Global Construction Drone Market: Industry Outlook

The global construction drone market reached US$8.72 billion in 2025 and is expected to reach US$24.30 billion by 2035, growing at a CAGR of 12.07% during the forecast period 2026–2035.

The global construction drone market is growing steadily, supported by increasing use in surveying, site monitoring, project tracking, and infrastructure inspection. Drones are becoming indispensable for improving construction quality, enhancing worker safety, and ensuring projects stay on schedule. This growth is further fueled by advancements in AI-driven analytics, autonomous flight systems, and real-time data capture, alongside rising investment in digital construction and smart infrastructure. Strategic partnerships between drone makers, software providers, and construction companies are also reshaping industry dynamics by offering integrated and scalable solutions.

The US holds a leading position in the construction drone market, driven by strong adoption in large-scale infrastructure and data center projects. In 2025, Drone Deploy secured nationwide US Beyond Visual Line of Sight (BVLOS) approval for critical infrastructure, reinforcing its leadership in reality capture and robotics for construction monitoring. More than 84% of its top 50 projects now focus on data center and infrastructure development worth US$35 billion, with its advanced platform helping contractors and developers boost efficiency, safety, and decision-making. Backed by technological innovation and extensive industry adoption, the US continues to set the pace for global market growth.

Japan is also emerging as a key market, where drones are being used for regular, minimally intrusive site surveys to detect issues early and keep projects on track. For instance, In 2024, NTT Communications, Skydio’s business partner and a leading ICT solutions provider, successfully applied Skydio’s drone and dock technology to monitor indoor construction progress. This highlights Japan’s growing focus on digital construction, precision monitoring, and proactive problem-solving to reduce delays and improve efficiency. With increasing partnerships and rapid adoption of drone-based solutions, Japan is strengthening its role as one of the fastest-growing construction drone markets in the region.

Key Takeaways

- The construction drone market is expected to expand from US$ 8.72 billion in 2025 to US$ 24.30 billion by 2035, reflecting sustained investment in digital construction technologies.

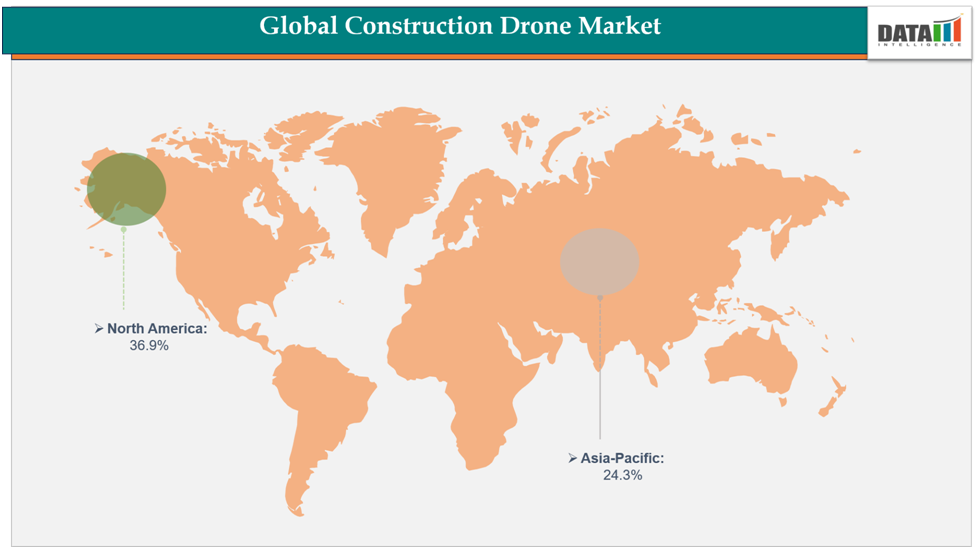

- North America accounted for 36.9% of global revenue in 2024, supported by infrastructure modernization, commercial construction activity, and widespread drone adoption.

- Asia Pacific represents the fastest growing regional market as governments increase spending on transportation, industrial facilities, and smart city developments.

