MASH Diagnostics Market Overview

The Global MASH Diagnostics Market stood at US$ 1.41 billion in 2025 and is expected to reach US$ 7.72 billion by 2035, growing with a CAGR of 23.94% during the forecast period 2026-2035. MASH diagnostics are shifting away from invasive biopsy validation to scalable noninvasive and therapy-related diagnostics. Recent developments have picked up speed following the USFDA approval of Rezdiffra in 2024 as the first drug treatment for MASH/NASH adults who do not have cirrhosis and suffer from MASH/NASH with moderate to advanced liver fibrosis, which will result in the requirement of diagnostics capable of validating such patients with stages F2-F3 and hence treatment suitability. Wegovy, or the GLP-1 receptor agonist semaglutide injection, was also approved by the USFDA in August 2025 for the treatment of MASH in adults with moderate to advanced fibrosis without cirrhosis.

The broadening of this therapy is enhancing the commercial potential of imaging diagnostics, elastography, blood-based biomarkers, fibrosis scoring, AI pathology, and liver quantification by MRI. The company Echosens continues building on the capabilities of FibroScan in assessing liver stiffness and steatosis non-invasively. The capabilities of AI pathology from PathAI for MASH trials allow for standardized histology scoring and assessment endpoints. Additionally, Perspectum advances the use of MRI in liver diagnostic applications for disease activity and monitoring purposes. On a whole, competitive value is being built around the integration of validated and repeatable diagnostics for enabling early diagnosis, staging of F2-F3, selection of GLP-1 therapy, payer documentation, and treatment monitoring.

