Iron Air Battery Market Overview

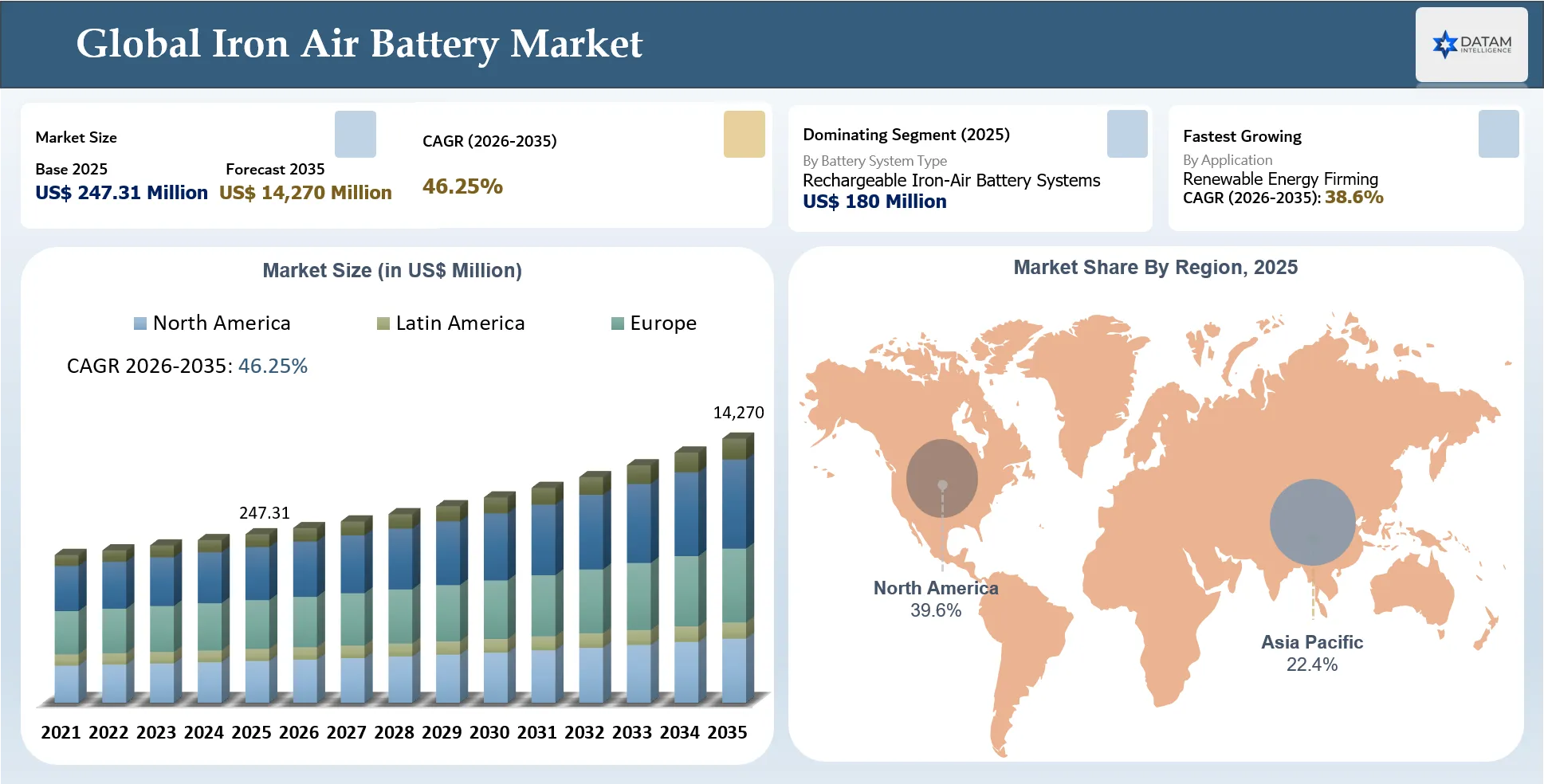

The Global Iron Air Battery Market stood at US$ 247.31 million in 2025 and is expected to reach US$ 14270 million by 2035, growing with a CAGR of 46.25% during the forecast period 2026-2035.

The Global Iron Air Battery Market is being considered as a promising prospect for long-duration energy storage applications due to increased demand for reliable, economic, and scalable storage capacity in renewable-dominated electricity networks. Unlike lithium-ion batteries, which are optimized mainly for short durations of storage, iron-air batteries enable long discharges over several days. Hence, they present significant potential to firm renewable energy resources, provide for system reliability, grid resilience and the displacement of peaker plants using fossil fuels. Iron-air batteries utilize common materials like iron, thereby minimizing reliance on lithium, cobalt, and nickel supply risks.

