The Next Aircraft Materials Cycle

How Lightweighting and Thermal Performance Are Driving Innovation

Aircraft material selection is entering a new cycle as airlines, aircraft OEMs, engine suppliers and defense programs pursue lighter structures, hotter engines, and more durable components. The shift is being driven by fleet renewal, fuel efficiency pressure, emissions rules, engine thermal loads, defense modernization and the need to reduce dependence on fragile metal supply chains. The most important innovation areas are advanced composites, titanium alloys, aluminum lithium alloys, ceramic matrix composites, high temperature polymers and thermal barrier coatings.

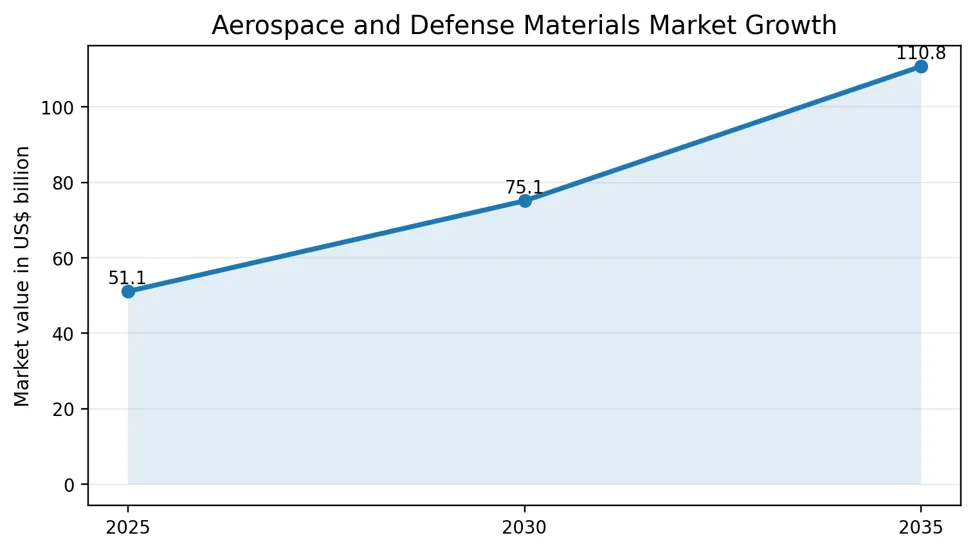

Chart 1. DataM Intelligence estimates the aerospace and defense materials market at US$ 51.10 billion in 2025, reaching US$ 110.75 billion by 2035.

Fleet Renewal Is Turning Materials Into a Strategic Lever

The next aircraft cycle is being shaped by a simple operating reality. Airlines need aircraft that burn less fuel, fly longer routes with better economics and meet stricter environmental expectations. Airbus projects demand for 42,060 new aircraft from 2026 to 2045, while Boeing expects strong demand for replacement aircraft because older jets are less efficient and supply is expected to remain tight for much of this decade.

This matters for materials because the fuel efficiency question cannot be solved only through aerodynamics or new engines. Weight reduction across the fuselage, wings, cabin structures, nacelles and fasteners is now part of every aircraft platform decision. Carbon fiber composites, advanced aluminum alloys, titanium and thermoplastic composites are becoming design choices that influence range, payload, maintenance and lifecycle emissions.

For a deeper view of structural, thermal and defense material demand, review the DataM Intelligence report on Aerospace and Defense Materials Market.