Key Takeaways

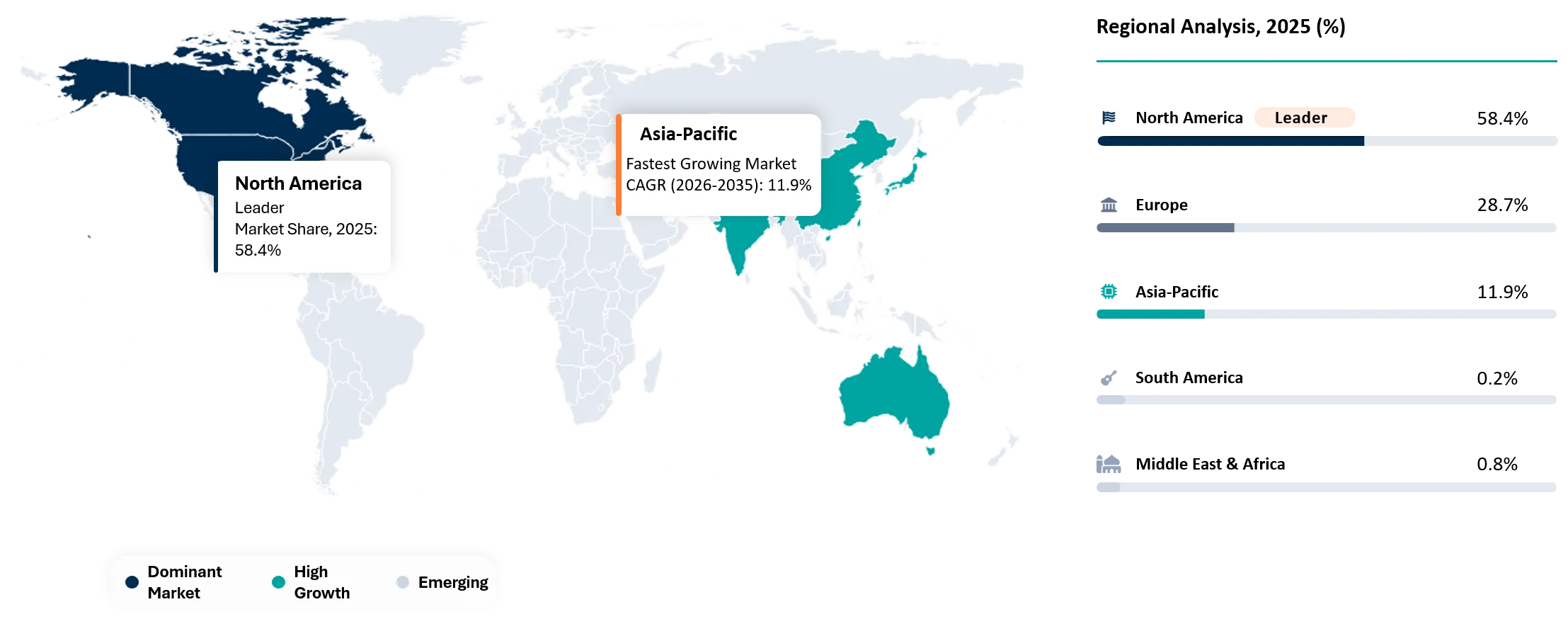

- North America held the highest market share at 58.4% in 2025, supported by strong hepatology infrastructure, high obesity and diabetes burden, early adoption of non-invasive liver testing and faster therapy-linked diagnostic integration.

- Europe remained the second-largest region with 28.7% share in 2025, driven by established gastroenterology networks, strong imaging infrastructure, liver disease screening initiatives and rising use of elastography and blood-based fibrosis assessment.

- Asia-Pacific accounted for 11.9% share in 2025, supported by rising MASLD burden, expanding diagnostic access, improving specialist liver care capacity and increasing adoption of non-invasive liver assessment across hospitals and imaging centers.

- Imaging diagnostics dominated the diagnostic method segment in 2025, supported by strong use of ultrasound, elastography, MRI-PDFF and MRE for non-invasive liver fat assessment, fibrosis staging and disease progression monitoring.

- GLP-1 therapy expansion is becoming a major demand catalyst for MASH diagnostics, as the FDA approved Wegovy in August 2025 for adults with noncirrhotic MASH and moderate to advanced liver fibrosis, creating stronger need for patient screening, fibrosis confirmation, treatment eligibility assessment and long-term response monitoring.

- Recent treatment approvals are reshaping diagnostic demand, as Rezdiffra received FDA approval in March 2024 for adults with noncirrhotic NASH or MASH with moderate to advanced fibrosis, strengthening demand for F2-F3 patient identification, therapy eligibility assessment and treatment monitoring.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 1.41 Billion | |

| 2035 Projected Market Size | US$ 7.72 Billion | |

| CAGR (2026-2035) | 23.94% | |

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Diagnostic Workflow | Initial Screening Methods, MASH Confirmation Methods, Fibrosis Staging Methods, Treatment Monitoring Methods, Disease Progression Surveillance Methods, and Emerging Diagnostic Technologies | |

| By Diagnostic Method | Imaging Diagnostics, Blood Based Diagnostics, Histopathology Diagnostics, Molecular Diagnostics, and AI Enabled Diagnostics | |

| By Diagnostic Purpose | Screening Diagnostics, Disease Confirmation Diagnostics, Fibrosis Staging Diagnostics, Therapy Eligibility Diagnostics, Companion Diagnostics, Treatment Monitoring Diagnostics, Disease Surveillance Diagnostics, and Progression Tracking Diagnostics | |

| By Disease Severity | MASLD, Early MASH, Mild Fibrosis, Moderate Fibrosis, Advanced Fibrosis, Severe Fibrosis, Cirrhosis Stage, and High Risk Progression Population | |

| By End-User | Hospitals, Hepatology Clinics, Gastroenterology Clinics, Diagnostic Laboratories, Imaging Centers, Specialty Liver Centers, Academic Research Centers, and Ambulatory Diagnostic Centers | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Why This Report Matters in 2026?

The MASH diagnostics market matters in 2026 because the disease is moving from an underdiagnosed liver condition to a treatment-linked clinical priority. With approved MASH therapies requiring identification of patients with clinically significant fibrosis, diagnostic demand is shifting from basic liver enzyme testing toward structured workflows covering risk screening, fibrosis staging, therapy eligibility and disease monitoring. Hospitals, hepatology clinics, endocrinology practices and diagnostic laboratories now need reliable tools that can identify F2-F3 patients earlier and reduce dependence on invasive liver biopsy.