Current market uptake for the iron-air battery technology is being seen mostly in commercial installations, pilot programs conducted by utilities and in governmental long-duration storage programs. The main customers in the coming years will be utilities and other network participants, requiring storage systems that can handle intermittency in renewable energy generation, climate conditions and transmission challenges. North America is expected to be the early leader in commercial installations, backed by policy funding and projects.

However, the market continues in the validation stage. Lack of commercial operating experience, bankability issues, lack of warranty confidence and performance assurance could hinder their adoption in the near term. Over the medium and long terms, successful project execution, falling costs of systems, and long-duration storage procurement are anticipated to enable iron-air batteries to become indispensable to lithium-ion batteries in green energy grids.

Key Takeaways

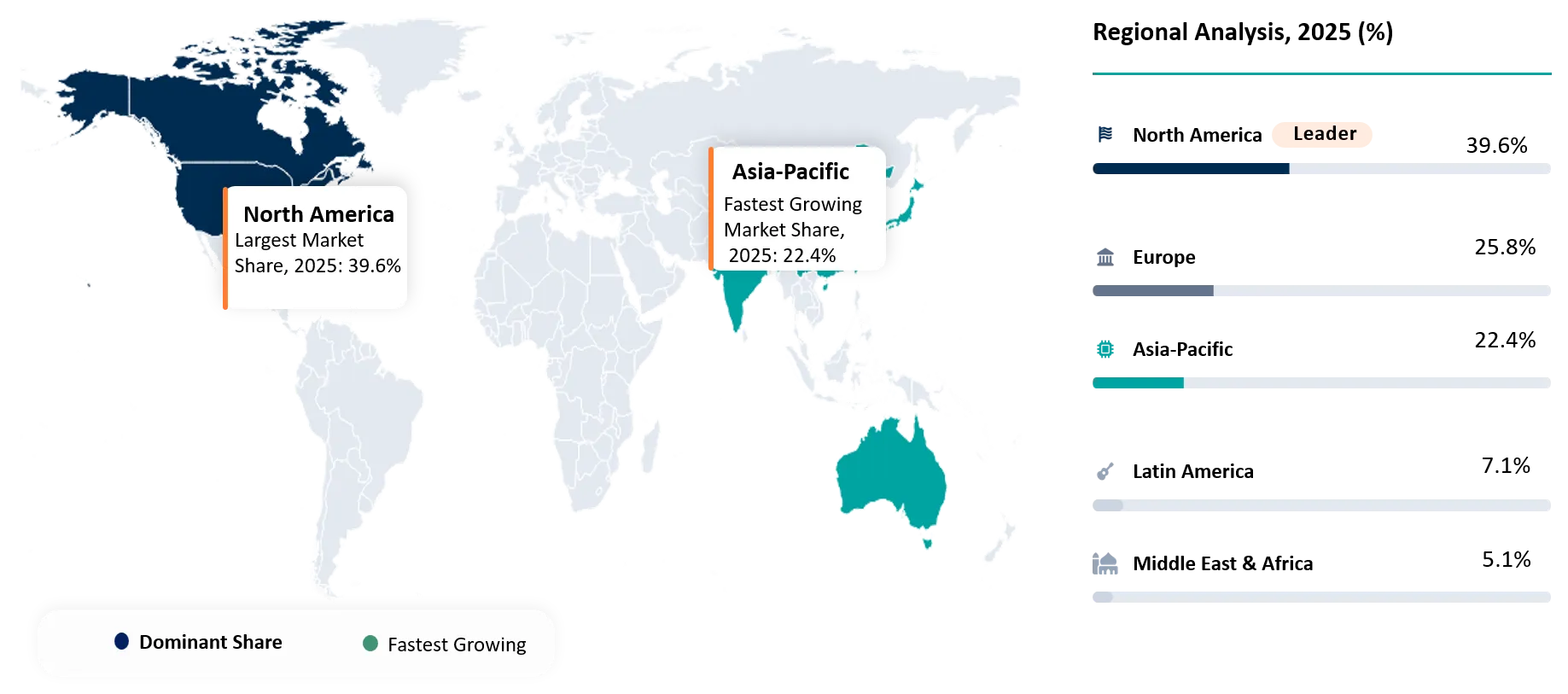

- North America held the highest market share at 39.6% in 2025, supported by early commercialization, utility-scale LDES procurement, federal funding and renewable-heavy grid resilience needs.

- Europe accounted for 25.8% share in 2025, driven by clean energy transition targets, grid flexibility programs, renewable integration and growing non-lithium storage pilots.

- Asia Pacific accounted for 22.4% share in 2025 and is expected to grow fastest, supported by renewable expansion, energy security priorities, grid modernization and rising long-duration storage investment.

