Japan Biologic Drug Lifecycle Management Market Overview

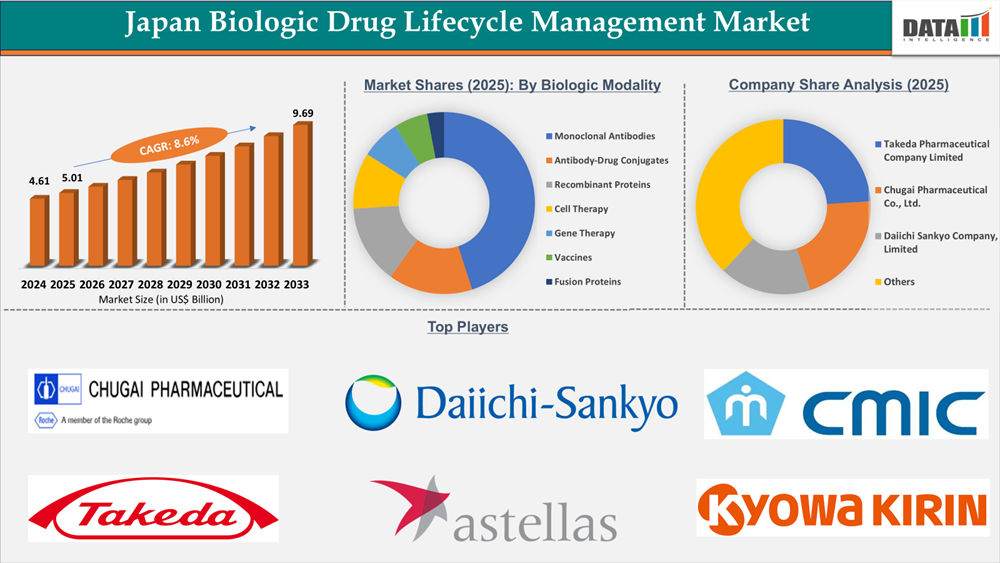

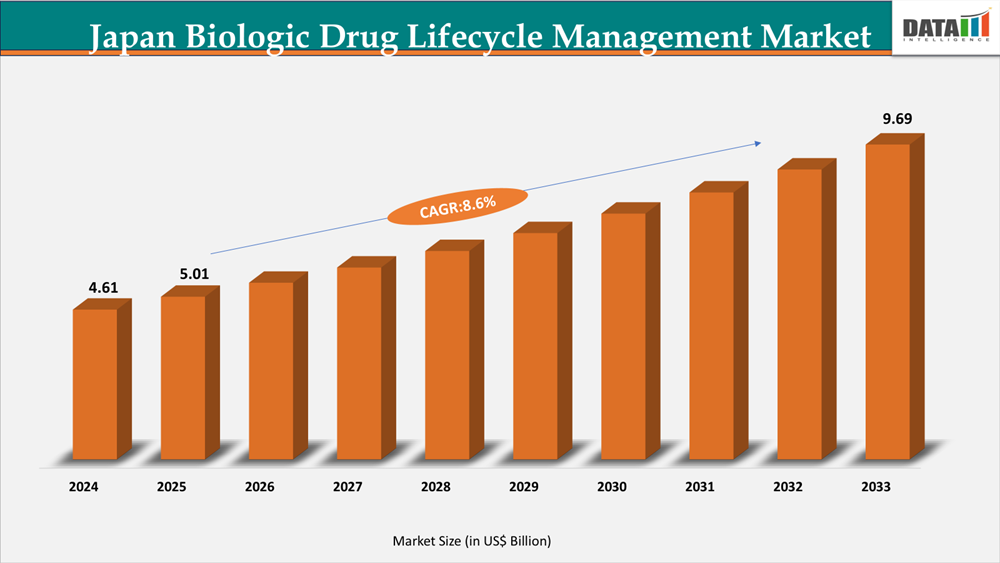

The Japan Biologic Drug Lifecycle Management Market reached US$4.61 Billion in 2024, rising to US$5.01 Billion in 2025 and is expected to reach US$9.69 Billion by 2033, growing at a CAGR of 8.6% from 2026 to 2033.

