Medical Batteries Market Overview

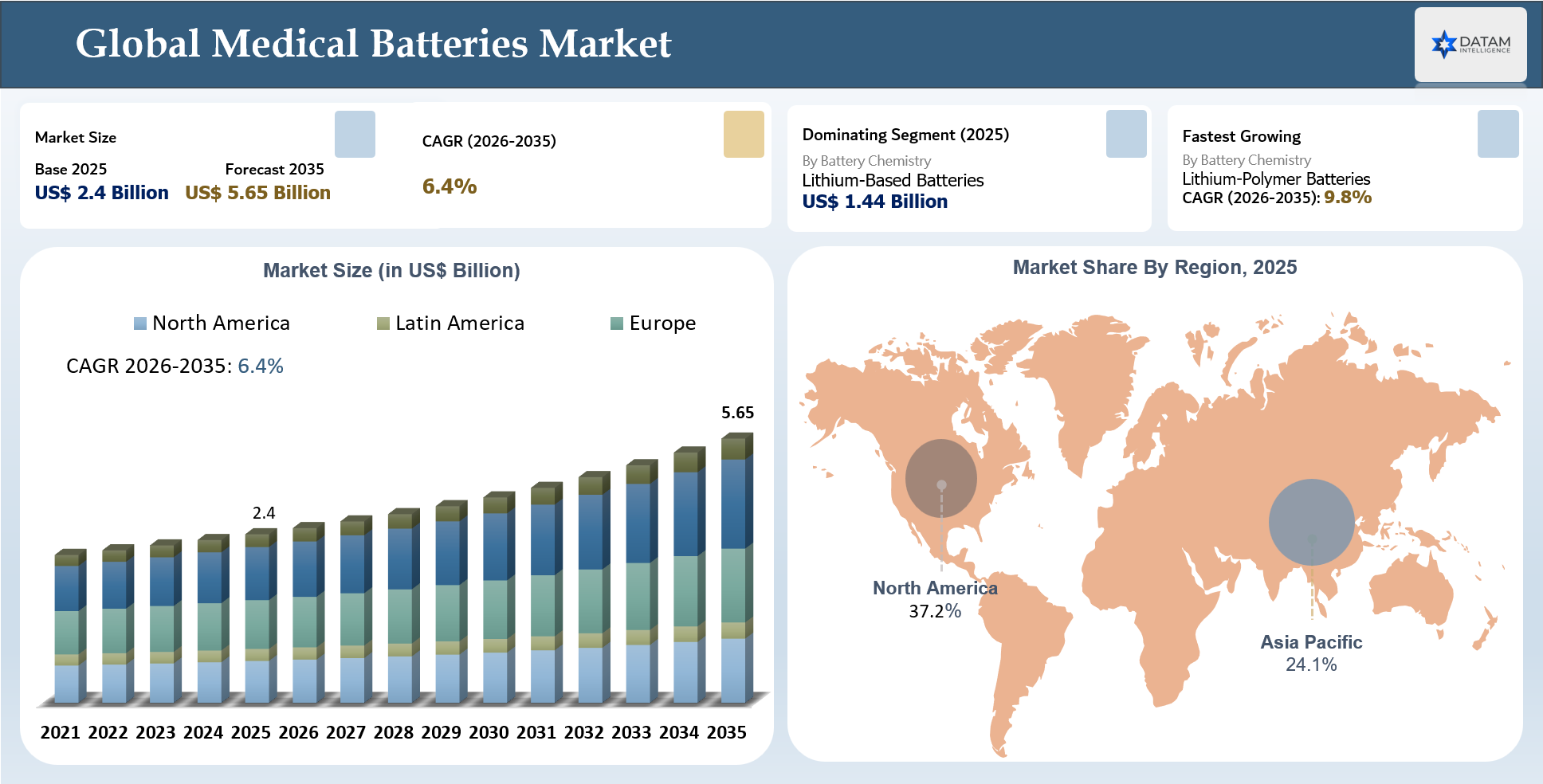

The Global Medical Batteries Market stood at US$ 2.4 billion in 2025 and is expected to reach US$ 5.65 billion by 2035, growing with a CAGR of 6.4% during the forecast period 2026-2035.

The medical batteries market globally is poised to enter an even more strategic era owing to the transition from stand-alone devices to connected, portable, and continuous operation systems. The most crucial development is battery intelligence, whereby the power systems are supposed to play a vital role in maintaining the uptime of devices, predicting replacements, safe charging, lifecycle management, and remote monitoring. These developments have become indispensable for pacemakers market, ICDs, neurostimulators, infusion pumps, patient monitors, ventilators, hearing aids, medical carts, smart patches, and other home medical devices.