- Rechargeable iron-air battery systems dominated the battery system type segment with 55.4% share in 2025, driven by strong fit for repeat-use grid-scale storage.

- Renewable energy firming led the application segment with 34.7% share in 2025, supported by rising solar and wind intermittency.

- Buyers are shifting from short-duration battery procurement toward multi-day storage solutions focused on resilience, resource adequacy, lifecycle cost, safety and utility-scale bankability.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 247.31 Million | |

| 2035 Projected Market Size | US$ 14,270 Million | |

| CAGR (2026-2035) | 46.25% | |

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Battery System Type | Rechargeable Iron-Air Battery Systems; Mechanically Rechargeable Iron-Air Battery Systems and Hybrid Iron-Air Battery Systems | |

| By Battery Format | Stationary Iron-Air Battery Systems and Portable Iron-Air Battery Systems | |

| By Storage Duration | 10–24 Hours; 24–72 Hours and Above 72 Hours | |

| By Electrode Architecture | Bielectrode Iron-Air Battery; Monolithic Bielectrode Iron-Air Battery and Monolithic Stack Iron-Air Battery | |

| By Capacity | Below 100 kWh; 100 kWh–1 MWh; 1–10 MWh; 10–100 MWh and Above 100 MWh | |

| By Application | Renewable Energy Firming; Peak Load Management; Resource Adequacy; Grid Resilience and Backup Power; Microgrid and Remote Power Storage; Transmission and Distribution Deferral and Others | |

| By End User | Utilities; Renewable Energy Developers; Independent Power Producers; Grid Operators; Commercial and Industrial Users; Mining; Residential Users and Government and Defense Facilities | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

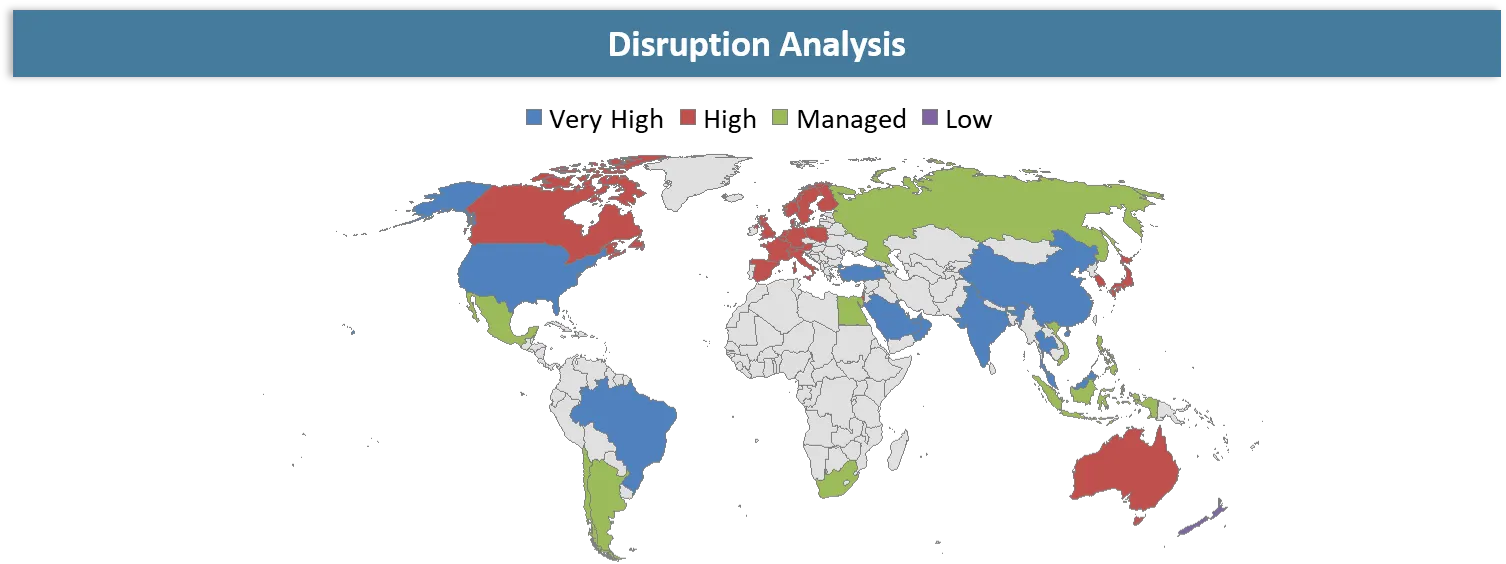

Disruption Analysis

Iron-Air Batteries Reshaping Multi-Day Grid Storage, Renewable Firming and Fossil Peaker Replacement Strategies in Renewable-Heavy Power Systems

Iron-air batteries are poised to disrupt the stationary storage space by offering a business case for grid stability that can span days rather than hours. Where lithium-ion batteries reign in short-term storage, it is much less economically attractive to use these batteries for backup storage that ranges between 24 and 100 hours. Iron-air batteries resolve this issue by leveraging cheap, plentiful iron and an air-based chemical reaction, enabling them to deliver sustained discharge for renewables-heavy grids.

