Radiology Market Size

The Radiology Market Size was reached US$ 37.28 billion in 2025 and is expected to reach US$ 83.42 billion in 2033, growing at a CAGR of 11.2% during the forecast period (2026-2033).

The radiology market has experienced significant growth in recent years, driven by the increasing prevalence of chronic diseases and rising technological advancements. Innovations like AI integration, portable imaging devices, and wearable technologies have enhanced diagnostic capabilities, contributing to market growth.

Executive Summary

For more details on this report – Request for Sample

Radiology Market Dynamics: Drivers & Restraints

Rising technological advancements in imaging systems are significantly driving the radiology market growth

Artificial intelligence (AI) algorithms can analyze radiological images with high precision, detecting even subtle abnormalities that might be missed by human radiologists. Thus, major market players and emerging players are focusing on AI-enabled radiology, which is driving the growth of the radiology market.

For instance, in May 2025, GE HealthCare launched CleaRecon DL, a technology powered by a deep-learning algorithm, to improve the quality of cone-beam computed tomography (CBCT) images. This artificial intelligence (AI)-driven solution is designed to remove streak artifacts caused by the pulsatile nature of blood flow in the arteries and changes in the distribution of contrast during CBCT acquisitions in liver, prostate, neuro, and endovascular aortic repair procedures. CleaRecon DL received U.S. FDA 510(k) clearance and CE mark and will be available for use on the Allia platform.

The transition from traditional film-based radiography to digital systems and software enables faster image processing, better storage, and easier sharing of diagnostic results. Cloud-based software and systems allow radiologists to access and interpret images remotely, improving accessibility and reducing diagnostic delays.

For instance, in June, Carestream introduced Image Suite MR 10 Software to help radiographers increase productivity and efficiency while also providing a more user-friendly imaging experience. Carestream's Image Suite Software, which includes a user-friendly interface, specialized measuring tools, and an optional Mini-PACS module, improves imaging performance for both Computed Radiography (CR) and Digital Radiography (DR) systems. These new capabilities help take Image Suite Software to the next level, providing a drastically better imaging experience.

Radiation exposure concerns are hampering the growth of the radiology market

Prolonged or excessive exposure to radiation, especially from imaging procedures like X-rays and CT scans, increases the risk of developing cancer. For instance, according to the National Institute of Health (NIH), from 0.50 mSv in radiology alone to 2.29 mSv in diagnostic radiology, interventional radiology, and nuclear medicine, the average radiation dose from diagnostic radiology has grown dramatically. According to the most recent data, the chance of developing cancer has doubled for the same dosage. With current radiation exposure, the increased risk is 4.1% with revised risk estimations, the risk rises to 8.2%.

While radiation exposure is a necessary component of many diagnostic imaging procedures, growing concerns over its risks have influenced the radiology market's growth. Stricter regulations, patient hesitance, and the push for safer, non-radiation-based alternatives are key factors limiting the market potential for traditional radiology. However, innovations in low-radiation technologies and efforts to adhere to safety guidelines are helping to address these concerns, mitigating their negative impact on the market.

Key Takeaways

- Diagnostic imaging systems, including X-ray, CT, MRI, ultrasound, and nuclear imaging, continue to witness strong demand due to the growing burden of chronic diseases and increasing emphasis on early disease detection.

- North America maintains market leadership, supported by advanced healthcare infrastructure, high healthcare expenditure, favorable reimbursement policies, and rapid adoption of AI-enabled imaging technologies.

- Asia-Pacific is projected to register the fastest growth as healthcare investments, medical tourism, aging populations, and expanding access to diagnostic services accelerate across emerging economies.

- Technological advancements such as artificial intelligence, cloud-based imaging platforms, and integrated PACS/RIS solutions are becoming key factors influencing purchasing decisions among healthcare providers.

- Rising prevalence of cancer, cardiovascular diseases, neurological disorders, and musculoskeletal conditions is increasing demand for high-resolution and minimally invasive diagnostic imaging procedures.

- Healthcare organizations are increasingly evaluating vendors based on imaging accuracy, workflow automation, interoperability, AI capabilities, service support, and cost efficiency rather than standalone imaging hardware features.

- Regulatory compliance, patient safety requirements, and initiatives to reduce radiation exposure are driving investments in next-generation radiology systems and advanced image management solutions.

- The transition toward value-based healthcare and personalized medicine is encouraging the adoption of AI-assisted diagnostics, teleradiology services, and data-driven imaging workflows across hospitals and diagnostic centers.

