Introduction: Lithium Chemicals as the Backbone of the Energy Transition

The global energy transition is fundamentally reshaping demand for lithium chemicals, particularly lithium carbonate, lithium hydroxide, and lithium chloride. As electric vehicle (EV) adoption accelerates and grid-scale energy storage expands, lithium compounds have become strategic inputs in the battery supply chain.

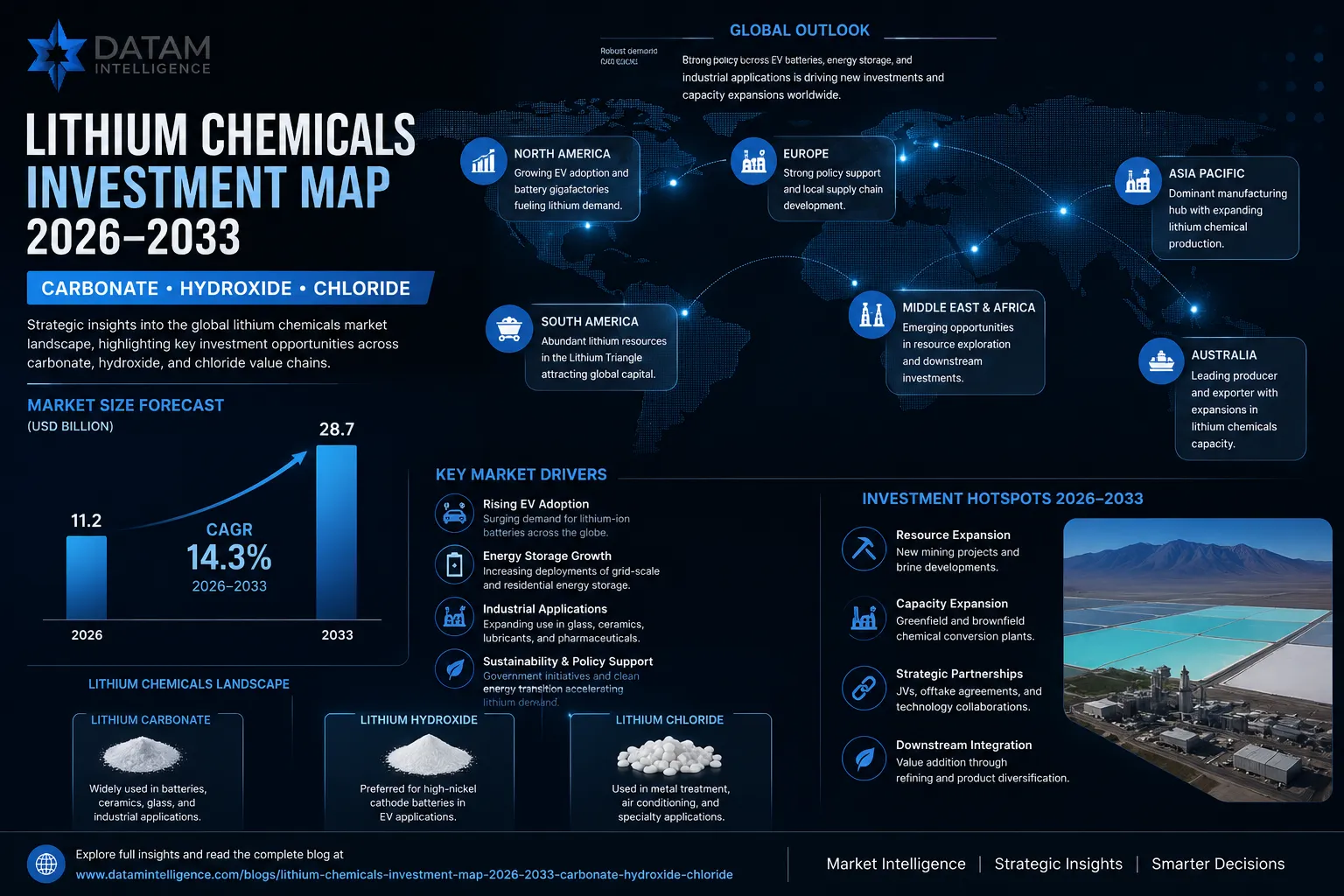

Between 2026 and 2033, capital investment is expected to intensify across upstream extraction, midstream refining, and battery-grade chemical conversion. However, investment allocation is increasingly diverging across lithium carbonate, lithium hydroxide, and lithium chloride segments based on battery chemistry evolution, regional policy incentives, and downstream OEM requirements.

This report provides a strategic investment map of the lithium chemicals market, highlighting where institutional capital, strategic partnerships, and capacity expansions are concentrated.

