Red Mud (Bauxite Residue) Market Overview

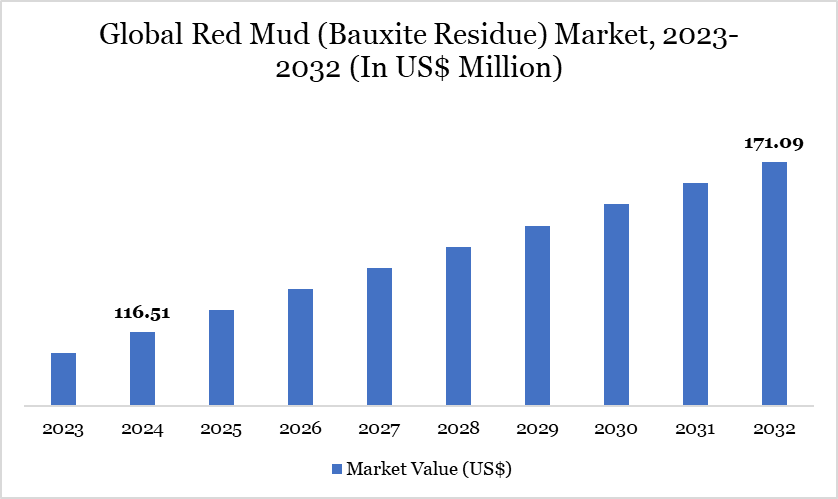

Red Mud (Bauxite Residue) Market reached US$ 116.51 million in 2024 and is expected to reach US$ 171.09 million by 2032, growing with a CAGR of 4.92% during the forecast period 2025-2032.

Red mud, also known as bauxite residue, is an industrial waste generated during the extraction of alumina from bauxite using the Bayer process. For every ton of alumina produced, approximately 1.5 tons of red mud is generated. Traditionally considered an environmental hazard due to its high alkalinity and heavy metal content, red mud is increasingly being viewed as a valuable secondary resource. This has led to a rise in red mud valorization projects, supported by advancements in separation technologies and a growing demand for sustainable raw materials in various downstream industries.

One of the primary driving factors is the increasing demand for sustainable construction materials. Red mud’s chemical properties make it a suitable raw material substitute in cement, bricks, and concrete production. For instance, in 2021, Alcoa has a goal to reduce bauxite residue land requirements per metric ton of alumina produced by 15 percent by 2030, from a 2015 baseline. Alcoa is a founding member of the four-year ReActiv project, which is seeking to transform bauxite residue into a reactive material suitable for new cement products that have a low carbon dioxide footprint.

Key Takeaways

- Secondary-resource economics are improving as refiners and governments prioritize critical minerals and circular industrial systems. Within the red mud (bauxite residue) market, that signal should shape product strategy, pricing discipline, and investment priorities.

- Commercialization is still pilot-led; the biggest winners are likely to be process owners that can prove both environmental compliance and offtake quality. Competitive advantage in the red mud (bauxite residue) market will increasingly go to companies that operationalize the insight better than peers.

- Partnerships between refiners, labs and specialty processors matter more than standalone technology claims at this stage. Capital allocation, partnerships, and go-to-market execution in the red mud (bauxite residue) market are likely to follow the same logic over the forecast period.

- Market sizing varies materially by scope; broad residue-management and narrower recovery-solution estimates should not be treated as identical. Longer-term winners in the red mud (bauxite residue) market usually turn that takeaway into repeatable execution rather than one-off launches.

Red Mud (Bauxite Residue) Market Trend

The red mud processing market is witnessing several emerging trends, driven by technological breakthroughs, regulatory shifts, and industry collaborations. One of the most prominent trends is the shift from disposal to resource recovery. Companies are increasingly treating red mud not as a waste, but as a potential Product of raw materials.

For instance, NALCO in India and Hydro's Alunorte refinery in Brazil are actively working on extracting valuable elements like iron, alumina, titanium, and rare earth elements (REEs) from red mud using acid leaching and other advanced processes. This trend is gaining traction as countries seek to secure their supply chains for critical minerals.

