Endpoint Security Market Size

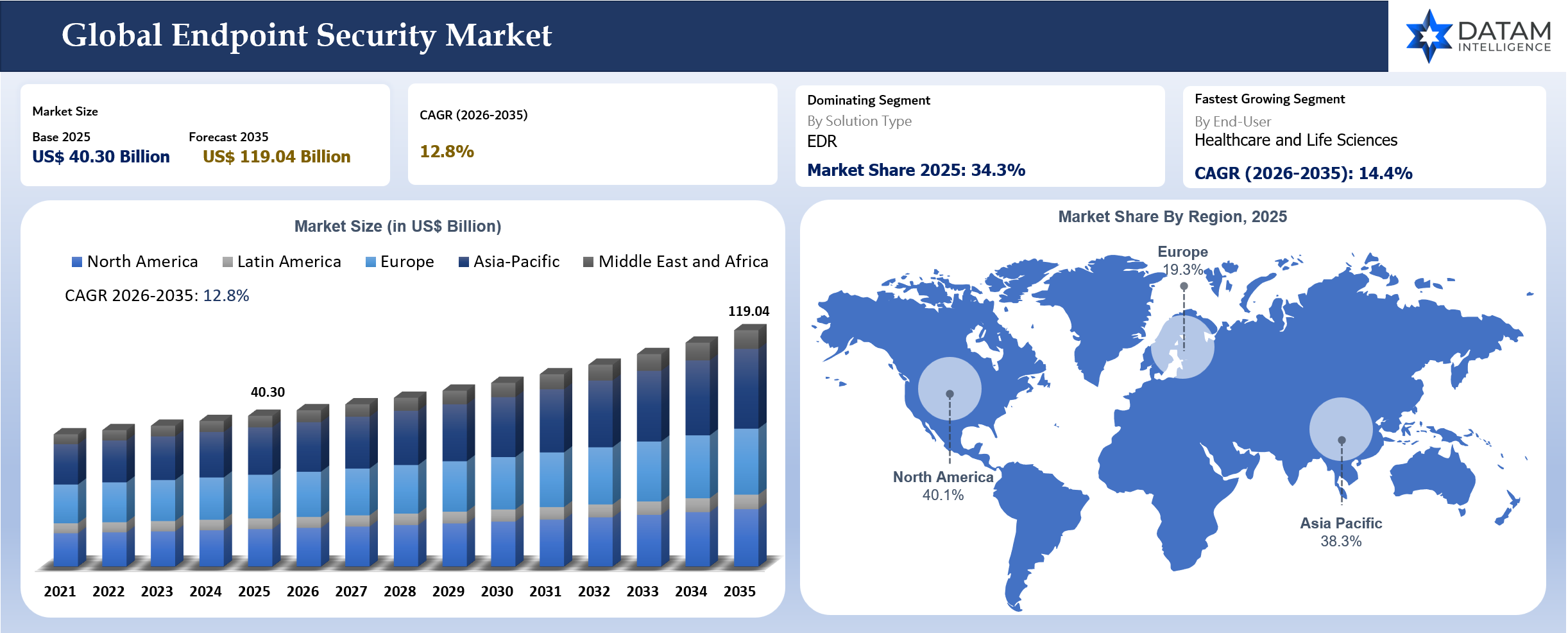

The global endpoint security market reached US$ 40.30 billion in 2025 and is expected to reach US$ 119.04 billion by 2035, growing at a CAGR of 12.8% during 2026 to 2035. Enterprise endpoint protection is moving beyond traditional antivirus because modern attacks use stolen identities, remote tools, browser sessions, cloud applications, and legitimate system processes. Endpoints now serve as the first evidence layer for ransomware, credential theft, remote workforce compromise, and cross-domain attacks. Buyers are therefore shifting toward EDR, XDR, MDR, identity-aware endpoint protection, and AI-assisted response.

