Chillers Market Overview

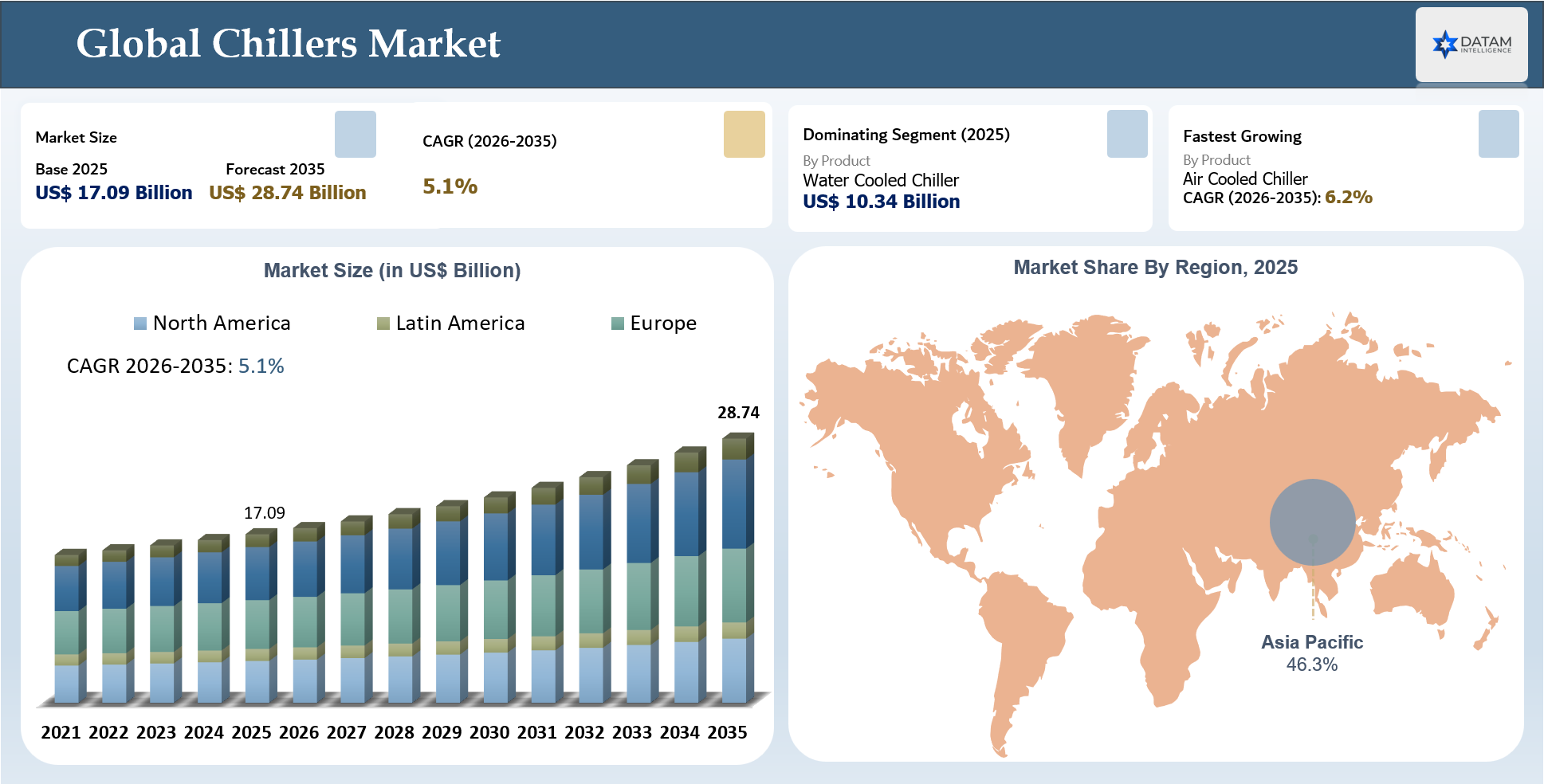

The Global Chillers Market stood at US$ 17.09 billion in 2025 and is expected to reach US$ 28.74 billion by 2035, growing with a CAGR of 5.1% during the forecast period 2026-2035.

