Electric Vehicle Testing, Inspection and Certification Market Overview

The global electric vehicle testing, inspection and certification market reached US$ 2.99 Billion in 2025 and is expected to reach US$ 5.71 billion by 2033, growing at a CAGR of 9.94 % from 2026 to 2033.

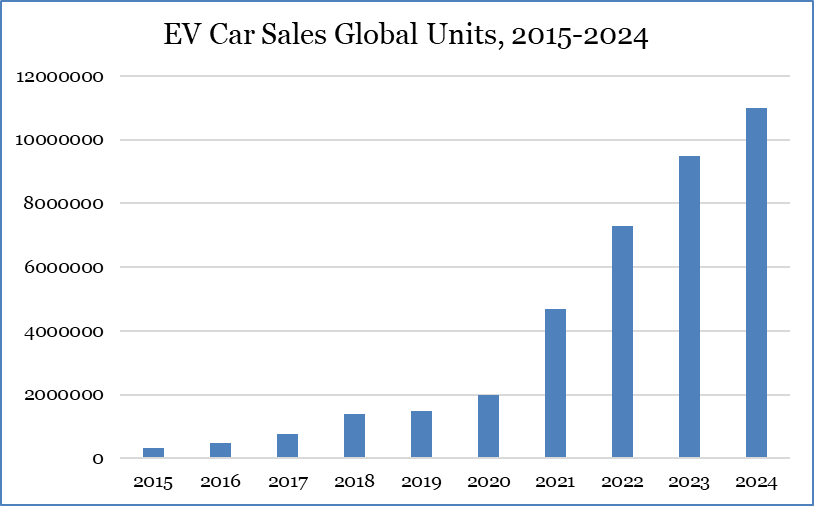

The global electric vehicle (EV) testing, inspection, and certification (TIC) market plays a critical role in enabling the growth of the EV ecosystem, ensuring compliance with stringent safety, performance, and regulatory standards for batteries, powertrains, and charging infrastructure. The growth is underpinned by the explosive rise in EV adoption, with global sales surpassing 14 million units in 2024, a 25% year-over-year increase, driven by net-zero emission goals and subsidies in regions like Europe and China.

Stringent regulations, such as the EU's Euro NCAP updates mandating advanced driver-assistance systems (ADAS) testing and China's GB/T standards for battery safety, amplify demand, as EVs must undergo rigorous validation to mitigate risks like thermal runaway, which affected 1 in 5,000 battery packs in 2024 recalls.

Electric Vehicle Testing, Inspection and Certification Market Industry Trends and Strategic Insights

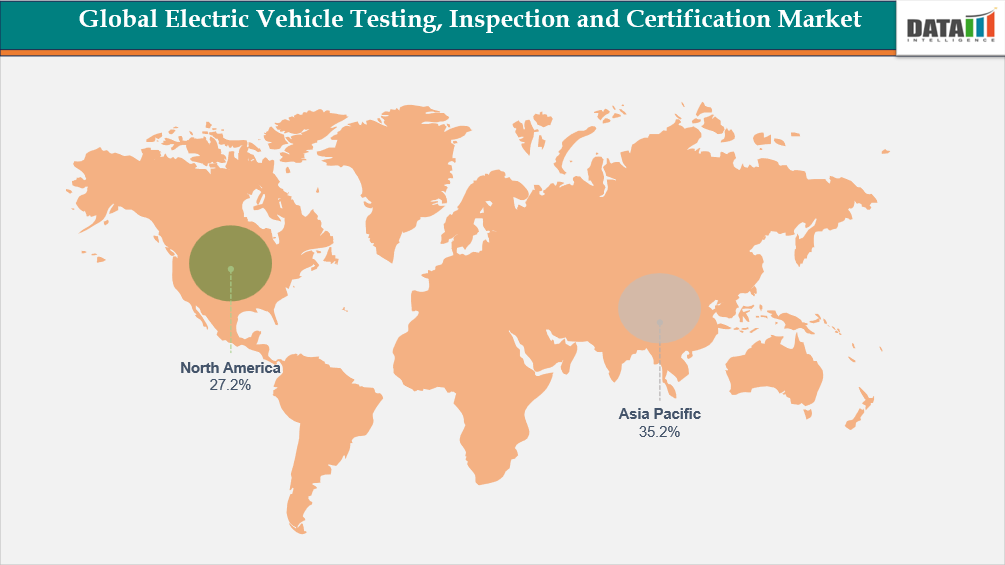

- Asia-Pacific leads the global electric vehicle testing, inspection and certification market, capturing the largest revenue share of 35.2% in 2024.