Asia-Pacific is becoming the strongest growth region as digital banking, healthcare modernization, government digitization, cloud adoption, and manufacturing cybersecurity expand across India, China, Japan, South Korea, and Southeast Asia. North America remains the largest revenue market because enterprise cybersecurity budgets, ransomware exposure, cyber insurance pressure, and platform consolidation are mature. Supplier differentiation will depend on detection quality, analyst productivity, endpoint agent performance, identity integration, managed response capability and telemetry cost control.

Market Scope

| Metrics | Details | |

| Market Size In 2025 | US$ 40.30 Billion | |

| Market Size By 2035 | US$ 119.04 Billion | |

| CAGR During 2026 To 2035 | 12.8% | |

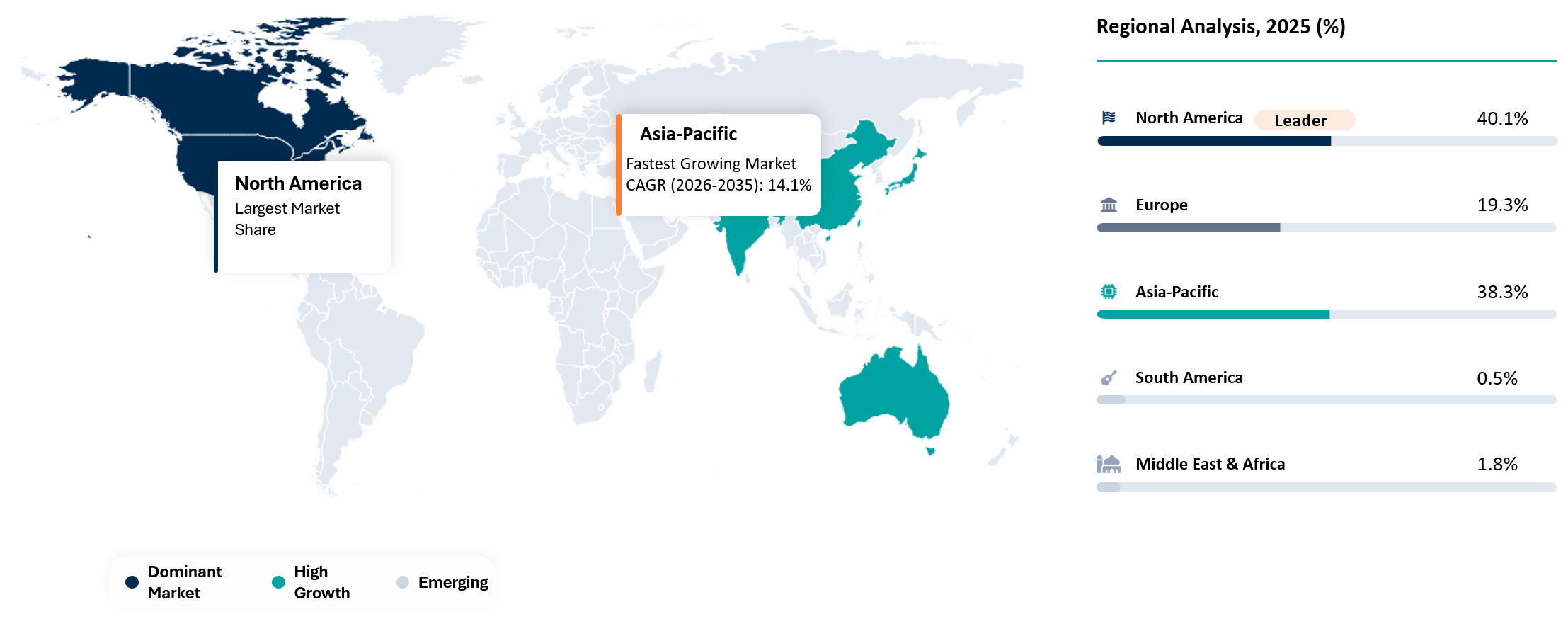

| Largest Region In 2025 | North America, 40.1% market share in 2025 | |

| Fastest Growing Region | Asia-Pacific, 14.1% CAGR between 2026 and 2035 | |

| Key Regional Shift | Asia-Pacific is expected to increase from 38.3% market share in 2025 to 42.5% market share by 2035 | |