Medical Device OEMs and healthcare purchasers are progressing past simple capacity and price considerations for their batteries. The purchasing process focuses on reliability, runtime capability, size, chemical safety, thermal management, charging capability, and ability to integrate within connected health environments. Lithium Primary batteries will continue to play an important role in the development of implantable devices, whereas lithium-ion batteries and LiPo batteries have become increasingly relevant for rechargeable medical carts, wearables, portable monitoring equipment, and at-home applications. As battery failures, charging issues and unexpected depletion can create clinical and regulatory risk, suppliers offering medical-grade battery platforms, custom packs, validated charging systems and lifecycle support will be better positioned than companies selling standard battery components.

Key Takeaways

- The Global Medical Batteries Market was valued at US$ 2.4 billion in 2025 and is projected to reach US$ 5.65 billion by 2035.

- The market is expected to grow at a CAGR of 6.4% during the forecast period 2026-2035.

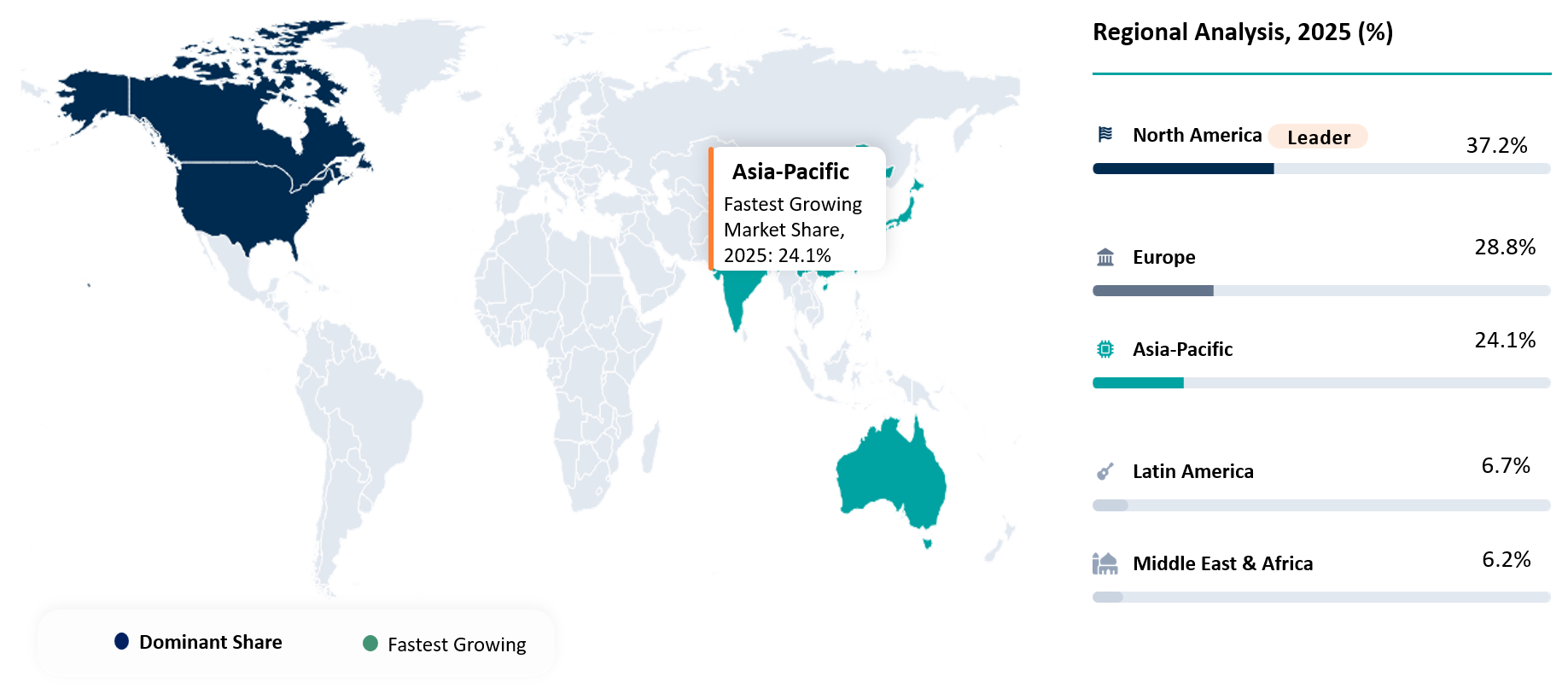

- North America held the highest market share at 37.2% in 2025, supported by strong medical device manufacturing, advanced hospital infrastructure and high adoption of implantable and portable medical devices.

- Asia-Pacific is expected to be the fastest-growing region, driven by expanding healthcare access, rising chronic disease burden, local medical device manufacturing and growing adoption of home healthcare devices.

- Lithium-Based Batteries were the largest battery chemistry segment in 2025, valued at approximately US$ 1.44 billion, supported by strong use in implantable, portable, wearable and connected medical devices.