Several factors are driving the growth of the global chillers market, including the ongoing switch to refrigerants with low global warming potential and advanced technology such as efficient chillers and digital HVAC systems. Consumers are abandoning traditional solutions due to higher expenses and less ability to manage them. There has been a rise in demand for inverter screw chillers, magnetic bearing centrifugal chillers, modular chillers, and digital control systems for their increased efficiency, lower energy consumption, and sustainability benefits.

In this regard, chillers have now become an integral part of infrastructure that enables uptime, process stability, and lifecycle management rather than just a tool for cooling purposes. Old machinery could lead to increased maintenance costs, unforeseen downtime and, in the future, refrigerant legislation. This opens a window of opportunity for providers who are able to integrate energy-efficient machinery, predictive maintenance solutions, building management system integration, heat recovery and effective after-sales services. As data centers, pharmaceuticals, food processing and precision manufacturing require continuous temperature control, procurement is shifting toward performance assurance, regulatory readiness and total cost of ownership.

Key Takeaways

- The Global Chillers Market was valued at US$ 17.09 billion in 2025 and is projected to reach US$ 28.74 billion by 2035.

- The market is expected to grow at a CAGR of 5.1% during the forecast period 2026-2035.

- Asia-Pacific held the highest market share at 46.3% in 2025, supported by strong industrial expansion, commercial construction, data center growth and process-cooling demand.

- Asia-Pacific is also expected to be the fastest-growing region, driven by manufacturing growth, smart building investments, cold-chain expansion, pharmaceuticals and data center cooling infrastructure.

- Water Cooled Chiller was the largest product segment in 2025, valued at approximately US$ 10.34 billion, supported by high cooling efficiency and strong adoption in large commercial and industrial facilities.

- Air Cooled Chiller is projected to be the fastest-growing product segment, expanding at an estimated 6.2% CAGR during 2026-2035.

- Data centers, food and beverage, pharmaceuticals, chemicals, plastics and commercial buildings are emerging as high-priority demand pockets for chiller manufacturers.

- Buyers are increasingly prioritizing energy efficiency, low-GWP refrigerants, smart controls, lower lifecycle cost and reliable after-sales service.

- The market has strong competitive participation from major players including Carrier Global Corporation, Daikin Industries, Ltd., Trane Technologies plc, Johnson Controls International plc and Mitsubishi Electric Hydronics & IT Cooling Systems S.p.A.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 17.09 Billion | |

| 2035 Projected Market Size | US$ 28.74 Billion | |

| CAGR (2026-2035) | 5.1% | |

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Type | Screw Chillers, Centrifugal Chillers, Absorption Chillers, Scroll Chillers and Reciprocating Chillers | |

| By Product | Air Cooled Chiller and Water Cooled Chiller | |

| By Power Range | Less Than 50 kW, 50 kW to 200 kW and More Than 200 kW | |

| By End-User | Plastics, Food and Beverage, Rubber, Printing, Medical and Pharmaceuticals, Chemicals, Alternative Energy and Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Disruption Analysis

Energy Efficiency, Refrigerant Transition and Smart Cooling Are Redefining Chiller Competitiveness

Disruption in the global chillers industry arises due to the move from traditional chiller units to highly efficient and environmentally friendly devices. The increased price of electricity, as well as energy efficiency regulations, have forced commercial and industrial facilities to upgrade their existing chillers to more efficient systems such as screw, centrifugal, magnetic bearing and inverters. This change in trends is forcing competition in the industry to evolve towards equipment supply combined with lifecycle services and compliance with new environmental regulations.

Simultaneously, rapidly increasing customer demands in data center cooling, pharmaceutical and chemical industries, food cooling, district cooling projects, and precision manufacturing require innovative chiller solutions. Today, customers require less costly units, reliable performance, small space occupancy, monitoring options, and the ability to use low global warming potential refrigerants. This trend provides a chance for innovative companies developing smart control systems, modular chillers, heat recovery technology, IoT monitoring, and tailored process cooling systems. At the same time, established vendors with traditional product lines experience strong competition from local firms and energy-efficient cooling equipment vendors.

