Lightweight Metals Market Overview

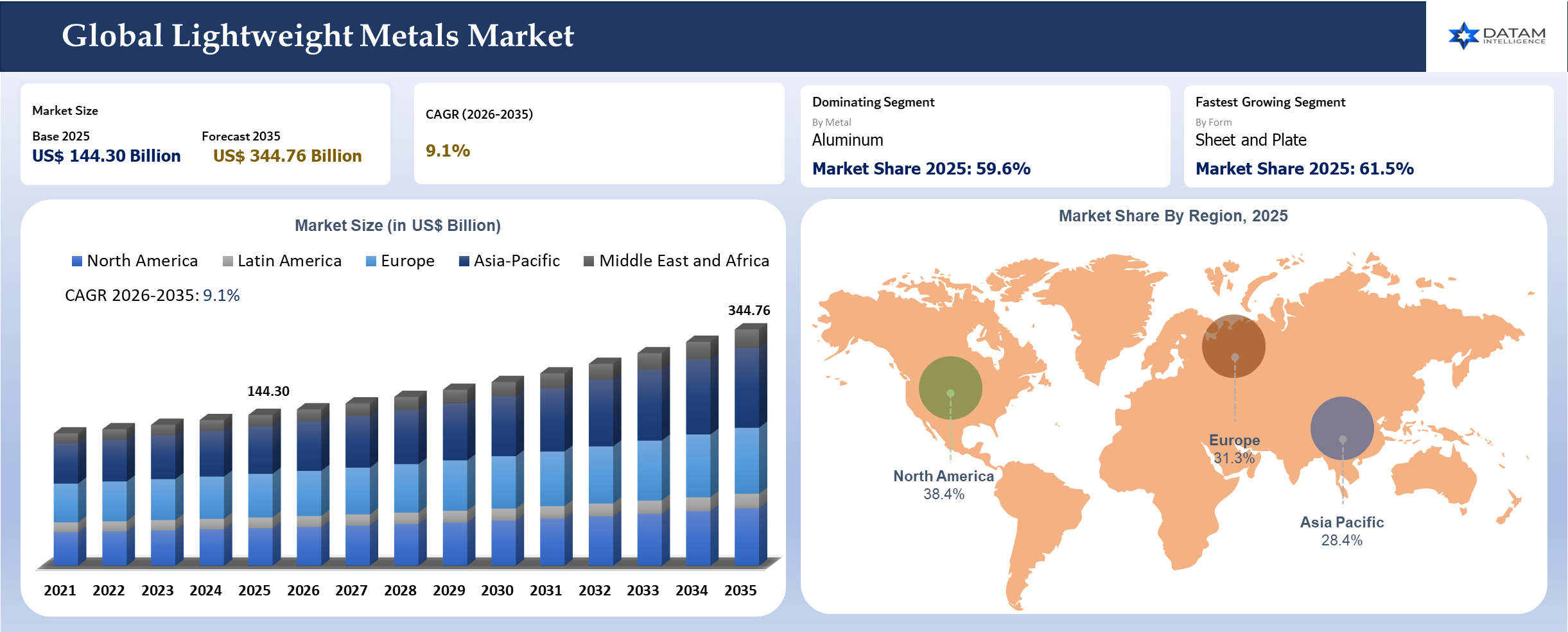

The global lightweight metals market reached US$ 144.30 billion in 2025 and is expected to reach US$ 344.76 billion by 2035, growing with a CAGR of 9.1% during the forecast period 2026-2035. Commercial decisions are now more about performance under particular operating circumstances, as well as the procurement process and problem-solving capacity of the supplier in practical terms. It means that there’s more to buying than just getting a product from a category. It’s all about selecting a configuration, chemistry, platform or service that is suitable for the demands of the situation at hand. Light metals are not only influenced by the broad growth of demand

The market structure is becoming more selective rather than more generic. End users are narrowing supplier lists around those players that can prove value in the exact part of the value chain where commercial pressure is highest. In some projects, that means stronger process control; in others, it means easier retrofitability, better traceability, lower downtime risk or the ability to comply with more demanding customer or regulatory standards. The result is a market where simple capacity claims matter less than commercial fit.

The revenue generation in this market will be influenced by the high specification intensity regions and those with lower risks associated with the cost of poor performance. It will reward suppliers for mitigating external risks, including the complexity of commissioning, variability in application, deterioration in quality, lack of field service or poor integration with adjacent systems. It creates an advantage for firms with both product excellence and technical support, application expertise and commercial integrity.