Japan's Biologic Drug Lifecycle Management market is shaped by robust biologics uptake, a highly controlled reimbursement system, and sustained national healthcare spending. According to the MHLW, Japan's overall healthcare expenditure exceeds USD 294 billion per year, with biologics accounting for an increasing share of high-cost pharmaceutical expenditure, particularly in oncology, immunology, and rare disorders. Every year, the country reports over 1 million new cancer cases (National Cancer Center Japan), and roughly 29% of the population is 65 years or older, indicating a long-term demand for sophisticated biologic therapy.

Drugs are subject to biennial price modifications under Japan's National Health Insurance (NHI) framework, which frequently lower prices for established items. This pricing environment forces biologic manufacturers to use structured lifecycle strategies such as indication expansion, line extensions, subcutaneous reformulations, pediatric approvals, manufacturing optimization using ICH-aligned standards, and patent term extensions reviewed by the Pharmaceuticals and Medical Devices Agency (PMDA). In parallel, government measures encouraging biosimilars to control pharmaceutical spending boost competitive pressure once patents expire. As a result, in Japan, lifecycle management functions as both a commercial growth strategy and a regulatory need for maintaining product differentiation, exclusivity, and long-term revenue stability in a disciplined healthcare market.

Biologic Drug Lifecycle Management Market Industry Trends and Strategic Insights

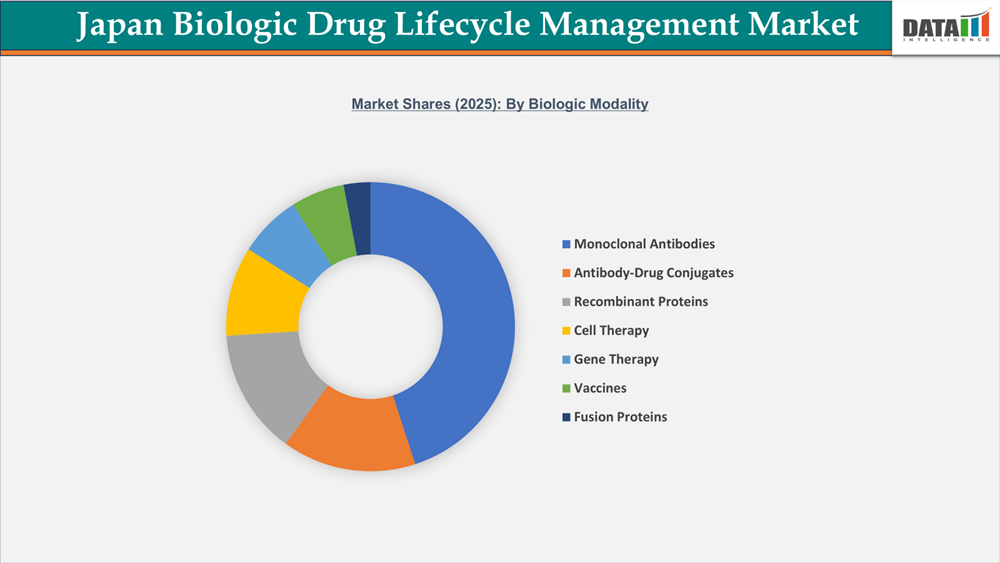

- By Biologic Modality segment, Monoclonal Antibodies (mAbs) led the Japan Biologic Drug Lifecycle Management Market, capturing the largest revenue share of 45% in 2025.