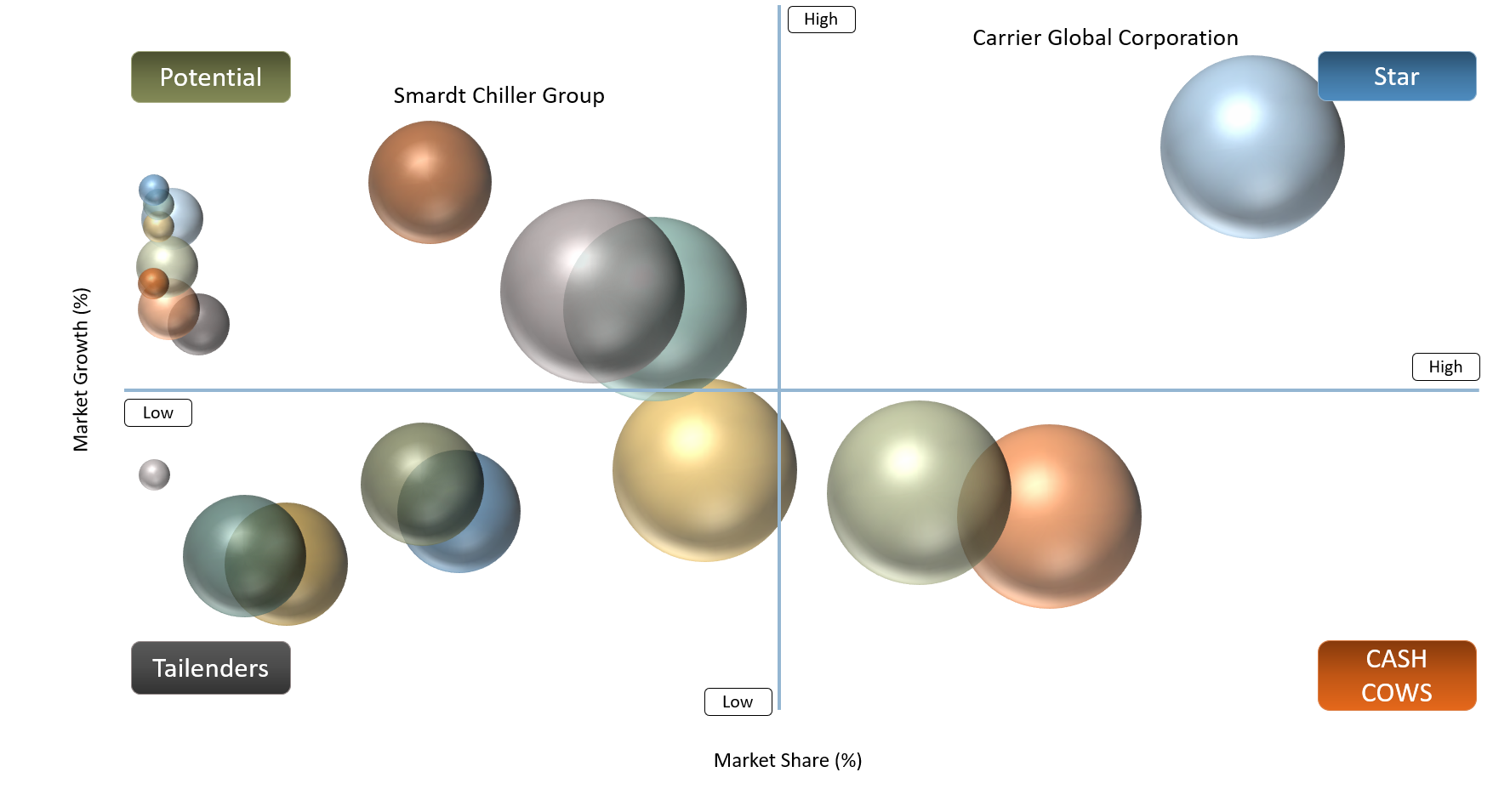

BCG Matrix: Company Evaluation

As for the BCG matrix, Stars in the Global Chillers Market include companies that are leaders in the HVAC industry on a global level, possess diversified ranges of chillers, have sophisticated energy-efficient technologies, well-established service networks and wide visibility among their commercial, industrial and data center cooling operations. Such companies as Carrier Global Corporation, Daikin Industries, Ltd., Trane Technologies plc, Johnson Controls International plc and Mitsubishi Electric Hydronics & IT Cooling Systems S.p.A. can serve as Stars thanks to their size, sophisticated technologies, capability of switching to low-GWP refrigerants, smart controls integration and prominence in valuable cooling solutions.