This report helps stakeholders understand where commercial value is forming across elastography, MRI-based diagnostics, blood biomarkers, AI pathology, molecular testing and multi-modal diagnostic algorithms. It is especially important for diagnostic companies, imaging providers, pharmaceutical firms and investors seeking to align product strategy with clinical adoption, reimbursement expectations and patient screening expansion. In 2026, competitive success will depend on accuracy, scalability, workflow integration and proof that diagnostics can support real treatment decisions.

AI Impact Analysis

AI technology is becoming a major driver in the MASH diagnostic market through improved consistency, scale and usability of liver assessments. AI algorithms have already started making their way into pathology, where they can help improve the inter-reader variability in fibrosis, steatosis, inflammation, and ballooning assessments during biopsy. The application of AI algorithms to imaging can result in a better evaluation of liver fat content, fibrosis risk and longitudinal monitoring. This is particularly relevant as the MASH diagnostic trend goes from a specialized physician-based analysis to mass screenings in patients with obesity, diabetes, and metabolic risk factors.

In addition to that, AI algorithms can assist clinicians in identifying patients who are likely to suffer from clinically relevant fibrosis requiring further testing or treatments. AI technology can be used by diagnostic companies to integrate multiple data types such as imaging, blood tests, clinical history, and data from the electronic health record for risk stratification purposes. Nevertheless, the application of AI technology will largely depend on regulatory approval, payer acceptance, clinician acceptance, and data integrity.

White Space Opportunities

The development of the primary care and diabetes-associated MASH diagnosis pathways is the white space in the market that can offer significant opportunities. Many patients with increased risk factors, such as obesity, type 2 diabetes, and metabolic syndrome, go untreated until they develop more severe fibrosis. It is possible for the companies to create an effective approach to diagnosis with the combination of FIB-4, blood biomarkers, elastography and referral to additional examinations.

It is likely that there will be an emergence of opportunities for diagnostics in determining the eligibility for MASH therapies after the appearance of the corresponding treatment options. Doctors need efficient methods of diagnosing significant fibrosis, particularly in F2-F3 stages, to decide about treatment and not rely primarily on biopsies. There is enough space for non-invasive tests, AI algorithms for imaging, biomarkers and diagnostics in general.

The field of monitoring patients with MASH is also underdeveloped. It is needed for hospitals, sponsors of clinical trials and drug manufacturers to measure the progress, monitor fibrosis regression, reduction of fatty liver content, and evaluate other indicators using standardized tests. Companies that use several approaches (imaging, biomarkers, AI technologies and EHR integration) will be successful.

Disruption Analysis

Shift from Biopsy-Led Diagnosis Toward Scalable Non-Invasive and Therapy-Linked MASH Diagnostic Workflows

MASH diagnostics have been affected by changes brought about by the move away from biopsy confirmation to a more scalable non-invasive process and therapy-linked diagnostics involving the use of tools like FibroScan, MRI-PDFF, MRE, ELF, FIB-4, biomarker-based blood tests, and artificial intelligence for imaging purposes to diagnose patients with conditions like obesity, diabetes, and other metabolic risks. These changes are transforming the concept of diagnostics from a one-off liver analysis process into a well-defined clinical decision process that assists in identifying patients at high risk, diagnosing F2-F3 fibrosis, therapy qualification, securing payment, and monitoring. As MASH drugs come into use, diagnostic firms are shifting their focus from routine liver analysis to more precise and less costly methods of screening treatment-ready patients, as well as decreasing the use of biopsies.