For more details on this report – Request for Sample

Market Scope

Metrics | Details |

By Product | Low-Iron Red Mud, High-Iron Red Mud, Others |

By Production Process | Bayer Process, Sintering Process, Others |

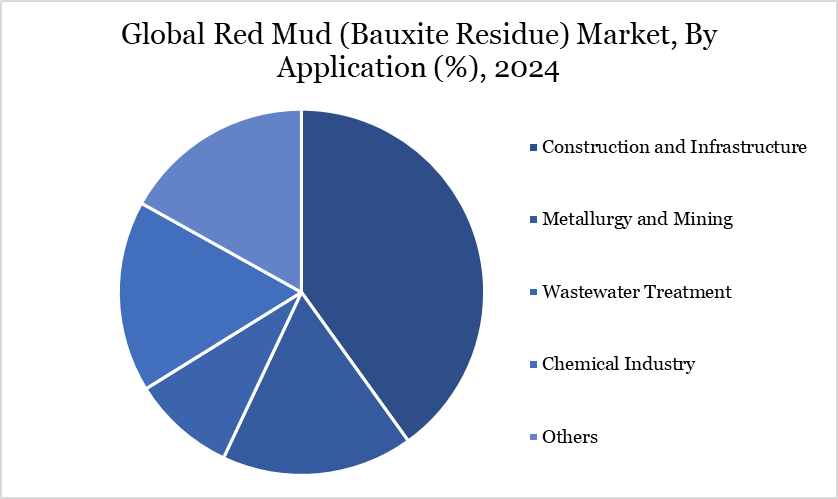

By Application | Construction and Infrastructure, Metallurgy and Mining, Wastewater Treatment, Chemical Industry, Others |

By Region | North America, South America, Europe, Asia-Pacific, Middle East and Africa |

Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth |

Red Mud (Bauxite Residue) Market Dynamics

Drivers: Critical-mineral recovery

Critical-mineral recovery remains the strongest growth driver in the red mud (bauxite residue) market because scandium, gallium, rare earths and iron recovery projects are moving residue economics from disposal-cost minimization toward resource monetization. Demand expands fastest when buyers can tie that catalyst to measurable gains in speed, compliance, operating efficiency, or customer experience.

Channel strategy also benefits when the leading catalyst solves a visible problem for end users rather than adding a marginal feature. Buyers tend to favor vendors that can document the operational gain in plain commercial terms.

Strategic momentum broadens further when critical-mineral recovery is supported by decarbonization pressure and industrial offtake formation. Companies that package the main catalyst with reliable execution and proof of performance are more likely to capture market share during the forecast period.

Restraints: Chemistry variability

Chemistry variability remains the most material restraint in the red mud (bauxite residue) market because residue composition varies by ore source and refining route, making standardized downstream processing difficult at scale. Adoption slows when the issue raises qualification risk, lengthens decision cycles, or weakens confidence in long-term economics.

Margin pressure can intensify even in a healthy market outlook when remediation costs are high. Procurement teams usually favor suppliers that can show tighter controls, steadier quality, and better risk visibility.

Secondary friction from capex and process complexity and regulatory/permitting friction can magnify the problem by adding more cost and complexity. Vendors that solve the primary restraint faster than peers usually protect pricing and strengthen enterprise trust.

How AI Impacted Market

Process optimization is influencing the red mud (bauxite residue) market in a material way. AI is being used to optimize leaching conditions, mineral separation routes and reagent consumption in pilot-scale valorization programs which reduces trial-and-error cost and shortens development or engineering cycles.

Predictive control is influencing the red mud (bauxite residue) market in a material way. Digital twins and ML models improve residue pond monitoring, moisture forecasting, and stability management in tailings-style storage systems while helping companies lower waste, improve inventory turns, and react faster to demand volatility.

Resource targeting is influencing the red mud (bauxite residue) market in a material way. AI-assisted geometallurgy helps refiners classify residue streams and prioritize the highest-value recovery pathways which improves speed, consistency, and visibility across high-value operating decisions.

Disruption Analysis

From waste to feedstock is a major disruption theme in the red mud (bauxite residue) market. The market is being disrupted by the view of red mud as a source of strategic minerals rather than a pure disposal problem which pushes competition toward vendors that combine product performance with services, data, and execution quality, and leadership in the red mud (bauxite residue) market will increasingly depend on how well companies operationalize the shift rather than merely describe it.