Further, there is a growing focus on buyer preference for future adaptability. It is not determined by production efficiencies or installation expenses but depends on whether the chosen system can accommodate future demands concerning stringent specifications, updated formulas, heavier payloads, electronic monitoring or faster commercialization.

Lightweight Metals Industry Trends and Strategic Insights

- The lightweight metals market is becoming more specification-driven, with buyers rewarding solutions that reduce operational risk rather than simply lowering purchase price.

- Value concentration is strongest in technically demanding or premium-use pockets where performance, consistency and support matter more than scale alone.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 144.30 Billion | |

| 2035 Projected Market Size | US$ 344.76 Billion | |

| CAGR (2026-2035) | 9.1% | |

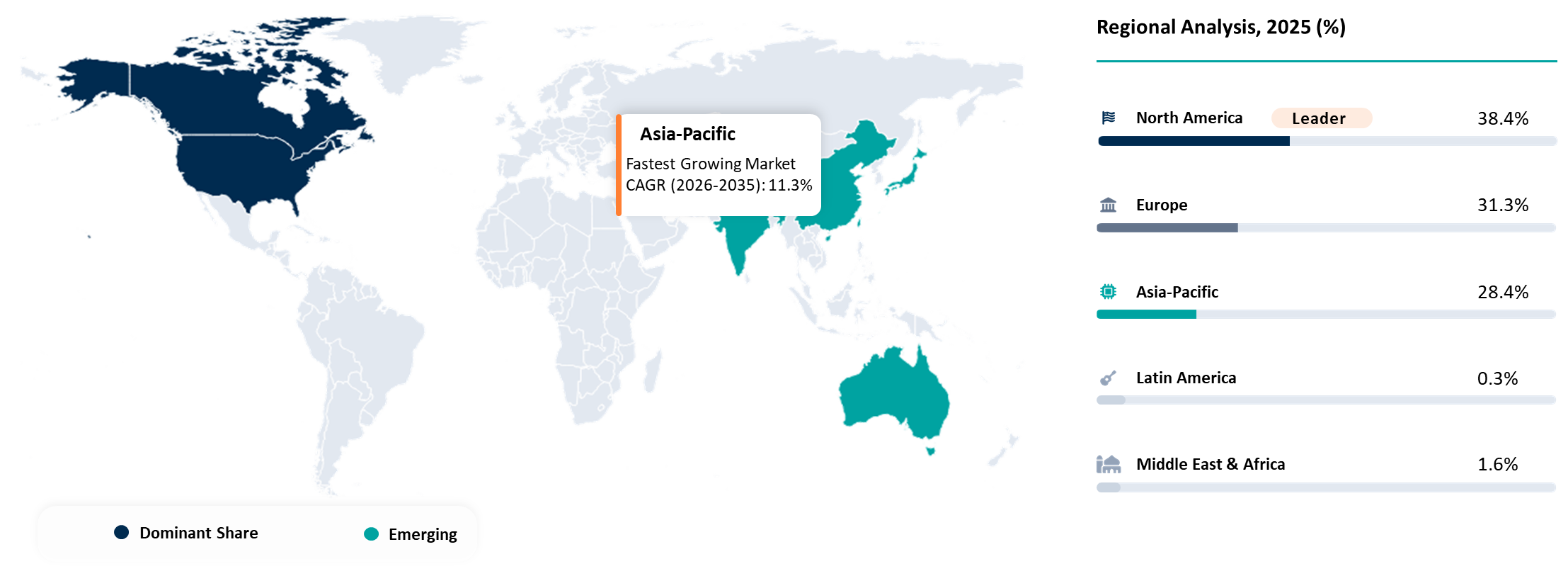

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Metal | Aluminum, Magnesium, Titanium, Beryllium, Aluminum-Lithium Alloys and Other Lightweight Metal Alloys | |

| By Form | Sheet and Plate, Bars and Rods, Billets and Ingots, Extrusions, Castings, Forgings, Foils, Powders, Wires and Tubes and Others | |

| By Manufacturing Process | Extrusion, Rolling, Casting, Forging, Machining, Powder Metallurgy, Additive Manufacturing, Joining and Welding and Others | |

| By Distribution Channel | Direct Sales, Distributors and Metal Service Centers, OEM Contracts and Online and Digital Procurement Platforms | |

| By Application | Body Structures, Chassis and Suspension, Engine and Powertrain Components, EV Battery Enclosures, Aircraft Frames and Fuselage Components, Landing Gear and Engine Components, Medical Implants and Surgical Devices, Consumer Electronics Housings, Industrial Equipment Components, Packaging and Foils, Building and Construction Profiles and Others | |

| By End-User | Automotive and EV, Aerospace and Defense, Consumer Electronics, Medical and Healthcare, Building and Construction, Packaging, Marine, Industrial Machinery, Energy and Power and Others | |