- Lithium-Polymer Batteries are projected to be the fastest-growing battery type, expanding at an estimated 9.8% CAGR during 2026–2035.

- Medical carts, portable monitors, infusion pumps, hearing aids, wearable devices and home healthcare equipment are creating strong demand for rechargeable and compact battery systems.

- Battery procurement is shifting toward longer runtime, high energy density, compact form factor, safety compliance, supplier reliability and lower replacement burden.

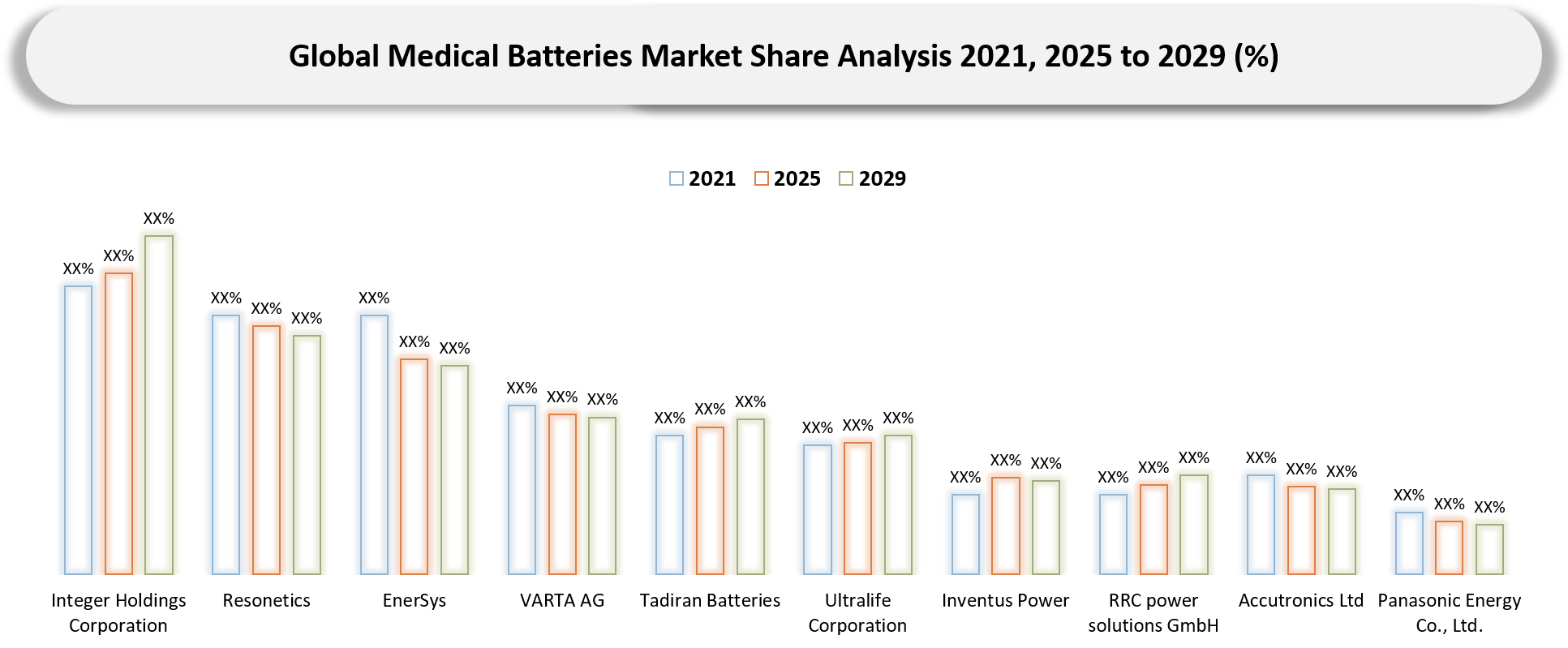

- The market has a strong competitive presence, with key players including Integer Holdings Corporation, Resonetics, EnerSys, VARTA AG, Tadiran Batteries, Ultralife Corporation, Inventus Power, RRC power solutions GmbH, Accutronics Ltd and Panasonic Energy Co., Ltd.