Market Scope

| Metrics | Details | |

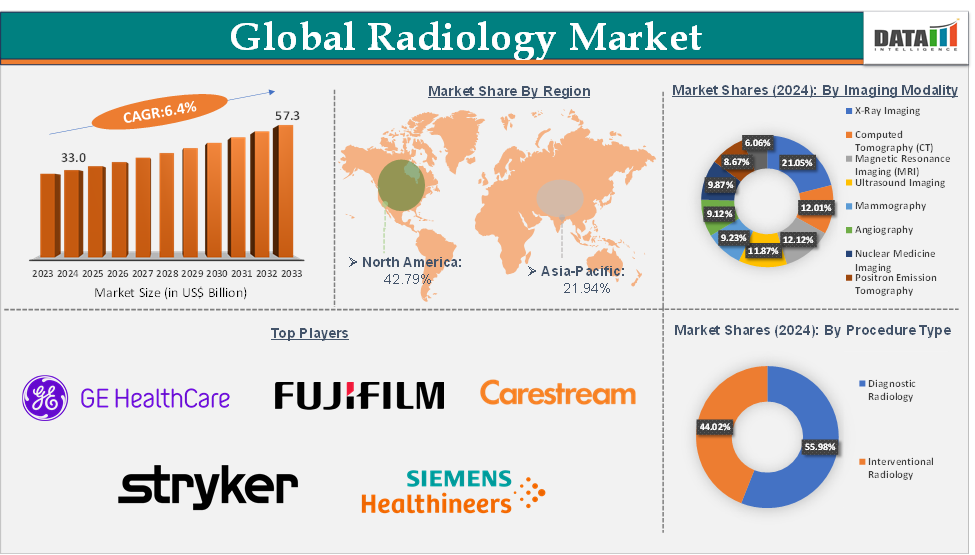

| CAGR | 6.4% | |

| Market Size Available for Years | 2025-2033 | |

| Estimation Forecast Period | 2026-2033 | |

| Revenue Units | Value (US$ Bn) | |

| Segments Covered | Imaging Modality | X-Ray Imaging, Computed Tomography (CT), Magnetic Resonance Imaging (MRI), Ultrasound Imaging, Mammography, Angiography, Nuclear Medicine Imaging, Positron Emission Tomography, and Others |

| Technology | Digital Radiology, Analog Radiology, and AI-Enabled Radiology | |

| Application | Oncology, Cardiology, Neurology, Orthopedics, Obstetrics and Gynecology, Others | |

| Procedure Type | Diagnostic Radiology and Interventional Radiology | |

| End-User | Hospitals, Specialty Clinics, Diagnostic Centers, Academic and Research Institutes, and Others | |

| Regions Covered | North America, Europe, Asia-Pacific, South America, and the Middle East & Africa | |

Radiology Market Segment Analysis

The global radiology market is segmented based on imaging modality, technology, application, Procedure type, end-user, and region.

The X-ray imaging from the imaging modality segment is expected to hold 21.05% of the market share in the radiology market

X-ray imaging is used extensively for diagnosing bone fractures, joint issues, chest conditions, and dental problems. Its versatility makes it the first-line diagnostic tool in many clinical settings. The development of portable X-ray systems helps healthcare practitioners to simplify the process of taking X-rays with advanced features and by moving the X-ray systems where needed. Advancements in X-ray imaging by market players are boosting the segment growth.

For instance, in January 2025, OXOS Medical launched its MC2 Portable X-ray System by achieving FDA 510(k) clearance. The X-ray device is portable and cordless, allowing healthcare practitioners to simplify the process of taking X-rays in traditional and non-traditional spaces. MC2 will have a profound impact on imaging by giving clinics clear imaging for a confident diagnosis, easy-to-use features for an efficient office, and freedom to move the device where needed, without hassle. MC2’s small scatter area and low radiation output can reduce the space and infrastructure needs required by larger systems.

The shift from traditional film-based X-rays to digital radiography (DR) has improved image quality, reduced radiation exposure, and enhanced the efficiency of diagnostic workflows. DR systems provide clearer, higher-resolution images with quicker processing times and easier storage and sharing capabilities. The adoption of digital X-ray systems by major healthcare providers like Siemens Healthineers has contributed to higher diagnostic accuracy and quicker turnaround times for radiologists.

Radiology Market Geographical Analysis

North America is expected to dominate the global radiology market with a 40.6% share

North America, especially the United States, is home to several key players in the medical device and imaging market, including GE Healthcare, Siemens Healthineers, Carestream Health, and other emerging players, who continuously innovate and improve imaging technologies, such as AI-driven systems, low-dose CT scanners, and advanced MRI machines. These rising technological advancements by market players are driving the market growth in the region.

Asia-Pacific is growing at the fastest pace in the radiology market, holding 21.94% of the market share

Asia-Pacific, especially China, India, and Japan witnessing rapid adoption of the latest imaging technologies such as AI-driven diagnostic tools, digital radiography, and low-dose CT scans. These technologies are improving diagnostic accuracy, reducing radiation exposure, and making imaging services more affordable and accessible. In India, many major market players such as Carestream Health, Siemens Healthineers, and GE Healthcare are actively expanding their products with advanced features, providing state-of-the-art imaging systems.