Executive Summary

- Lithium hydroxide demand is accelerating due to high-nickel NMC batteries used in long-range EVs.

- Lithium carbonate remains dominant in LFP battery systems, especially in China and stationary storage.

- Lithium chloride is gaining industrial relevance in processing efficiency and niche chemical applications.

- Investment is shifting from upstream mining to refining, conversion, and battery-grade chemical production.

- Asia-Pacific continues to dominate capacity, but North America and Europe are rapidly expanding localization strategies.

Explore Lithium Chemicals Market Analysis report

1. Global Lithium Chemicals Market Overview (2026–2033 Outlook)

The lithium chemicals market is undergoing structural transformation driven by:

- Rapid EV penetration (>40% CAGR in select regions)

- Energy storage system (ESS) deployment at grid scale

- Supply chain localization policies (US IRA, EU Critical Raw Materials Act)

- Shift in cathode chemistry balance: NMC vs LFP competition

Key Market Segments:

- Lithium Carbonate (Li₂CO₃)

- Lithium Hydroxide (LiOH)

- Lithium Chloride (LiCl)

Each segment is experiencing distinct investment dynamics based on downstream battery chemistry requirements.

2. Lithium Carbonate Investment Trends: The LFP Expansion Engine

Lithium carbonate remains the most widely traded lithium chemical globally, largely driven by its dominance in LFP (Lithium Iron Phosphate) batteries.

Key Demand Drivers:

- Mass-market EVs (cost-sensitive segments)

- Grid energy storage systems

- China-led LFP battery expansion

Investment Flow Patterns:

- Expansion of carbonate refining capacity in South America (lithium brines)

- Strong midstream investments in China

- Rising interest in low-cost conversion technologies

Strategic Insight:

Lithium carbonate is increasingly viewed as a volume-driven commodity market, where scale efficiency and low-cost production determine competitiveness.

3. Lithium Hydroxide Investment Surge: High-Nickel Battery Revolution

Lithium hydroxide is emerging as the premium-grade lithium chemical, essential for NMC (Nickel Manganese Cobalt) and NCA batteries used in long-range EVs.

Key Demand Drivers:

- Premium EV segment growth (Tesla-style long-range models)

- Increased nickel intensity in cathodes

- Western OEM supply chain diversification

Investment Trends:

- Heavy CAPEX in North America and Australia conversion plants

- Strategic partnerships between miners and automakers

- Vertical integration across refining and cathode production

Strategic Insight:

Lithium hydroxide represents a margin-rich segment, with higher technical barriers and stronger OEM lock-in compared to carbonate.

4. Lithium Chloride: Emerging Industrial and Processing Segment

Lithium chloride remains a smaller but strategically important chemical, primarily used in:

- Lithium extraction and purification processes

- Industrial desiccants and specialty chemical applications

- Battery precursor processing pathways

Investment Characteristics:

- Lower volume, high technical specialization

- Increasing adoption in advanced refining technologies

- Indirect exposure to EV supply chain growth

Strategic Insight:

While not a primary battery material, lithium chloride plays a critical enabling role in refining efficiency and process optimization, making it relevant in upstream investment strategies.

5. Regional Investment Map: Where Capital is Flowing in Lithium Chemicals (2026 - 2033)

The global lithium chemicals investment landscape is becoming increasingly geographically fragmented yet strategically interdependent. Capital flows are no longer driven solely by resource availability; instead, they are shaped by policy incentives, battery chemistry localization, refining capacity control, and supply chain security mandates.

Between 2026 and 2033, four regions Asia-Pacific, North America, Europe, and South America will collectively define the structure of global lithium chemical production and conversion capacity.

Asia-Pacific (Dominant Global Hub for Lithium Chemicals)

Asia-Pacific, led overwhelmingly by China, remains the center of gravity for global lithium chemical processing and battery material conversion. The region controls a disproportionate share of refining capacity, downstream battery manufacturing, and cathode integration ecosystems.

Key Structural Advantages

- Largest global refining and conversion capacity

- China dominates lithium carbonate and lithium hydroxide refining output.

- Highly integrated midstream chemical processing clusters reduce cost per ton significantly.

- Strong LFP ecosystem integration

- Lithium iron phosphate (LFP) batteries are deeply embedded in China’s EV and ESS markets.

- This directly supports sustained demand for lithium carbonate as the primary feedstock.

- Battery manufacturing dominance

- Proximity between lithium refiners, cathode producers, and gigafactories ensures tight supply chain synchronization.

- Companies benefit from scale economies and rapid commercialization cycles.

Investment Insight

Asia-Pacific is shifting from resource-driven growth to efficiency-driven chemical scaling, where the key competitive advantage is not lithium access—but processing cost leadership and integrated battery ecosystem control.