Medical Batteries Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 2.4 Billion | |

| 2035 Projected Market Size | US$ 5.65 Billion | |

| CAGR (2026-2035) | 6.4% | |

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Battery Chemistry | Lithium-Based Batteries, Nickel-Based Batteries, Zinc-Based Batteries, Silver-Based Batteries, Alkaline Batteries, Lead-Based Batteries and Others | |

| By Battery Type | Primary Batteries and Secondary Batteries | |

| By Product Type | Implantable Medical Batteries, Portable Medical Device Batteries, Wearable Medical Device Batteries, External Medical Equipment Batteries, Backup and Emergency Power Batteries, Hearing Aid Batteries and Diagnostic Equipment Batteries | |

| By Battery Form Factor | Cylindrical Cells, Coin Cells, Button Cells, Prismatic Cells, Pouch Cells, Thin-Film Cells, Custom Battery Packs, Modular Battery Packs and Others | |

| By Application / Use Cases | Implantable Cardiac Devices, Neurostimulation Devices, Drug Delivery Devices, Patient Monitoring Devices, Respiratory Care Devices, Hearing Care Devices, Medical Carts and Mobile Workstations, and Home Healthcare and Wearable Devices | |

| By End-User | Medical Device OEMs, Hospitals and Clinics, Ambulatory Surgical Centers, Diagnostic Centers, Home Healthcare Providers, Long-Term Care Facilities, Retail and Hearing Care Centers and Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Disruption Analysis

Medical Batteries Becoming the Power Backbone of Connected, Portable and Implantable Care

The global medical batteries market is being upended by the fast-paced transformation into an era of connected, mobile, and self-managed devices within the healthcare industry. Batteries are moving away from mere energy sources to become pivotal to reliable operation, mobility, miniaturization, and round-the-clock care enabled by implantable devices, remote patient monitoring systems, infusion pumps, mobile medical carts, smart patches, and mobile ventilators, thereby generating demand for small-sized, high-density, and customized batteries that offer better runtime and safety characteristics.

Disruption is also emerging from AI-enabled battery diagnostics, predictive replacement alerts, wireless charging, safer chemistries and stricter medical-grade quality expectations. Hospitals and OEMs are increasingly evaluating batteries based on lifecycle reliability, thermal stability, device compatibility, regulatory compliance and total cost of ownership. Suppliers that can combine chemistry expertise, form-factor flexibility, OEM co-development and aftermarket replacement support will be better positioned. The market’s next phase will favor battery companies that shift from product supply to engineered medical power solutions.