Japan Biologic Drug Lifecycle Management Market Size and Future Outlook

- 2025 Market Size: US$5.01 Billion

- 2033 Projected Market Size: US$9.69 Billion

- CAGR (2026–2033): 8.6%

Market Dynamics

Growth of Advanced Biologic Modalities

The expansion of advanced biological products, such as cell and gene therapies and antibody-drug conjugates (ADCs), bispecific antibodies, and monoclonal antibodies (mAbs) has been a major factor in driving the Japanese market for biologics through lifecycle management. In all therapeutic areas (oncology, rare disease, and regenerative medicine), Japan has strong scientific and regulatory support for these novel therapies. Because of their complexities, costs, and need for long-term post-approval safety surveillance, advanced biologics require a continuous generation of post-market data, an ongoing optimization of manufacturing processes, and a comprehensive strategy for indication expansion. Japan's pro-active regulatory process for regenerative medicine supports efficient timeline development from pre-approval to market entry and therefore makes structured lifecycle planning a key strategy for managing both long-term clinical follow-up and the commercial viability of advanced biologic products. Premium pricing for advanced biologics under the National Health Insurance system requires the ongoing generation of real-world evidence and the demonstration of value, which further underscores the need for comprehensive lifecycle management strategies.

Data Generation & Real-World Evidence Challenges

Challenges in Data Generation and Real-World Evidence (RWE) represent a constraint, since biological lifecycle strategies primarily rely on post-marketing clinical data as evidence that can support post-marketing clinical data, support for pricing justification, and long-term safety validation through additional studies. In Japan, challenges related to fragmented hospital databases, insufficiently standardized data, privacy regulations, and long follow-up times, primarily associated with advanced therapies, can result in delays in the generation of evidence. The result is that these challenges can create a bottlenecking effect on regulatory approvals, reimbursement negotiations, and lifecycle extension efforts, and subsequently restrain growth in the market.

Segmentation Analysis

The Japan Biologic Drug Lifecycle Management Market is segmented based on lifecycle phase, lifecycle strategy type, biologic modality, therapeutic area, business model, lifecycle support services and end user.

Monoclonal Antibodies Drive Growth in Japan’s Biologic Drug Lifecycle Management Market

Monoclonal antibodies (mAbs) form the largest part of all the biologics created to manage a drug’s lifecycle within Japan, especially in the management of oncological and chronic diseases. With a projected number of greater than 1,023,100 cancers diagnosed in 2025 cancer, there will be a continued long-term need for targeted therapies to be optimized across multiple indications and treatment regimens for years to come. mAbs are becoming more common as first-line therapies and post-chemotherapy maintenance therapies, with the use of mAbs, such as avelumab in post-chemotherapy maintenance therapy for urothelial carcinoma patients, among many patients older than the median age. mAbs in Japan will continue to be managed throughout their lifecycle by expanding their indications, adjusting the mode of administration and route of delivery, and providing real-world data from extensive post-marketing surveillance systems to help provide extended duration of therapy and improved clinical outcomes; this will further position mAbs as a fundamental pillar of any biologics strategy, as well as being integrated into any strategy of use of a biologic based on long-term utilization, in the course of Japan's healthcare reform process.

