Portable Oxygen Concentrators Market Size

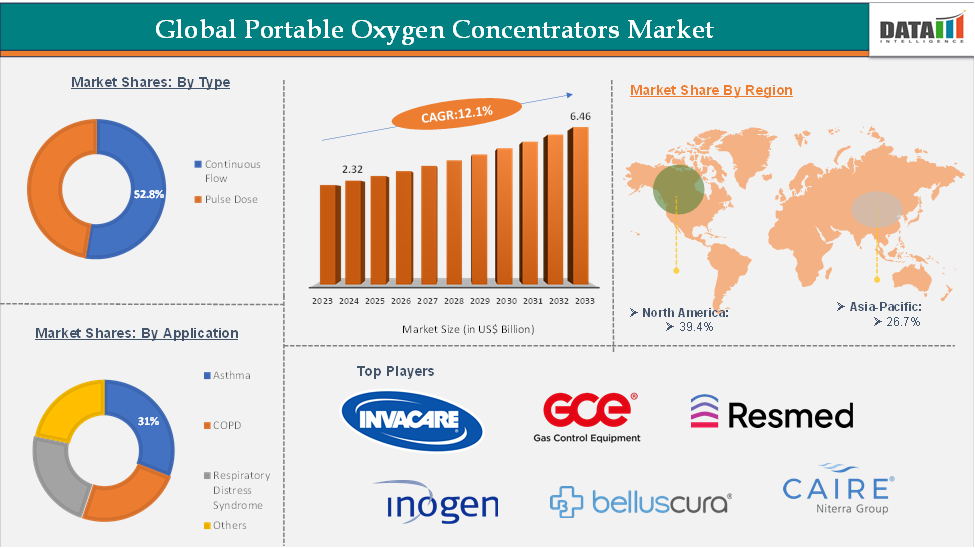

The portable oxygen concentrators market size reached US$2.60 billion in 2025 and is expected to reach US$6.46 billion by 2033, growing at a CAGR of 12.1% during the forecast period 2026-2033.

Executive Summary

For more details on this report – Request for Sample

Portable Oxygen Concentrators Market Dynamics: Drivers & Restraints

Rising adoption of portable oxygen concentrators is expected to drive the portable oxygen concentrators market growth significantly

The portable oxygen concentrators (POCs) market is experiencing significant growth, largely driven by the increasing adoption of these devices. Several key factors contribute to this trend, including advancements in technology, a growing patient population, and evolving healthcare dynamics. As the global population ages, there is a corresponding rise in age-related respiratory issues.

Older adults are particularly vulnerable to conditions like chronic obstructive pulmonary disease (COPD) and other chronic lung diseases, which often necessitate long-term oxygen therapy. For instance, according to the American Lung Association, Chronic Obstructive Pulmonary Disease (COPD) affects approximately 11.7 million adults and leads to hundreds of thousands of emergency room visits annually, contributing to healthcare expenditures amounting to tens of billions of dollars each year.

Elderly patients, who are more likely to require oxygen therapy, prefer portable solutions that enable them to maintain their daily activities and active lifestyles. For instance, according to the National Institute of Health, in 2024, each year, approximately 1.5 million patients in the USA receive long-term oxygen therapy. This demographic shift significantly boosts the demand for POCs.

Many individuals requiring long-term oxygen therapy favor portable concentrators for home use over stationary systems or cylinders. POCs allow users to maintain mobility within their homes and facilitate outdoor activities. Modern devices are now smaller, lighter, and more user-friendly compared to earlier models. Innovations in battery technology have enhanced the portability of these concentrators, resulting in longer battery life and improved comfort during use, making them more appealing to patients.

Limited oxygen flow rates are expected to hinder the portable oxygen concentrators market

Portable oxygen concentrators generally provide oxygen flow rates between 1 to 3 liters per minute (LPM) for continuous flow, with higher rates available for pulse flow settings. However, patients with more severe respiratory conditions may require higher flow rates, such as 5 LPM or more. This limitation restricts the usability of many POCs for individuals with advanced-stage COPD or other serious respiratory diseases, thereby narrowing the target market for manufacturers. Thus, the above factors could hinder the market growth.

Portable Oxygen Concentrators Market Segment Analysis

The global portable oxygen concentrators market is segmented based on type, application, end-user, and region.

Type:

The continuous flow oxygen concentrators segment is expected to hold 52.8% of the market share in 2024 in the portable oxygen concentrators market

The continuous flow oxygen concentrators segment is expected to dominate the portable oxygen concentrators market. Continuous flow concentrators are particularly advantageous for patients with severe respiratory conditions, as they provide a steady supply of oxygen without the need for breath detection technology, making them more reliable for those requiring higher flow rates.