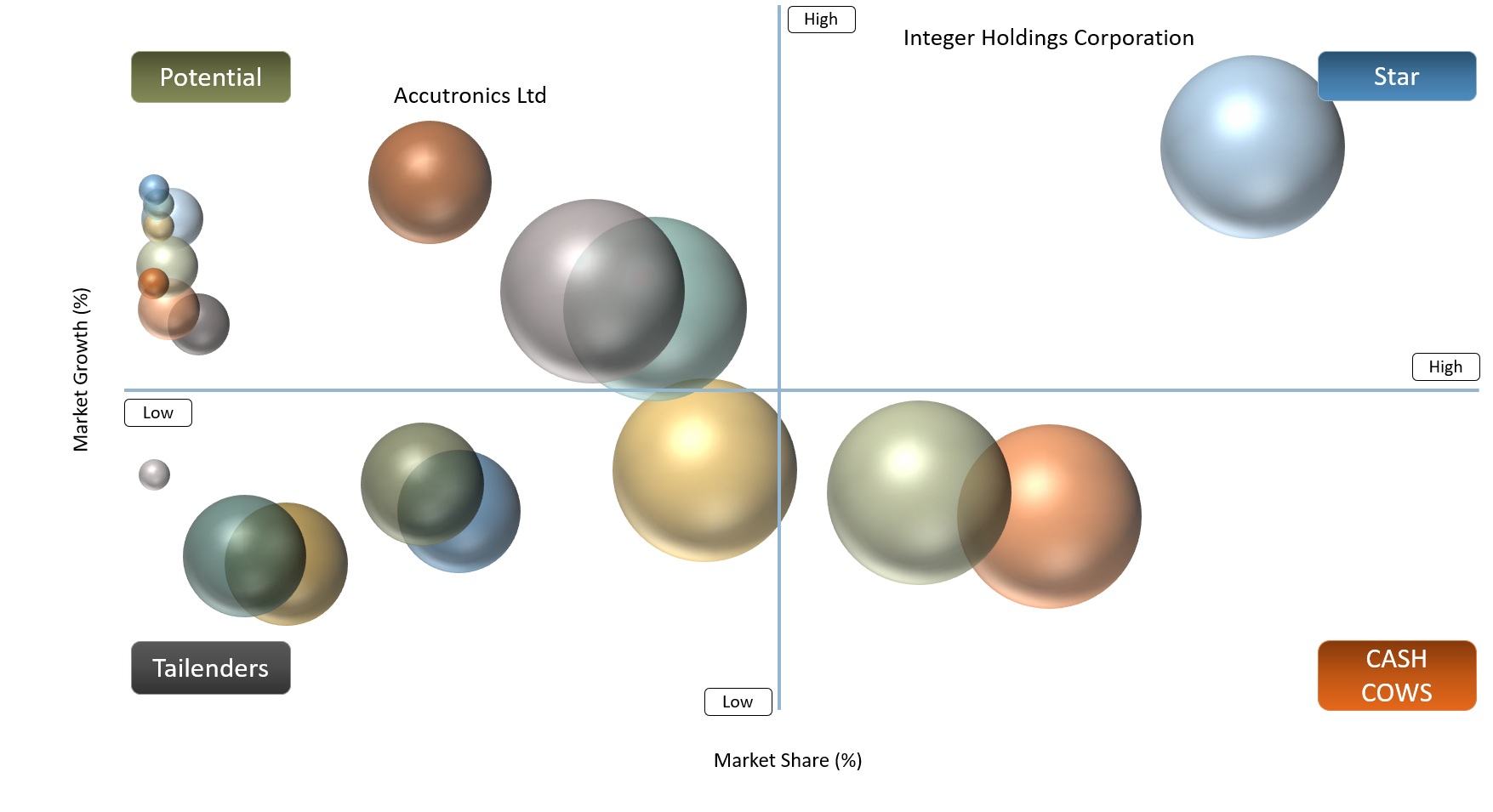

BCG Matrix: Company Evaluation

As for the BCG matrix, for the Global Medical Batteries Market, Stars are companies with strong medical-grade battery portfolios, global OEM relationships, advanced lithium battery capabilities and relevance across implantable, portable, wearable and high-criticality medical devices. Integer Holdings Corporation, Resonetics, EnerSys, VARTA AG, Tadiran Batteries, Inventus Power and Panasonic Energy Co., Ltd. can be positioned as Stars due to their strong technology depth, medical device integration capabilities, implantable or rechargeable battery expertise and ability to support high-growth medical applications.

The cash cows in the market would be those companies that have an established business model in the battery industry, repeat demand for replacements, a strong brand name and stable demand in portable medical equipment, hearing aid batteries, home care products, medical carts and back-up power solutions. Some of the companies that fall in the category of cash cows are Ultralife Corporation, RRC power solutions GmbH, Accutronics Ltd, Saft Groupe SAS, Energizer Holdings, Inc., Duracell Inc., Renata SA and Maxell, Ltd.

Question Marks have high growth potential, but their positive potential depends upon greater penetration by medical devices, qualifying OEMs, application customization, and expanding uses for medical batteries. Inventus Power, RRC Power Solutions GmbH, Accutronics Ltd, Renata SA, and Maxell, Ltd. can also be considered Question Marks that are growing rapidly in custom battery packs, rechargeable medical battery systems, microbatteries, wearable medical devices, and future compact medical electronics products.

Market Dynamics

Implantable and Connected Medical Devices Are Raising Demand for High-Reliability Battery Platforms

The proliferation of implantable and connected medical devices makes battery performance an important consideration in the Global Medical Batteries Market. Implantable and other portable medical devices such as pacemakers, ICDs, neurostimulators, implantable loop recorders, insulin pumps, infusion pumps, and remote monitoring devices depend on batteries that provide reliable performance, longevity and safety even while used continuously. For such medical applications, any form of malfunction is associated with potential risks, meaning that reliability, chemical stability and consistent discharge properties are key requirements when sourcing for such batteries by medical device manufacturers.

Moreover, connected healthcare devices will create new demand for compact and rechargeable battery technology. Wearable health monitoring devices, diagnostic equipment, smart patches and home healthcare devices will require batteries that facilitate wireless communications and energy efficiency in order to transmit more data. These will favor the use of lithium primary batteries for use in implantable medical devices as well as lithium-ion and LiPo batteries for portable and wearable applications. Suppliers capable of combining miniaturization, safety compliance, OEM customization and lifecycle reliability are expected to gain stronger traction.

Battery Safety Risks, Thermal Issues and Device Recall Exposure Limit Faster Adoption in Critical Applications

Battery safety poses one of the most significant constraints in the Global Medical Batteries Market, particularly in critical scenarios where the device is used in implants, infusion pumps, ventilators, medical monitors, and mobile carts. Problems in terms of overheating, swelling, leaking, short circuiting, battery charging problems, and even depletion of the battery are some of the potential hazards that might affect the performance and safety of patients. The choice of batteries for use in these devices is therefore extremely critical for both OEMs and buyers.

This becomes more of a concern due to the ever-decreasing size and increased connectivity and rechargeability of medical devices. Both lithium-ion and LiPo batteries have good energy densities, yet need to be managed properly in terms of heat dissipation, charging protocols, casing designs and quality assurance procedures. Any problems associated with the batteries can result in product recalls, regulatory concerns, warranty claims and damaged reputation for both the supplier of the batteries and the company making the medical devices. As a result, adoption can slow in critical applications where buyers prefer proven chemistries, validated suppliers, and long-term reliability data over faster technology shifts.

Segmentation Analysis

The global medical batteries market is segmented based on the battery chemistry, battery type, product type, battery form factor, application/use cases, end-user, sales channel, and region.