The cash cows of the global chillers market include companies that have a well-established market position, steady demand, loyal institutional and industrial consumers and regional or specific product portfolios. Such companies as LG Electronics Inc., Gree Electric Appliances, Inc. of Zhuhai, Midea Group, Thermax Limited, Danfoss A/S and Blue Star Limited can be regarded as Cash Cows for their long-established HVAC and cooling business, consistent demand from commercial buildings, industrial enterprises and infrastructure works and continued success in air-cooled, water-cooled, absorption and process chillers.

Question Marks are organizations that possess specialized capabilities in chiller technology but have relatively limited global reach or limited applicability. Smart Chiller Group, Dimplex Thermal Solutions, Drake Refrigeration, Inc. and PolyScience fall into the category of Question Marks since they are significant in oil-free centrifugal chillers, process cooling systems, industrial chillers and precision temperature control systems. The position of these firms in the future will depend on their ability to expand geographically, diversify in product offerings and increase energy efficiency.

Market Dynamics

Tremendously Improving Demand for Process Cooling in Industrial Applications Is Driving the Global Market Share for Chillers

Industrial process cooling is one of the key demand drivers for the Global Chillers Market since manufacturers have to ensure optimal temperatures to maintain product quality, efficiency, and uninterrupted operations. For instance, in the food and beverages processing, chillers are required for pasteurization, baking, fermenting, cooling, and packaging processes, where excessive heat may lead to variations in production outputs. In healthcare and pharmaceuticals, chillers play an important role in ensuring adequate cooling for medical imaging equipment, laser therapy devices, and laboratory apparatus, among others, and therefore, reliable cooling is crucial to operations.

Furthermore, there is a growing demand for semiconductors, plastic products, rubber, paper, cement, chemicals, petroleum products, power generation, and industrial automation sectors. With the growth in the number of machines used within industrial plants, customers purchase chillers that provide effective cooling, energy savings, reliability and better integration into the factory control systems. Initiatives such as government-backed industrialization, electronics manufacturing programs, and advanced manufacturing projects will contribute significantly towards construction and growth in production capacity, hence rising demand for screw chillers, centrifugal chillers, scroll chillers, and water-cooled chillers.

Stringent government regulatory standards and the high cost of chillers are hurdling the growth of the product

Higher capital intensity associated with industrial chillers continues to be a primary constraint for the Global Chillers Market. Generally, industrial chillers cost more compared to conventional commercial cooling systems because of their higher requirements for installation, controls, pipework, and commissioning & maintenance activities. Even today, several potential buyers continue to focus on initial costs when making decisions regarding equipment procurement. High-efficiency chillers may not get purchased because of this mindset, despite their proven benefits from lower energy consumption and lower downtime.

Furthermore, stricter environmental regulations are also increasing the challenge level. There are many instances where manufacturers and end users have to redesign, retrofit, or even replace their existing chillers because of limitations associated with refrigerants used by these machines. In particular, restrictions on high-GWP gases such as HFCs and F-gases become important issues for Europe. Consequently, equipment procurement becomes even more complicated for buyers, and vendors have to manage several aspects at once to keep the market growing.

Segmentation Analysis

The Global Chillers Market is segmented based on type, product, power range, end-user, and region.

Screw chillers are cleverly designed to work according to the requirements, offering high-quality functions in different applications

The global chillers market is segmented based on type into screw chillers, centrifugal chillers, absorption chillers, scroll chillers, and reciprocating chillers. Out of the mentioned chillers, screw chillers hold a dominating portion of the global chillers market. Screw chillers are cleverly designed to work according to the requirements. These chillers are made from high-quality materials obtained from reputable vendors. The quality management section closely monitors the development of these chillers.

Screw coolers use two interlocking revolving helical rotors to compress the refrigerant and can be air-cooled or water-cooled. A slider or speed control is used to control the capacity of the products. Different types of screw chillers are available in the market, including air-cooled screw chillers, water-cooled screw chillers, and industrial screw chillers.

