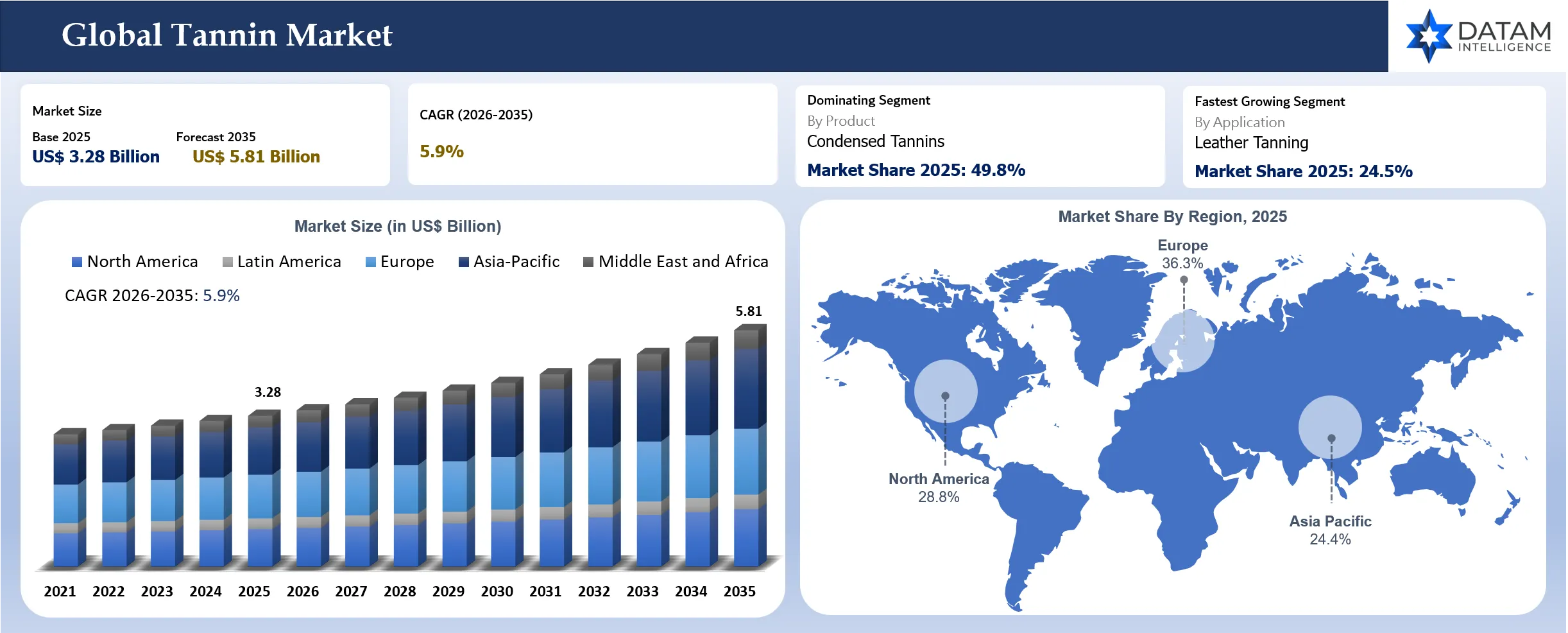

Tannin Market Size

The global tannin market reached US$ 3.28 billion in 2025 and is expected to reach US$ 5.81 billion by 2035, growing at a CAGR of 5.9% during 2026 to 2035. Demand is supported by vegetable leather tanning, wine and beverage processing, animal feed, wood adhesives, nutraceuticals, pharmaceuticals and natural dyeing. Tannin buyers are increasingly separating bulk extract demand from premium specialty grades. Tanneries focus on consistent color, penetration and yield, while wineries need tannins that improve mouthfeel, color stability, oxidation control and sensory profile. Feed and nutraceutical buyers require stronger documentation, purity control and safety support.

Asia-Pacific remains the fastest-growing market because leather production, feed manufacturing, food processing and plant extract demand are concentrated across China, India and Southeast Asia. Europe remains a high-value market due to wine, leather, specialty ingredients and bio-based resin development. Supplier differentiation will depend on extract source security, forest sourcing credibility, product standardization, technical application support, documentation and the ability to serve both bulk and specialty customers.