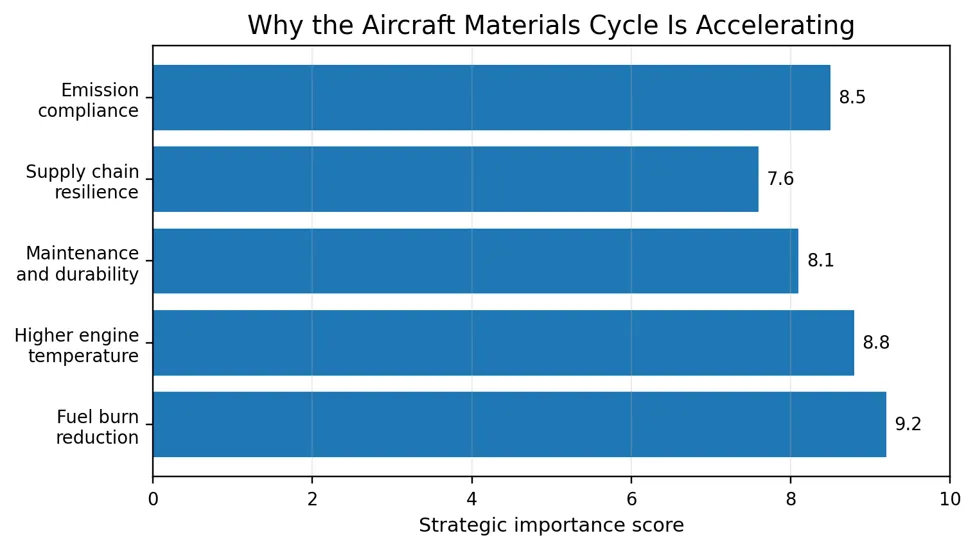

Chart 2. Fuel burn, high-temperature performance, and emission compliance are now the strongest commercial drivers for aircraft material innovation.

Lightweighting Is Moving From Airframes to Smaller Certified Components

Large composite airframes are already proven in modern widebody aircraft, but the next wave of lightweighting is moving into smaller aircraft components where production scale and certification have historically slowed adoption. Wing ribs, brackets, clips, potted inserts, cabin panels, structural inserts and nacelle components are becoming important opportunities for automated composite manufacturing and thermoplastic composite processing.

The commercial logic is strong. Every kilogram removed from an aircraft can improve fuel burn and operating economics across thousands of flight cycles. The supplier opportunity is shifting from material supply alone to process repeatability, quality assurance, traceability and repair readiness. This creates space for carbon fiber suppliers, resin formulators, thermoplastic composite processors and automated fiber placement technology providers.

This is why the DataM Intelligence Advanced Composites Market report is directly linked to the aircraft materials cycle. The market is estimated at US$ 47.10 billion in 2025 and is forecast to reach US$ 105.60 billion by 2033.

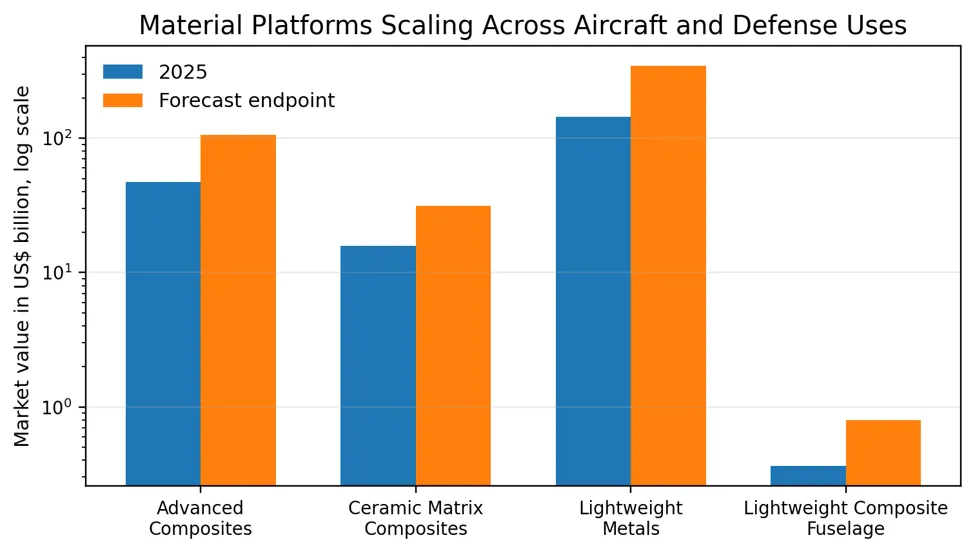

Chart 3. Advanced composites, ceramic matrix composites, and lightweight metals are expanding as aircraft design shifts toward stronger, lighter, and more thermally capable materials.