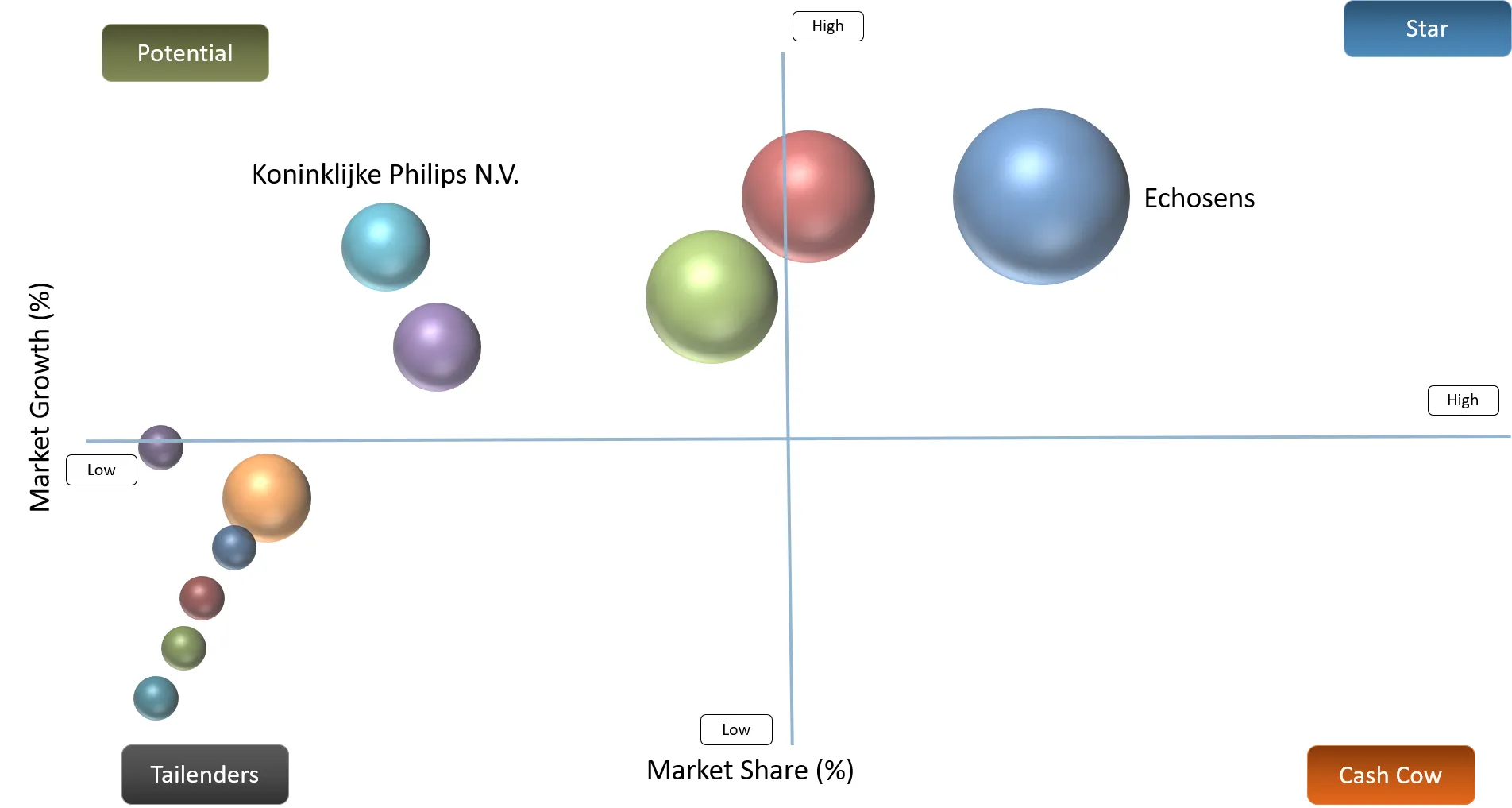

BCG Matrix: Company Evaluation

Star

According to the BCG matrix, Echosens is considered a Star for the company's specializations in the area of liver assessment without invasions and the strong relevancy of its solutions to the procedures associated with the assessment of the stages of fibrosis progression. F. Hoffmann-La Roche Ltd. is viewed as a powerful high growth company with well-developed infrastructure for diagnostics along with strong laboratory affiliations and molecular diagnostics, which allows the company to provide assistance for blood-based verification, eligibility, and companion diagnostics upon the increasing popularity of MASH drugs.

Potential

Koninklijke Philips N.V., GE HealthCare and Siemens Healthineers AG companies are categorized as being in the Potential quadrant due to their imaging products' portfolio and potential for AI-assisted liver assessment and diagnosis in hospital and imaging centers settings. Histindex Pte Ltd., BioPredictive, Perspectum Limited, PathAI, Nordic Bioscience and Rubió Metabolomics fall under the category of Tailenders due to offering their specializations in digital pathology, biomarkers' panel, pathology by means of artificial intelligence, and advanced methods of liver assessment, but depending on the clinical validation and acceptance.