| Leading Solution Type | EDR (Endpoint Detection and Response) | |

| Fastest Growing Solution Type | XDR (Extended Detection and Response) | |

| Leading End-User | BFSI | |

| Fastest Growing End-User | Healthcare and Life Sciences | |

| Market Maturity | Growth Stage | |

| Key Buying Question | Which endpoint platform can reduce ransomware dwell time without increasing analyst workload? | |

| By Component | Solution, Services | |

| By Solution Type | EPP, EDR, XDR, MDR, NGAV, Endpoint Firewall, Device Control, Application Control, Endpoint Encryption, Patch and Vulnerability Management, Mobile Threat Defense, Browser Isolation and Browser Security, Others | |

| By Deployment Mode | Cloud, On Premises, Hybrid | |

| By Endpoint Type | Workstations and Laptops, Servers, Mobile Devices, POS Terminals, OT Endpoints, IoT Endpoints, Virtual Desktops, Others | |

| By End-User | BFSI, Healthcare and Life Sciences, IT and Telecom, Government and Public Sector, Manufacturing, Retail and E-Commerce, Energy and Utilities, Education, Transportation and Logistics, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Key Takeaways

- North America remained the largest regional market with 40.1% market share in 2025, supported by advanced enterprise security budgets, cyber insurance pressure, ransomware exposure and high adoption of EDR, XDR and MDR platforms.

- Asia-Pacific is the fastest-growing region with 14.1% CAGR between 2026 and 2035 and is expected to increase from 38.3% market share in 2025 to 42.5% market share by 2035.

- EDR remains the leading solution type because enterprises need endpoint-level investigation, containment and response after prevention fails.

- XDR is expected to be the fastest-growing solution type as buyers connect endpoint telemetry with identity, email, network, cloud and SaaS signals.

- BFSI remains the leading End-User because financial institutions require strong endpoint control, fraud protection, user activity visibility and incident response evidence.

- Healthcare and life sciences is the fastest-growing End-User because clinical uptime, patient data protection and connected medical environments increase exposure to ransomware disruption.

- Supplier differentiation is moving toward AI-assisted investigation, low endpoint agent impact, identity integration, telemetry efficiency, managed response quality and platform consolidation.

Why is the Endpoint Security Market Growing?

The endpoint security market is experiencing strong growth as organizations face an increasing volume of sophisticated cyberattacks targeting laptops, desktops, mobile devices, servers, and connected endpoints. As businesses accelerate digital transformation initiatives and adopt hybrid work models, securing endpoint devices has become a top cybersecurity priority.

One of the primary growth drivers is the rise in ransomware, phishing campaigns, fileless malware, and advanced persistent threats (APTs). Cybercriminals increasingly exploit endpoint vulnerabilities as entry points into enterprise networks, prompting organizations to invest in advanced protection technologies capable of detecting and responding to threats in real time.

The widespread adoption of cloud computing, remote work environments, and Bring Your Own Device (BYOD) policies has further expanded the endpoint attack surface. Security teams are turning to Endpoint Detection and Response (EDR), Extended Detection and Response (XDR), Zero Trust security frameworks, and AI-powered threat intelligence solutions to improve visibility and strengthen cyber resilience.

Additionally, growing regulatory requirements related to data protection, privacy, and cybersecurity compliance are encouraging enterprises to implement robust endpoint security strategies. Industries such as banking, healthcare, government, manufacturing, and technology are increasing investments in endpoint protection to safeguard sensitive information, maintain operational continuity, and reduce cybersecurity risks.

As organizations continue to modernize their IT infrastructure and cyber threats become more complex, demand for intelligent, automated, and cloud-native endpoint security solutions is expected to remain strong across global markets.

Why Does This Report Matter In 2026?

Endpoint security matters in 2026 because ransomware and identity-led attacks are moving faster than traditional security operations can respond. Attackers increasingly use valid credentials, unmanaged devices, remote access tools and legitimate business software to avoid old signature-based defenses. Endpoint protection must now capture behavior, user context, device posture and cloud activity before an attacker reaches sensitive systems.