Thermal Performance Is Becoming the Engine Innovation Bottleneck

The second major driver is thermal performance. Engine manufacturers want hotter cores because higher operating temperatures can improve thermal efficiency. This creates demand for materials that can survive extreme heat, oxidation, stress and vibration inside propulsion systems. Nickel based superalloys remain essential, but ceramic matrix composites and advanced coatings are gaining strategic importance because they can enable hotter operating environments with lower weight.

Ceramic matrix composites are especially important for turbine shrouds, combustor liners, nozzles and hot section components. Oak Ridge National Laboratory notes that CMCs can withstand temperatures 300 to 400 degrees Fahrenheit hotter than metal alloys, which supports more efficient combustion and lower emissions. NASA research on next generation engine cores also points to higher energy density and higher thermal loads, increasing the importance of SiC based CMC systems and environmental barrier coatings.

For engine, thermal and aircraft electronics applications, the most relevant related DataM Intelligence report is Aerospace Advanced Ceramics Market, which covers alumina, zirconia, silicon carbide, silicon nitride and other high performance ceramic materials for aircraft applications.

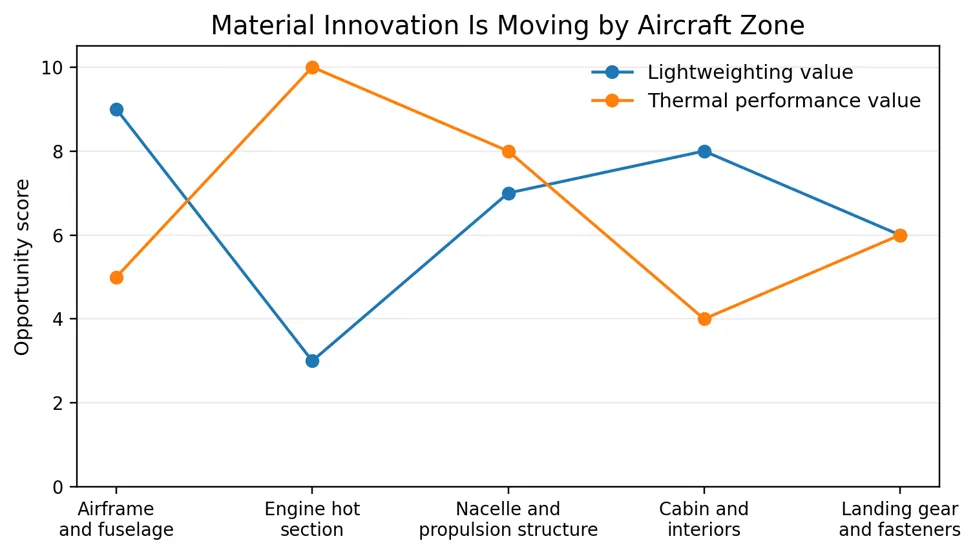

Chart 4. Lightweighting dominates structural areas, while thermal performance is strongest in engine hot sections and propulsion systems.

Titanium and Lightweight Metals Remain Critical Despite Composite Growth

The rise of composites does not remove the importance of lightweight metals. Titanium remains critical for landing gear, engine parts, fasteners, structural components and areas that require high strength with corrosion resistance. Aluminum lithium alloys also remain important for airframes because they offer weight reduction with established manufacturing pathways and certification familiarity.

Supply security is becoming more important because aircraft OEMs and defense programs cannot easily substitute certified materials once a platform is approved. Titanium sponge, forged titanium parts, specialty alloys and aerospace aluminum all carry qualification requirements that make long term supplier relationships more valuable. Buyers are therefore looking for materials partners with stable capacity, quality systems and regional supply resilience.

DataM Intelligence covers this metals opportunity through the Titanium Market and the Lightweight Metals Market, both of which connect directly to aerospace, defense and high strength lightweight component demand.