Market Dynamics

Shift from biopsy toward non-invasive fibrosis assessment is accelerating adoption

The MASH diagnostic pathway is shifting from invasive liver biopsy confirmation to risk-based, non-invasive fibrosis evaluation due to the invasiveness, cost, variation, and unsuitability of liver biopsy in large cohorts with diabetes and obesity. The current clinical pathway increasingly utilizes FIB-4 as the initial triaging modality, followed by transient elastography/FibroScan, ELF blood test, MRI-PDFF, MRI elastography, and referral for specialist management for high-risk individuals. The 2024 EASL guidelines suggest a staged approach that begins with FIB-4 and then elastography in individuals with cardiometabolic risk factors, abnormal liver enzymes, steatosis, diabetes, or obesity.

The market driver has become even stronger following the FDA approval of Rezdiffra in March 2024 for noncirrhotic NASH/MASH with moderate-to-advanced fibrosis, making the identification of F2-F3 fibrosis essential for treatment, monitoring, and reimbursement.The disease burden is contributing to a significant screening base, with recent epidemiology studies suggesting a global MASLD incide

nce rate of 38% among adults and an MASH prevalence rate ranging between 5% and 7% in the general population; one of the most affected regions is Latin America, where MASLD adult prevalence is 44.4%.Government and health system involvement is also moving towards early detection. This includes Indian-related state programs that are introducing fatty liver screening via their NCD/obesity programs and FibroScans via their obesity programs. It also involves international research networks analyzing the scalability of the MASH screening program.

Advanced imaging and specialty tests remain unevenly accessible across regions

MASH guidelines are progressing more quickly than infrastructure can support. The EASL-EASD-EASO guidelines call for case-finding of liver fibrosis in cardiometabolic-risk patients with non-invasive diagnostics, progressing through FIB-4 to transient elastography/VCTE and imaging. While this strategy is more feasible in North America, Western Europe and advanced urban areas, it is less practical in places where elastography, ELF, MRI-PDFF and MR elastography are not routinely accessible.

Advanced imaging is still a resource limitation, not just a medical decision. The WHO points out that many low- and lower-middle-income nations lack the financial resources to purchase imaging equipment, in addition to experiencing a shortage of qualified imaging technicians. This restricts the widespread adoption of MRI-PDFF for liver fat quantification and MR elastography for fibrosis diagnosis, with these high-end technologies limited to tertiary facilities, teaching hospitals and private diagnostic networks.

Two-tiered diagnostic models are evolving in the marketplace. According to the AASLD guidelines, FIB-4 should be used as the primary risk stratification tool, while VCTE or ELF should be used as the secondary diagnostic test when FIB-4 is either elevated or ambiguous. In cases where secondary testing is unavailable, patients may find themselves between abnormal laboratory screening results and confirmation of fibrosis staging.The government initiatives are making people aware about the disease, but the disparities in access continue to be structural. The newly revised guidelines for 2024 by India regarding NAFLD help in early detection of the problem through the route of primary care; however, their full application still requires wider access to equipment, biomarkers, as well as trained personnel for referrals.

Segmentation Analysis

The Global MASH Diagnostics Market is segmented based on diagnostic workflow, diagnostic method, diagnostic purpose, disease severity, end user, and region.

Advanced CT-Based Opportunistic Liver Assessment is Creating a Scalable Non-Invasive Pathway for Early MASH Risk Detection and AI-Enabled Fibrosis Evaluation

The application of CT imaging to MASH diagnostics has a niche purpose in the worldwide market, especially for opportunistic hepatic steatosis detection during CT scans of the abdomen, heart, or cancer patients. The significance of this section increases due to CT's ability to generate liver attenuation, liver/spleen ratio, texture information, and radiomic features that might be used for liver fat and liver disease progression without invasive techniques.

Nevertheless, CT cannot become the preferred MASH diagnostic technique due to radiation hazard, lower sensitivity to mild steatosis, and inferior fibrosis evaluation capabilities than FibroScan, MRI-PDFF, or MRE. CT-based techniques are being developed and According to Hu et al. (2023), CT-based strategies have progressed to include liver/spleen ratios, dual-energy CT, photon-counting CT, texture analysis, deep learning, and radiomics for detecting steatosis and staging fibrosis in the future, allowing for AI-powered opportunistic screening.