The air-cooled screw chillers are suitable for working in extreme tropical weather conditions and maintaining energy and operational efficiency. The equipment is developed and built to the highest possible design and manufacturing standards. The environmentally friendly chillers are simple to install and have passed all of the necessary international tests to ensure they are up to par with the best.

Furthermore, Industrial screw chillers are designed and constructed for various cooling processes, each distinct from the others. The industrial chillers are made of high-quality materials and metallurgy, and they're equipped with Europe's most efficient compressors. Materials and metallurgies are selected based on the process fluid used and requirements.

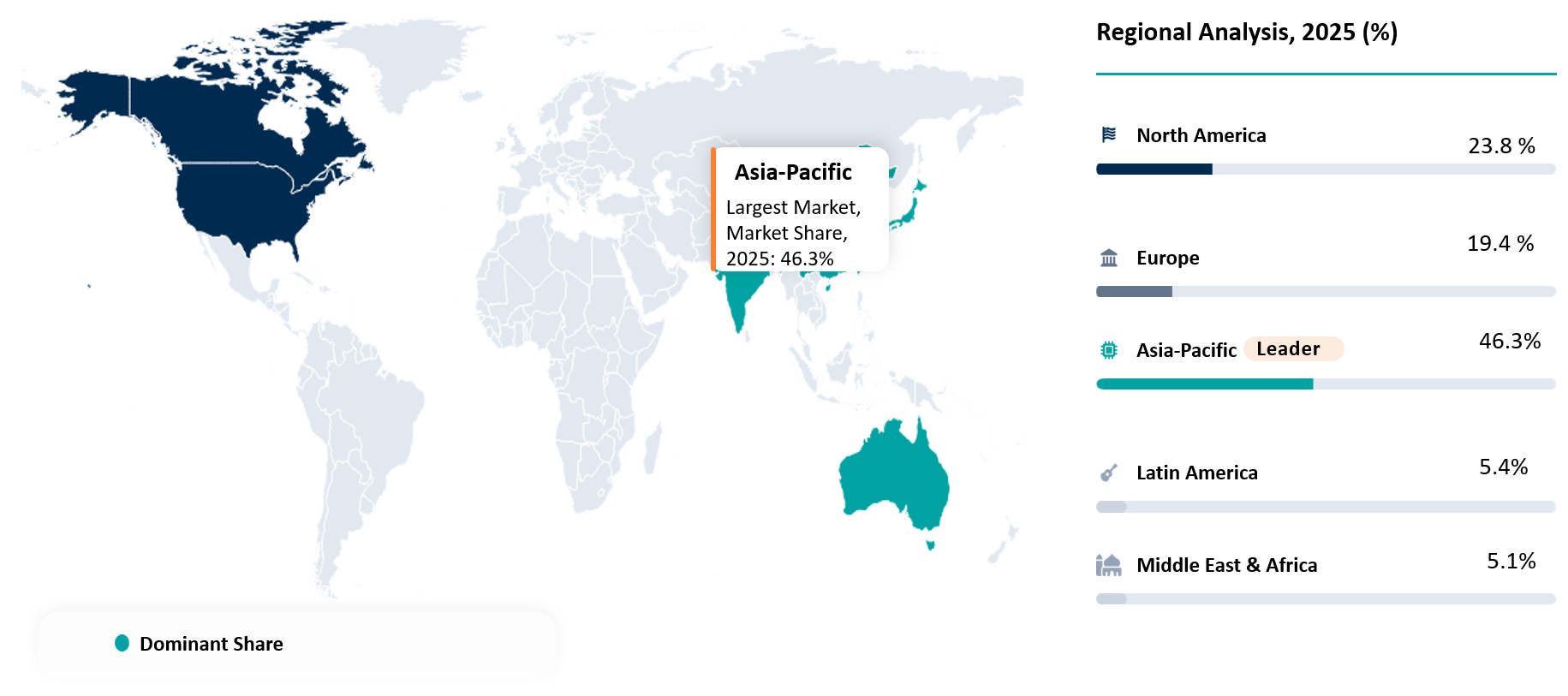

Geographical Penetration

Asia-Pacific Leads Global Chillers Market as Cooling Demand Intensifies Across Industrial, Commercial and Data Center Infrastructure

Asia-Pacific is projected to have a 46.3% share of the Global Chillers Market in 2025 due to industrial growth, commercial construction, electronics production, food processing, pharmaceutical industries, and data center development. Cooling needs have become a significant part of infrastructure as factories, healthcare facilities, airports, shopping centers, and tall structures need stable chillers for air conditioning and process cooling. For example, according to the IEA, in India, the rise in temperature by 1°C in 2024 would add about 7 GW to peak electricity demand, showing that cooling loads have turned into the key issue for infrastructure planning in hot regions of Asia.