Iron-air batteries would have a significant disruptive effect on storage needs associated with renewable energy firming, resource adequacy, fossil peaker replacement, grid resilience and grid extension. There is a growing trend among utilities towards not only the purchase but also the development of storage solutions capable of delivering capacity values over prolonged periods when the wind and sunlight fail or the demand peaks.

Finally, iron-air batteries might disrupt supply chain strategy by eliminating dependency on rare metals such as lithium, cobalt and nickel. However, market disruption depends not only on successful trials but also on proven economic and financial feasibility of iron-air systems and project warranty.

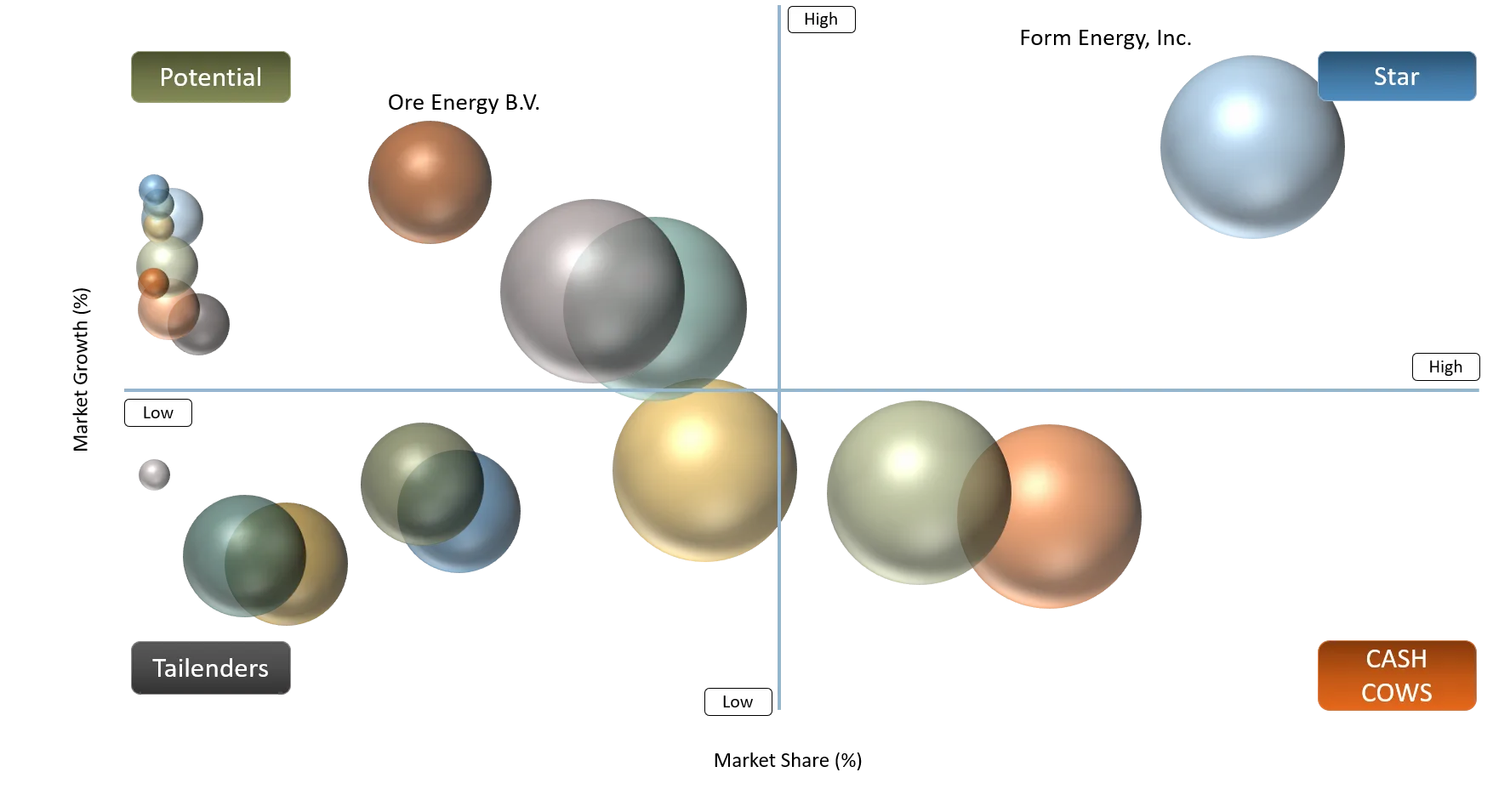

BCG Matrix: Company Evaluation

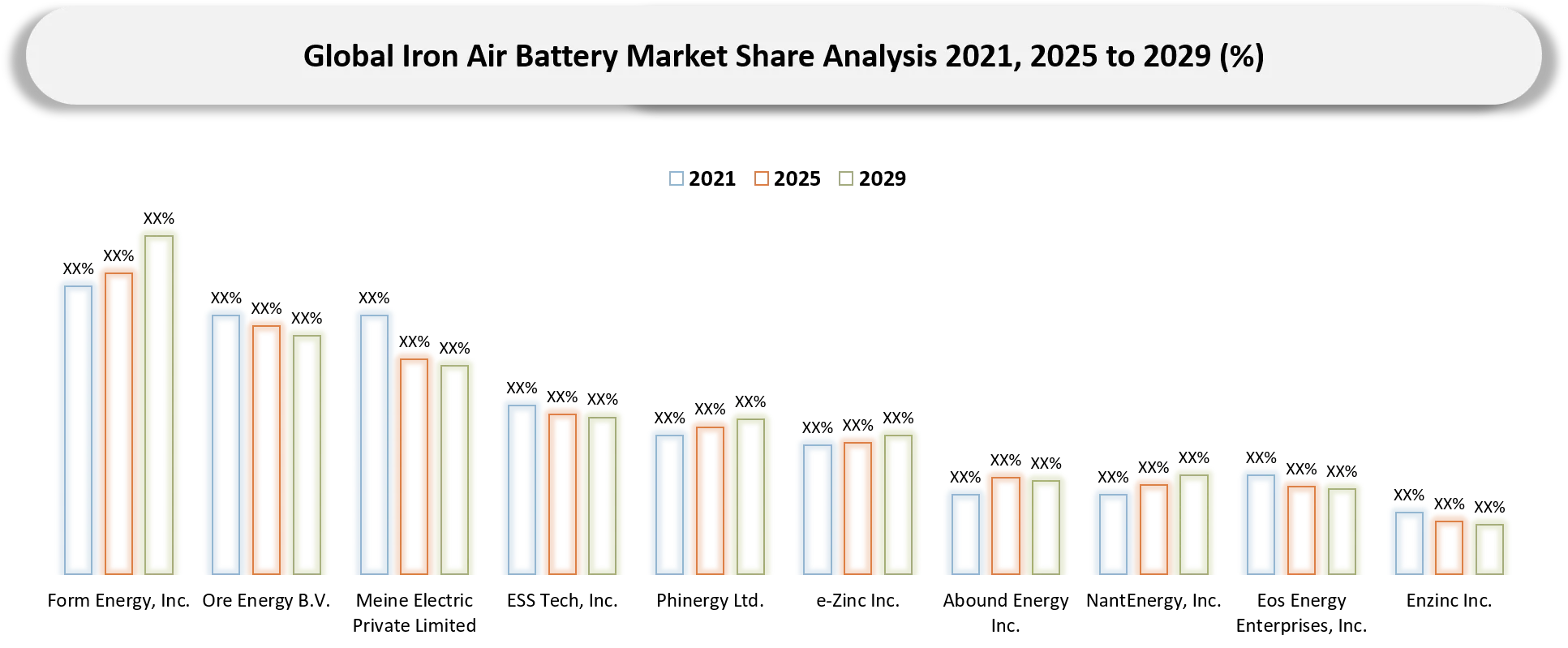

In the iron-air battery market, Form Energy, Inc., Ore Energy B.V. and Meine Electric Private Limited can be positioned as Stars, as they are directly linked to iron-air battery commercialization and operate in a high-growth long-duration storage market. ESS Tech, Inc., Eos Energy Enterprises, Inc., e-Zinc Inc. and Abound Energy Inc. fall under Question Marks, as they are strong adjacent long-duration storage players but not pure iron-air companies. Phinergy Ltd., NantEnergy, Inc., Fuji Pigment Co., Ltd., PolyPlus Battery Company, Inc., Enzinc Inc. and Fluidic Energy LLC can be placed as Niche or Cash Cow Adjacent Players, supported by metal-air, zinc-air or related battery technology expertise, but with weaker direct linkage to iron-air grid storage. Overall, the market is still early-stage, with limited commercial leaders and a broader ecosystem of adjacent technology companies that may support future innovation, partnerships and competitive benchmarking.