Hybrid business models are a major disruption theme in the red mud (bauxite residue) market. Projects increasingly combine environmental services, metals recovery and building-material applications to improve project IRR which pushes competition toward vendors that combine product performance with services, data, and execution quality, and suppliers that adapt early can capture share while slower competitors remain tied to legacy pricing and delivery models in the red mud (bauxite residue) market.

Policy-linked value creation is a major disruption theme in the red mud (bauxite residue) market. Circular-economy, critical-mineral and industrial-waste policies are converging, giving residue valorization stronger strategic relevance which pushes competition toward vendors that combine product performance with services, data, and execution quality, and strategic winners usually emerge when management teams translate disruption into product redesign, channel change, and faster capital allocation in the red mud (bauxite residue) market.

Red Mud (Bauxite Residue) Market Segmentation Analysis

The global red mud (bauxite residue) market is segmented based on product, production process, application, and region.

Rising Adoption of Red Mud in the Construction and Infrastructure Sector

The construction and infrastructure sector holds a significant share in the red mud (bauxite residue) market due to its ability to utilize large volumes of this industrial by-product as a raw material. In January 2025, Shailesh Kumar Agarwal, Executive Director of the Building Materials and Technology Promotion Council under MoHUA, India, stated that India's construction sector is experiencing rapid growth and is projected to reach a value of US$1.4 trillion by 2047.

This growing sector enhances the market potential for red mud by integrating it into high-demand infrastructure applications. The expansion of India's construction industry is, therefore, directly contributing to the increased use of red mud in building materials. Red mud is increasingly being used as a substitute for conventional materials like clay, sand and laterite in cement and brick manufacturing. Its high content of iron oxide, alumina and silica makes it suitable for producing construction-grade materials, helping reduce reliance on natural resources.

Cement manufacturers, especially in regions like India and China, are integrating red mud into clinker production, contributing to cost efficiency and lower carbon emissions. For instance, red mud can replace up to 20% of cement in concrete mixes, enhancing sustainability without compromising structural integrity.

Red Mud (Bauxite Residue) Market Geographical Share

APAC Dominates the Red Mud (Bauxite Residue) Market with Robust Infrastructure and Industrial Demand

The Asia-Pacific region holds a significant share in the Red Mud (Bauxite Residue) Market due to its dominant role in global bauxite production, with countries like China, India and Australia being major players in the mining and refining industries. These countries produce a substantial volume of bauxite, a key raw material for aluminum production, resulting in a considerable amount of red mud as a byproduct.

In August 2020, Hindalco Industries signed a Memorandum of Understanding (MoU) with UltraTech Cement to deliver 1.2 million metric tonnes of red mud annually to UltraTech’s 14 plants across seven states. This initiative marks a significant step in sustainability, as red mud, a byproduct of alumina manufacturing, will be used as a replacement for mined minerals in cement production.

China, as the largest aluminum producer in the world, generates vast quantities of red mud, contributing significantly to the regional market. India, with its rapidly growing aluminum industry, also plays a pivotal role in the market's expansion. Moreover, Australia, a leading bauxite exporter, adds to the growing production of red mud.

Sustainability Analysis

The utilization of red mud (bauxite residue) aligns strongly with global sustainability goals, particularly in promoting circular economy practices, reducing industrial waste, and conserving natural resources. Traditionally regarded as an environmental burden due to its high alkalinity and potential toxicity, red mud is now being reclassified as a valuable secondary raw material.

Its integration into sectors like construction, cement, and ceramics helps reduce dependence on non-renewable materials such as clay, limestone, and sand, which are heavily extracted and energy-intensive. For instance, using red mud in cement production can lower carbon emissions by reducing clinker content, which is a significant source of CO₂ in the cement industry. Furthermore, red mud’s reuse prevents the long-term environmental risks associated with its landfilling, such as groundwater contamination and land degradation.