Market Scope

| Metric | Insight |

| Market Size In 2025 | US$ 3.28 Billion |

| Market Size By 2035 | US$ 5.81 Billion |

| CAGR During 2026 To 2035 | 5.9% |

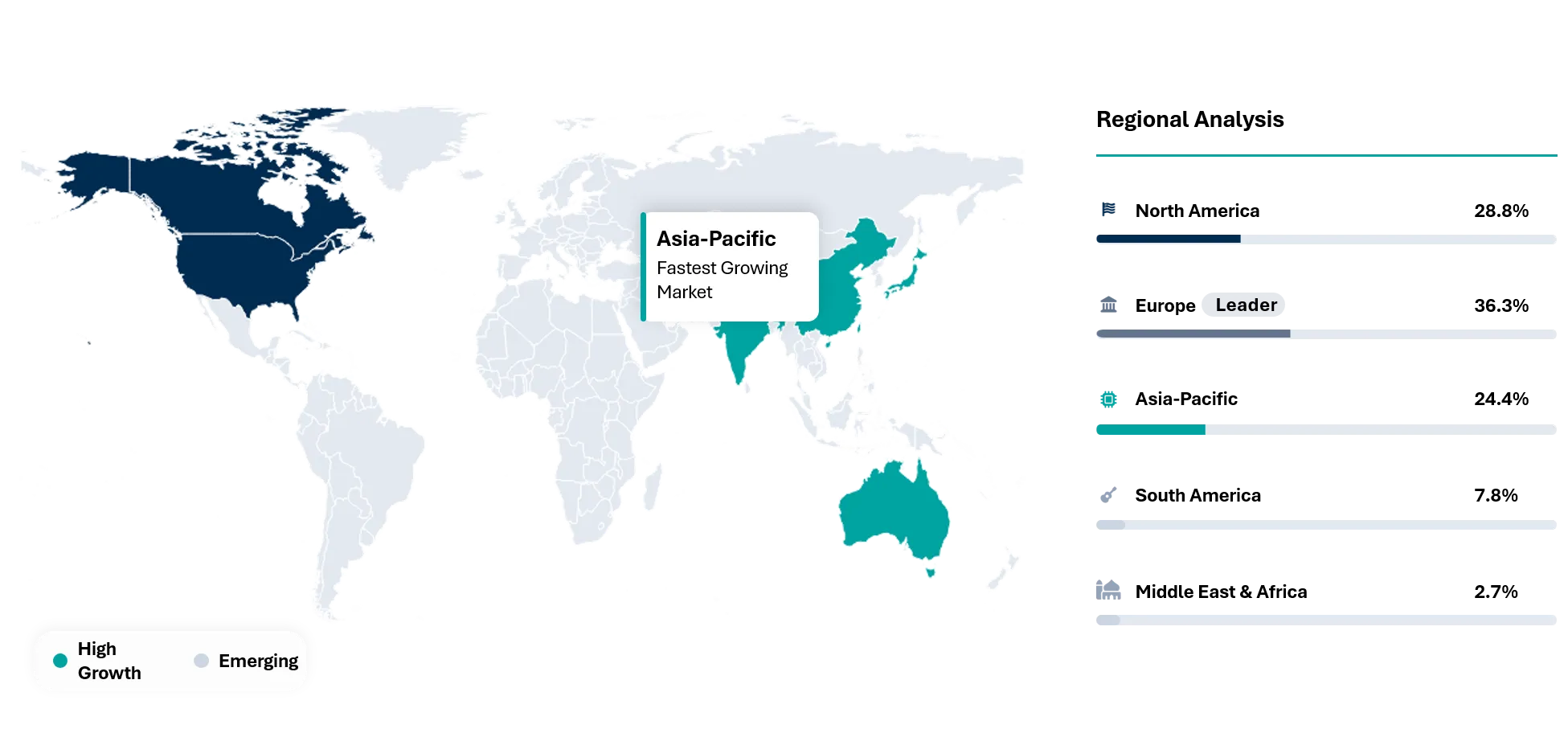

| Largest Region In 2025 | Europe, 36.3% market share in 2025 |

| Fastest Growing Region | Asia-Pacific, 5.6% CAGR between 2026 and 2035 |

| Key Regional Shift | Asia-Pacific is expected to increase from 24.4% market share in 2025 to 27.3% market share by 2035 |

| Leading Product Type | Condensed Tannins |

| Fastest Growing Product Type | Hydrolysable Tannins |

| Leading Application | Leather Tanning |

| Fastest Growing Application | Food and Nutraceuticals |

| Market Maturity | Growth Stage |

| Key Buying Question | Which tannin source can deliver consistent performance, traceable sourcing and application-specific documentation? |

| By Product Type | Condensed Tannins, Hydrolysable Tannins, Phlorotannins, Complex Tannins, Others |

| By Source | Quebracho, Mimosa, Chestnut, Tara, Oak, Gallnut, Grape Seed, Green Tea, Others |

| By Form | Powder, Liquid Extract, Granules, Blends |

| By Application | Leather Tanning, Wine and Beverage Processing, Wood Adhesives and Resins, Animal Feed, Food and Nutraceuticals, Pharmaceuticals and Personal Care, Water Treatment, Textile Dyeing and Mordants, Others |

| By End-User | Tanneries, Wineries and Beverage Producers, Wood Panel and Adhesive Manufacturers, Feed Additive Producers, Food and Nutraceutical Companies, Pharmaceutical and Personal Care Companies, Textile Processors, Others |

| By Region | North America, Europe, South America, Asia-Pacific, Middle East and Africa |

Key Takeaways

- Asia-Pacific is the fastest-growing region with 5.6% CAGR between 2026 and 2035 due to stronger demand from China, India, Indonesia, Vietnam and South Korea.

- Condensed tannins remain the leading product type because quebracho and mimosa extracts are widely used in leather tanning, wood adhesives and industrial applications.

- Hydrolysable tannins are expected to grow faster as chestnut, tara, gallnut and oak-derived grades gain demand in wine, food, nutraceutical and pharmaceutical applications.

- Leather tanning remains the leading application because vegetable tannins provide color, body and handle in specialty leather categories.

- Food and nutraceuticals are expected to grow fastest as plant polyphenols gain demand in natural antioxidants, gut health and clean-label positioning.

- Supplier differentiation is moving toward traceable sourcing, extract standardization, low-variation active content, application support and regulatory documentation.

Why Does This Report Matter in 2026?

Tannin demand matters in 2026 because natural chemistry is moving from legacy tanning into higher-value applications such as wine quality management, animal nutrition, bio-based resins, nutraceuticals and personal care. Customers no longer purchase tannins only as bulk extracts. They increasingly need source-specific performance, predictable active content and documentation that supports food, feed, beverage and industrial use. Leather remains important, but the market is changing. Chrome tanning still dominates global leather production because of cost and speed, while vegetable tanning is gaining value in premium leather, luxury goods and sustainability-driven branding. Tannin suppliers must support tanneries with consistent extract performance, color control and technical blending rather than selling undifferentiated plant extracts.

Bio-based materials create a new market layer. Wood panels, insulation and adhesive manufacturers are evaluating tannins as partial replacements for fossil-based phenols in resin systems. Feed producers are using plant polyphenols for gut health and methane-related positioning. Wineries use enological tannins to improve structure, color and oxidation stability. These application shifts make supplier capability more important than raw extract availability alone.

Strategic Indicators for Tannin

High Regulation Impact

Tannin regulation varies by application. Leather tanning inputs require chemical safety documentation, while food, feed, beverage and pharmaceutical applications require stronger purity, safety and traceability controls. Wineries need products suited for enological use, while feed additive producers need clear labeling, safety data and regional compliance. Regulatory pressure is therefore highest in food, beverage, feed and healthcare-related uses.