The use of artificial intelligence and digital infrastructure has also contributed to the development of the market. According to PwC, Asia-Pacific holds about 30% of the global data center capacity, with more than 1,800 data centers and 12.2 GW live capacity. Thus, a high demand for efficient chillers, integrated liquid cooling solutions, and advanced thermal management technologies has appeared. In order to satisfy customers' needs, vendors compete on efficiency, environmentally-friendly refrigerants, compact chiller plants, intelligent control, and after-sales services. Buyers' focus is shifting to cooling systems based not on the price but on efficiency.

U.S Chillers Market Trends

In the U.S. Chiller Market, there is a trend towards procurement based on performance metrics as commercial buildings, hospitals, manufacturing units, and data centers increasingly require reduced energy consumption, increased uptime reliability, and reduced life cycle costs. Cooling is taking a strategic infrastructure approach amid projections by EIA that electricity consumption in the U.S. will increase to about 4,250 BkWh by 2026, and sales of electricity in the commercial sector, including data centers, will grow by 2.2% in 2026. There is consequently rising demand for highly efficient centrifugal chillers, screw chillers, modular chillers, magnetic bearing chillers, and advanced control-driven systems.

Government policy initiatives have also become increasingly influential in influencing purchase decisions. Within the context of the U.S. EPA's AIM Act framework, there is a phase-down of HFC production and consumption to 15% of the baseline historical average by 2036, and certain technology types are banned from using high-GWP HFCs from January 1, 2025. Consequently, low-GWP refrigerant chillers, leak management preparation, predictive maintenance, and BMS-integrated chillers are key priorities, hence making data centers, healthcare, pharmaceuticals, food processing, and large commercial segments the most promising demand areas.

Japan Chillers Market Outlook

Japan’s Chillers Market is expected to gravitate towards high-efficiency, low-GWP and digitally-enabled cooling technologies as commercial buildings, hospitals, semiconductor facilities and data centers experience increased energy cost and emission reduction pressures. The 2025 Strategic Energy Plan from Japan’s Agency for Natural Resources and Energy suggests that electricity demand is set to rise from FY2024 due to new data centers and semiconductor plants, meaning cooling equipment becomes not only strategically critical but also no longer a simple HVAC investment.

Most promising are applications where mission-critical cooling, process cooling and retrofits are involved. According to Japan’s Agency for Natural Resources and Energy, total electricity consumption is forecasted to grow despite efficiency gains, with industrial usage to increase due to new data centers and semiconductors. This opens up the prospects for screw chillers, centrifugal chillers, modular chillers and heat pump chiller systems characterized by smart operation, low environmental footprint and high efficiencies under partial loads.

Competitive Landscape

Global Chillers Market leaders include big HVAC firms and industrial cooling equipment manufacturers with diversified product ranges, strong service coverage, and capabilities in commercial, institutional, and industrial cooling systems. Companies such as Carrier Global Corporation, Daikin Industries, Ltd., Trane Technologies plc, Johnson Controls International plc, and Mitsubishi Electric Hydronics & IT Cooling Systems S.p.A. continue to have a strong position in the market because of their range of products from air cooled and water cooled chillers, centrifugal and screw chillers, emphasis on use of low GWP refrigerants, smart controls, and participation in large building, hospital, infrastructure, and data center projects.

The market competition is also influenced by other regional-scale players as well as specialized companies focusing on application-specific cooling needs. Some of the competing firms include LG Electronics Inc., Gree Electric Appliances, Inc. of Zhuhai, Midea Group, Thermax Limited, Danfoss A/S, and Blue Star Limited, who can compete in the market using their HVAC scale, absorption cooling, process chillers, components, and energy-efficient integrated system design capabilities. Competing firms include Smardt Chiller Group, Dimplex Thermal Solutions, Drake Refrigeration, Inc., and PolyScience, who add to the competitive environment using their oil-free centrifugal chillers and process cooling capability.

