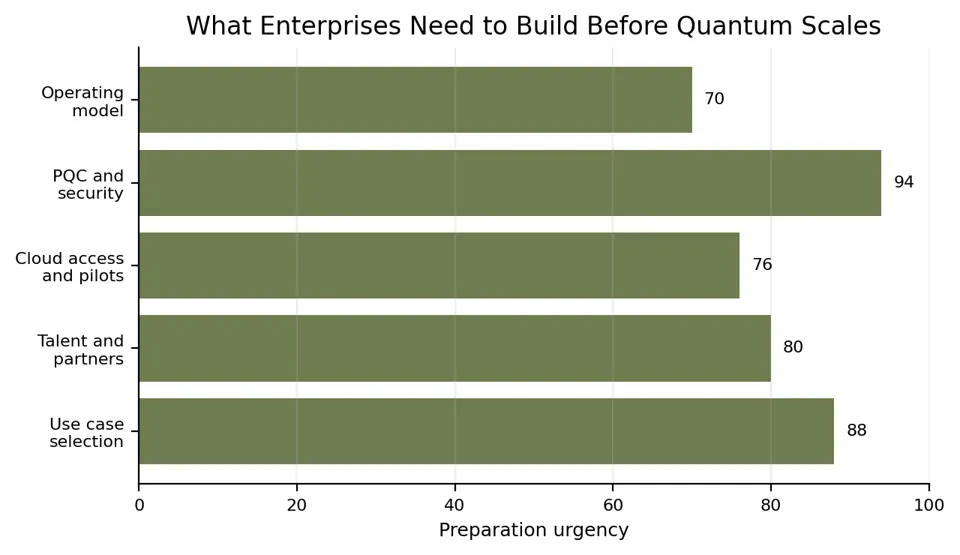

Chart 4. Enterprise readiness depends on use cases, talent, cloud access, post quantum security and operating model design.

The Semiconductor and Sensor Ecosystem Will Benefit Before Broad Enterprise Adoption

One of the strongest near term opportunities may sit in the supplier ecosystem rather than the end user market. Quantum chips, cryogenic systems, photonics, control electronics, advanced materials and quantum sensors are all becoming strategic investment areas. DataM Intelligence estimates the quantum chip market could expand from US$ 0.22 billion in 2025 to around US$ 3.0 billion by 2033, while quantum sensors are also moving from pilot deployments toward structured procurement in defense, navigation, healthcare and industrial applications.

For sensing, defense and precision measurement demand, see DataM Intelligence’s Quantum Sensors Market Report

This matters because the quantum acceleration will create demand across multiple layers of the technology stack. Hardware makers will compete on logical qubit quality, error correction and scalability. Cloud providers will compete on access and orchestration. Software companies will compete on tools that allow enterprises to translate business problems into quantum ready algorithms. Defense and aerospace users will accelerate quantum sensing, navigation and secure communications even before enterprise computing use cases scale widely.

For semiconductor level opportunity, see DataM Intelligence’s Quantum Chip Market Report

The Best Strategy Is to Prepare Without Overcommitting

The right enterprise response is balanced. Companies should avoid treating quantum as a near term transformation program across the full business. They should also avoid ignoring it until hardware is fully mature. The highest value approach is to define a strategic posture, identify high value use cases, create a small capability center and build partnerships with cloud quantum providers, universities and specialist vendors.

The first wave of pilots should be narrow and measurable. Companies should focus on problems where improved computation has a clear commercial link, such as cost reduction, faster research, better risk modeling or improved network performance. The goal is to build organizational learning and identify where quantum can complement existing analytics and AI systems. By 2029, companies with real pilots, trained teams and a clear use case roadmap will be better positioned to industrialize what works.

Quantum Advantage Will Reward Companies That Start Building Capability Now

The quantum computing market is entering a critical preparation phase. Hardware progress is accelerating, cloud access is lowering experimentation barriers and cybersecurity urgency is increasing. The technology will not create value for every enterprise at the same time, but the companies operating in simulation heavy, optimization heavy and security sensitive sectors have a clear reason to act before the market reaches broader commercial maturity.

The next few years will separate companies that understand quantum as a practical capability from those that treat it as a distant research theme. The winners will not simply be the organizations that buy access to the most advanced machines. They will be the companies that know which problems quantum should solve, how to connect those problems to business value and how to integrate quantum into analytics, AI and high performance computing workflows.