Market Dynamics

Rising need for 24–100 hour long-duration energy storage is increasing demand for iron-air batteries in renewable-heavy power grids

The increasing demand for 24-100 hours of long-duration energy storage is emerging as one of the primary factors driving the global iron-air battery market, because power grids having a high share of renewables are increasingly relying on storage systems that provide more than the 4-8 hours provided by lithium-ion-based energy storage systems. Power grids with an abundance of renewables have reliability concerns during cloudy days, days with no wind, peak load in the evening hours, and weather-related events. Iron-air batteries are directly designed to solve this issue through their ability to discharge energy over several days. According to Form Energy, the initial iron-air battery developed by it can store and discharge energy for as many as 100 hours.

This driver is becoming commercially significant as utility companies and grid managers shift from short-term balancing to resource adequacy planning. One such example is the Irish project being planned by Form Energy, which involves a 10 MW 1,000 MWh project, and clearly illustrates how iron-air batteries are capable of delivering large amounts of energy over a number of days. Iron-air batteries are also getting a lot of interest in terms of hyperscale adoption, according to some reports, which point out the use of an iron-air battery from Form Energy with a capacity of 300 MW by Google in its Minnesota-based renewable energy project.

Limited commercial deployment history is creating caution among utilities, investors and project financiers

Limited history of commercial deployments is an important constraint to the iron-air battery market, considering that the battery technology is still at the stage of being transferred from pilot projects to commercial operations. While there are numerous examples of lithium-ion batteries deployed on both large and small scales with proven performance records, iron-air batteries lack comparable historical precedent. As grid storage facilities are typically used for a period of 15-25 years, reliability of performance throughout such a period poses certain risks. The problem, however, lies not in the possibility of the technology itself, but in whether it will reliably perform within specified contractual terms during several days-long discharges, seasonal fluctuations, severe weather conditions and many charging/discharging cycles. The reliability of energy recovery and efficiency, battery degradation, maintenance, safety measures, life cycle and other related issues must be confirmed before large-scale purchases can be made.

It also influences the financing of such projects. Banks may view iron-air battery plants as risky investments in the absence of proven bankability, thereby resulting in high financing costs and reliance on grants and subsidies to finance such projects. This is expected to cause a gradual commercialization process that will see iron-air batteries being accepted as a reliable source of energy storage.

Segmentation Analysis

The Global Iron-Air Battery Market is segmented based on battery system type, battery format, storage duration, electrode architecture, capacity, application, end user, and region.

Rechargeable Iron-Air Battery Systems Lead Market Adoption as Utilities Prioritize Scalable Multi-Day Storage for Renewable Firming and Grid Resilience

Iron-Air Battery Rechargeable Systems are likely to dominate the iron-air batteries sub-segment due to the fact that the market revolves around reusable and stationary long-term storage solutions. Compared to other forms such as mechanical rechargeable and portable iron-air batteries, rechargeable iron-air batteries cater more towards utility procurement whereby the batteries are required to absorb excess energy from solar and wind farms during periods of high energy output and release it during times of grid strain, evening peak times, low renewables and extreme weather conditions.

It is also due to the fact that this particular type of iron-air battery is filling a business opportunity that currently does not exist in terms of short term lithium-ion batteries. The iron-air batteries produced by Form Energy are said to be capable of discharging electricity for up to 100 hours, emphasizing the relevance of rechargeable iron-air batteries in ensuring renewable energy sources last for several days. Moreover, rechargeable iron-air batteries provide an option with reduced risk of exposure to critical minerals.

From a buyer’s point of view, utilities and grid companies will always lean towards rechargeable systems since such systems will deliver operational benefits to the utility company. As long-duration energy storage is increasingly sought after in coming years, rechargeable iron-air batteries will occupy a sizable chunk of market share because of their scalability and usability for repeating cycles.

Geographical Penetration

North America Leads Iron-Air Battery Commercialization as Utilities Accelerate Multi-Day Storage Adoption for Renewable-Heavy and Resilience-Focused Power Grids

The North American market is expected to continue dominating the iron-air batteries segment, due to technology commercialization, utility procurement activity and growing need for long-duration energy storage solutions. The region’s leading country is the U.S., whose activities are underpinned by Form Energy’s iron-air battery platform, which is capable of providing 100 hours of energy storage for grid stability, renewable firming and fossil peaker replacement purposes.

Another factor behind North American growth is increasing installation capacity of utility-scale battery storage. According to EIA estimates, developers are set to commission 24 GW of battery energy storage in 2026, following an all-time high level of 15 GW added in 2025. While the vast majority of installations are lithium-ion in nature, this increasing capacity base illustrates the growing need for unique storage options, which would be applicable to longer-duration use cases. Regulatory environment is also favorable, with the Department of Energy setting an ambitious target of decreasing costs associated with energy storage by 90% within a decade to 2030, if it provides 10 or more hours of capacity.