Forest sourcing scrutiny is also increasing. Quebracho, mimosa, chestnut and oak extracts depend on plant raw materials. Customers are asking suppliers to demonstrate responsible sourcing, sustainable harvesting and controlled supply chains. Tannin suppliers with traceability and forest stewardship practices can build stronger customer trust. Pharmaceutical and nutraceutical buyers require tighter specifications. Active polyphenol content, contaminants, solvent residues and microbial quality matter more than in bulk leather applications. Suppliers moving into premium applications need quality systems that can support audit requirements.

White Space & Investment Opportunities

- Standardized tannin extracts for food, feed and nutraceutical customers remain undersupplied where buyers require stable polyphenol content, contaminant control and batch-to-batch documentation.

- Bio-based phenolic resin development is attractive because wood panels, insulation boards and molded materials need renewable chemistry that can reduce fossil phenol dependence without losing performance.

- Traceable quebracho, mimosa, chestnut and tara supply programs can serve premium leather, wine and ingredient buyers that now treat sourcing proof as part of procurement qualification.

- Regional blending and application labs in Asia-Pacific, Europe and South America can help suppliers localize dosage guidance, reduce customer trials and improve conversion from commodity extracts to specialty grades.

Economic & Investment Analysis

Macroeconomic exposure in tannins is tied to forest availability, leather production cycles, wine production quality, feed additive adoption and specialty ingredient demand. Bulk vegetable extract customers remain sensitive to freight, harvest yield and extraction cost because large-volume leather and industrial buyers usually work with tight formulation budgets. Premium enology, nutraceutical and pharmaceutical grades behave differently. Customers in those channels pay for documented purity, active content, application support and reliable sensory or functional performance rather than buying only on extract weight.

Investment is moving toward source security, extraction efficiency, quality standardization and application laboratories. South American and African raw material positions remain important for quebracho and mimosa economics while Europe keeps value through wine, specialty ingredients and bio-based material development. Asia-Pacific offers consumption growth because leather, feed, food processing and plant extract manufacturing sit close together. Margin improvement will come from better batch control, lower extraction variability, traceable sourcing and technical selling into higher-value uses.

Interest rate pressure and inflation can slow discretionary investment by tanneries, wood panel producers and smaller ingredient buyers. Even so, the market has a defensive growth layer because tannins serve multiple industries with different cycles. Leather may weaken in one year while wine, feed or nutraceutical demand holds up. Suppliers that balance bulk extract contracts with specialty grade portfolios can reduce earnings volatility and improve customer retention.

Investment Trends in the Market

Investment is shifting from basic extraction capacity toward application-specific development, traceable supply chains and premium grade documentation. Suppliers are prioritizing extraction optimization, spray drying, active content testing, blending systems and customer-facing laboratories. The strongest investment cases are not only linked to more output. They are linked to lower batch variation, better source control and stronger technical proof for regulated or sensory-sensitive applications.

- Extraction process upgrades for higher yield, lower color variation and improved active content consistency.

- Application labs for leather, wine, feed, nutraceuticals and bio-based resin formulation support.

- Sustainable forestry programs, source mapping and supplier audits for premium customer qualification.

- Specialty grade development for enology, animal nutrition, food ingredients and plant polyphenol blends.

Supply Chain Disruption

Supply risk is tied to forest raw materials, harvest cycles, extraction capacity, weather conditions, transport and regional export rules. Quebracho, mimosa and chestnut extracts depend on wood and bark availability. Poor harvest conditions or sourcing restrictions can affect extract supply and price. Quality variation is a practical supply challenge. Plant extracts can vary by species, geography, season, age and extraction method. Customers in leather may manage variation through blending, but food, feed and enology buyers need tighter control. Suppliers that standardize active content can reduce customer risk.

Logistics also affects tannin availability. Bulk extracts may move from South America, Europe, Africa and Asia to processing and consumption markets. Freight disruptions can influence tannery and beverage supply chains. Local inventory and diversified sourcing reduce risk.

Pricing Volatility

Tannin pricing depends on raw material availability, extract yield, active content, purity, form, application grade and documentation requirements. Bulk leather tannins are more price-sensitive, while enology, nutraceutical and pharmaceutical grades command higher pricing due to tighter specifications and application value. Quebracho and mimosa extract pricing is affected by forestry conditions and extraction economics. Tara, chestnut and gallnut tannins can be more specialized and may carry higher prices. Grape seed and green tea extracts are often linked to nutraceutical and food ingredient markets.

Premium pricing is strongest when tannins solve application-specific problems. Wineries pay for sensory outcomes, color stability and brand consistency. Feed producers pay for measurable performance and safety documentation. Wood adhesive buyers evaluate cost against phenol replacement value and resin performance.

Procurement Pressure

Tanneries require predictable color, penetration and handling properties. A tannin extract with inconsistent performance can create leather quality variation and production rework. Procurement teams compare price but also evaluate yield, solubility, blending behavior and supplier technical support. Wineries require a different buying approach. Tannins must align with grape variety, wine style, phenolic profile and processing stage. Enology suppliers need strong application guidance and sensory credibility. Price matters less than performance consistency and winemaker trust.

Feed and nutraceutical buyers focus on safety, documentation and active content. Suppliers need certificate support, contaminant controls and traceability. Procurement teams increasingly ask for specification stability and regional compliance support.

Buyer Decision-Making Criteria

Tanneries usually assess suppliers through extract performance, shade consistency, penetration behavior, solubility, delivery reliability and price per usable effect. Price matters but it is not the only decision factor because inconsistent extract performance can affect leather feel, color uniformity and rework rates. Early technical support can influence formulation choices and create stronger supplier stickiness than spot selling. Buyers also prefer suppliers that can hold inventory close to production hubs because leather production schedules are sensitive to shipment delays.