AI is also changing both sides of the threat model. Attackers can generate better phishing lures, automate reconnaissance, vary payloads and accelerate social engineering. Security teams need AI-assisted triage, incident summarization and automated containment to keep up. Endpoint platforms that reduce investigation time without creating business disruption will become preferred choices.

Tool consolidation is another 2026 priority. Many organizations already operate antivirus, vulnerability management, patching tools, device management, identity tools, SIEM and MDR services. Buyers want fewer agents and more useful telemetry. A strong endpoint security platform must reduce operational friction while improving ransomware containment, investigation quality and executive-level security reporting.

Strategic Indicators For Endpoint Security

High Regulation Impact

Endpoint security is becoming more closely tied to compliance because devices handle customer data, patient records, financial transactions, government information and intellectual property. BFSI, healthcare, public sector, energy and education buyers need endpoint controls that support audit evidence, device compliance, encryption, incident logs, vulnerability management and ransomware response. A basic antivirus tool no longer satisfies the expectations of regulators or cyber insurers.

Incident reporting requirements also increase endpoint telemetry value. Security teams need evidence showing when an attack started, which device was affected, how the attacker moved and whether sensitive data was accessed. EDR and XDR platforms help create this timeline. Buyers therefore evaluate endpoint tools not only by blocking capability but also by forensic detail and reporting usefulness.

Endpoint compliance is also becoming harder because employees use laptops, mobile devices, virtual desktops, servers and cloud-connected applications across multiple locations. Remote work has made device posture a continuous requirement rather than a one-time IT check. Vendors with strong compliance dashboards and integration with identity systems will remain well positioned.

High Investment Activity

Investment is concentrated in EDR, XDR, MDR, identity threat detection, browser security, endpoint vulnerability management and AI-assisted security operations. Vendors are expanding platform coverage because customers want fewer tools and better correlation across attack surfaces. Endpoint platforms are becoming broader security operations layers rather than isolated device protection products.

Mergers and acquisitions show that endpoint vendors are moving into adjacent security categories. Browser security, identity security and AI security are increasingly relevant because attacks often begin or progress outside traditional endpoint malware activity. Vendors that can link endpoint telemetry with identity, browser, SaaS and cloud signals will gain stronger enterprise relevance.

Managed response is another investment area. Many mid-sized organizations cannot staff a full security operations team. MDR turns endpoint telemetry into an operational service with investigation, escalation and response support. This creates recurring service revenue and helps vendors reach customers that cannot manage advanced platforms alone.

Supply Chain Disruption

Endpoint security supply-chain disruption is software-led rather than raw-material led. Vendor cloud availability, update quality, endpoint agent stability, operating system compatibility and telemetry pipelines are critical. A faulty update can affect large endpoint fleets quickly. Buyers therefore review vendor update discipline, staged rollout options, rollback capability and support responsiveness before large deployments.

Operating system changes can also disrupt endpoint performance. Windows, macOS, Linux, mobile operating systems and cloud-managed device environments continue evolving. Endpoint vendors must adapt without slowing user devices or blocking business applications. A platform that creates device crashes, high CPU use or compatibility issues can lose buyer confidence quickly.

Vendor concentration creates additional risk. Endpoint agents have deep system-level access, so enterprises need confidence in vendor security practices and incident handling. Procurement teams are asking more questions about software supply chain, internal security controls, data residency and telemetry handling. Trust is becoming a commercial differentiator.

Pricing Volatility

Endpoint pricing has shifted from per-device antivirus licenses toward broader platform subscriptions. EDR, XDR, MDR, vulnerability management, identity protection, mobile threat defense, browser security and AI investigation are often priced as separate modules or bundles. Buyers may reduce tool count but still face higher recurring cost when premium features and managed services are included.

Telemetry volume creates another pricing issue. XDR platforms depend on large data flows from endpoints, identities, email, cloud and network sources. Storage, retention and investigation costs can rise as coverage expands. Buyers increasingly ask vendors to justify telemetry cost through measurable response improvement and lower incident risk.