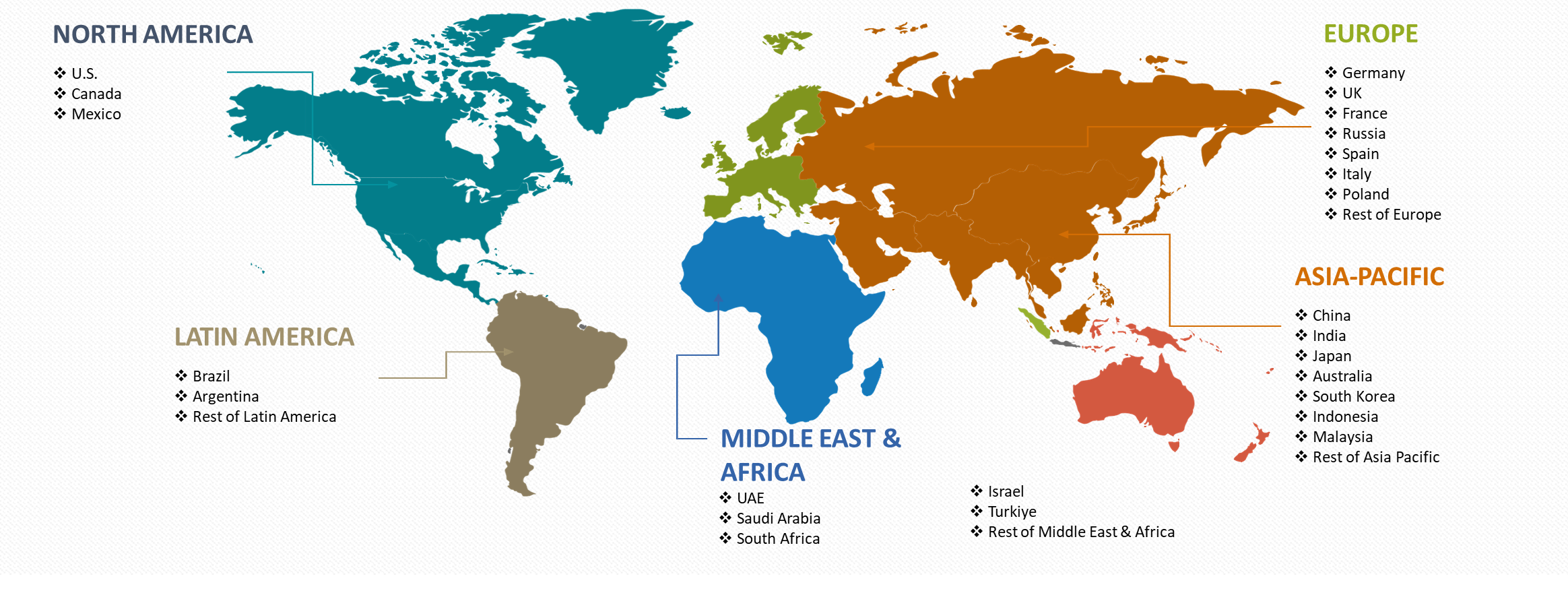

| By Region | North America | USA, Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

AI Impact

AI is beginning to influence the lightweight metals market less as a marketing label and more as a practical decision layer. The real value sits in pattern recognition, optimization and earlier visibility into process drift, maintenance risk or demand changes that traditional supervision misses. Where buyers are managing high-throughput lines, tight tolerance windows or high-value assets, these capabilities are becoming commercially relevant because they reduce hidden losses before they become visible failures.

A second impact comes from predictive planning. AI-enabled analytics can help operators identify where conditions are moving away from validated performance ranges, where maintenance should be prioritized and where recipe, load or usage patterns are likely to create downstream instability. The matters because many markets in this field are not constrained only by product demand; they are constrained by execution quality, labor availability and the speed with which teams can respond to abnormal conditions.