For instance, in January 2025, Royal Philips, a global leader in health technology, launched the artificial intelligence (AI) enabled CT 5300 at the 23rd Asian Oceanian Congress of Radiology (AOCR) 2025. Philips CT 5300 system, equipped with advanced AI capabilities, is designed for diagnosis, interventional procedures, and screening. The flexible X-ray CT system increases diagnostic confidence, streamlines workflow efficiency, and maximises system uptime, helping to improve patient outcomes and department productivity.

There is a growing awareness of the importance of early disease detection and preventive healthcare across the region. This awareness is driving people to seek regular medical check-ups and diagnostic imaging, particularly for detecting cancers, heart diseases, and neurological conditions. In countries like Japan and South Korea, early cancer screening programs have become more common, which drives the demand for diagnostic imaging technologies like CT scans, mammograms, and ultrasound.

Why This Report Matters in 2026

Healthcare providers enter 2026 under growing pressure to expand diagnostic capacity while improving efficiency, accuracy and patient outcomes. Radiology departments are no longer viewed solely as imaging centers because they now play a central role in early disease detection, precision medicine, oncology management and integrated clinical decision-making. Hospital administrators and procurement teams require clearer visibility into technology investments, imaging modalities, service models and vendor capabilities to optimize performance while controlling operational costs.

Healthcare systems are also facing complex modernization challenges. Decision-makers must evaluate investments across digital radiography, computed tomography, magnetic resonance imaging, ultrasound, nuclear imaging and interventional radiology solutions. Increasing adoption of AI-assisted diagnostics, cloud-based imaging platforms, teleradiology services and enterprise imaging ecosystems creates varying implications for workflow efficiency, data management, reimbursement, patient access and long-term infrastructure requirements. A comprehensive market perspective enables healthcare organizations to compare technology pathways rather than viewing radiology expansion as a single equipment purchase decision.

Radiology transformation is becoming increasingly outcome driven as regulators, healthcare networks and payers demand measurable improvements in diagnostic accuracy, turnaround times and patient care quality. Hospitals, diagnostic imaging centers, specialty clinics and academic institutions need reliable benchmarks on vendor portfolios, regional growth opportunities, application trends, channel strategies and managed service models. The report helps clients identify where demand is evolving, which companies are best positioned and which investment priorities should be addressed first to strengthen diagnostic capabilities while improving healthcare delivery and operational resilience.

Radiology Market Major Players

The major global players in the radiology market include GE HealthCare, Koninklijke Philips N.V., FUJIFILM Holdings Corporation, Carestream Health, Hologic, Inc., Stryker Corporation, Boston Scientific Corporation, Siemens Healthineers AG, CANON MEDICAL SYSTEMS USA, INC., and Shimadzu Corporation, among others.

Recent Developments

- In March 2026, GE HealthCare expanded its radiology portfolio with AI-enabled imaging systems for faster and more accurate diagnostics. The innovation focuses on workflow automation and image precision. This supports improved clinical outcomes.

- In February 2026, Siemens Healthineers introduced next-generation radiology solutions with advanced imaging modalities and AI integration. The development enhances diagnostic efficiency and accuracy. This benefits healthcare providers.

- In January 2026, Philips Healthcare strengthened its radiology systems with cloud-based platforms and connected imaging technologies. The focus is on data integration and remote access. This supports digital radiology ecosystems.

Why Purchase the Report?

- To visualize the global radiology market segmentation based on product type, imaging modality, application, end-user, and region, while gaining insights into key commercial assets and leading market participants.

- Identify revenue opportunities by analyzing emerging trends, technological advancements, strategic collaborations, and innovation activities across the radiology ecosystem.

- Excel data sheet with numerous data points at the radiology market level covering all segments and sub-segments.

- PDF report consists of comprehensive analysis supported by exhaustive qualitative interviews and in-depth industry research.

- Product mapping available in Excel format, covering major imaging systems, software solutions, and offerings of leading companies.

- The global radiology market report provides approximately 78 tables, 78 figures, and 181 pages of detailed market intelligence.

Target Audience

- Medical Imaging Equipment Manufacturers

- Hospitals and Diagnostic Imaging Centers

- Healthcare Providers and Buyers

- Industry Investors and Investment Bankers

- Research Professionals and Market Analysts

- Healthcare IT and AI Solution Providers

- Regulatory Authorities and Government Organizations

- Emerging Companies and Start-ups

- Distributors and Channel Partners

- Academic Institutions and Research Organizations

Related Reports

- Radiology Information System (RIS) Market

- Picture Archiving and Communication System (PACS) Market

- Ultrasound Devices Market

- Nuclear Imaging Market

The global radiology market report delivers a detailed analysis with 78 key tables, more than 82 visually impactful figures, and 198 pages of expert insights, providing a complete view of the market landscape.