Mid-market buyers are particularly sensitive to pricing. MDR bundles can improve coverage but increase recurring spend. Procurement teams compare cost against ransomware downtime, breach response expenses, cyber insurance requirements and internal staffing limitations. Vendors that show clear return through reduced tool sprawl and faster response will defend pricing more effectively.

Procurement Pressure

Procurement teams are under pressure to select endpoint platforms that satisfy security leaders, IT operations and finance teams at the same time. Security teams want high detection quality and rapid response. IT teams want low agent overhead, stable updates and minimal help desk burden. Finance teams want predictable pricing and evidence that tool consolidation will reduce total cost.

Proof-of-value testing is becoming essential. Buyers test detection coverage, false positives, agent performance, operating system support, policy management and integration with SIEM, SOAR, identity and ticketing systems. Vendor claims carry less weight without live validation. Procurement teams also ask for customer references from similar industries.

Migration pressure remains high because many organizations still use legacy antivirus contracts, multiple endpoint tools and fragmented response workflows. Switching can require agent removal, policy rebuilding, staff training and phased deployment. Vendors that provide migration support and clear deployment playbooks can reduce buyer hesitation.

New Technology Adoption

New technology adoption is strongest in AI-assisted investigation, identity-linked endpoint detection, browser runtime protection, mobile threat defense and automated containment. Endpoint alerts are becoming more context-rich as platforms combine process behavior, user identity, device posture and cloud activity. AI can help analysts understand which alerts need immediate action.

Browser protection is gaining attention because enterprise work is increasingly SaaS-based. Session theft, malicious extensions, phishing pages and data leakage can occur inside browser workflows. Endpoint platforms that monitor browser risk and enforce policy can address threats that traditional antivirus may miss.

Automated containment is also expanding. Security teams need tools that can isolate devices, kill processes, block hashes, suspend accounts and stop lateral movement faster than humans can act manually. Buyers still require careful governance because automated actions can disrupt business if misapplied.

Regional Expansion Opportunity

North America remains the largest endpoint security market because cybersecurity spending is mature and ransomware exposure is high. Enterprises in BFSI, healthcare, government, technology and retail invest heavily in EDR, XDR and MDR. Cyber insurance and board-level risk reporting continue to support spending.

Asia-Pacific offers the strongest growth opportunity. India, China, Japan, South Korea, Australia and Southeast Asia are expanding digital banking, cloud adoption, healthcare technology, manufacturing digitization and public-sector cybersecurity. Endpoint modernization is moving from antivirus replacement toward cloud-managed EDR and MDR adoption.

Europe remains a high-value region because of regulatory pressure, data protection requirements and cyber resilience initiatives. Buyers in Germany, France, UK, Italy and the Nordics prioritize audit evidence, data handling, identity integration and supplier trust. Growth is steady, although Asia-Pacific will expand faster due to larger modernization cycles.

Government Policy Support

Government policy supports endpoint security through cyber resilience programs, critical infrastructure protection, public-sector modernization and incident reporting expectations. Agencies, schools, healthcare providers and municipal services increasingly need better endpoint visibility because legacy IT systems remain exposed.

National cyber agencies are also pushing stronger endpoint hygiene. Secure configuration, patching, vulnerability management, multifactor authentication and rapid incident response all depend on endpoint visibility. Government guidance influences private sector procurement, especially in regulated industries.

Public-sector demand can support channel growth. Local managed security providers often help government agencies and smaller public institutions deploy endpoint protection. Vendors with strong partner ecosystems and public-sector procurement readiness will gain advantage.

AI Impact Analysis

AI is reshaping endpoint security because attackers and defenders are both increasing automation. Attackers use AI to improve phishing quality, produce more convincing social engineering, accelerate reconnaissance and vary malware or scripts. Endpoint platforms need behavior-based detection and automated response because known signatures are not enough against fast-changing attack patterns.

Security teams can use AI to reduce investigation time. Endpoint incidents often include process trees, command lines, files, registry changes, user actions and network connections. AI can summarize attack paths, identify likely root causes, recommend containment and reduce analyst fatigue. The greatest value appears where AI helps junior analysts operate closer to senior analyst speed.