AI also changes commercial positioning. Suppliers that can combine equipment, materials or ingredients with better data visibility gain stronger access to premium projects and multi-year service relationships. Buyers increasingly see digital insight as part of the delivered value, particularly when it can improve uptime, reduce waste, protect quality or support auditable compliance.

Our analysis indicates that the strongest AI opportunities are not universal across every subsegment. They are concentrated where decision cycles are repetitive and data-rich, such as predictive maintenance, quality control, route optimization, process tuning, visual inspection or demand matching. In those areas, AI can shorten response times and create a measurable return rather than simply adding another software layer.

Disruption Analysis

The biggest disruption in the lightweight metals market is the shift from product-led competition to solution-led competition. Suppliers can no longer rely on broad category relevance alone. Buyers want a clearer connection between product choice and specific commercial outcomes such as lower waste, better consistency, easier retrofit, higher uptime, stronger traceability or less exposure to volatile inputs. The changes how suppliers design portfolios and how they sell.

The technical, operations, sustainability and financial executives jointly specify requirements for products within various industries. It means that suppliers have to justify themselves on different grounds. It is not enough to demonstrate superior performance under laboratory conditions anymore when a product does harm to customer service, implementation and the general costs and sustainability agenda.

A channel-level disruption is also underway. Digital discovery, direct specification influence and stronger service expectations are changing where value sits in the chain. In many markets, the highest-margin opportunities are moving away from one-time sales and toward optimization services, modernization programs, custom formulations or application-engineering support. Our analysis indicates that disruption will favor companies that understand where the market is becoming more technical and where it is becoming more service-led. Players that remain too dependent on generic volume strategies risk margin erosion as buyers become more selective and more data-driven.