Lithium-Based Batteries Become the Core Power Platform for Implantable, Portable and Connected Medical Devices

Batteries based on lithium are projected to continue dominating the Global Medical Batteries Market on account of the suitability of lithium-based batteries in the medical applications of implantable, portable, wearable and connected devices. The advantages of lithium batteries, including high energy density, smaller size, stable voltage, and longer runtime, make them very well-suited for critical devices such as pacemakers, ICDs, neurostimulators, implantable loop recorders, infusion pumps, and portable patient monitors, wherein the performance of the batteries significantly impacts the safety of the patients.

There has been rapid adoption of rechargeable Li-ion and Li-polymer batteries in medical applications, which includes medical carts, wearable sensors, smart patches, portable diagnostics devices, respiratory care devices and home health care devices, owing to the need to have batteries which provide longer runtime, smaller form factors, fast charging and safe operation. Companies that offer specialized lithium battery platforms, customized battery packs, thermal management technologies and OEM design assistance services can potentially capture higher value in this segment.

Geographical Penetration

North America Leads Medical Batteries Demand Through Advanced Device Adoption and High-Reliability Healthcare Power Requirements

The Global Medical Batteries Market will be led by the North America region as it holds a dominant market share position of 37.2%. North America's leadership in the market can be attributed to factors such as a vibrant medical devices manufacturing industry, sophisticated hospital infrastructure, and higher adoption rates of implantable, portable, and connected medical devices. There is high demand for medical batteries among applications such as pacemakers, ICDs, neurostimulators, infusion pumps, patient monitors, portable ventilators, hearing aids, and medical carts, which rely on batteries for their operation.

There has been significant momentum in the medical battery market owing to home health care services, remote patient monitoring, and mobility in hospitals. Factors such as selection of batteries based on life cycle, safety compliance, miniaturization, recharging capability, supplier qualifications, and replacement planning will drive demand for medical batteries in North America. Primary lithium batteries have applications in medical implants, while lithium-ion and LiPo batteries are gaining traction among portable monitors, wearable devices, infusion pumps, medical carts, and home health care equipment.

U.S Medical Batteries Market Trends

The U.S. Medical Batteries Market is moving toward higher reliability, smarter battery monitoring and application-specific power systems as hospitals and OEMs expand connected care, implantable devices and mobile clinical workflows. Demand is strongest across insulin pumps, patient monitors, portable ventilators, medical carts, hearing aids, neurostimulators and cardiac implants, where battery failure can interrupt therapy or clinical workflow. In 2024, the FDA reported a Class I recall for Tandem’s t:connect mobile app used with the t:slim X2 insulin pump, where software behavior could cause rapid pump battery depletion and unexpected shutdown risk.

Stronger focus is emerging on charging reliability, thermal safety and replacement planning for life-supporting and home-use devices. The U.S. market is shifting toward lithium-ion and LiPo batteries for portable devices and medical carts, while lithium primary batteries remain important for implantable applications. In 2024, the FDA also reported Baxter’s Life2000 ventilator recall due to potential battery charging dongle failure, which could prevent charging or allow intermittent charging. Overall, the U.S. market is moving toward battery intelligence, validated charging systems and application-specific power platforms, making reliability a stronger differentiator than price alone.

Japan Medical Batteries Market Outlook

The Japan Medical Batteries Market is expected to grow steadily as the country’s healthcare system shifts toward compact medical devices, home-based care and continuous patient monitoring. Japan’s aging population creates strong demand for battery-powered devices such as pacemakers, hearing aids, infusion pumps, patient monitors, home care respiratory devices and wearable health systems. According to Japan’s Statistics Bureau, the population aged 65 years and above reached 36.24 million, representing 29.3% of the total population in 2024, creating a strong demographic base for long-term medical device usage.

The market outlook is also supported by Japan’s strength in precision electronics, battery miniaturization and high-quality medical device manufacturing. Lithium primary batteries are expected to remain important in implantable devices, while lithium-ion and LiPo batteries will gain stronger traction in portable monitors, smart patches, medical carts and home healthcare equipment. Overall, Japan’s opportunity lies in compact, safe and high-reliability medical batteries that support aging-led care demand, remote monitoring and patient mobility.

Medical Batteries Market Competitive Landscape

The Global Medical Batteries Market has moderate consolidation, with competition driven by medical grade performance capabilities, chemical expertise, OEM certifications, customization capabilities, and assured supply. The market includes firms like Integer Holdings Corporation, Resonetics, and EnerSys, which have a strong presence in the field of high-criticality batteries and implantable batteries. On the other hand, VARTA AG, Tadiran Batteries, and Panasonic Energy Co., Ltd., offer their competitive edge in terms of their lithium-based batteries, micro batteries, and specialty batteries. Inventus Power, RRC power solutions GmbH, and Accutronics Ltd feature in the field of rechargeable battery packs and chargers.

Competitive nature is also driven by battery brands and specialty cells suppliers catering to replacements, home health care, hearing aids, and small-scale medical electronics markets. The players such as Ultralife Corporation, Saft Groupe SAS, Energizer Holdings, Inc., Duracell Inc., Renata SA, and Maxell, Ltd. compete using consistent product availability, after-market presence, specialty offerings, and recurring need for replacement products. In the coming years, competitiveness will be based on chemical safety, increased run time, small size, compliance, OEM partnership, extended life cycle, and compatibility for implantable and portable devices.

Recent Developments

- March 2026: RRC power solutions launched POWERPAQ RRC3570-4, a battery developed for medical and industrial applications, strengthening its position in mobile medical workstations, patient monitoring carts and portable healthcare equipment.

- January 2026: Integer Holdings Corporation showcased innovations in neuromodulation and miniaturized active implantable device technology at NANS 2026, reinforcing demand for compact, high-reliability implantable battery solutions.

- March 2026: Ultralife Corporation prepared to showcase three-second hot-swap power solutions for medical carts at HIMSS 2026, supporting hospital demand for uninterrupted mobile workstation power.

- November 2025: Ultralife expanded the positioning of its X5 Power System from medical carts toward broader mission-critical power use, signaling rising demand for modular, hot-swappable battery architectures.

- June 2025: Murata announced the transfer of its micro primary battery business to Maxell, strengthening Maxell’s role in compact primary batteries used across medical wearables, hearing care and small healthcare electronics.

- December 2024: Inventus Power announced participation in MD&M West and the Medical Battery Conference 2025, reflecting growing OEM focus on medical battery design, safety, compliance and application-specific engineering.

- October 2024: Medtronic notified MiniMed 600 and 700 series insulin pump users about reduced battery life risk after physical impact, highlighting battery reliability as a critical safety factor in connected therapy devices.

- July 2024: Baxter recalled Life2000 ventilators due to potential battery charging dongle failure, reinforcing the importance of charging reliability in respiratory care and home ventilation devices.

AI Impact Analysis

AI is anticipated to drive the Global Medical Batteries Market via battery design improvements, runtime monitoring, predictive maintenance, and energy optimization. OEMs for medical devices are leveraging the simulation capabilities of AI technologies to test battery chemistry, performance, runtime, temperature considerations, safety concerns, and performance throughout the life of the batteries, even before market commercialization, particularly for applications that are implantable, wearable, used for patient monitoring, as well as infusion pumps, ventilators, and medical carts.

AI may affect the global medical batteries market, which involves battery diagnostic capabilities, battery usage analytics, and forecasting future replacement needs for batteries at hospitals, as well as at home health care facilities. Connected devices in medicine can benefit from AI technology in predicting battery degradation, preventing failures, and optimizing battery charging. For battery manufacturers, opportunities within the Global Medical Batteries Market driven by AI include manufacturing custom medical batteries, rechargeable lithium batteries, LiPo batteries, implantable-grade batteries, and batteries with remote monitoring capabilities.

White Space Opportunities

White space opportunities in the Global Medical Batteries Market continue to increase as technology enables greater portability, connectivity and patient-controlled devices. There is a significant unmet demand for small and dense batteries capable of offering extended runtime capability for use in wearables, smart patches, infusion pumps, portable monitors, hearing aids, and home healthcare equipment. The development of medical cart batteries presents another definite white space as facilities explore mobile power sources that minimize downtime, streamline workflow and allow for constant bedside care.

Other growth spaces include custom battery packs, batteries for implantable devices, rechargeable lithium-ion and LiPo batteries, and next-generation, safer batteries such as solid-state and thin-film technologies. Companies that can offer a combination of safety certification, miniaturization capabilities, lifecycle consistency and OEM customization will be poised for success. Demand is especially strong in aftermarket replacement batteries, remote monitoring-enabled power systems and solutions designed for aging populations, chronic disease management and decentralized healthcare delivery.

Capital Deployment Roadmap: To read a detailed strategic breakdown of where private equity firms and global battery suppliers are concentrating their investment funds, explore our analytical assessment: 5 Biggest Investment Opportunities in the Medical Battery Industry.

DMI Opinion

As per the findings of DataM, the Global Medical Batteries Market is moving from a simple component-based industry into one based on the strategic development of medical devices. No longer simply judged by the amount of energy supplied or cost alone, batteries are now being judged by their reliability, safety, compatibility, miniaturizability, performance, and the burdens associated with their replacements. High demand for batteries will come in applications such as implantable devices, patient monitoring systems, infusion pumps, hearing aids, medical carts, portable ventilators, and other portable healthcare devices.