AI also introduces new endpoint risk. Employees use AI tools through browsers and desktop applications, sometimes pasting sensitive data into unmanaged tools. Endpoint and browser telemetry can help identify unauthorized AI use, risky extensions and data leakage. Vendors that monitor endpoint activity and AI tool usage together will gain relevance.

Automation must remain governed. Isolating a device, killing a process or blocking a business application can disrupt operations if done incorrectly. Buyers will prefer AI that is explainable, auditable and connected to human approval for high-impact actions. Endpoint vendors that combine speed with governance will be more trusted.

Disruption Analysis

Endpoint security disruption is coming from the convergence of endpoint, identity, browser, cloud and managed response. Attacks do not stay within one control point. A compromised device can lead to stolen credentials, SaaS access, cloud workload compromise and data exfiltration. Buyers increasingly want platforms that connect signals across domains.

Browser security is a fast-emerging disruption layer. Enterprise work has shifted into SaaS applications and browser sessions. Threats such as malicious extensions, session hijacking, phishing pages and browser-based data leakage require controls beyond traditional endpoint malware detection. Endpoint vendors are expanding into browser protection because the browser is now a major enterprise workspace.

MDR is changing the buying model. Many organizations do not have enough analysts to operate EDR and XDR platforms continuously. Managed response turns endpoint telemetry into a service-led outcome. Vendors and partners that can deliver high-quality MDR will capture customers that otherwise cannot use advanced platforms effectively.

Platform bundling is also reshaping competition. Microsoft and large platform vendors can bundle endpoint security with identity, email, device management and cloud tools. Specialist vendors must prove superior detection quality, faster response or lower operational burden to defend premium pricing. Competitive advantage will depend on measurable security outcomes rather than feature lists alone.