Another opportunity presented by Canada includes renewable energy integration and reliability of remote power grids as well as energy transition programs. Generally, the North American continent seems like an appropriate choice for the commercialization of iron-air batteries because of several favorable factors.

U.S. Iron-Air Battery Market Trends

United States leads in iron-air battery markets owing to early commercial projects, significant utility involvement, and federal funding for alternative long-duration storage systems not relying on lithium. For instance, Form Energy has secured many U.S.-based iron-air battery projects, including a 1.5 MW, 150 MWh pilot facility in partnership with Great River Energy of Minnesota, and a planned 15 MW, 1,500 MWh battery with Georgia Power. United States Department of Energy has also awarded Form Energy an 85 MW, 8,500 MWh battery in Maine that would become one of the biggest non-lithium battery projects in the world when operational. California Low Emission Development Strategy has invested more than US$ 247 million for the development and commercial deployment of non-lithium long-duration storage technologies in California. These factors make the United States the leading country in iron-air battery commercialization.

Japan Iron-Air Battery Market Outlook

Iron-air batteries are predicted to see a rise in popularity in Japan due to its struggles with renewable integration, insufficient land area, energy security, and a lack of safe, long-term energy storage options. Japan's 6th Strategic Energy Plan aims to increase renewable sources' share in electricity production to 36-38% by 2030, increasing the requirement for energy storage systems capable of handling the intermittent nature of solar energy, managing congestion and balancing over multiple hours or days.

The Japanese government is enhancing the policies supporting storage deployment. METI's subsidy scheme offers a rebate covering up to 50% of the cost of installing batteries larger than 10 MW and having fewer than six hours of duration and 66% in cases when the duration exceeds six hours. Despite the fact that Japan's immediate interest in batteries will remain limited to lithium-ion systems, iron-air batteries have potential uses in scenarios requiring inexpensive and safe energy storage with long durations of discharge, such as renewable stabilization, grid enhancement for islands, microgrids, and reduction of fossil fuels dependence.

Competitive Landscape

The iron-air battery market is highly emerging, with competition led by a small group of direct technology developers and a wider set of adjacent long-duration storage companies. Form Energy, Inc. currently holds the strongest competitive position due to its direct iron-air battery commercialization focus, utility partnerships and large-scale grid storage pipeline. Ore Energy B.V. and Meine Electric Private Limited are emerging challengers with direct iron-air positioning, but they remain at earlier stages of commercialization.

The broader competitive ecosystem includes iron-flow, zinc-air, metal-air and zinc-based long-duration storage players such as ESS Tech, Inc., Phinergy Ltd., e-Zinc Inc., Abound Energy Inc., NantEnergy, Inc., Eos Energy Enterprises, Inc., Enzinc Inc. and Fluidic Energy LLC. These companies compete indirectly by addressing similar grid resilience, renewable firming and long-duration storage requirements. Fuji Pigment Co., Ltd. and PolyPlus Battery Company, Inc. add technology depth through aluminum-air and lithium-air R&D, although their direct commercial linkage to grid-scale iron-air storage is limited. Overall, the market remains innovation-led, with competition shaped by project bankability, storage duration, cost reduction, utility validation and manufacturing scalability.

Recent Developments

- February 2026: Ore Energy completed its 100-hour iron-air long-duration energy storage pilot at EDF Lab les Renardières in France, strengthening Europe’s validation pathway for multi-day grid storage.

- July 2025: Ore Energy connected its pilot iron-air battery system to the Dutch electricity grid, marking one of Europe’s first grid-connected iron-air battery deployments.

- December 2024: Form Energy completed UL9540A safety testing for its iron-air battery system, supporting safety validation and improving utility confidence in large-scale deployment.

- October 2024: Form Energy secured US$ 405 million in Series F financing to expand its iron-air battery business, manufacturing capacity and commercial deployment pipeline.

AI Impact Analysis

The introduction of AI technology in iron-air batteries is anticipated to have a positive effect on the market for such batteries through the enhanced planning, management, and maintenance of long-term storage resources. With grid forecasting that involves artificial intelligence, utilities will be able to accurately forecast generation shortages, peak hours, and extended periods of grid unreliability. This would help in maximizing the charging and discharging of iron-air batteries. AI dispatch optimization will help developers achieve revenue stacking in capacity, energy, renewable firming, and transmission deferral. Situations analysis algorithms will help determine the optimal site for developing such projects. They include proximity to renewable resource hubs, critical network junctions, and decommissioned fossil fuel plants. In addition, predictive maintenance algorithms will help monitor battery operations and minimize the risk of any operational issues. Increased demand for energy among other factors can lead to growth in the development of AI data centers.