Wineries evaluate tannins through sensory outcome, grape variety fit, oxidation control, color stability and confidence in technical advice. A winemaker will not switch easily if a product is already integrated into a style profile or vintage workflow. Enology suppliers therefore win through trust, trial support and clear dosage guidance. Procurement teams may negotiate price but product approval often sits with technical and sensory teams that focus on consistency and brand risk.

Food, feed and nutraceutical buyers use a more compliance-led process. They review active content, purity, microbial limits, contaminants, solvent residues, labeling status and regional regulatory support before approving a new supplier. Commercial buyers also look for audit readiness and documentation speed because delayed paperwork can slow customer launches. Suppliers that combine raw material control, analytical testing and practical application guidance will have stronger approval rates across regulated end uses.

New Technology Adoption

Technology adoption is strongest in extraction efficiency, active content standardization, low-solvent processing, spray drying, microencapsulation and application-specific blending. Better extraction can improve yield and reduce waste. Standardization helps buyers manage performance variation across batches. Bio-based resin technology is a strong innovation area. Tannins can act as phenolic building blocks in adhesives, foams and wood panels. Performance, cost and curing behavior remain critical. Suppliers able to support formulation work with panel manufacturers can open new demand.

Feed and nutraceutical development is also increasing. Tannin blends can be tailored for animal species, gut health, protein binding and methane-related positioning. Controlled release and encapsulated forms may gain relevance where taste, stability or bioavailability matter.

Regional Expansion Opportunity

Asia-Pacific offers the strongest regional opportunity because leather production, food processing, nutraceuticals and feed additives are expanding. China and India are especially important because they combine leather production with large food and animal nutrition sectors. Southeast Asia adds tannery, food and feed demand. Europe remains a high-value market due to wine, premium leather, nutraceuticals and bio-based materials research. France, Italy, Spain and Germany are important because wine, leather goods, specialty chemicals and sustainability-led innovation are strong. European buyers value documentation and traceability.

South America is important on the supply side. Argentina and Brazil are relevant for quebracho and tara-linked supply chains, while local leather and food processing also support demand. Regional suppliers can strengthen global positions through sustainable sourcing and extract standardization.

Government Policy Support

Government policy supports tannin demand indirectly through sustainable chemistry, forestry management, bio-based materials and food safety frameworks. Programs encouraging bio-based industrial materials can support tannin use in adhesives and resins. Forest management rules influence raw material availability and sourcing credibility. Food and feed safety rules also shape demand. Suppliers serving nutraceutical, food and feed markets need documentation that satisfies regional authorities. Compliance readiness can become a competitive advantage.

Leather sector policy matters in regions where environmental rules restrict wastewater discharge and chemical handling. Vegetable tanning can gain attention where brands and regulators encourage cleaner production. However, cost and processing time remain barriers against full replacement of chrome tanning.

Future Market Transformation

By 2035, tannin suppliers will operate less like commodity extract sellers and more like application chemistry partners. Leather, wine, animal nutrition, nutraceutical and bio-based material customers will expect validated performance data, traceable origin records, tailored blends and technical service. Demand will still include bulk vegetable tanning extracts but value growth will increasingly come from standardized grades that help customers reduce formulation risk or support premium product claims.

Business models are likely to shift toward long-term sourcing programs, application co-development and region-specific technical support. Wine and food customers will require tighter quality records. Feed producers will need species-specific performance guidance. Bio-based resin developers will expect formulation collaboration and pilot-scale testing. Forest origin and harvest practices will become more visible in supplier evaluations because customers will connect ingredient choice with brand reputation and ESG commitments.

The strongest companies will combine secure plant raw material access with analytical control, blending capability and customer education. Suppliers that only compete on bulk extract price may face margin pressure as customers demand more proof and faster documentation. Companies that build technical depth across enology, animal nutrition, adhesives and specialty ingredients can capture higher-value contracts while reducing exposure to leather cycles.

Import-Export and Pricing Intelligence

Tannin trade is linked to vegetable tanning extracts, tannic acid, plant extracts, enology inputs, feed additives and natural polyphenol ingredients. Bulk tanning extracts may be tracked differently from refined tannic acid and specialty plant extracts.

Pricing varies strongly by source and purity. Quebracho and mimosa extracts are often positioned for leather and industrial applications. Chestnut, tara, gallnut, oak, grape seed and green tea tannins may be used in more specialized food, beverage, nutraceutical or pharmaceutical applications. Specialty grades carry higher value because active content, color, solubility and documentation requirements are stricter.

Leather demand supports larger volume, while wine, nutraceutical and feed applications support higher value per kilogram. Procurement teams compare not only price but also active tannin content, extract yield, solubility, sensory profile and compliance documentation. Strong suppliers help customers optimize use level and performance rather than selling extracts on weight alone.

AI Impact Analysis

AI impact in the tannin market is strongest in extraction optimization, quality control, formulation and demand forecasting. Plant extracts vary naturally, so producers can use analytics to compare raw material characteristics, extraction yield, active content and color behavior. Better models can reduce batch variation. In wine applications, AI can support tannin selection by analyzing grape chemistry, phenolic balance and target wine profile. Such tools can help winemakers select tannin types and dosage ranges more efficiently. Human sensory judgment will remain important, but data can improve consistency.

Bio-based adhesive development can also benefit from AI. Tannin resin performance depends on source, molecular structure, pH, curing chemistry and blending. Modeling can reduce trial cycles and help formulators design tannin-based systems with better bonding and lower formaldehyde reliance. Feed applications can use analytics to connect tannin dose, animal species, diet composition and performance outcomes. Better data can help suppliers provide more precise product recommendations. This will support premium positioning for standardized feed tannins.