BCG Matrix: Company Evaluation

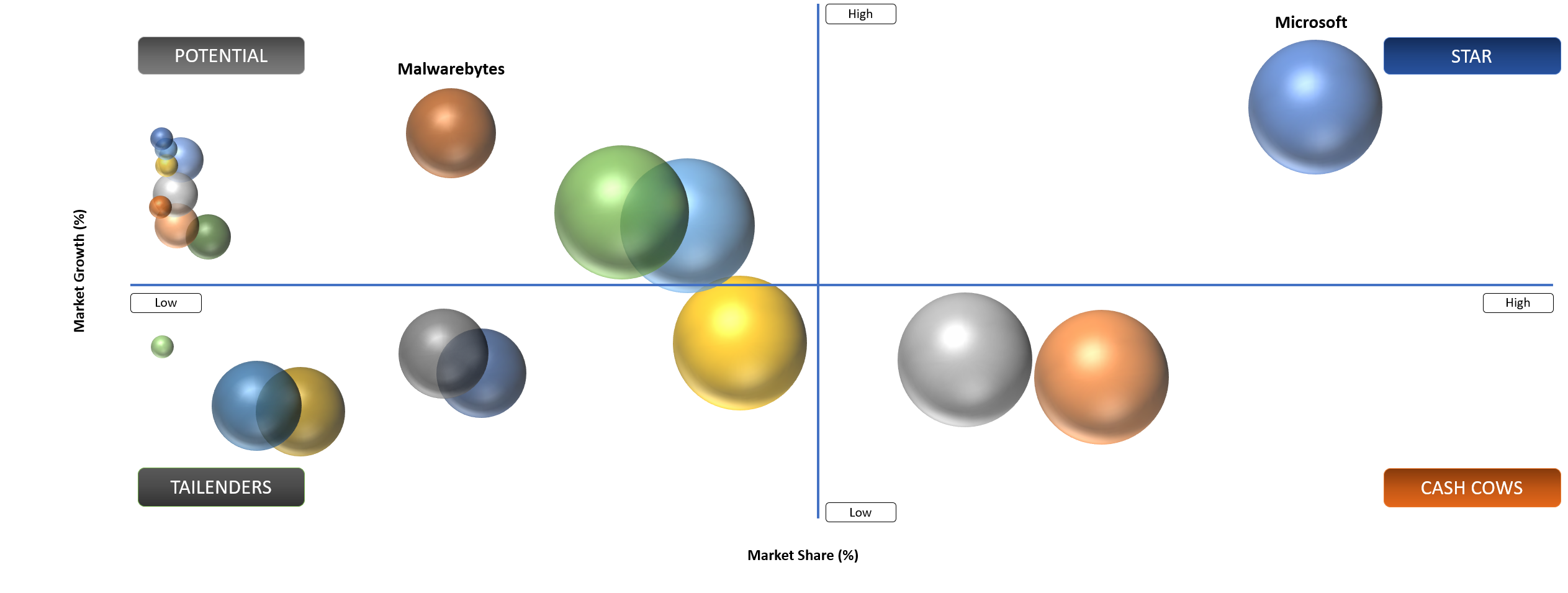

Star

Star players include CrowdStrike Holdings, Inc., Microsoft Corporation, SentinelOne, Inc., Palo Alto Networks, Inc., Trend Micro Incorporated, Sophos Limited, Bitdefender SRL, Check Point Software Technologies Ltd. and Trellix. These companies combine broad endpoint protection portfolios, EDR and XDR capabilities, AI workflows, enterprise buyer trust and strong partner ecosystems. CrowdStrike and Microsoft are particularly strong because they influence how buyers think about platform depth, telemetry quality and response automation.

Potential

Potential companies include Malwarebytes Inc., BlackBerry Limited and WatchGuard Technologies, Inc. Malwarebytes can gain share among mid-market and managed service provider customers through simpler endpoint protection and MDR-led delivery. BlackBerry has potential in selected regulated and embedded environments where Cylance-based AI security and legacy customer relationships remain relevant. WatchGuard can expand through unified security bundles and channel-led endpoint protection for SMEs that need practical protection without complex operations.

End Point Security Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact | Demand Concentration | Impacted Use Case | Strategic Impact |

AI-Powered Ransomware and Identity Abuse Increase Endpoint Detection Demand | High | North America, Europe and Asia-Pacific | EDR, XDR and MDR | Supports behavior-based detection and automated response |

Remote Work Expands Unmanaged Device Exposure | High | Global Enterprises | Device Compliance and Threat Detection | Raises demand for cloud-managed endpoint security |

Security Teams Shift From Antivirus To EDR and XDR | High | BFSI, Healthcare and Government | Incident Investigation | Accelerates platform migration |

MDR Adoption Grows Due To Analyst Shortage | Medium To High | SMEs and Mid-Market Buyers | Managed Response | Expands service revenue |

AI-Powered Ransomware and Identity Abuse Increase Endpoint Detection Demand

Ransomware groups are becoming more operationally mature and faster-moving. Attacks increasingly begin with credential theft, phishing, remote access tools and exposed services rather than obvious malicious files. Endpoint security must detect unusual behavior, privilege misuse, suspicious scripts and lateral movement. EDR and XDR are gaining because prevention alone cannot stop every intrusion.

Identity abuse makes endpoint security more important. A legitimate user account operating from a compromised device can bypass many static controls. Endpoint telemetry helps security teams understand whether the device, user behavior and access pattern match normal activity. Identity-aware endpoint security improves detection quality because it combines user context with device behavior.

AI increases the need for faster detection and response. Attackers can generate convincing social engineering content and adapt quickly. Security teams need tools that can prioritize alerts, explain attack chains and automate containment. Endpoint platforms that reduce mean time to detect and mean time to respond will capture larger budgets.

The business case is strongest where downtime is expensive. BFSI, healthcare, government, manufacturing and retail cannot afford widespread endpoint disruption. Buyers increasingly connect endpoint security with business continuity, cyber insurance readiness and executive-level risk management.