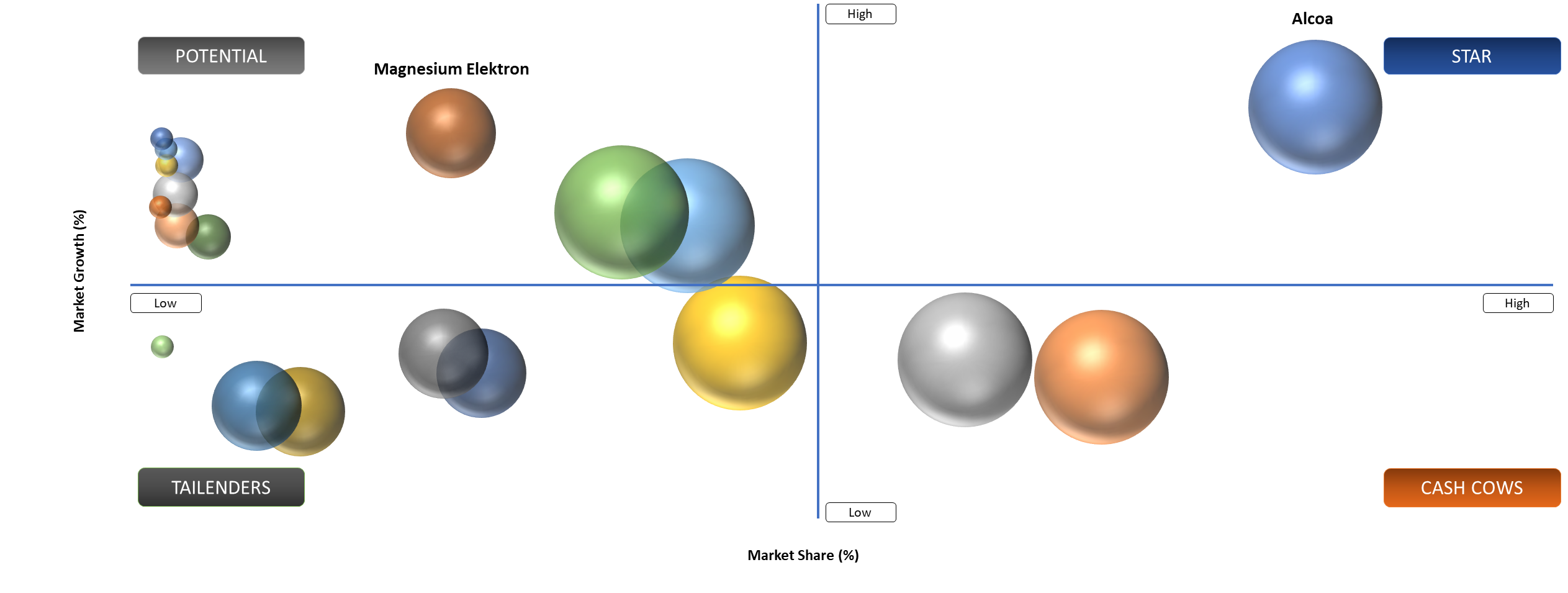

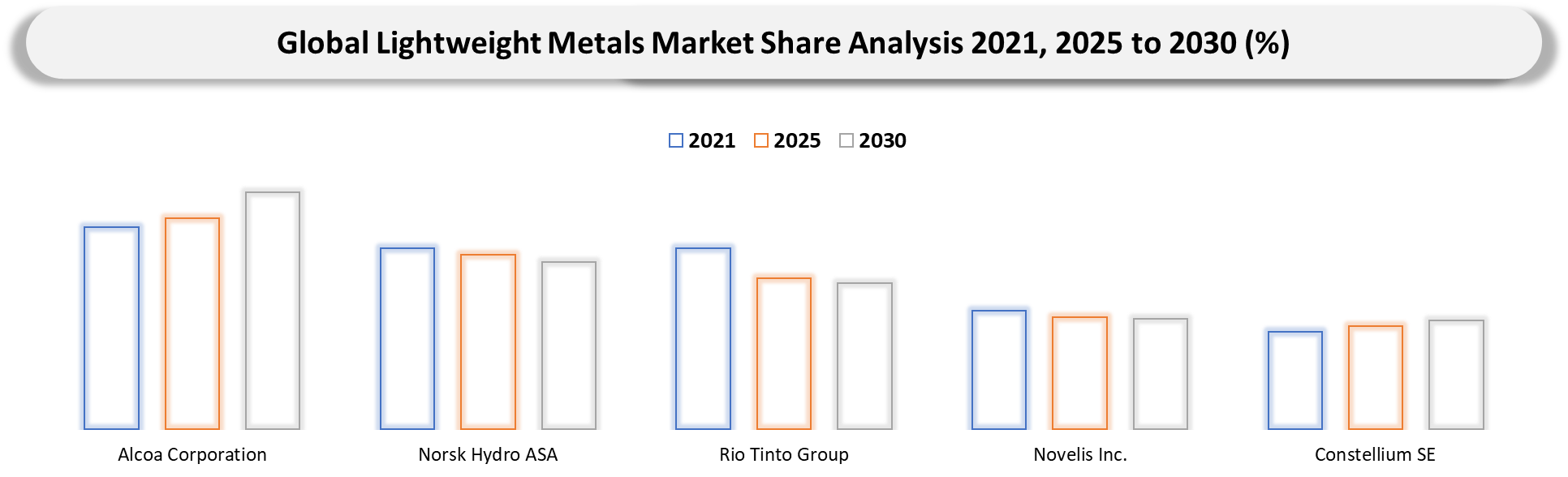

BCG Matrix: Company Evaluation

Alcoa and Norsk Hydro fall into Stars since they have great involvement in aluminum and aluminum happens to be the top-revenue earner in the category of lightweight metals. Alcoa has well-integrated alumina and aluminum businesses with significant application in automotive, aerospace, packaging and industrial industries. On the other hand, Norsk Hydro's competence lies in areas such as extrusions, recycling and low-carbon aluminum that help build EVs, construction and transportation lightweight materials.

Magnesium Elektron and VSMPO-AVISMA belong to Potential since they are linked with high-value but narrow applications of lightweight metals. Magnesium Elektron's business is based on magnesium alloy products that find applications in the manufacture of EVs, electronics and aerospace. However, this company faces challenges in gaining widespread acceptance due to corrosion and difficulties involved in processing. VSMPO-AVISMA, however, has good titanium exposure in aerospace, military and medical industry applications.

Market Dynamics

EV Light weighting, Aerospace Demand and Industrial Efficiency Are Strengthening the Commercial Case for Lightweight Metals

Due to the pressure on manufacturers to make their products lighter while maintaining high strength levels and not affecting safety or longevity, there is a growing demand for lightweight metals. Auto and EV makers are resorting to aluminum, magnesium and other lightweight alloys as they help offset battery weight and enhance energy efficiency. On the other hand, aerospace firms continue to use aluminum and titanium because the aircraft industry places a premium on strength-to-weight ratio, fatigue endurance, corrosion resistance and performance.

Metals that can reduce fuel consumption, increase load capacity, enhance equipment performance and contribute towards developing a higher performing design are becoming highly sought after. No longer do firms involved in making vehicles, planes, trains, ships, medical devices and consumer electronics consider lightweight metals solely as raw material inputs.