Recent Developments

- April 2026: Carrier introduced the AquaEdge 19MV4 water-cooled centrifugal chiller for AI data centers, delivering 2.1 MW to 3.3 MW of cooling capacity to support GPU and TPU-driven thermal loads.

- February 2026: Carrier launched the AquaEdge 30CF air-cooled centrifugal chiller, designed to improve data center cooling reliability, continuous performance and uptime protection.

- January 2026: Daikin Applied unveiled the Magnitude WME-C Quad Chiller at AHR Expo 2026, featuring magnetic-bearing technology, 2,000 to 3,000 tons capacity and ultra-low GWP refrigerants.

- April 2026: Carrier Global announced an investment of ₹863 crore to establish a chiller and cooling systems manufacturing facility in Sri City, Andhra Pradesh, supporting India’s data center and climate-control ecosystem.

- July 2025: LG Electronics expanded the availability of its air-cooled inverter scroll chiller using R32 refrigerant, targeting mid-sized commercial buildings requiring both chilled and hot water.

- April 2025: Johnson Controls expanded YORK YVAM chiller availability in the Middle East, positioning it for extreme ambient conditions up to 55°C and compatibility with liquid and immersion cooling.

- September 2025: Shree Refrigerations partnered with Smardt Chillers to introduce oil-free chiller cooling solutions for data centers in India, strengthening high-efficiency chiller availability for digital infrastructure.

- January 2024: Johnson Controls introduced the YORK YVWH Water-to-Water Dual Variable Speed Screw Heat Pump, using ultra-low GWP R-1234ze refrigerant for commercial and industrial applications.

AI Impact Analysis

AI will soon have a transformative effect on the Global Chillers Market through shifting cooling solutions from reactive maintenance to predictive and optimized performance. In commercial buildings, data centers, hospitals, and other facilities, an AI-driven control system can monitor factors such as load fluctuation, weather conditions, occupancy, performance of equipment, and energy usage to optimize the performance and efficiency of chillers. Such features will enable buyers to cut down costs, increase uptime, and improve equipment longevity, particularly for facilities that rely on constant cooling and require critical uptime.

There will be a significant impact on smart chillers, integrated HVAC solutions, and service-centric business models. The combination of AI, IoT sensors, building management systems, remote diagnostics, and predictive maintenance will allow vendors to compete beyond their products' prices. In turn, customers will be able to benefit from rapid fault detection, refrigerant leak detection, energy benchmarking, and automated tuning of systems performance. With energy efficiency and sustainability becoming procurement drivers, AI-based chillers will emerge as a premium product category in data centers, large buildings, district and process cooling applications.

White Space Opportunities

The strongest white space in the Global Chillers Market lies in high-efficiency retrofit and replacement demand. Many commercial buildings, hospitals, industrial plants and public facilities still operate older chillers with high energy consumption, aging refrigerants and limited digital monitoring. This creates a clear opportunity for vendors offering inverter-driven screw chillers, magnetic-bearing centrifugal chillers, modular systems, low-GWP refrigerant platforms and performance-based service contracts that reduce energy cost and improve lifecycle value.

Another opportunity is emerging in mission-critical and process-specific cooling applications. Data centers, pharmaceuticals, food and beverage, chemicals, plastics and district cooling networks require reliable, scalable and precision-controlled cooling infrastructure. Vendors can differentiate by offering customized cooling capacity, remote monitoring, predictive maintenance, heat recovery, compact plant design and integration with building management systems. Growth will increasingly favor companies that move beyond equipment supply and position chillers as part of a broader energy-efficiency, uptime assurance and sustainability solution.

DMI Opinion

According to DataM, the main factor limiting the growth of the Global Chillers Market isn’t low cooling demand, but whether companies can provide systems that minimize power usage, meet refrigerant changes and maintain efficiency. The focus is moving from traditional standalone chillers to high-efficiency screw chillers, magnetic bearing centrifugal chillers, modular chillers, inverter chillers and GWP refrigerant systems.