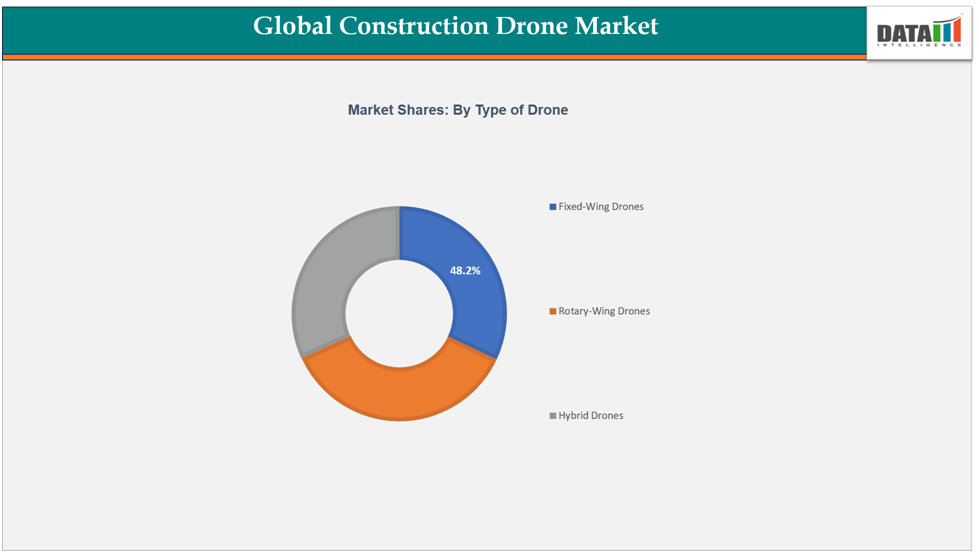

- Rotary wing drones continue to lead product demand with an estimated 48.2% market share, owing to their operational flexibility for surveying, inspection, and site monitoring.

- AI powered analytics, autonomous navigation, LiDAR integration, and cloud connected workflows are becoming important competitive differentiators across Construction Drone top companies.

- Long term revenue opportunities increasingly extend beyond drone hardware into software subscriptions, analytics services, maintenance, training, and fleet management.

Market Scope

| Metric | Details |

| Market Size (2025) | US$ 8.72 Billion |

| Market Size (2035) | US$ 24.30 Billion |

| CAGR | 12.07% |

| Historic Years | 2023 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Segments Covered | Drone Type, Component, Technology, Application, Region |

| Leading Region | North America |

| Fastest Growing Region | Asia Pacific |

Drivers & Restraints

Driver: Advancements in Technology

The global construction drone market is being propelled by rapid technological innovations, including AI-driven analytics, autonomous flight capabilities, real-time data capture, and high-resolution imaging. These advancements enable construction professionals to efficiently conduct site surveys, monitor progress, detect potential issues early, and optimize project timelines with minimal manual intervention. Furthermore, drones are increasingly integrated with AI for structural safety and emergency management. For instance, the Delhi Police plan to monitor under-construction buildings using drones and create AI-based structural models to provide immediate assistance when required. This system not only identifies structural vulnerabilities but also allows for quick emergency response, highlighting the critical role of technology in enhancing both safety and operational efficiency.

Restraint: Regulatory and Airspace Restrictions

Construction drones face operational challenges due to strict regulations and airspace limitations. Rules on line-of-sight, flight permissions, altitude, and no-fly zones especially in urban areas or near critical infrastructure can restrict deployment. Compliance adds administrative burden, increases costs, and may delay projects. Privacy laws and inconsistent regional standards further limit large-scale adoption, making regulatory constraints a key barrier to market growth.

Digital Construction Investment Is Expanding the Market

Construction organizations are moving toward connected project management environments where drones collect accurate field data that supports planning, scheduling, quality assurance, and compliance. Compared with traditional surveying methods, drone-based workflows significantly reduce inspection time while providing high-resolution imagery, three-dimensional mapping, and real-time progress reporting.

Growing investment in highways, airports, industrial plants, renewable energy facilities, commercial buildings, and data centers is increasing demand for construction drones capable of delivering consistent project intelligence throughout the construction lifecycle.

Technology Innovation Continues to Improve Construction Drone Automation ROI

Rapid improvements in autonomous flight systems, AI-based image analysis, thermal imaging, LiDAR sensors, and cloud computing have expanded drone capabilities well beyond aerial photography. Construction firms now use automated drone missions for volumetric calculations, structural inspections, progress validation, asset documentation, and predictive maintenance planning.

Improved automation reduces manual surveying requirements while enabling project managers to make faster operational decisions. As software platforms become increasingly integrated with BIM, GIS, and digital twin environments, Construction Drone automation ROI continues to improve for contractors managing multiple projects simultaneously.

Regulatory Environment Remains a Critical Business Consideration

Although drone adoption continues to accelerate, regulatory compliance remains an operational challenge. Airspace restrictions, flight permission requirements, altitude limitations, and beyond visual line of sight regulations influence deployment strategies across different countries.

Privacy regulations and varying aviation standards also increase implementation complexity for multinational construction companies. Organizations investing in drone operations increasingly prioritize regulatory compliance software, pilot certification, and standardized operational procedures to minimize project disruptions.

Commercial Opportunities Across the Construction Drone Ecosystem

Manufacturers have opportunities to develop lighter, longer endurance platforms equipped with AI-enabled sensors, while software companies can expand recurring revenues through cloud-based analytics, digital inspection platforms, and project management integration.