Disruption Analysis

Bio-based materials are disrupting tannin demand by creating new industrial use cases beyond leather. Wood panel and insulation producers are evaluating tannins as renewable phenolic inputs. If performance and cost improve, tannins can capture value in adhesives and resins. Premium wine and beverage applications are shifting tannins from a corrective additive to a precision quality tool. Wineries increasingly select tannins based on grape variety, vintage condition and style objective. Enology tannin suppliers with strong technical guidance can capture premium margins.

Leather sustainability narratives are changing demand. Vegetable tanning is gaining attention in luxury goods and eco-positioned leather. However, chrome tanning remains cost-effective and fast. Tannin suppliers must position vegetable tanning as a premium value route rather than a direct commodity replacement. Supply scrutiny is also disruptive. Customers want traceable and sustainable plant materials. Suppliers that cannot demonstrate responsible sourcing may face procurement risk. Such pressure can favor larger and more documented suppliers.

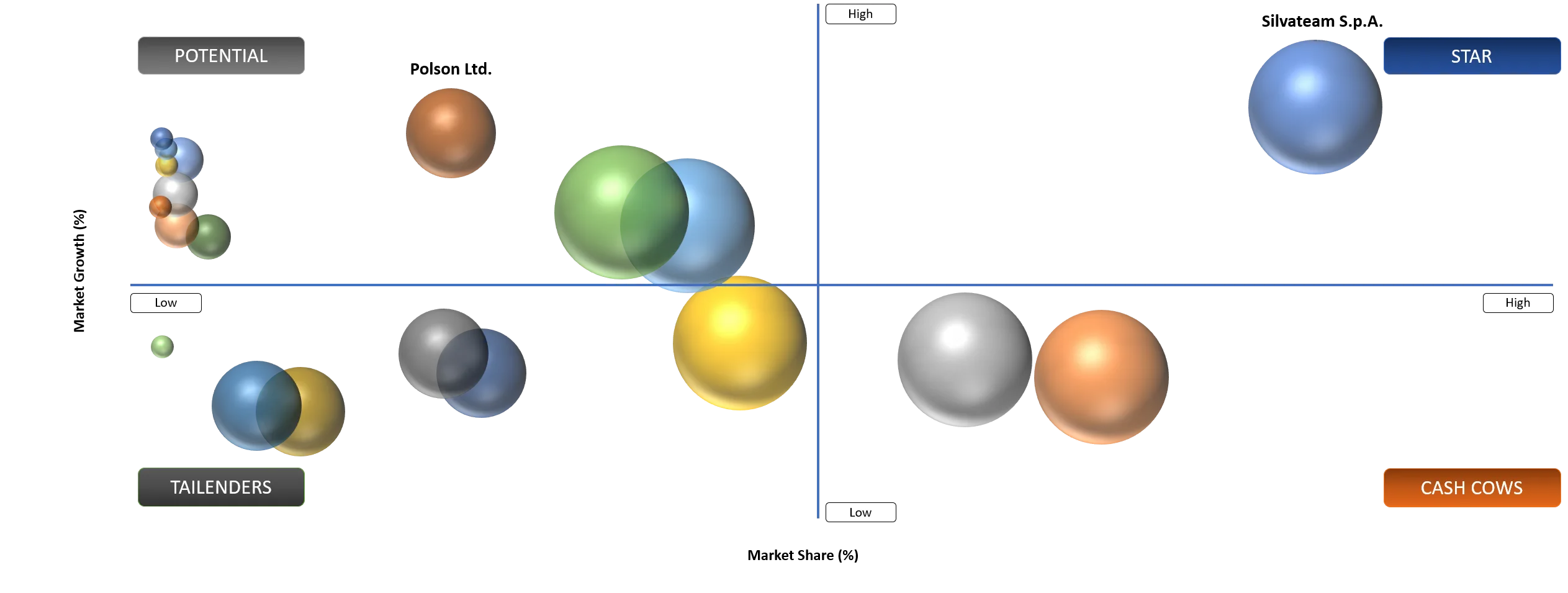

BCG Matrix: Company Evaluation

Star

Star players include Silvateam S.p.A., TANAC S.A., Unitán S.A.I.C.A., Laffort, Enartis, AEB Group S.p.A., Tannin Corporation and S.A. Ajinomoto OmniChem N.V. These companies have strong application coverage, recognized product portfolios, sourcing capability or technical depth across leather, wine, specialty extracts, industrial use and regulated applications.

Potential

Potential companies include Polson Ltd., Hubei Tianxin Biotech Co., Ltd. and Xi’an Sost Biotech Co., Ltd. Polson can gain share through food and industrial tannin supply in India. Hubei Tianxin and Xi’an Sost can grow through plant extract and nutraceutical ingredient demand, especially if they improve documentation, active content consistency and export compliance.

Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact | Demand Concentration | Impacted Use Case | Strategic Impact |

Leather Producers Increase Demand For Vegetable Tanning Inputs | High | Asia-Pacific, Europe and South America | Leather Tanning | Supports condensed tannin demand |

Wine Producers Use Tannins For Mouthfeel and Color Stability | Medium To High | Europe, North America and South America | Enology Tannins | Supports premium specialty grades |

Bio-Based Adhesives Need Phenol Replacement Materials | Medium | Europe, Asia-Pacific and North America | Wood Adhesives and Resins | Opens industrial growth route |

Animal Nutrition Customers Seek Plant Polyphenol Additives | Medium | Asia-Pacific and Europe | Feed Additives | Supports standardized tannin blends |

Driver: Leather Producers Increase Demand for Vegetable Tanning Inputs

Leather tanning remains the largest tannin demand base because vegetable extracts provide body, color and handle in specialty leather. Tanneries use quebracho, mimosa, chestnut and blended extracts to achieve specific leather properties. Premium leather goods, saddlery and artisanal leather categories support stable demand for vegetable tannins. Vegetable tanning also fits brand narratives around natural materials and heritage production. Luxury and craft leather producers use vegetable-tanned leather to differentiate from commodity chrome-tanned products. It does not mean chrome tanning will disappear, but it creates value pockets where tannins can command stronger margins.