Thermoplastics Are Changing the Manufacturing Equation

Thermoplastic composites are emerging as one of the most practical material opportunities because they can support faster processing, welding, recycling potential and higher production repeatability than many traditional thermoset composite routes. Their relevance is rising as aircraft manufacturers try to reduce build times while maintaining strict quality and certification standards.

The near term opportunity is strongest in parts that need repeatability, damage tolerance and faster cycle times. Wing ribs, clips, brackets, access panels and interior structures are likely to see growing interest. The long term opportunity is broader because thermoplastic materials can help aerospace manufacturers align lightweighting with circularity and lower lifecycle waste.

For aircraft structure specific demand, DataM Intelligence’s Lightweight Composite Fuselage Market provides a focused view of how composite fuselage demand is linked to automation, regional aircraft manufacturing and next generation aircraft design.

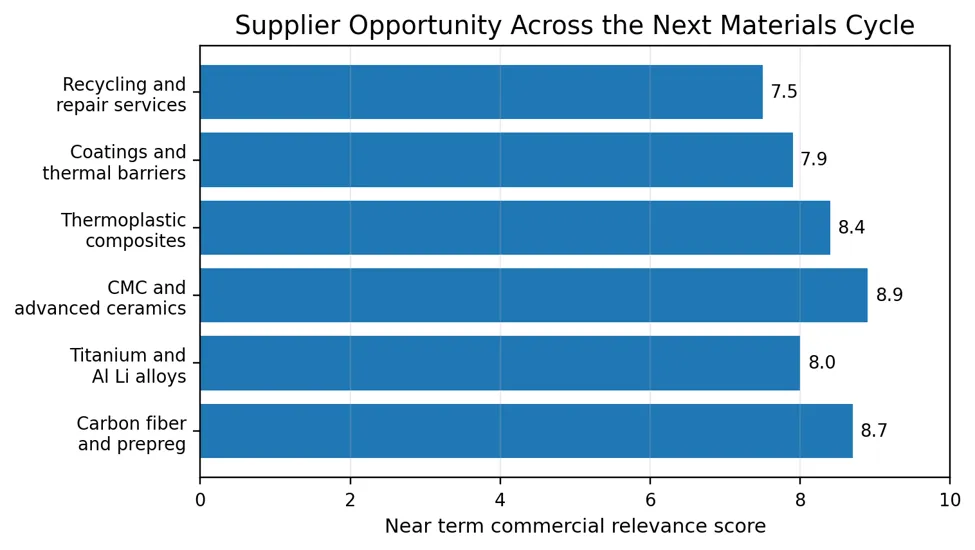

Chart 5. Supplier opportunity is strongest where lightweighting, thermal resistance, process repeatability and certification readiness converge.

Who Benefits From the Next Aircraft Materials Cycle

The first beneficiaries are advanced composite suppliers that can deliver carbon fiber, prepreg, resin systems and automated processing support at aerospace quality levels. Their opportunity is tied to structural lightweighting and the growing use of composite parts across commercial aircraft, defense aircraft, drones and space systems.

The second group is high temperature material suppliers serving engines and propulsion systems. Ceramic matrix composite producers, thermal barrier coating specialists, silicon carbide material suppliers and advanced ceramics companies are positioned to benefit as engines require higher heat tolerance and improved durability.

The third group is specialty metal suppliers focused on titanium, aluminum lithium alloys and high strength aerospace alloys. These companies benefit from platform qualification, long program lifecycles and limited substitution once materials are approved. The fourth group is manufacturing technology providers that help automate composite layup, inspection, repair and joining.

Investment Implications for Aerospace Suppliers

The highest value opportunities are likely to sit at the point where material science meets certified production. Aerospace buyers do not only need lighter materials. They need materials that can be qualified, manufactured repeatedly, repaired efficiently and sourced reliably across long program timelines. That makes process control, nondestructive inspection, traceability and supplier qualification as important as the chemistry of the material itself.

Near term investment opportunities are strongest in carbon fiber capacity, aerospace grade thermoplastic composite processing, CMC components, thermal barrier coatings, titanium forging capacity, aluminum lithium alloy supply and composite repair services. Over the next decade, the winning suppliers will be those that combine material performance with production scale and certification readiness.