Recyclability is also increasing the attractiveness of aluminum and other lightweight metals. Already a long-standing infrastructure supporting the recycling of aluminum is there. The material appeals to procurement organizations aiming at sustainable and low-carbon supply chains and material management. As more and more procurers look for materials that enable them to reach their objectives regarding both performance and sustainability, the competitive advantage of lightweight metals with robust economics will grow, especially compared to heavier materials and non-circular materials.

Other growth factors include new applications in areas such as construction, packaging, consumer electronics and machinery and equipment. Building facades, beverage cans, electronic housing, implant devices, light machinery and fabricated parts offer significant markets. Growth does not rest upon a single market segment but is spread across various end uses with differing uptake dynamics and pricing considerations.

High Material Cost, Processing Complexity and Qualification Barriers Limit Faster Adoption

Many lightweight metals are inherently more costly than standard steels and commodities due to their higher raw materials or processing prices. Both titanium and magnesium are particularly sensitive to cost, qualification difficulties and availability issues. While titanium is a great performer, it is very expensive and difficult to qualify, thus being utilized in aerospace, defense, medical and unique industrial applications.

On the other hand, there are corrosion prevention, safety in processing, difficulty with casting and the requirement of special design knowledge related to the adoption of magnesium alloys. The consumers know about the benefits, yet they can be reluctant to switch over since changes in tooling, joining techniques, surface treatments and testing methods will have to be made at the manufacturing facility.

A significant hindrance is associated with lengthy qualification processes in aerospace, defense, automotive and medical industries. Original Equipment Manufacturers demand certain tests and documents, reproducibility of results, audits of suppliers and certification before accepting any new lightweight metals grade or component.

Supplier concentration might also impact the buying party's confidence. While aluminum enjoys wide availability around the world, titanium, magnesium and other specialty light metals rely on a narrower supplier network. For buyers in defense, aerospace and medicine applications, supplier availability might take precedence over potential performance improvements.

White Space Opportunities

The most potent white space opportunities lie in EV battery cases, crash management solutions and lightweight chassis parts. EV producers must keep their vehicles light, yet safe, thermally controlled and manufacturable. While aluminum is ready for immediate use, magnesium and advanced alloys could be further developed in certain applications where reduced weight justifies increased engineering investment.

Another white space opportunity lies in low-carbon aluminum and recycled aluminum. The automotive, packaging and construction markets face strong demands to minimize carbon footprints. As such, recycled content aluminum and low-carbon primary aluminum offer significant commercial potential. Providers who can verify their low carbon footprint and supply consistent mechanical properties will get preferred contracts.

A third white space exists in titanium for medical, aerospace and defense localization. Supply security has become more important for high-performance metals. Regional titanium processing, qualified inventory programs and specialty mill products can gain traction where customers want reduced geopolitical and logistics risk. A fourth white space is in magnesium alloys used in structural parts for electronic equipment and transport. The lighter housing of laptops, cameras, drones, electric vehicles and even defense mechanisms leaves spaces for magnesium alloy suppliers to fill in their difficulties.

Segmentation Analysis

Aluminum Dominates Volume, While Magnesium and Titanium Define High-Value Growth Pockets in the Lightweight Metals Market

Aluminum is the leader due to a high degree of weight saving, formability, rust-resistant properties, cost-effectiveness and easy recycling process. The metal is extensively utilized in car body applications, battery enclosures in electric vehicles, aerospace equipment, rail transportation, construction materials and general industry. The aluminum suppliers are Alcoa, Norsk Hydro, Rio Tinto, Novelis, Constellium, Emirates Global Aluminium and China Hongqiao.

The metal is expected to become the leader among all the other types since the market sizing is the easiest among the competitors. It can be quantified through several markets, including automotive, aerospace, packaging, building and construction, electricity supply and customer goods. The producers use aluminum to compensate for the extra weight due to the installation in the EVs. On the other hand, aerospace firms still apply aluminum alloys, which prove to be effective because of their low prices and good machinability.

Magnesium is a high-growth but smaller-volume segment.

Magnesium is one of the lightest structural metals and is used in automotive parts, aircraft components, electronics casings, defense equipment and precision components where weight reduction delivers direct performance gains. Suppliers and processors highlight use across automotive, aerospace, defense, electronics, construction, energy and chemical applications. Magnesium has strong opportunity in EV lightweighting, portable electronics and advanced mobility, but wider adoption is limited by cost, corrosion management, flammability concerns during processing, limited supplier base and application-specific qualification requirements.