Asia-Pacific supports volume demand because leather processing remains large across China, India and Southeast Asia. Europe supports premium demand through luxury leather and specialty applications. Suppliers that can provide consistent extract performance and technical support are better positioned. Tanneries need more than raw extract. They need solubility, penetration, color consistency, yield and blending support. Tannin producers with application laboratories and leather technicians can help buyers reduce process variation and improve finished leather quality.

Restraint Impact Analysis

| Restraint | Drag On Market Growth | Primary Impact Area | Impacted Use Case | Strategic Impact |

Raw Material Seasonality Raises Extract Supply Risk | High | Plant Extract Supply | Quebracho, Mimosa and Chestnut Tannins | Raises sourcing and price risk |

Chrome Tanning Cost Advantage Limits Leather Conversion | High | Leather Applications | Vegetable Tanning | Limits full replacement potential |

Food and Feed Documentation Requirements Slow New Supplier Approval | Medium | Specialty Grades | Food, Feed and Nutraceuticals | Raise compliance cost |

Forest Sourcing Scrutiny Increases Compliance Burden | Medium | Bulk Extracts | Leather and Industrial Tannins | Favors traceable suppliers |

Restraint: Raw Material Seasonality Raises Extract Supply Risk

Tannin production depends on plant raw materials that can vary by season, climate and sourcing region. Quebracho, mimosa, chestnut, tara, oak and gallnut supply chains face natural yield variation. Extract producers must manage these variations through blending, quality control and inventory planning. Seasonal variation can affect active content, color, solubility and extract yield. Leather buyers may adjust formulations, but food, wine and feed buyers have less tolerance for variation. Suppliers need stronger analytical controls when serving high-value applications.

Forest sourcing scrutiny can also limit supply flexibility. Customers want proof that raw materials are sourced responsibly. Suppliers that rely on poorly documented harvest chains may lose premium customers. Traceability is becoming a commercial requirement, not just a sustainability claim. Logistics disruptions add risk because tannin extracts often move across continents. Freight delays can affect tanneries and wineries with seasonal production windows. Suppliers with diversified sourcing and regional stock points can reduce buyer risk.

Segmentation Analysis

Condensed Tannins Will Continue to Dominate Bulk Demand

Condensed tannins will continue to dominate because quebracho and mimosa extracts are widely used in leather tanning and industrial applications. The tannins provide strong protein-binding behavior and are valued for body, fullness and color in leather. Bulk consumption remains tied to tannery production and industrial resin exploration. Quebracho tannins are especially important because they are well established in vegetable tanning. It supports leather firmness and reddish-brown tone, depending on processing and formulation. Tanneries often use blends to balance penetration and final leather feel.

Mimosa tannins are used where lighter color and specific tanning performance are required. Mimosa extract also has relevance in adhesives and industrial applications. Supply reliability depends on plantation management, extraction capacity and regional logistics. Condensed tannins also support bio-based adhesive development. Their phenolic structure makes them relevant for wood panel and resin applications. Commercial adoption depends on performance, consistency and cost competitiveness against synthetic phenolic systems.

Enology Tannins Are Creating Premium Specialty Demand

Enology tannins are a high-value specialty segment because wineries use them to manage structure, color, oxidation and sensory profile. Unlike leather tannins, wine tannins must meet strict quality and sensory requirements. Customers value technical guidance and brand trust. Wineries use tannins at different stages including fermentation, aging and finishing. The same tannin may not suit every grape variety or wine style. Suppliers need deep enology knowledge to recommend the right product and dosage. This creates service-led differentiation.

Europe, North America, South America and Australia are important enology markets. Premium wineries are more willing to pay for consistent and targeted tannin solutions. Demand can vary by vintage because grape quality and phenolic maturity change each season. Competition in enology tannins is based on performance and trust. Laffort, Enartis and AEB Group have strong positions because they serve wineries with broader processing portfolios. Tannin producers that lack enology support may struggle to enter premium wineries.

Food, Feed and Nutraceuticals Are Expanding Beyond Traditional Use

Food, feed and nutraceutical applications are growing because plant polyphenols are associated with natural antioxidant and functional positioning. Tannins can support products where natural origin and bioactivity matter. However, these applications require better documentation than leather tanning. Feed additives are gaining attention as producers look for plant-based tools to support gut health and reduce reliance on antibiotics. Tannin use must be carefully managed because dosage and animal species influence outcomes. Suppliers need technical evidence and safety data.

Nutraceutical buyers evaluate active content, purity, contaminant control and regulatory compliance. Grape seed, green tea, tara and gallnut-derived extracts can serve different product needs. Premium demand depends on standardized active compounds and transparent sourcing. Food and feed applications are not simple volume markets. Customers require documentation, specification stability and application support. Suppliers moving from industrial tannins into regulated uses need stronger quality systems.

Geographical Penetration

Asia-Pacific Tannin Market Trends

The Asia-Pacific region is the fastest-growing with 5.6% CAGR between 2026 and 2035. Growth is supported by leather processing, feed additives, food ingredients, nutraceuticals and plant extract manufacturing. China is a major demand center for leather, food ingredients, nutraceuticals and specialty plant extracts. Local suppliers compete strongly in plant extracts, while imported tannins are used where performance or source specificity matters. Demand growth depends on higher-value applications and export-grade documentation.

India is important due to leather, pharmaceuticals, nutraceuticals and food processing. Tanneries use vegetable tannins in selected leather categories, while nutraceutical suppliers support growing domestic and export demand. Polson and regional ingredient suppliers have opportunities if they meet quality and documentation requirements. Japan and South Korea are high value but smaller markets. Customers prioritize quality, traceability and safety. Nutraceuticals, beverages, cosmetics and specialty ingredients are more important than bulk leather demand. Suppliers with documented purity and stable specifications can gain traction.