North America (Rapid Expansion Through Policy-Led Industrialization)

North America is undergoing one of the fastest transformations in the global lithium chemicals landscape, driven primarily by policy intervention under the Inflation Reduction Act (IRA) and national critical mineral security strategies.

Key Investment Drivers

- IRA-driven investment incentives

- Tax credits and subsidies are accelerating domestic lithium refining and battery material production.

- Strong push to reduce dependency on imported lithium chemicals from Asia.

- New lithium hydroxide refining projects

- Significant CAPEX is flowing into hydroxide conversion facilities in the U.S. and Canada.

- Focus is on supplying high-nickel NMC battery supply chains for premium EVs.

- EV OEM localization strategies

- Automakers are forming long-term offtake agreements with lithium producers.

- Vertical integration is increasing across mining, refining, and cathode production.

Investment Insight

North America’s lithium strategy is chemistry-selective rather than volume-driven, prioritizing lithium hydroxide production aligned with premium EV battery architectures.

Europe (Strategic Security & Supply Chain Sovereignty Focus)

Europe’s lithium chemicals strategy is defined less by resource abundance and more by industrial security, regulatory alignment, and decarbonization mandates.

Key Structural Trends

- Supply chain independence initiatives

- The EU Critical Raw Materials Act is driving domestic lithium refining investments.

- Strategic focus is on reducing exposure to Asian chemical imports.

- Battery gigafactory expansion

- Rapid growth of EV battery manufacturing hubs in Germany, France, and Eastern Europe.

- This is increasing long-term demand for both lithium carbonate and hydroxide.

- Increasing hydroxide import dependency

- Despite localization efforts, Europe remains structurally dependent on imported lithium hydroxide.

- This creates a persistent supply-demand imbalance, attracting foreign investment.

Investment Insight

Europe represents a demand-heavy but supply-constrained lithium chemicals market, where strategic investments are focused on refining security rather than upstream resource control.

South America (Global Resource Base for Lithium Brines)

South America continues to function as the primary upstream lithium resource basin, particularly through its dominance in lithium brine extraction across the “Lithium Triangle.”

Core Regional Strengths

- Lithium brine dominance (Chile, Argentina, Bolivia)

- The region holds the world’s largest and lowest-cost brine-based lithium reserves.

- Chile and Argentina are already major contributors to global lithium carbonate supply.

- Growing upstream-to-midstream integration

- Increasing investment in local refining and chemical conversion facilities.

- Governments are pushing for value addition rather than raw export models.

Investment Insight

South America is transitioning from a raw material exporter to a vertically integrated lithium production base, with rising emphasis on domestic lithium carbonate processing and midstream chemical upgrading.

Strategic Global Takeaway (Investor Lens)

The regional investment map reveals a clear structural shift in the lithium chemicals market:

- Asia-Pacific = processing and scale dominance

- North America = policy-driven hydroxide expansion

- Europe = supply security and demand concentration

- South America = upstream resource leverage moving toward value addition

Key Insight for Investors

The next phase of the lithium supercycle will not be defined by where lithium is mined but by where lithium is chemically converted, refined, and locked into battery supply chains.

6. Key Market Drivers

- Electric vehicle battery demand growth

- Battery chemistry transition (LFP vs NMC)

- Energy storage system deployment

- Government subsidies and mineral security policies

- Supply chain localization strategies

- ESG and sustainable mining practices

7. Competitive Landscape & Strategic Positioning

The lithium chemicals value chain is becoming increasingly vertically integrated:

- Mining companies are moving into refining

- Battery manufacturers are securing upstream supply

- Automakers are investing directly in lithium conversion assets

Key Strategic Trend:

Control of refining capacity is becoming more valuable than raw lithium extraction.

8. Investment Outlook 2026 - 2033

Key Forecast Themes:

- Hydroxide CAGR outpacing carbonate in premium EV segment

- Carbonate maintaining dominance in mass-market EVs and ESS

- Chloride growing as a process-enabling chemical

- Increasing CAPEX concentration in refining infrastructure

Investor Takeaway:

The lithium chemicals market is transitioning from a commodity extraction model to a vertically integrated chemical processing ecosystem.

Conclusion: Strategic Allocation of Capital Defines the Next Lithium Super cycle

Between 2026 and 2033, lithium chemicals will remain central to the global electrification economy. However, investment success will depend not only on resource access but on chemical specialization, refining capability, and downstream integration.

- Lithium carbonate = scale-driven commodity growth

- Lithium hydroxide = high-margin EV premium segment

- Lithium chloride = enabling industrial efficiency layer

Investors, OEMs, and governments are now competing for position in a chemistry-driven energy transition supply chain, where refining capability is the new strategic bottleneck.