Construction drone pricing and adoption trends also indicate growing demand for bundled hardware and software offerings rather than standalone drone sales. Service providers offering surveying, inspection, maintenance, training, fleet management, and regulatory support can benefit from organizations seeking outsourced drone operations instead of maintaining internal teams.

Infrastructure developers, EPC contractors, engineering consultants, mining companies, utilities, renewable energy operators, and transportation agencies are expected to remain key buyers through 2035 as drone-enabled workflows become part of standard project execution.

Hardware and Software Stack Is Becoming Increasingly Integrated

The construction drone ecosystem is evolving into a connected technology platform rather than a hardware-only market. Modern deployments typically combine high-resolution cameras, LiDAR sensors, thermal imaging equipment, autonomous flight controllers, cloud analytics platforms, AI-based image processing, and project management software.

This integrated hardware software stack enables continuous site documentation, automated inspection reporting, volumetric measurement, digital twins, and collaboration across engineering, procurement, and construction teams. Vendors capable of providing complete workflow solutions are likely to strengthen customer retention while generating recurring software and support revenues.

Industry Use Cases Continue to Expand

Construction drone use cases by industry extend well beyond traditional surveying.

Commercial real estate developers rely on drones for construction progress verification and stakeholder reporting. Infrastructure contractors use drones to inspect bridges, highways, railways, and utilities while reducing manual inspection risks. Mining operations benefit from volumetric analysis and stockpile measurement, whereas renewable energy developers increasingly deploy drones for wind farm and solar project construction monitoring.

Industrial facilities, oil and gas infrastructure, ports, airports, and large manufacturing projects also represent expanding application areas as organizations seek greater operational visibility throughout asset construction.

Segmentation Analysis

The global construction drone market is segmented based on type of drone type, technology, application and region.

Type of Drone: The rotary-wing drones segment accounts for an estimated 48.2% of the global construction drone market.

The rotary-wing drones segment dominates the market, accounting for an estimated xx% share. Rotary-wing drones are valued for their versatility, precision, and ability to hover, making them ideal for site surveys, real-time monitoring, and safety inspections. Manufacturers focus on producing lightweight, durable, and energy-efficient platforms equipped with advanced sensors, cameras, and autonomous navigation systems.

Market growth is driven by demand for accurate site mapping, progress tracking, volumetric calculations, and automated inspections across residential, commercial, and infrastructure projects. North America remains the largest regional market due to extensive infrastructure projects and technological adoption, while Asia-Pacific is the fastest-growing region, fueled by rapid urbanization and government-backed construction initiatives.

Rotary-wing drones are expected to maintain their leading position in the market, supported by continued innovations in autonomy, AI integration, and energy efficiency. Despite regulatory challenges and operational costs, their ability to enhance construction quality, productivity, and safety is projected to sustain strong growth for this segment.

Geographical Analysis

The North America construction drone market was valued at 36.9% market share in 2024

The North America construction drone market held approximately 36.9% of the global market share in 2024, making it the largest regional contributor. Growth in the region is driven by extensive use of drones in large-scale infrastructure, commercial construction, and critical projects. The adoption of advanced technologies such as AI-powered analytics, autonomous flight, and real-time site monitoring is enhancing project efficiency, safety, and quality. Strong R&D capabilities, technological expertise, and an established ecosystem for drone operations continue to reinforce North America’s leading position in the global market.

The Asia-Pacific needle vibrator market was valued at 24.3% market share in 2024

The Asia-Pacific construction drone market is expected to be the fastest-growing region, supported by rising investments in urban development, industrial facilities, and large infrastructure projects. Countries including Japan, China, and South Korea are driving regional growth by using drones for frequent site inspections, progress tracking, and early detection of construction issues. Government-led infrastructure programs, rapid urbanization, and growing adoption of digital construction practices are accelerating the region’s share in the global construction drone market.

Competitive Landscape

The major players in the construction drone market include EagleNXT, DJI, Parrot Drones SAS., Propeller, 3DR, Inc, AeroVironment, Inc., JOUAV, Skycatch, Inc., Microdrones, Quantum-Systems GmbH

EagleNXT :EagleNXT is a prominent player in the global construction drone market, specializing in advanced drone platforms and software solutions for site monitoring, surveying, and construction management. Its drones are equipped with high-resolution cameras, LiDAR sensors, and AI-powered analytics, enabling accurate mapping, real-time progress tracking, and structural inspections. With strong R&D capabilities and strategic collaborations with construction firms and technology partners, EagleNXT drives innovation in autonomous flight, data capture, and project management solutions, reinforcing its position as a key contributor to enhancing efficiency, safety, and productivity in construction projects worldwide.

The global construction drone market report delivers a detailed analysis with 70 key tables, more than 66visually impactful figures, and 195 pages of expert insights, providing a complete view of the market landscape.