Europe Tannin Market Outlook

Europe remains a high-value tannin market because wine, luxury leather, bio-based materials and specialty ingredients are strong. France, Italy and Spain are especially important due to wine and leather. Germany supports industrial and bio-based material development. Wine tannins are a key European value driver. Wineries use tannins for structure, mouthfeel, color and oxidation management. Enology suppliers compete through technical support and winemaker trust. Demand varies by vintage and wine style.

Vegetable leather tanning is linked to premium goods and heritage manufacturing. Italian and French leather industries use tannins where natural leather positioning matters. Chrome tanning remains common, but vegetable tanning holds value in premium categories. Europe also supports tannin-based resin innovation. Bio-based adhesives and phenol replacement programs align with sustainability goals. Commercialization depends on cost and performance, but Europe is likely to remain an important development region.

U.S. Tannin Market Landscape

The U.S. tannin market is led by wine, food ingredients, nutraceuticals, animal feed and specialty industrial uses. Leather is less dominant than in Asia-Pacific, but premium leather and craft production support selected demand. Customers place strong emphasis on documentation and supplier reliability. Wine tannins are important in California, Oregon, Washington and other wine regions. Wineries use tannins to manage structure, mouthfeel and color stability. Enology suppliers with strong technical teams and local distribution have an advantage.

Nutraceuticals and food ingredients are strong growth areas. Plant polyphenols fit clean-label and natural antioxidant positioning. Suppliers need strong safety, purity and traceability documentation to serve U.S. buyers. Animal feed additives also support demand. Producers are exploring plant-based additives for gut health and production efficiency. Tannin suppliers must provide clear technical guidance because performance can vary by diet and animal species.

India Tannin Market Growth

India combines leather demand, nutraceutical production, plant extract manufacturing and food ingredient growth. Tanneries remain an important demand base, but premium and export-oriented applications are becoming more attractive. Vegetable tanning is valued in specialty leather and branded natural leather categories. India’s nutraceutical and herbal extract industry creates opportunities for tannin-rich extracts. Export-oriented producers need stronger documentation, active content control and contaminant testing. Suppliers that support international compliance can command better pricing.

Animal feed demand is also developing. Poultry, dairy and aquaculture producers are looking at plant-based additives for performance and health positioning. Tannin adoption will depend on evidence, formulation support and price. Indian buyers remain cost-sensitive in bulk applications. Local suppliers can compete on price, while imported specialty tannins need clear performance benefits. Technical service will be important for premium adoption.

Competitive Landscape

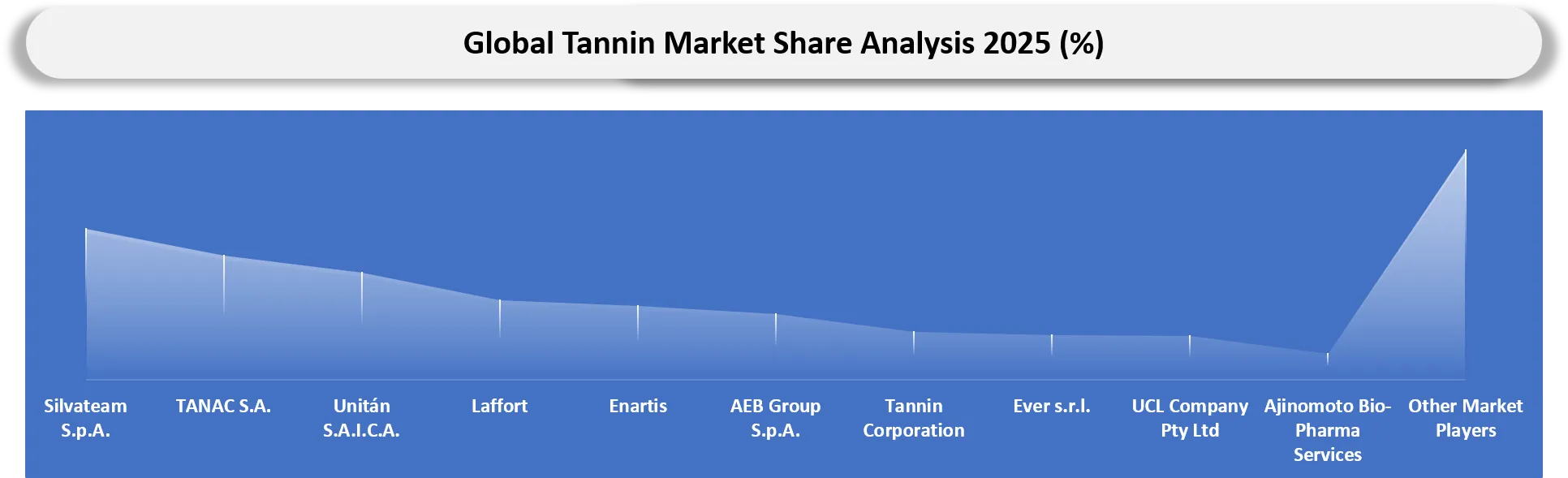

- Competition is split between bulk vegetable extract producers, enology suppliers, specialty plant extract companies, chemical ingredient suppliers and regional distributors. Silvateam, TANAC and Unitán are important in vegetable tannins, while Laffort, Enartis and AEB Group are stronger in wine-focused tannins.

- Bulk tannin competition depends on source access, extraction efficiency, active content and cost. Quebracho, mimosa and chestnut producers compete on supply reliability and performance consistency. Tanneries require stable product quality and technical support.

- Enology tannin competition is service led. Wineries need product guidance, sensory credibility and vintage-specific recommendations. Strong enology brands can defend pricing because purchase decisions are tied to wine quality.

- Food, feed and nutraceutical competition depends on documentation and regulatory readiness. Plant extract suppliers must prove purity, safety and active content. Companies that only serve leather may struggle to enter regulated applications without upgraded quality systems.

- Competitive benchmarking should track source security, extract standardization, application expertise, documentation, sustainability claims, regional inventory and customer technical support.

Key Companies

- Silvateam S.p.A.

- TANAC S.A.

- Unitán S.A.I.C.A.

- Laffort

- Enartis

- AEB Group S.p.A.

- Tannin Corporation

- Ever s.r.l.

- UCL Company Pty Ltd

- Ajinomoto Bio-Pharma Services

- Polson Ltd.

- W. Ulrich GmbH

- Jyoti Dye Chem Agency

- Forestal Mimosa Ltd.

- Mimosa Central Co-operative Ltd.

- S.A. Ajinomoto OmniChem N.V.

- Hubei Tianxin Biotech Co., Ltd.

- Zhushan County Tianxin Medical and Chemical Co., Ltd.

- Hangzhou Qinyuan Natural Plant High-Tech Co., Ltd.

- Xi’an Sost Biotech Co., Ltd.

Company Coverage Preview

Silvateam S.p.A. is one of the most important tannin suppliers due to its presence in chestnut, quebracho, tara and specialty plant extracts. The company is relevant across leather, wine, animal nutrition, food and industrial applications. Its advantage comes from broad source coverage, extraction capability and application knowledge across both bulk and specialty tannin markets.

TANAC S.A. and Unitán S.A.I.C.A. are important in vegetable tannin supply because South American quebracho and mimosa resources remain central to condensed tannin supply. These companies are relevant for leather tanning, wood adhesives and industrial applications where bulk extract consistency and sourcing security matter.

Laffort, Enartis and AEB Group are important in enology tannins. Their role is not only extract supply but also wine application support. Wineries need guidance on mouthfeel, color stabilization, oxidation control and sensory profile. Enology suppliers gain trust through technical service and winemaker relationships.

Major Pain Points

- Plant raw material variation can affect tannin active content, color and solubility.

- Forest sourcing scrutiny increases documentation requirements.

- Chrome tanning remains cheaper and faster than vegetable tanning in many leather applications.

- Enology tannins require sensory validation and strong technical support.

- Feed and nutraceutical applications require tighter safety and purity documentation.

- Freight delays can affect seasonal wine and leather production windows.

- Bulk tannin pricing is exposed to harvest yield and extraction cost.

- Bio-based adhesive adoption depends on resin performance and curing economics.

- Small suppliers may lack compliance systems for food and feed markets.

- Regional customers often require local inventory and technical service.

Recent Developments

- March 2026: Laffort expanded its enology communication around tannin selection and wine structure management, reinforcing premium demand for application-specific wine tannins.

- January 2026: Enartis continued promoting enological tannins for color stabilization, antioxidant protection and sensory refinement in wine production.

- September 2025: Silvateam continued expanding specialty plant extract positioning across leather, food, feed and industrial applications, supporting higher-value tannin demand.

- July 2025: TANAC continued emphasizing sustainable plantation-based tannin supply, supporting buyer interest in traceable vegetable extracts.

Analyst Insights

DataM Intelligence views the tannin market as a specialty extract market moving steadily beyond its leather heritage. Leather tanning will remain an important volume base but the best value creation will come from wine, feed, nutraceuticals and bio-based resins. Condensed tannins will retain leadership because quebracho and mimosa remain deeply embedded in vegetable leather and industrial uses. Hydrolysable tannins should gain greater commercial attention because chestnut, tara, oak and gallnut sources align better with premium wine, food and wellness positioning.

Supplier differentiation will increasingly depend on traceability, active content standardization and application support. Customers are no longer satisfied with broad natural-origin claims. They want proof of source, stable specifications and reliable technical guidance. Forest sourcing scrutiny will strengthen this requirement because premium brands and regulated customers need credible documentation. Enology suppliers will defend margins through sensory credibility while feed and nutraceutical suppliers will need stronger evidence around safety, dosage and functional performance.

Asia-Pacific will remain the most important growth region because leather processing, food manufacturing, plant extract production and animal nutrition are expanding together. Europe will stay a premium-value market because wine, luxury leather and bio-based material research create demand for higher specification products. Suppliers that invest in extraction control, blending technology, responsible sourcing and local technical service will capture better contracts. Suppliers focused only on low-cost bulk extract sales may remain relevant but will face weaker pricing power through 2035.

Target Audience

| Industry | Who Should Buy This Report? | Reason To Buy This Report |

| Tanneries | Procurement Managers, Technical Teams, Leather Chemists | Evaluate vegetable tannin sourcing, pricing and performance |

| Wine and Beverage Producers | Winemakers, Enology Teams, Procurement Teams | Understand tannin demand for structure, color and oxidation management |

| Feed Additive Producers | Product Managers, Nutritionists | Assess plant polyphenol demand and formulation opportunities |

| Wood Adhesive Manufacturers | Research Teams, Sustainability Leaders | Evaluate tannin-based phenolic replacement potential |

| Nutraceutical Companies | Ingredient Sourcing Teams, Product Developers | Track standardized tannin and plant polyphenol demand |

| Pharmaceutical and Personal Care Companies | Formulation Teams, Sourcing Teams | Assess specialty tannin ingredient opportunities |

| Investors | Specialty Chemical Investors, Natural Ingredient Funds | Identify growth pockets beyond leather tanning |

| Consulting Firms | Chemicals and Ingredients Teams | Support market entry, partner mapping and product strategy |

What DataM Uniquely Provides:

- DataM maps tannin demand by product type, source, form, application, end-user and region.

- DataM separates bulk leather tannins from premium enology, feed, nutraceutical and industrial resin applications.

- DataM evaluates source-specific demand across quebracho, mimosa, chestnut, tara, oak, gallnut, grape seed and green tea.

- DataM benchmarks suppliers by raw material control, application support, documentation and regional reach.

- DataM tracks bio-based adhesive opportunities and phenol replacement potential.

- DataM includes procurement-risk mapping for seasonality, forest sourcing, extract variation and regulatory documentation.

- DataM provides trade intelligence for vegetable tanning extracts, plant extracts and tannic acid proxies.

- DataM supports buyer decisions across tanneries, wineries, feed producers, nutraceutical firms and bio-based material developers.