DataM expects that future growth in the Global Chillers Market will come from lifecycle value and not just equipment price. End users have become more interested in vendor capabilities regarding power reduction, uptime, adaptability in cooling capacity, cost of maintenance, intelligent control, after-sales services and total cost of ownership. Companies able to supply complete cooling solutions for commercial buildings, data centers, healthcare facilities, food and beverages, pharmaceutical, chemicals, plastics and district cooling will perform better in the Global Chillers Market.

Why This Report Matters in 2026?

The global chillers market will be highly strategic by 2026 due to the importance of efficient cooling and low power consumption among commercial buildings, data centers, hospitals, and industrial establishments. Increasing cost of energy and stringent regulations regarding refrigerants have led customers to upgrade their existing cooling units to energy-efficient screw chillers, centrifugal chillers, modular chillers, inverter-driven units, and chillers with low GWP refrigerants.

With an increase in the importance of cooling, the focus of purchases is increasingly shifting from purchasing equipment to analyzing its overall performance during its life cycle. The main purchase consideration includes cooling capacity, efficiency, part load performance, reliability, refrigerant compatibility, maintenance cost, smart control compatibility, and post-sales service strength.

This study helps stakeholders understand the areas witnessing rapid growth in demand for chillers, end-user industry segments investing in cooling infrastructure, trending technologies, and the most suitable vendors for the given application areas.

Why Choose DataM?

- End-to-End Chillers Ecosystem Assessment: Covers the entire chiller ecosystem, which encompasses screw chillers, centrifugal chillers, absorption chillers, scroll chillers, reciprocating chillers, air-cooled chillers, and water-cooled chillers used for HVAC and process cooling purposes.

- Product and Technology Assessment: Focuses on analyzing high-efficiency chillers, inverter-driven technology, magnetic bearing centrifugal chillers, modulating chillers, low GWP refrigerants, and advanced control systems that could be commercially viable.

- Application / Use Case and End-User Assessment: Monitors adoption of chillers in plastics, food and beverage, rubber manufacturing, printing, medical & pharmaceutical, chemicals & petrochemicals, alternate energy sector, commercial buildings, data centers, and industrial applications.

- Regulation, Efficiency & Sustainability Analysis: Examines how energy efficiency mandates, refrigerant transition, green buildings policies, reduction in carbon emissions, and sustainability-led cooling upgrades impact chiller demand in different regions.

- Benchmarking for Competitive Strategy: Benchmarks Carrier Global Corporation, Daikin Industries, Ltd., Trane Technologies plc, Johnson Controls International plc, Mitsubishi Electric Hydronics & IT Cooling Systems S.p.A., LG Electronics Inc., Gree Electric Appliances, Inc. of Zhuhai, Midea Group and Thermax Limited for strengths in portfolio, efficiency innovations, service networks, and market coverage.

- Pricing, Procurement, and Market Entry Strategies: Analyzes customer needs for cooling capacities, energy efficiency, refrigerants, installation costs, maintenance costs, total lifecycle cost, after-sales services, and bidding considerations.

- Opportunities and Strategic Expansion: Highlights growth prospects in data center cooling, district cooling systems, industrial process cooling, chillers, modular plant cooling, low GWP technology and high efficiency replacement.

Key Procurement Priorities and Buyer Evaluation Criteria

- Buyers in the Global Chillers Market are increasingly prioritizing systems that deliver higher energy efficiency, lower lifecycle cost, reliable cooling performance, low maintenance requirements and compliance with evolving refrigerant regulations.

- Procurement decisions are shifting toward integrated cooling solutions that combine chillers, smart controls, heat exchangers, pumps, cooling towers, sensors and building management system compatibility for optimized HVAC and process-cooling performance.

- Commercial buildings, data centers, hospitals, food and beverage plants, pharmaceutical facilities, chemical units and industrial users are evaluating vendors based on energy savings, cooling capacity, uptime, service network, refrigerant type, installation flexibility and total cost of ownership.

- Vendors with strong capabilities in inverter-driven chillers, magnetic-bearing centrifugal chillers, modular systems, low-GWP refrigerants, predictive maintenance and after-sales service are better positioned to win long-term contracts as buyers move toward performance-driven cooling procurement.