Red Mud (Bauxite Residue) Market Major Players

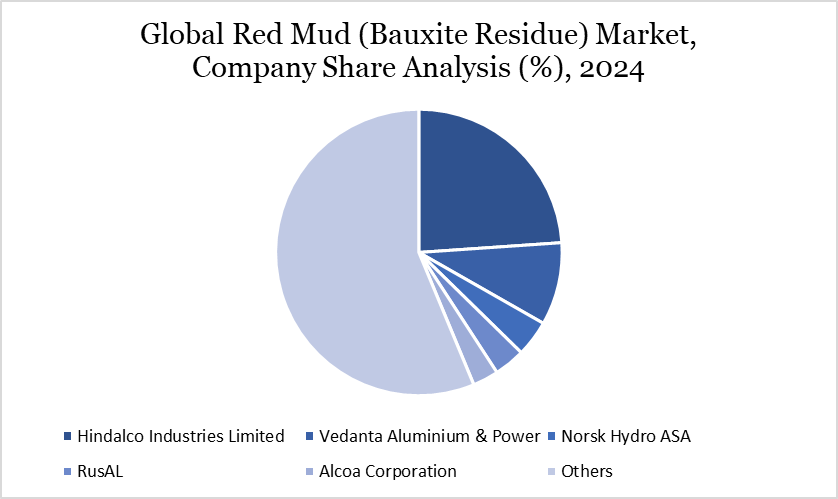

The major global players in the market include Hindalco Industries Limited, Vedanta Aluminium & Power, Norsk Hydro ASA, RusAL, Alcoa Corporation, Alum Tulcea, Rio Tinto Group, National Aluminium Company Limited (NALCO), South32 Limited, Enervoxa and among others.

Mergers and Acquisitions:

- Direct pure-play M&A remains limited; the market is still dominated by pilots, JVs, technology licensing and strategic funding.

- 2025–2026 activity was more partnership-led than acquisition-led, with refiners preferring staged technology de-risking before larger transactions.

- Where deal activity occurs, it is typically embedded in broader aluminum, critical-minerals or industrial-waste portfolios rather than stand-alone red-mud platforms.

Key Developments:

- Jan 2026: NALCO signed technology-development partnerships with CSIR-IMMT and CSIR-NML to recover alumina, scandium, lithium and other values from red mud.

- Dec 2025: Metallium and ElementUSA announced a USD 10 million agreement tied to gallium and scandium recovery from red mud at Gramercy, Louisiana.

- Apr 2025: Rio Tinto and The University of Queensland advanced work to transform bauxite residue into soil and other higher-value applications.

Technological Upgradation

- 2026: NALCO/CSIR programs highlighted process-upgrade work aimed at scaling red-mud recovery beyond bench studies.

- 2025: Vedanta Aluminium and MTM Critical Metals advanced reprocessing work using flash Joule heating concepts for residue treatment.

- 2025: refiners and research groups expanded digital monitoring and beneficiation workflows to improve residue classification and recovery yields.

Key Growth Factors

- Critical-mineral monetization: scandium, gallium, iron and rare-earth recovery is turning residue into a strategic asset class.

- Compliance-cost reduction: refiners want lower long-tail storage risk, lower remediation exposure and stronger ESG positioning.

- Construction-material substitution: demand for lower-carbon binders and fillers is opening selective routes for residue-derived materials.

Advanced Technologies

- Selective hydrometallurgical recovery systems for scandium, gallium and iron from alkaline residue streams.

- AI-assisted residue characterization and digital-twin monitoring for storage ponds and valorization plants.

- Stabilization chemistries and engineered binders that improve transportability and downstream reuse safety.

What's Trending

- Critical-mineral narrative: red mud is increasingly framed as a strategic minerals source linked to Western supply-security goals.

- Pilot-to-commercial transition: the market is moving from lab validation toward demonstration plants, but scale-up discipline remains decisive.

- Cross-industry circularity: construction materials, specialty chemicals and metals players are becoming more active around residue reuse.

Geopolitical Impact

Supply security is making red-mud valorization more strategic. Countries seeking scandium, gallium and other specialty inputs want non-Chinese supply options, while alumina-producing jurisdictions want to reduce long-lived residue liabilities. Trade frictions, permitting expectations and industrial-policy incentives now influence where pilot plants and recovery facilities are likely to scale first.

Why Choose DataM?

Data-Driven Insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. This approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. This personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. These insights complement and go beyond what is typically available in generic databases.

Target Audience 2026

Manufacturers/ Buyers

Industry Investors/Investment Bankers

Research Professionals

Emerging Companies