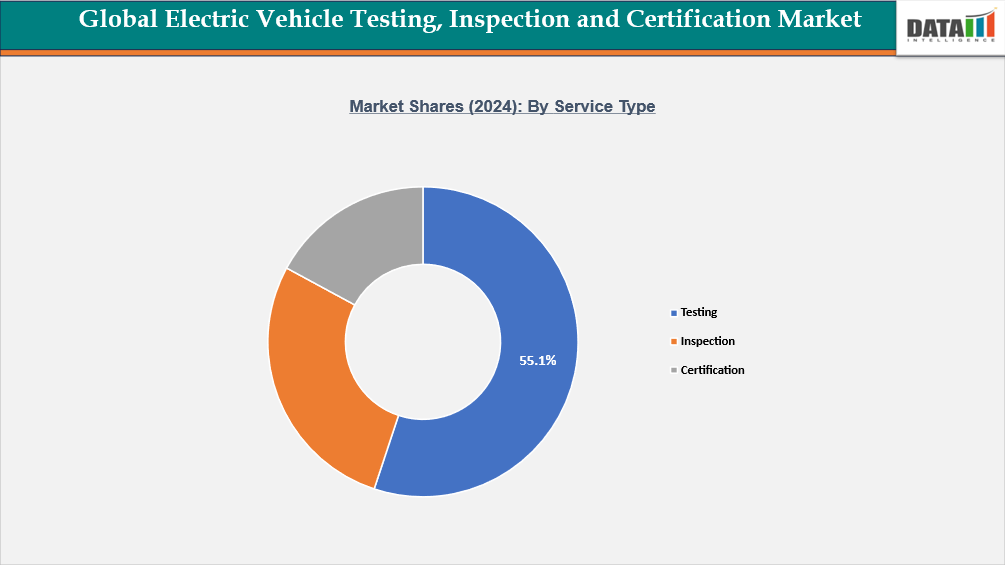

- By testing segment leading the global electric vehicle testing, inspection and certification market, capturing the largest revenue share of 55.1% in 2024.

Global Electric Vehicle Testing, Inspection and Certification Market Size and Future Outlook

- 2025 Market Size: US$ 2.99 Billion

- 2032 Projected Market Size: US$ 5.71 Billion

- CAGR (2025–2033): 9.94 %

- Dominating Market: Asia-Pacific

Market Scope

| Metrics | Details |

| By Service Type | Testing, Inspection and Certification |

| By Service Category | Electrical Safety Testing, Performance Testing, Conformance and Interoperability Testing, Functional Safety Testing, EMC Testing, Wireless Testing, Software Testing, Environmental & Stress Testing, Chemical Testing and Others |

| By Application | Battery Systems, Charging Infrastructure, Electric Motors & Propulsion, Safety & Security Systems, Electric Systems & Components, Electronics, Interior/Exterior Materials & Bodies, Software and Others |

| By Vehicle Type | BEV (Battery Electric Vehicle), PHEV (Plug-in Hybrid), HEV (Hybrid), FCEV (Fuel Cell Electric Vehicle) |

| By End-user | Automotive OEMs, Component Manufacturers and Government Agencies |

| By Region | North America, South America, Europe, Asia-Pacific, Middle East and Africa |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth |

For More Detailed information, Request for Free Sample

Market Dynamics

Rising Battery Safety Incidents and Stringent Global Regulations Drive Demand for Global Electric Vehicle Testing, Inspection and Certification Market

One pivotal driver propelling the global electric vehicle testing, inspection, and certification (TIC) market is the escalating prevalence of battery safety incidents and stringent regulatory mandates, which necessitate rigorous validation to avert risks like thermal runaway and fires. In 2024, over 500,000 EVs were recalled worldwide due to battery (ICCU) defects as reported by the National Highway Traffic Safety Administration (NHTSA) and China's State Administration for Market Regulation (SAMR). This surge underscores the urgency for comprehensive TIC services, particularly as lithium-ion battery packs, which comprise 40% of an EV's cost, face vulnerabilities exposed in high-profile cases, such as Li Auto's recall of 11,411 Mega models in November 2025 for coolant flaws triggering potential fires.