White Space Opportunities

In the iron-air battery market, there's a growing chance to create crop-specific and region-specific pest control. This is huge for high-value produce like fruits, nuts, veggies, and vineyards. Also, protected cultivation spots really benefit from residue control and export quality needs. Companies have big chances in long-lasting release products, sprayable pheromones, and smart traps that cut down on manual checking. Plus, there's a lot of room in developing regions of Asia Pacific, Latin America, the Middle East, and Africa. However, limited awareness and product access hold things back a bit. So, firms can expand by forming distributor-led advice models, government-supported integrated pest management programs, and combining pheromones with biocontrols. There's also untapped potential in minor crops and niche pests, where conventional insecticide replacements are thin on the ground but badly needed.

DMI Opinion

Iron-air batteries have become one of the most promising energy storage technologies that can be used for renewable power systems. In contrast to Li-ion batteries, which excel in providing short-term energy storage, iron-air batteries meet the needs of 24-100 hour energy storage that is necessary for the firming of renewable generation and to ensure reliability of the grid. Low prices for abundant iron may provide competitive costs of iron-air battery installation on the utility scale without the need for critical minerals.

Based on DMI expectations, the market development will start with pilot-scale validation followed by commercial use during the coming decades due to the increasing amount of renewable energy and the long duration energy storage demand for grid resilience. Limited experience of the technology operation and the issues regarding the financial bankability are the main problems. However, the successful implementation of large-scale projects will facilitate further investments. Utility companies and grid operators will be the main adopters of the technology, making it a good addition to Li-ion batteries.

Why Does This Report Matter in 2026?

This report is pertinent to the year 2026 because iron-air batteries are in a key early commercialization period due to the efforts of utilities looking to find cost-effective energy storage solutions that will last multiple days. Power grids that depend on a higher share of renewables need to have power storage capacities ranging between 24 to 100 hours in order to accommodate the intermittencies of solar and wind sources and to deal with the problem of curtailment and evening peaks, as well as extreme weather events that may cause a disruption in the source of supply. While lithium-ion batteries perform well for short-term applications, they are often not the best choice from a cost perspective when it comes to multi-day backup. Iron-air batteries provide a differentiated offering in terms of using low-cost, abundant iron while providing long duration resilience in grid services without heavy dependency on critical minerals like lithium, cobalt, and nickel.

Why Choose DataM?

- End-to-End Iron-Air Battery Ecosystem Assessment: DataM provides detailed insights across battery system types, storage duration, applications, end users, system configurations, deployment models and regions, helping clients understand where iron-air battery demand is commercially scaling.

- Commercially Feasible Segmentation: Our segmentation is built around measurable revenue pools such as battery system type, storage duration, application, end user, system configuration, deployment model and region, reducing overlap and improving market-sizing accuracy.

- Long-Duration Storage-Focused Intelligence: The report evaluates demand across renewable energy firming, peak load management, resource adequacy, grid resilience, microgrid storage and transmission deferral applications.

- Competitive and Ecosystem Mapping: DataM tracks iron-air battery developers, metal-air technology companies, long-duration energy storage players, utilities, project developers and strategic investors to provide a clear competitive view.

- Utility and Grid Adoption Analysis: The report assesses how renewable curtailment, resource adequacy needs, fossil peaker replacement, grid resilience planning and LDES procurement programs are shaping iron-air battery adoption.

- Decision-Ready Strategic Add-Ons: Clients receive actionable insights such as BCG matrix, white space opportunities, AI impact analysis, disruption analysis, market dynamics, recent developments and adoption priorities.

- Client-Specific Growth Support: DataM helps companies identify priority applications, high-potential geographies, utility partnerships, project opportunities, technology gaps and commercialization strategies.

Key Procurement Priorities and Buyer Evaluation Criteria

- Buyers in the Global Iron-Air Battery Market are prioritizing providers that can demonstrate proven long-duration performance, reliable multi-day discharge capability, strong safety credentials and grid-scale project execution experience.

- Procurement decisions are shifting from simple battery cost comparison toward total lifecycle value, including storage duration, capacity availability, degradation profile, maintenance needs, warranty strength and levelized cost of storage.

- Utilities, IPPs, renewable developers, grid operators, data centers and government buyers are evaluating iron-air systems based on resource adequacy value, renewable firming capability, grid resilience benefits and fossil peaker replacement potential.

- Buyers are placing higher importance on bankability, including commercial references, project financing support, performance guarantees, insurance acceptance and long-term serviceability.

- Project developers are assessing technology providers based on site integration capability, interconnection readiness, permitting support, EPC partnerships and compatibility with renewable or hybrid storage projects.

- Procurement teams are also evaluating supply chain resilience, use of abundant raw materials, domestic manufacturing potential and lower exposure to lithium, cobalt and nickel price volatility.

Related Report: