Typhoid Fever Market Size & Industry Outlook

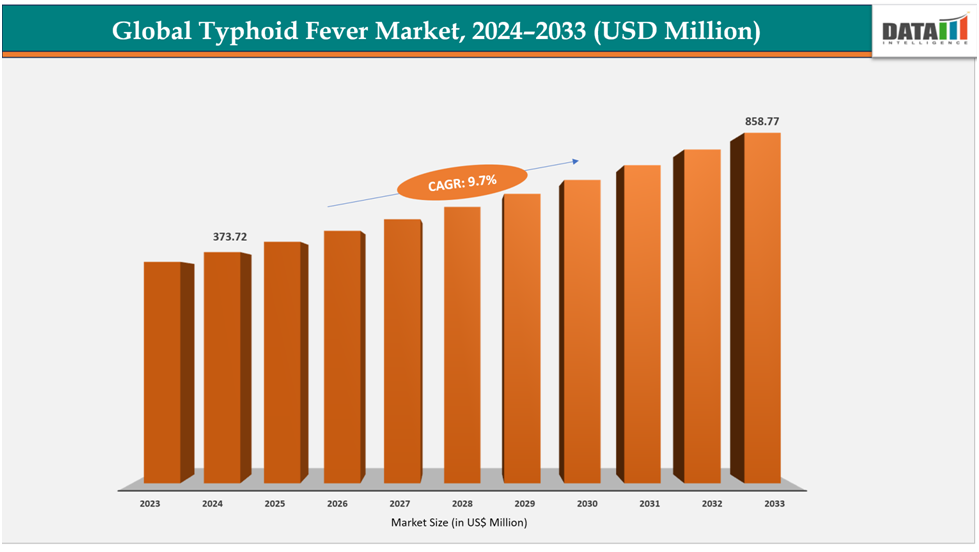

The global typhoid fever market size reached US$ 342.86Million with a rise of US$373.72Million in 2024 and is expected to reach US$ 858.77Million by 2033, growing at a CAGR of 9.7% during the forecast period 2025-2033.

Rising incidence of typhoid fever in urban slums and peri-urban regions is a major driver of market growth. These areas often face poor sanitation, unsafe water, and overcrowding, which accelerate transmission of Salmonella Typhi. Investments in typhoid prevention and treatment are increased by governments, non-governmental organizations, and donors as the disease burden rises. Rapid diagnostics, antibiotics, especially second-line treatments for resistant strains, and Typhoid Conjugate Vaccines (TCVs) are all in high demand as a result. International funding is being used to assist the growing focus of vaccination campaigns and surveillance operations on high-risk urban populations. Therefore, the worldwide typhoid fever market is directly driven by the rising prevalence in slum communities.

Key Highlights

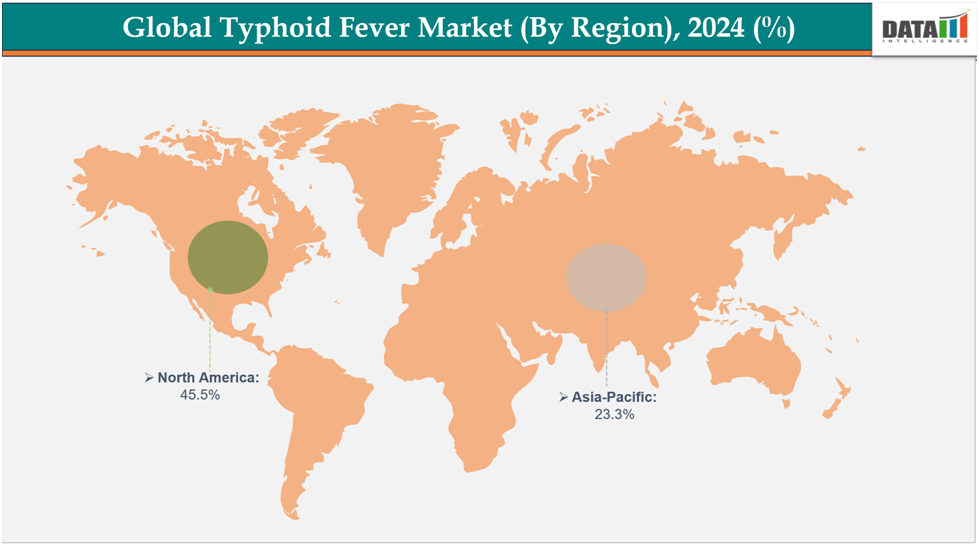

- North America dominates the typhoid fever market with the largest revenue share of 45.5% in 2024.

- The Asia Pacific is the fastest-growing region and is expected to grow and it is holding 23.3% market share in 2024.

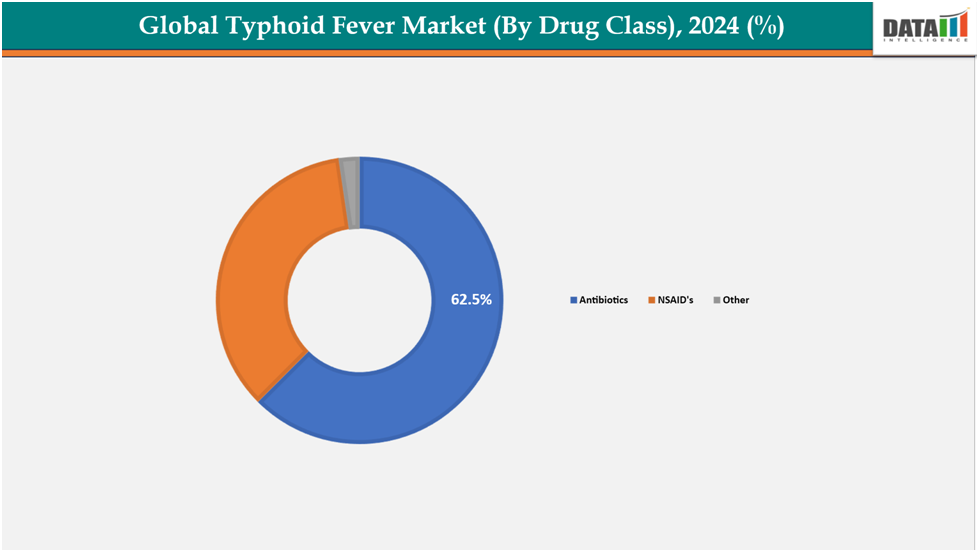

- Based on drug class, the antibiotics segment led the market with the largest revenue share of 62.5% in 2024.

- Top companies in the typhoid fever market include Pfizer Inc., F. Hoffmann-La Roche Ltd, Bayer AG, DAIICHI SANKYO COMPANY, LIMITED, GSK plc., AstraZeneca, Merck & Co., Inc., AbbVie Inc., Sanofi, and Johnson &Johnson, among others.

Typhoid Fever Market Dynamics

Drivers: Growing awareness of antimicrobial-resistant s. typhi is significantly driving the typhoid fever market growth

Growing awareness of antimicrobial-resistant Salmonella Typhi is significantly driving the typhoid fever market. Adoption of advanced antibiotics has increased as a result of the need for newer, more potent therapies brought on by resistance to conventional antibiotics. The diagnostic market is also being driven by the requirement for quick and precise diagnostics in order to identify resistant strains. Antibiotic dependence has decreased as a result of increased vaccination campaigns and new medication development against AMR, especially with the introduction of more recent typhoid conjugate vaccines.

For instance, in July 2025, the CDC reported the emergence of ceftriaxone-resistant Salmonella enterica serovar Typhi in Bangladesh. The isolates belonged to genotype 4.3.1.2 and carried the blaCTX-M-15 gene on the pCROB1 plasmid. This genotype-plasmid lineage represented a recent introduction, highlighting the need for strengthened surveillance, enhanced antimicrobial stewardship, and expanded vaccination strategies.

Restraints: The high cost of treatment is hampering the growth of the typhoid fever market

High treatment costs are restraining the growth of the typhoid fever market. Antibiotics and newer typhoid conjugate vaccines, though effective, are often expensive, limiting access in low- and middle-income countries where the disease burden is highest. Many patients rely on out-of-pocket payments, and limited insurance coverage further reduces affordability. High costs also discourage mass vaccination campaigns and lower adoption rates, particularly in rural and underserved areas. For pharmaceutical companies, expensive treatments restrict sales volumes and reduce incentives for further investment in R&D.

For instance, the high cost of typhoid treatments and vaccines limits access, especially in low- and middle-income countries with high disease burdens. Inpatient treatment can range from $201 to $976 per case, while typhoid conjugate vaccines cost $1.39 per dose, rising to $2.37 including delivery and administration.

For more details on this report, see Request for Sample

Typhoid Fever Market Segmentation Analysis

The global typhoid fever market is segmented based on drug class, route of administration, distribution channel, and region.

Drug Class:

The antibiotics segment from drug class is dominating the typhoid fever market with a 62.5% share in 2024

The antibiotics segment dominates the typhoid fever market because they are the primary and most effective treatment against Salmonella Typhi, the bacterial cause of the disease. According to WHO and CDC clinical guidelines, antibiotics should be used as first-line treatment, whilst NSAIDs and other medication groups simply relieve symptoms. The need for novel, broad-spectrum antibiotics has increased due to an increase in incidence of antimicrobial-resistant bacteria. Recurrent infections in endemic areas further encourage use. Antibiotics are essential since supportive therapies are unable to reverse the condition. They continue to be the largest and most lucrative section of the typhoid market due to their quick efficacy, high prescription rates, and crucial role in managing resistance.

For instance, in June 2025, Cornell researchers identified rifampin, an antibiotic that proved 99.9% effective against Salmonella Typhi, the bacterium responsible for typhoid fever. The researchers also predicted that rifampin could be effective against other life-threatening bacterial infections, including pneumonia and meningitis.

The intravenous route segment is estimated to have a 65.6% of the typhoid fever market share in 2024

The intravenous (IV) route segment dominated the typhoid fever market because it allowed rapid and direct delivery of antibiotics into the bloodstream, ensuring faster therapeutic effects, particularly in severe or complicated cases. IV administration was preferred in hospitals for patients with high fever, dehydration, or resistance to oral medications, as it guaranteed better bioavailability and consistent drug levels. Additionally, critically ill patients often required hospitalization, further increasing the use of IV antibiotics. Compared to oral or other routes, the IV segment generated higher market demand and revenue.

Typhoid Fever Market Geographical Analysis

North America is expected to dominate the global typhoid fever market with 45.5% in 2024

North America is expected to dominate the Global Typhoid Fever Market due to high awareness of oral health, advanced dental infrastructure, and widespread insurance coverage. A high prevalence of gum disease, aging populations, and risk factors like smoking and diabetes further drive demand. Strong R&D, frequent product innovations, and regulatory support boost market growth. Higher disposable incomes and willingness to spend on oral care strengthen this dominance, with the U.S. holding the largest share and projected steady growth in the coming years.

Europe is the second region after North America, which is expected to dominate the global typhoid fever market with 32.5% in 2024

Europe is emerging as a key market for typhoid fever treatment, second only to Asia-Pacific, supported by its strong healthcare infrastructure, advanced diagnostic capabilities, and access to broad-spectrum antibiotics such as azithromycin, ceftriaxone, and ciprofloxacin. Although typhoid fever incidence in Europe is relatively low compared to endemic regions, rising cases among international travelers, migrants, and returning expatriates are driving steady demand for effective treatment options across hospitals and travel clinics.

The region is witnessing notable government and institutional initiatives to prevent and manage typhoid outbreaks. To improve reporting and treatment compliance, organizations like the European Centre for Disease Prevention and Control (ECDC) keep a close eye on imported cases, provide revised guidelines, and work with member states. In order to ensure prompt detection and focused treatment, hospitals and public health organizations in Germany, the UK, France, and Italy are in the forefront of the implementation of modern diagnostic tests.

For instance, a 2025 joint EFSA‑ECDC report highlighted persistently high resistance of Salmonella to key antibiotics, including fluoroquinolones, in humans and animals across Europe. This underscores the urgent need for “One Health” surveillance and prudent antibiotic use, as rising resistance threatens the effectiveness of traditional typhoid treatments.

The Asia Pacific region is the fastest-growing region in the global typhoid fever market, with 23.3% market share in 2024.

Asia-Pacific is projected to be the fastest-growing region in the typhoid fever treatment market, driven by the high disease burden and increasing awareness of prevention and early treatment. Typhoid fever is most common in countries like Bangladesh, Pakistan, and India, which increases need for efficient antibiotics and better access to healthcare. While continuous investments in healthcare facilities, diagnostic capabilities, and antimicrobial stewardship programs are expanding treatment access and market growth potential throughout the region, poor sanitation, congested urban environments, and gaps in clean water infrastructure make transmission worse.

Governments and healthcare providers in Asia-Pacific are increasingly investing in digital health and telemedicine initiatives to improve the diagnosis, administration, and monitoring of typhoid fever treatments, particularly in rural and underserved regions. For instance, in October 2025, India launched its National Disease Control Campaign, a month-long initiative in Varanasi targeting typhoid, dengue, malaria, and other illnesses. The concurrent 'Dastak' program focused on household screening for fever and chronic diseases, with Anganwadi workers and ASHAs playing a central role in awareness, prevention, and patient identification.

Competitive Landscape

Top companies in the typhoid fever market include Pfizer Inc., F. Hoffmann-La Roche Ltd, Bayer AG, DAIICHI SANKYO COMPANY, LIMITED,GSK plc., AstraZeneca, Merck & Co., Inc., AbbVie Inc., Sanofi, and Johnson &Johnson, among others.

Pfizer Inc.: Pfizer Inc. is a leading global pharmaceutical and biotechnology company headquartered in New York. Founded in 1849, it develops medicines and vaccines across various therapeutic areas. With operations in over 200 countries, Pfizer emphasizes innovation, strong R&D, and a diverse product portfolio, including vaccines, oncology, and anti-infective treatments.

Market Scope

| Metrics | Details | |

| CAGR | 9.7% | |

| Market Size Available for Years | 2022-2033 | |

| Estimation Forecast Period | 2025-2033 | |

| Revenue Units | Value (US$ Mn) | |

| Segments Covered | Drug Class | Antibiotics, NSAIDs, and Others |

| Route of Administration | Intravenous, Others | |

| End User | Hospital Pharmacies, Retail Pharmacies, Online Pharmacies | |

| Regions Covered | North America, Europe, Asia-Pacific, South America and the Middle East & Africa | |

The Global Typhoid Fever Market report delivers a detailed analysis with 62 key tables, more than 51 visually impactful figures, and 159 pages of expert insights, providing a complete view of the market landscape.