Competitive Landscape

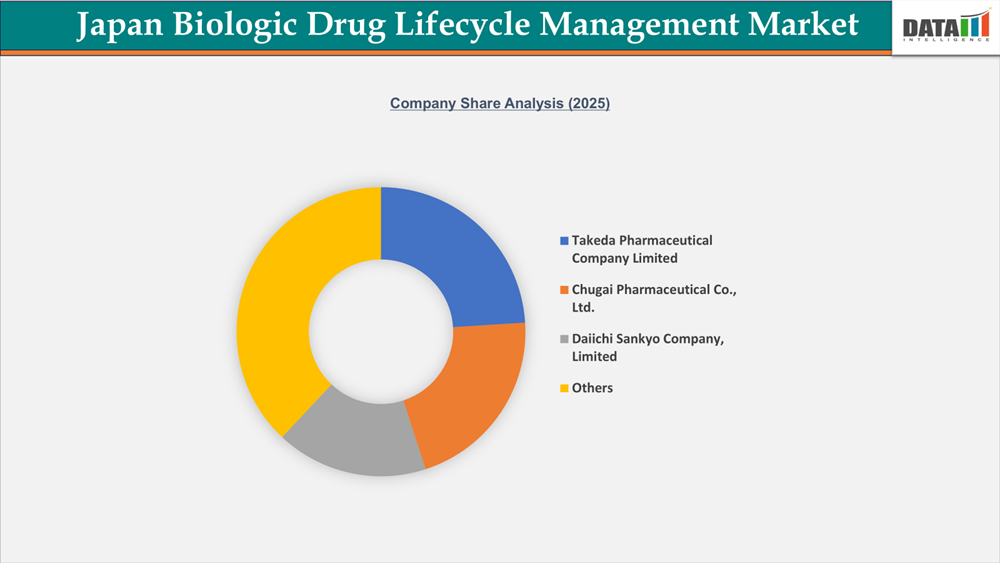

The Japan Biologic Drug Lifecycle Management Market is moderately concentrated, with leading domestic innovators including Takeda Pharmaceutical Company Limited, Chugai Pharmaceutical Co., Ltd., and Daiichi Sankyo Company, Limited. These firms achieve market leadership by leveraging strong biologics pipelines, indication growth plans, formulation optimization, and global commercialization skills. To maximize long-term asset value, their lifecycle management strategies include label extensions, combination medicines, next-generation biologics, and strategic portfolio prioritization. Other important firms, such as Astellas Pharma Inc., Kyowa Kirin Co., Ltd., Eisai Co., Ltd., Otsuka Pharmaceutical Co., Ltd., and JCR Pharmaceuticals Co., Ltd., maintain a strong position through specialty biologics, rare disease therapeutics, cancer antibodies, and biosimilar development. Contract research and lifecycle support firms, such as CMIC Holdings Co., Ltd. and EPS Holdings, Inc., contribute by providing regulatory advice, post-marketing surveillance, and clinical development services, thereby improving lifecycle execution efficiency.

Competitive market strategies are increasingly focusing on indication extension, formulation innovation, real-world evidence gathering, digital integration in medication research, and strategic worldwide collaborations. As Japan's aging population increases demand for oncology, immunology, and rare disease biologics, businesses are focusing on long-term market competitiveness through sustainable lifetime value creation and portfolio diversity.

Key Developments

- In 2025, Chugai Pharmaceuticals and Rani Therapeutics made a deal allowing them to work together on developing an oral antibody treatment that will utilize state-of-the-art drug delivery systems. This collaboration has been designed to revolutionize the way biologics are delivered, providing patients with greater convenience than ever before, as well as enhancing the lifetime value of these products beyond current injectable formulations.

- In 2024, Astellas Pharma Inc. received regulatory approval from the MHLW for VYLOY™ (zolbetuximab), a first-in-class antibody therapy used in the treatment of gastric cancer, to enhance its oncology biologics portfolio and lifecycle positioning in primary markets.

What Sets This Japan Biologic Drug Lifecycle Management Market Intelligence Report Apart

- Latest Data & Forecasts – Comprehensive and up-to-date market intelligence with forecasts through 2033, covering Japan demand by key segmentation including the lifecycle phase, lifecycle strategy type, biologic modality, therapeutic area, business model, lifecycle support services and end user.

- Regulatory Intelligence – In-depth analysis of Japan's regulatory environment influencing biologic lifecycle strategies, including PMDA approval pathways, regenerative medicine frameworks, re-examination systems, post-marketing surveillance (PMS) requirements, biosimilar guidelines, pricing revisions under the National Health Insurance (NHI) system, patent exclusivity, and label expansion processes.

- Competitive Benchmarking – Structured benchmarking of prominent Japanese and global biopharma firms based on biologic portfolio maturity, lifecycle extension tactics, pipeline strength in advanced biologics, biosimilar defensive strategies, partnership models, and commercialization approaches inside Japan.

- Actionable Strategies & Cost Dynamics – Strategic insights into biologic lifecycle optimization, including indication sequencing, real-world evidence utilization, pricing pressure management during periodic NHI revisions, biosimilar competition risks, manufacturing complexity, supply chain considerations, and long-term value maximization strategies, are supported by perspectives from regulatory experts, clinical researchers, and biopharmaceutical executives.