Additionally, advancements in technology have improved the efficiency and reliability of these devices, enhancing their appeal in both home healthcare settings and medical facilities. The cost-effectiveness of continuous flow concentrators, which tend to be cheaper than pulse flow models due to their simpler design, also contributes to their growing market dominance. For instance, the range of continuous flow portable oxygen concentrators begins from Philips SimplyGo, costing around ₹ 1.80 Lakh, to the top-end SeQual Eclipse, costing around ₹ 3.20 Lakh. This makes the consumers feel convenient than the other types.

Portable Oxygen Concentrators Market Geographical Analysis

North America is expected to dominate the global portable oxygen concentrators market with a 39.4% share in 2024

North America holds a major portion of the portable oxygen concentrators market and is expected to hold a significant position in the portable oxygen concentrators market. This is due to the growing adoption of portable oxygen concentrators, the increasing number of product launches, and the rising prevalence of respiratory diseases. The region is experiencing high rates of respiratory diseases such as asthma and COPD, among others, which increases the need for oxygen therapy. Increasing these conditions in the region increases the demand for these devices.

For instance, according to the Asthma and Allergy Foundation of America report published in 2025, more than 28 million people in the U.S. are living with asthma. Of these, over 23 million are adults aged 18 and older. Asthma disproportionately affects certain groups, with the highest rates seen among black adults and a greater prevalence in women than men; about 11.0% of adult women have asthma compared to 6.8% of men. In children, asthma remains one of the most common chronic conditions, currently affecting around 4.9 million individuals under the age of 18.

The presence of a large number of key players in the region is also contributing to the growth of the region’s market. Companies are introducing the latest portable oxygen concentrators in the region. For instance, in October 2024, Inogen, Inc. announced that it had commenced the U.S. market release of the Inogen Rove 4 Portable Oxygen Concentrator. With an additional, fourth flow setting delivering up to 840ml/min of medical grade oxygen, in a lightweight user-friendly design of less than 3 lbs1 and three battery configurations providing up to 5 hours and 45 minutes of operation2, the versatility of Rove 4 empowers patients with choices that may help them with normal activities of daily living.

Key Developments

February 2026: Growing adoption of portable devices across North America and Europe accelerated demand for compact oxygen concentrators for home healthcare and long-term respiratory support.

January 2026: Increasing investments in home healthcare infrastructure in Asia-Pacific and Middle East & Africa strengthened accessibility to portable oxygen concentrators for chronic respiratory disease patients.

December 2025: Rising integration of smart monitoring technologies across Europe and North America improved patient tracking, oxygen flow management, and remote healthcare support capabilities.

November 2025: Expansion of telehealth services in North America and Asia-Pacific enhanced adoption of portable oxygen concentrators for home-based respiratory care and post-hospital recovery.

October 2025: Increasing prevalence of COPD, asthma, sleep apnea, and other respiratory disorders in Asia-Pacific and North America boosted demand for effective oxygen therapy devices globally.

September 2025: Growing advancements in battery technology across Europe and North America improved portability, operational efficiency, and longer runtime of oxygen concentrator systems.

August 2025: Rising awareness regarding elderly care in Latin America and Middle East & Africa encouraged greater adoption of lightweight and travel-friendly oxygen concentrators.

July 2025: Increasing government healthcare initiatives and investments in respiratory care infrastructure across Asia-Pacific and Europe accelerated development and accessibility of advanced portable oxygen concentrator systems worldwide.

Portable Oxygen Concentrators Market Top Companies

Top companies in the portable oxygen concentrators market include Inogen, Inc., Koninklijke Philips N.V., Pure O2 Ltd, Belluscura, BPL Medical Technologies, GCE Group, Timago, CAIRE Inc., ResMed, and Invacare Corporation, among others.

Market Scope

Metrics | Details | |

CAGR | 12.1% | |

Market Size Available for Years | 2023-2033 | |

Estimation Forecast Period | 2026-2033 | |

Revenue Units | Value (US$ Bn) | |

Segments Covered | Type | Continuous Flow, Pulse Dose |

Application | Asthma, COPD, Respiratory Distress Syndrome, Others | |

End-User | Homecare, Hospitals, Ambulatory Surgical Centers, Others | |

Regions Covered | North America, Europe, Asia-Pacific, South America, and the Middle East & Africa | |

The global portable oxygen concentrators market report delivers a detailed analysis with 54 key tables, more than 45 visually impactful figures, and 159 pages of expert insights, providing a complete view of the market landscape.