Geographical Penetration

North America Leads MASH Diagnostics Growth as Therapy Eligibility, Non-Invasive Testing and High-Risk Patient Screening Reshape Clinical Demand

The North America market remains a leader due to the high number of metabolic risk populations within the US in need of structured MASLD and MASH diagnostics. The American Diabetes Association indicates that MASLD prevalence in type 2 diabetic population in the US is ≥70% with about half of the patients suffering from a more advanced MASH disease form. This means that there will be large opportunities for the diagnostic funnel across diabetes management, obesity practices, primary care, and hepatology referral.

The dominant diagnostic pathway is shifting toward FIB-4-led sequential screening. In MASLD monitoring, The American Diabetes Association screening pathway recommends repeat testing when FIB-4 is <1.3, further fibrosis testing when FIB-4 is ≥1.3, and specialist referral when FIB-4 is >2.67. patients with a FIB-4 score below 1.3 are generally monitored and retested after one year, while those with a FIB-4 score of 1.3 or above proceed to non-invasive liver fibrosis assessment such as transient elastography, ELF, MRE or specialist evaluation. Patients with a FIB-4 score above 2.67 are treated as high-risk and referred to specialists because the probability of advanced fibrosis is higher.

The recent approval of Rezdiffra in the U.S. is increasing the need for diagnosis of the fibrosis stage since the drug was approved by the FDA for use among adults with non-cirrhotic NASH with fibrosis stages ranging from moderate to advanced (i.e., F2 to F3). This is driving the need for the diagnosis for more than just screening purposes.

Government efforts and public health activities are also aiding the development of the market. The CDC identified that 40.1 million people in America have diabetes in 2023, and the NIDDK and NIH are still engaged in the study of diabetes, obesity, and digestive diseases. There is also the “Think Liver Think Life” campaign by the American Liver Foundation continue to support research, screening awareness and care coordination for metabolic, liver and digestive diseases.

U.S. MASH Diagnostics Market Trends

As per Le P et al. (2025), there is increasing demand for MASH diagnosis in the U.S. as MASLD and MASH continue to be significantly underdiagnosed, with about 86.3 million U.S. adults being affected with MASLD as per estimation in 2020 and the number of MASH cases expected to rise from 14.9 million in 2020 to 23.2 million by 2050. Diagnostic tests are moving from the current biopsy procedures to non-invasive approaches, where FIB-4 is the commonly recommended primary diagnostic tool, and then the subsequent tests are Fibroscan /VCTE or the ELF test for assessing the risk of fibrosis.

The relevance of the ELF Test has been enhanced with its FDA approval as part of the clinical approach in advanced fibrosis associated with NASH/MASH. Biopsy remains the definitive testing approach; however, its use has been reserved for difficult and high-risk cases. Reimbursement support in the U.S. is becoming an important adoption driver, as coverage for non-invasive fibrosis assessment can reduce patient cost burden, improve specialist referral compliance and support broader use of ELF, FibroScan/VCTE and lab-based risk stratification in routine clinical pathways.

Japan MASH Diagnostics Market Outlook

Japan is transitioning from reactive detection to proactive risk-based screening. About 30% of adults in Japan aged 30+ suffer from MASLD, while MASH impacts about 3-5% of the population, making early-stage fibrosis detection crucial. Current dominant screening technique is non-invasive and workflow-efficient. Japan’s 2023 guideline on NAFLD/NASH recommends using ultrasound, CT/MRI, blood markers, platelet count, fibrosis markers, FIB-4 index, NAFLD fibrosis score, and ultrasound/MRI elastography; biopsy is used for definitive diagnosis of NASH/MASH. Japan has clinical guidelines on MASLD/MASH but lacks a specialized MASLD/MASH policy; MHLW’s Smart Life project encourages exercise, healthy diets, quitting smoking, and regular check-ups, engaging almost 11,000 entities.

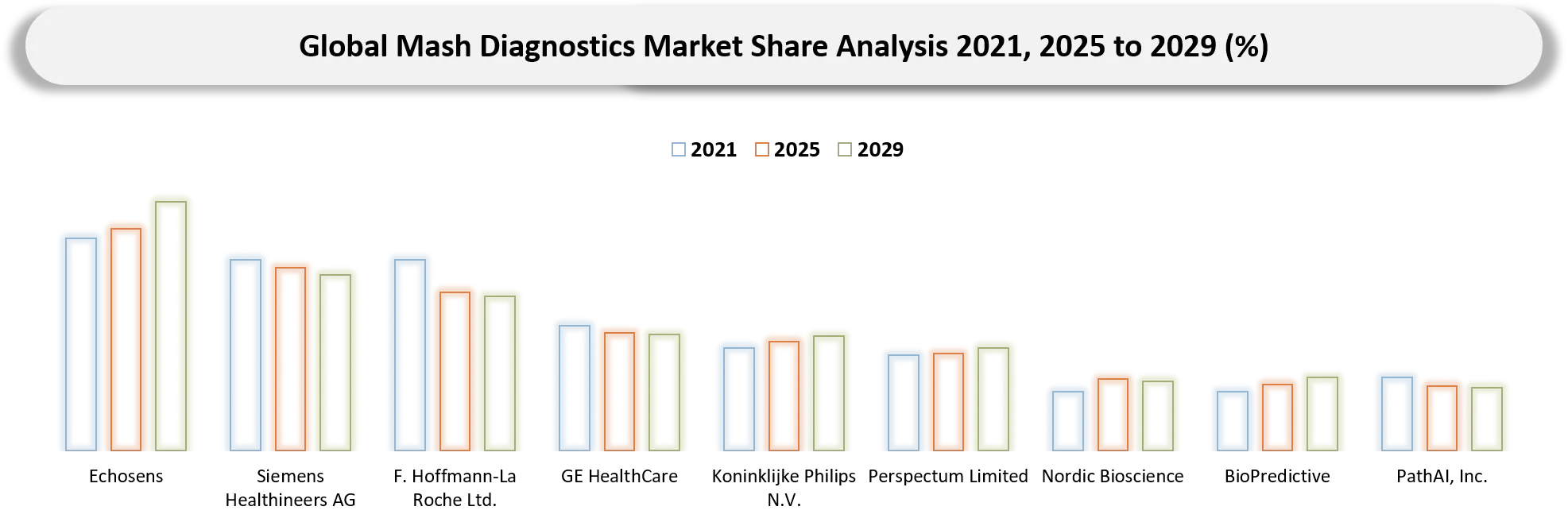

Competitive Landscape

The competitive environment for the MASH diagnostics market is comprised of international companies involved in imaging, liver-focused diagnostic specialists, pathology and biomarkers innovators. Echosens is a prominent company, owing to its dominant technology for the non-invasive staging of liver fibrosis and liver stiffness measurement. Siemens Healthineers, GE HealthCare, and Koninklijke Philips N.V. are other companies contributing to imaging with their respective technologies – ultrasound, MRI, and artificial intelligence enabled imaging infrastructure used in hospitals, hepatology clinics, and imaging centers. They have a competitive edge due to their existing footprint and ability to scale outside specialized units.

Specialists include Perspectum Limited, Nordic Bioscience, BioPredictive, Rubió Metabolomics, PathAI, Inc., and Histindex Pte Ltd. These companies are competing in their respective segments with innovative solutions that include liver imaging, serum biomarkers, metabolomics, AI pathology, and digital histology. With an increased emphasis being placed on multi-modal diagnostics of MASH disorders, there is a significant rise in their importance.

Recent Developments

- December 2025: PathAI’s AIM-MASH AI Assist became the first AI-powered tool to receive FDA qualification for MASH clinical trials, strengthening the role of AI-based pathology in standardized fibrosis and disease activity assessment.

- November 2025: PathAI highlighted Liver Explore for quantifying liver fibrosis in chronic liver diseases including MASH, supporting more precise digital pathology-based fibrosis measurement and clinical trial endpoint assessment.

- September 2025: Perspectum reported that corrected T1 from LiverMultiScan is positioned as a non-invasive, non-contrast MRI-based tool for diagnosing and monitoring liver disease activity, fat and iron, supporting wider MASH patient assessment through existing MRI infrastructure.