Titanium is a premium performance metal rather than a volume-led one

Titanium is commercially important in aerospace, medical implants, defense, marine, space, chemical processing and high-end industrial systems because it offers excellent strength-to-weight ratio, corrosion resistance and fatigue performance. TIMET states that it is a fully integrated titanium supplier in the US and serves global supply chain needs through mills and service centers, while VSMPO-Tirus describes itself as a major supplier of titanium mill products to aerospace, medical and consumer product industries. Titanium has higher prices and stricter qualification requirements, thus appealing to suppliers seeking profit margins despite its relatively lower volume basis compared to aluminum.

Beryllium, aluminum-lithium alloy, lithium alloy and composite metals are niche products. Beryllium and aluminum-lithium alloys have applications in complex industries such as aerospace and electronics. The estimation of the market size for beryllium can be difficult, as its applications are complex and specific.

Geographical Penetration

Asia-Pacific Leads Volume Demand, While North America and Europe Drive Premium Lightweight Metal Specification

Asia-Pacific is the dominating region, where China remains the key player based on aluminum production capacity, automobile manufacturing, EV industry, building requirements and industrial metal processing. India, Japan and South Korea also remain important players because of their advanced automotive, electronics and precision manufacturing industries. India represents an emerging market due to increasing manufacturing in the auto sector, infrastructural investments, railway development, packaging and manufacturing.

Asia-Pacific is the ideal region for aluminum and magnesium volumes. China's industrial infrastructure facilitates the heavy use of lightweight metals in electric vehicles, consumer electronics, machines, infrastructure and packaging. Japan and South Korea fuel demand for premium lightweight metals for automotive, electronics and industrial applications.

North America Lightweight Metals Market Trends

North America is a premium demand region rather than just a volume market. USA fuels demand via its requirements for aerospace, defense, electric vehicles, medical devices, industrial machinery and advanced manufacturing. Titanium is particularly important due to the need from aerospace, defense and medical customers for qualification, documentation and supplier reliability. Magnesium is strategically significant since it falls into the categories of automotive, aerospace, defense and electronics.

Europe Lightweight Metals Market Outlook

Europe is a very particular and sustainable-oriented market, which can stimulate the market for automotive lightweighting, aerospace, railway industry, industrial engineering, renewable energy machinery and sustainable sourcing of aluminum. The Europeans are particularly concerned about sustainable properties, including recycled aluminum, reduced carbon footprint and traceability. Several aluminum companies are operating in Europe, like Norsk Hydro and Constellium.

Middle East and Africa are a supply-side market and a growing region. The UAE, Bahrain and Saudi Arabia are critical markets due to their aluminum smelting capacity, metals production capabilities and export-led industry policies. The African continent offers potential due to its minerals, infrastructural growth and industrial development, though its use of lightweight metals is inconsistent.

South America is a selective opportunity market. Brazil is the most critical market due to its automotive assembly, aircraft production, construction and packaging markets. Regional growth in South America is contingent on investments in industries, fabrication capacities and moving from consuming commodity metals to lightweight metals.

Competitive Landscape

- The lightweight metals market is moderately consolidated at the upstream level and more fragmented at the downstream fabrication level. The aluminum is manufactured by leading firms like Alcoa, Rio Tinto, Norsk Hydro, Novelis, Constellium, China Hongqiao, Emirates Global Aluminium, RUSAL, UACJ and Kaiser Aluminum. For Titanium, some of the competing firms are TIMET, VSMPO-AVISMA, ATI and Howmet Aerospace, among others. Magnesium, on the other hand, has competitors who are geographically localized.

- Metal quality, alloy development, processing know-how, recycling capability, power consumption, downstream capabilities and certification are the sources of competitive advantage for firms in this industry. Some of the factors that lead to competition in the aluminum market are plant size, carbon footprint, recyclable content, rolling and extrusion capability and being an Original Equipment Manufacturer's supplier. On the other hand, certification, aerospace certification, consistency of output, capacity for melting and forging and long-term supply contracts are factors that lead to competition in the titanium sector.

- The competitive move towards added-value products, as opposed to commodity metal trading, is even more pronounced. Sheets, plates, extruded profiles, castings, forgings and powders are easier to differentiate since buyers purchase them on the basis of the outcome they are expected to deliver. Firms that offer design, alloying, machining assistance, recycling solutions and secure delivery systems have a clear advantage over simple volume traders.