Regulatory frameworks amplify this demand; the European Union's Battery Regulation (effective August 2025) requires third-party certification for recycled content and carbon footprint tracking, while China's GB/T 36276 standard mandates annual safety audits for all EV batteries, covering 60% of global production. Consequently, TIC compliance costs for manufacturers have climbed, driving outsourcing to specialized firms like TÜV SÜD and SGS.

These pressures not only ensure consumer trust but also foster innovation in predictive testing, such as AI-driven simulations that reduce failure rates by 30%, per International Electrotechnical Commission (IEC) benchmarks. Overall, the market is expected to witness sustained expansion, safeguarding the EV sector's integrity amid projections of 20 million annual sales by year-end.

Segmentation Analysis

The global electric vehicle testing, inspection and certification market is segmented based on service type, service category, application, vehicle type, end-user and region.

Advancements in EV Software and ADAS Integration Propel Testing Segment Growth

The testing segment within the global electric vehicle (EV) testing, inspection, and certification (TIC) market is surging due to the rapid integration of advanced software-defined architectures and ADAS features, demanding rigorous validation for real-time performance and cybersecurity. ADAS-equipped EVs necessitate over 1,000 hours of software testing per vehicle to comply with ISO 26262 standards.

Emerging over-the-air (OTA) update protocols further intensify this demand, with 40% of 2025 EV models requiring continuous testing cycles to maintain type approval under UNECE WP.29 regulations. Outsourced testing labs, such as those from Intertek, reported a 28% increase in ADAS validation contracts in 2024, reflecting OEMs' shift from in-house to specialized facilities amid talent shortages.

These innovations not only mitigate risks like phantom braking incidents, which affected 12% of ADAS vehicles in U.S. NHTSA reports for 2024, but also unlock revenue streams through recurring OTA re-certifications. The testing segment's dominance positions it as the market's growth engine, fostering AI-driven tools that cut validation time by 35% while ensuring seamless integration of V2X communications.

The Battery Systems are fueled by rising demand for safety, reliability, and compliance in energy storage technologies.

Battery systems represent the most valuable and sensitive component of electric vehicles, requiring rigorous testing for performance, durability, and safety. Increasing concerns over thermal runaway, fire hazards, and charging efficiency have intensified the need for standardized inspection protocols. As EV adoption accelerates, certification ensures batteries meet international safety benchmarks, supporting consumer confidence and regulatory compliance.

Global EV battery demand is increasing, with lithium-ion batteries dominating the growth. This surge drives the need for advanced TIC services to validate energy density, lifecycle performance, and recycling standards. Agencies emphasize certification to mitigate risks associated with high-capacity batteries, particularly in fast-charging applications. The growing complexity of battery chemistries further strengthens the role of TIC providers in ensuring safe deployment.

Geographical Penetration

DOMINATING MARKET:

Government Policies and Incentives Fuel Asia-Pacific's Dominance

The Asia-Pacific (APAC) region is a leader in the global Electric Vehicle (EV) Testing, Inspection, and Certification (TIC) market, driven by aggressive government policies and incentives that accelerate EV manufacturing and adoption, necessitating extensive compliance testing. In 2024, China produced 12.4 million EVs, according to the International Energy Agency (IEA). These policies, including China's "New Energy Vehicle Industry Development Plan (2021–2035)", target 20% EV sales penetration by 2025.

China Electric Vehicle Testing, Inspection and Certification Market Insights

Incentives like subsidies, tax rebates, and infrastructure investments have doubled China's charging units to 5.2 million in 2022, fostering a testing ecosystem for battery safety and emissions under GB/T standards. This regulatory push mandates third-party TIC, elevating APAC's TIC demand as firms like CATL and BYD scale operations.

India Electric Vehicle Testing, Inspection, and Certification Market Industry Growth

Growth in India is fueled by increasing demand for battery safety validation, charging infrastructure compliance, and international certification for exports. With India’s ambitious EV targets and localization of battery manufacturing, TIC services are becoming essential to ensure reliability, consumer trust, and regulatory alignment.

SECOND LARGEST MARKET:

Europe is the Second-Largest Region Driven by Stringent Regulatory Frameworks, Rapid EV Adoption, and Sustainability Mandates.