Suppliers with strong abilities in producing lithium primary cells, rechargeable lithium-ion cells, LiPo batteries, custom medical battery packs, and medical-grade battery quality management are best suited for success in this industry. OEM relationships, customized solutions for specific needs, and reliability of after-market replacement parts will be critical differentiating factors. Suppliers who can effectively serve both higher-end critical care devices, such as implantable devices, along with high-growth portable applications, will see the greatest success in the market.

Why This Report Matters in 2026?

The Global Medical Batteries Market will become increasingly strategic by 2026 as healthcare systems move toward portable care, connected monitoring, home healthcare, implantable devices and mobility-based hospital workflows. Reliable battery performance is becoming critical for pacemakers, ICDs, neurostimulators, infusion pumps, patient monitors, ventilators, hearing aids, medical carts and wearable medical devices.

As medical devices become smaller, smarter and more connected, buyers are focusing on longer runtime, high energy density, compact form factor, safer chemistries, rechargeability, lower replacement burden and uninterrupted device performance. Demand is shifting toward lithium primary batteries for implantable devices and rechargeable lithium-ion and LiPo batteries for portable, wearable and medical cart applications.

This report matters because it helps stakeholders understand where medical battery demand is growing, which battery chemistries and form factors are gaining adoption, how OEM and aftermarket demand is evolving, which regions offer stronger growth potential, and which companies are best positioned to capture value in the medical power ecosystem.

Why Choose DataM?

- End-to-End Medical Batteries Ecosystem Evaluation: Includes assessment of the entire medical batteries ecosystem such as batteries for implantation, batteries for use in portable devices, batteries for wearables, power system batteries for medical carts, batteries for backup and power failure conditions, batteries for hearing aids and diagnostics devices.

- Battery Chemistry and Technology Evaluation: Focuses on evaluation of lithium batteries, lithium-ion batteries, lithium-polymer batteries, nickel-metal hydride batteries, nickel-cadmium batteries, zinc-air batteries, silver oxide batteries, alkaline batteries and lead acid batteries to identify commercially viable technologies.

- Application/Use Case and End-User Evaluation: Monitors the demand for batteries in pacemakers, ICDs, neurostimulators, infusion pumps, insulin pumps, patient monitors, ventilators, hearing aids, medical carts, diagnostics devices and wearables.

- Regulatory, Safety and Quality Assessment: Looks at the impact of safety standards for medical devices, battery reliability, certification requirements, device compatibility, replacement frequency and risk of failure management.

- Competitive Strategy Benchmarking: Benchmarked Integer Holdings Corporation, Resonetics, EnerSys, VARTA AG, Tadiran Batteries, Ultralife Corporation, Inventus Power, RRC power solutions GmbH, Accutronics Ltd, Panasonic Energy Co., Ltd., Saft Groupe SAS, Energizer Holdings, Inc., Duracell Inc., Renata SA and Maxell, Ltd. in terms of technology orientation, product range, OEM partnerships and expertise in medical batteries.

- Pricing, Procurement & Market Entry Insight: Provides information regarding purchasing criteria for medical devices OEMs, demand for batteries in hospitals, distribution networks, aftermarket pricing, custom batteries pack development, supplier selection criteria and total cost of ownership.

- Growth Opportunities & Product Line Extension Strategy: Determines white space opportunities in the segment of implantable grade batteries, rechargeable lithium batteries, LiPo batteries, batteries for medical carts, power solution for wearable devices, home healthcare batteries, customized batteries packs and future generation medical micro-batteries.

Key Procurement Priorities and Buyer Evaluation Criteria

- Buyers in the Global Medical Batteries Market are increasingly prioritizing batteries that deliver longer runtime, high energy density, stable discharge performance, compact design, strong safety profile and reliable operation across critical medical devices.

- Procurement decisions are shifting toward medical-grade battery solutions that support implantable devices, portable monitors, infusion pumps, medical carts, hearing aids, respiratory devices and home healthcare equipment with consistent performance and lower replacement burden.

- Medical device OEMs, hospitals, clinics, diagnostic centers, home healthcare providers and emergency care teams are evaluating vendors based on battery life, chemistry suitability, device compatibility, regulatory compliance, quality certifications, supply reliability, customization capability and total cost of ownership.

- Vendors with strong capabilities in lithium primary batteries, rechargeable lithium-ion and lithium-polymer batteries, custom battery packs, implantable-grade batteries, medical cart power systems and aftermarket replacement batteries are better positioned to win long-term OEM and healthcare procurement contracts.

Access and Download the Full Market Data

The complete, multi-tiered publication provides definitive metrics on market sizing splits, battery chemistry performance curves, specific application use-cases, and regional regulatory compliance frameworks through 2035.

Data Availability Notice: To download the primary statistical datasets, interactive market charts, and comprehensive executive summaries, secure your copy through the official intelligence platform:

Download the Global Medical Batteries Market Research Report (2026 - 2035)