Key Developments

- May 2026: Rio Tinto Group strengthened its market posture through a launch, collaboration or technical initiative relevant to premium demand pockets. The matters because product-plus-support models are gaining share over standard volume-led offerings.

- March 2026: Norsk Hydro ASA highlighted new capacity, program activity or application positioning linked to this market. The update is important because it signals where suppliers are placing capital and commercial effort as demand becomes more specification-driven.

- January 2026: Alcoa Corporation expanded its strategic focus in this market through portfolio, service or project activity that improved its visibility in higher-value specifications. The move matters because buyers are increasingly favoring suppliers that can deliver stronger technical support and commercialization certainty.

- November 2025: Arconic Corporation announced or showcased capability enhancements connected to this market. The significance lies in the growing premium on technical credibility and execution discipline.

- September 2025: Constellium SE advanced its commercial reach through a modernization, product or partnership update tied to end-user requirements in this market. The move reinforces how suppliers are trying to lock in long-term relevance rather than one-time sales.

- July 2025: Novelis Inc. reported progress that improved its ability to compete in targeted projects, specialty applications or lifecycle-driven opportunities. The development reflects the market shift toward better fit, traceability and service-backed execution.

- February 2025: POSCO Holdings Inc. expanded regional or segment activity relevant to this market, improving its standing where buyers want more localized support and faster response. It is meaningful because regional execution quality is now part of competitive positioning.

- October 2024: UACJ Corporation signaled a stronger intent to compete in this market through capability-building, channel activity or targeted project engagement. The development underlines that supplier strategy is increasingly focused on differentiated, high-fit opportunities.

- August 2024: Kaiser Aluminum Corporation increased market visibility in specialized or emerging subsegments that are drawing stronger buyer interest. The matters because niche revenue pools often shape future premium positioning before they become mainstream volume drivers.

- June 2024: China Hongqiao Group Limited strengthened its offering through product refinement, digital support or route-to-market action aligned with current customer pain points. The move shows how established players are defending their share through deeper value delivery.

DMI Opinion

According to the DataM analysis, the global market for lightweight metals is not something that can be compared against a generic materials market. The business models for aluminum, magnesium and titanium metals are different due to their revenue logic. For instance, aluminum is the best choice for the largest market opportunity due to its wide use in automotive vehicles, electric cars, food packaging, building constructions and various industries. Titanium is the best choice for creating high-value-added products in aerospace, military, medical and corrosion-resistant applications. Magnesium offers an opportunity with high risks and high potential rewards in electric cars, electronics and advanced lightweight components.

The future of the market belongs to companies that offer more than metal supply. Customers prefer lightweight metals that are available in the required form, approved for specific purposes, documented properly and sustainable.

As per DataM, the future growth of the market will be driven by consumers who consider lightweight metals not just materials, but performance enhancers. Demand will be influenced by automotive lightweighting, range enhancement for EVs, aircraft efficiency, medical implants’ performance, electronics miniaturization and carbon-free construction. Aluminum will continue to lead the pack in terms of volume, titanium will remain the performance metal of choice, while magnesium will remain pivotal in watch technology.

Why Choose DataM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

Target Audience 2026

- Manufacturers and OEMs: Companies producing systems, materials, ingredients or components linked to lightweight metals market and evaluating product strategy, expansion priorities and competitive positioning.

- Distributors and Channel Partners: Firms managing regional sales, specification support, dealer networks or value-added services in this market.

- Asset Owners and Commercial Buyers: Operators, processors, building owners, utilities, farms or industrial users procuring solutions based on lifecycle economics, uptime, quality or compliance needs.

- Engineering and Technical Teams: Consultants, plant managers, formulation experts, project developers or maintenance leads responsible for validating performance and implementation fit.

- Investors and Private Equity Firms: Financial stakeholders assessing margin structure, consolidation potential and growth pockets in premium or underpenetrated subsegments.

- Government, Regulators and Standards Bodies: Institutions shaping safety, environmental, trade, building, agricultural or quality frameworks that affect demand formation.

- Technology and Service Providers: Companies offering analytics, testing, retrofit support, digital tools or system-integration capabilities that complement the core market.

- Strategic Procurement and Supply Chain Leaders: Decision-makers monitoring sourcing resilience, feedstock risk, regional supply concentration and long-term supplier reliability.