The region’s growth is fueled by the European Union’s Green Deal, which mandates carbon neutrality by 2050, pushing automakers to accelerate EV deployment. Rising EV sales, which surpassed 3.2 million units in 2023, intensify demand for battery safety validation, charging infrastructure compliance, and recycling certification. Advances in digital diagnostics, including AI-enabled testing and predictive analytics, enhance efficiency and accuracy. With leading TIC providers such as TÜV SÜD and DEKRA headquartered in Europe, the region remains central to global EV safety and compliance

Germany Electric Vehicle Testing, Inspection and Certification Market Outlook

Germany’s market benefits from its strong automotive base and leadership in EV innovation. The country’s EV market is supported by stringent environmental policies and government incentives. Automotive TIC services, including crash, emission, and electrical system testing, are expanding to meet rising EV production. Germany’s engineering expertise and export-driven industry amplify the need for internationally recognized certification, ensuring vehicles meet EU and global standards. This positions Germany as a hub for advanced TIC services, aligning safety with innovation in electrified mobility.

UK Electric Vehicle Testing, Inspection and Certification Market Trends

The UK market is driven by government decarbonization targets and rising EV penetration. Growth in the market is supported by the expansion of charging infrastructure, battery safety requirements, and homologation testing for exports. Certification services are critical as the UK strengthens its regulatory framework to align with EU and global standards. The combination of policy support and consumer demand ensures TIC providers play a pivotal role in enabling safe and sustainable EV adoption.

Sustainability and ESG Analysis

The sustainability of the market lies in its ability to ensure safe, reliable, and environmentally responsible mobility. By validating batteries, charging systems, and vehicle components, TIC reduces risks of accidents, enhances energy efficiency, and supports recycling initiatives. Certification frameworks also promote circular economy practices, enabling the use of second-life batteries and reducing waste. As governments tighten emission standards and consumers demand greener solutions, TIC providers play a pivotal role in strengthening trust, compliance, and accelerating the transition toward sustainable electric transportation worldwide.

Competitive Landscape

- The global electric vehicle testing, inspection and certification market is competitive, characterized by the presence of numerous multinational corporations and regional players. Key companies present are Eurofins Scientific, DEKRA, SGS SA, Bureau Veritas, TUV Rheinland, TUV SUD, Intertek Group, UL LLC, DNV,Applus+

- Leading players such as SGS SA, TÜV SÜD, Bureau Veritas SA, and Intertek Group plc pursue strategic partnerships with automakers, enabling early integration of compliance into product development.

- Firms are expanding through regional accreditation and localized services, balancing cost efficiency with credibility.

- Outsourcing and in-house hybrid models are enhancing flexibility, while digital platforms for certification management are improving client engagement. Success hinges on combining technical expertise, accreditation, and global scalability to capture rising EV demand.

Key Developments

- In December 2024, SGS SA launched a comprehensive “single source” ESG solution under its IMPACT NOW sustainability suite, integrating testing, inspection, certification, and advisory services to help organizations manage environmental, social, and governance compliance and reporting.

- In November 2025, UL Solutions expanded its battery-powered vehicle testing services to include electric motorcycles, scooters, and construction, agriculture, and mining vehicles, introducing new certification programs to address electrical system safety, battery risks, and regulatory compliance requirements.

What Sets This Global Electric Vehicle Testing, Inspection and Certification Market Intelligence Report Apart

- Latest data and forecasts: Comprehensive, up-to-date insights through 2032 covering EV Service Type, Service Category, Application, Vehicle Type, and End-user.

- Regulatory intelligence: Detailed analysis of UN ECE regulations, ISO/IEC standards, regional homologation pathways, safety and EMC directives, cybersecurity requirements, and charger/grid compliance frameworks.

- Competitive benchmarking: Profiles and strategies of top TIC providers and emerging innovators, mapped by service breadth, lab footprint, accreditation scope, sector focus, and turnaround performance.

- Emerging market coverage: Opportunities and localization strategies in Asia-Pacific, Africa, and Latin America, including public policy momentum, grid readiness, and OEM-TIC collaboration models.

- Actionable strategies: Guidance on accelerating certification cycles, optimizing outsourced vs in-house testing, leveraging digital twins and simulation, and maximizing ROI across multi-standard compliance.

- Pricing and cost analysis: Detailed breakdown of typical test program costs, lab utilization economics, accreditation impacts, bundled service pricing, and cost-benefit trends for OEMs and suppliers.

- Expert analysis: Insights from specialists in EV TIC engineering, functional safety, EMC, cybersecurity, battery reliability, and charging infrastructure conformance.