- March 2025: Perspectum released multinational study results showing MRI-based liver diagnostics can support cost-effective diagnosis and management of steatotic liver disease, reinforcing the use of advanced imaging in MASH care pathways.

- November 2024: PathAI published clinical validation work for an AI-based pathology tool for MASH scoring, addressing reader variability in liver biopsy interpretation and supporting more standardized trial enrollment and endpoint assessment.

- March 2024: The FDA approved Rezdiffra for adults with noncirrhotic NASH or MASH with moderate to advanced fibrosis, creating stronger demand for diagnostics that can identify F2-F3 patients for therapy eligibility and treatment monitoring.

Analyst Opinion

In this regard, the MASH diagnostics market is now approaching an interesting structural point at which diagnosis will be moved from specialist-led confirmatory liver biopsies to scalable, non-invasive and therapy-linked patient diagnostics. It appears likely that companies that can assist in developing sequential diagnostic pathways, from initial risk screening in diabetes, obesity and metabolic clinics to subsequent fibrosis staging, therapy indication and disease monitoring will be best positioned commercially.

With the increasing adoption of MASH therapy options, diagnostic solutions will need to offer improved confidence for clinicians, support appropriate reimbursement models, be easy to integrate into workflows and be able to identify F2-F3 stage fibrosis reliably. DMI sees little room for standalone diagnostic providers in this market, but rather favors integrated solutions based on accurate non-invasive technology, scalability and therapy monitoring capabilities.

Why Choose DataM?

- End-to-End MASH Diagnostics Ecosystem Assessment: DataM provides detailed insights across diagnostic workflow, diagnostic method, diagnostic purpose, disease severity, end users and regional adoption patterns, helping clients understand where MASH diagnostic demand is commercially scaling.

- Commercially Feasible Segmentation: Our segmentation is built around measurable revenue pools such as screening, confirmation, fibrosis staging, treatment eligibility assessment, disease monitoring, imaging diagnostics, blood-based diagnostics, histopathology, molecular testing and AI-enabled tools, reducing overlap and improving market-sizing accuracy.

- Therapy-Linked Diagnostic Intelligence: DataM evaluates how approved and pipeline MASH therapies are reshaping demand for F2-F3 fibrosis identification, patient stratification, treatment eligibility testing and long-term response monitoring.

- Competitive and Innovation Mapping: DataM tracks leading players across elastography, MRI-based diagnostics, blood biomarkers, AI pathology, molecular diagnostics and digital liver assessment platforms, helping clients benchmark product positioning and partnership opportunities.

- Actionable Strategic Insights: DataM converts clinical, regulatory, reimbursement and technology trends into practical recommendations for diagnostic companies, imaging providers, pharmaceutical firms, investors and healthcare stakeholders planning entry, expansion or portfolio prioritization in MASH diagnostics.

Key Procurement Priorities and Buyer Evaluation Criteria

- Buyers in the Global MASH Diagnostics Market are increasingly prioritizing providers that can deliver clinically validated, non-invasive and workflow-ready diagnostic solutions with proven performance in fibrosis staging, steatosis assessment, disease activity evaluation and treatment eligibility identification across high-risk metabolic patient groups.

- Procurement decisions are shifting from standalone diagnostic tests toward integrated MASH assessment pathways that combine blood-based biomarkers, elastography, MRI-based tools, AI-enabled pathology and clinical risk scores, enabling hospitals, diagnostic laboratories and hepatology centers to improve patient stratification, reduce biopsy dependence and support long-term disease monitoring.

- Buyers are evaluating vendors based on diagnostic accuracy, reproducibility, clinical guideline alignment, reimbursement acceptance, regulatory validation and ability to identify F2-F3 fibrosis patients who may qualify for therapy or closer clinical management.

- Healthcare providers are also prioritizing solutions that can be integrated into existing hospital imaging systems, laboratory workflows, electronic health records and specialist referral pathways, reducing operational friction while improving screening efficiency across diabetes, obesity, gastroenterology and hepatology settings.

- Pharmaceutical companies, CROs and clinical trial sponsors are placing higher value on diagnostic partners that can support patient recruitment, endpoint standardization, biopsy reduction, treatment response tracking and multi-site consistency in MASH clinical development programs.