Restraint Impact Analysis

| Restraint | Drag On Market Growth | Primary Impact Area | Impacted Use Case | Strategic Impact |

Endpoint Tool Sprawl Raises Operational Burden | High | Large Enterprises | EDR, XDR and Vulnerability Tools | Drives platform consolidation |

Telemetry Cost Pressures XDR Budgets | Medium To High | Cloud Analytics | Data Retention and SIEM Integration | Raises price scrutiny |

Agent Performance Concerns Slow Migration | Medium | Device Operations | Endpoint Deployment | Requires proof of low device impact |

Legacy Antivirus Contracts Delay Platform Switching | Medium | SMEs and Public Sector | Antivirus Replacement | Slows upgrade cycles |

Endpoint Tool Sprawl Raises Operational Burden

Many enterprises already operate antivirus, endpoint detection, vulnerability scanning, device management, encryption, identity and ticketing tools. Adding another endpoint platform can increase alert volume and administration workload. Security leaders want better detection, but IT operations teams often resist additional agents that may slow devices or break applications.

Telemetry cost also restrains adoption. XDR value depends on collecting and correlating data, but data storage, retention and ingestion can increase total cost. Buyers are asking whether additional telemetry actually improves detection or only adds noise. Vendors must show that data collection reduces investigation time and improves incident outcomes.

Migration complexity can slow replacement. Removing old agents, deploying new policies, training analysts and integrating with SIEM or SOAR can take months in large organizations. Legacy contracts and procurement cycles add delay. Vendors that provide migration playbooks, deployment support and proof of low device impact can reduce friction.

False positives remain a practical concern. Overly aggressive endpoint controls can block legitimate applications, frustrate users and increase help desk tickets. Buyers want protection that is strong but not disruptive. Endpoint vendors need to balance prevention, detection and usability.

Segmentation Analysis

EDR (ENDPOINT DETECTION AND RESPONSE) will remain the core enterprise endpoint control.

EDR (ENDPOINT DETECTION AND RESPONSE) will remain the core enterprise endpoint control because prevention cannot stop every attack. Modern adversaries often use legitimate tools, stolen credentials and native operating system functions. EDR gives security teams visibility into process activity, command execution, file changes, persistence mechanisms and lateral movement. These signals are essential for understanding how an incident developed.

Enterprise buyers value EDR because it supports investigation and containment. A ransomware incident requires quick answers: which device was first affected, which user account was involved, which systems were touched and whether lateral movement occurred. EDR provides the timeline and evidence needed to act. Strong EDR platforms reduce guesswork during a crisis.

EDR is also becoming the foundation for MDR. Managed response providers rely on endpoint telemetry to investigate alerts and contain threats. Customers that lack internal analysts can still benefit from advanced endpoint data when an MDR provider operates the workflow. This makes EDR relevant across both large enterprises and mid-market companies.

Market competition in EDR is shifting from detection claims to operational performance. Buyers want low false positives, useful context, fast search, reliable isolation and integration with identity and cloud systems. Vendors that help analysts move from alert to action will defend share.

XDR Is Expanding Endpoint Security Into Cross-Domain Detection

XDR is growing because endpoint alerts become more useful when connected with identity, email, network, cloud and SaaS signals. A suspicious process on a laptop may be part of a larger attack involving phishing, stolen credentials and cloud access. XDR helps security teams see the complete chain rather than isolated device events.

Buyers are adopting XDR to reduce tool fragmentation. Security operations teams often struggle with separate consoles and duplicate alerts. XDR promises correlated incidents, better prioritization and faster response. The strongest XDR platforms will integrate endpoint telemetry with identity and cloud data without creating excessive data cost.

AI improves the XDR value proposition. Cross-domain incidents can be difficult to analyze manually because data comes from many systems. AI-assisted summaries and recommended actions help analysts understand the attack faster. Vendors that make XDR practical for lean security teams will gain adoption.

XDR adoption still requires careful planning. Enterprises must connect data sources, define workflows, tune detections and manage retention cost. A poorly configured XDR platform can become another dashboard rather than a true response tool. Successful adoption depends on deployment services and operational maturity.

MDR Is Turning Endpoint Security Into A Service-Led Market

MDR is one of the most important growth layers because many organizations do not have enough security analysts to monitor endpoint platforms continuously. Advanced EDR tools create value only when someone can investigate and respond. MDR providers close this gap by offering monitoring, triage, threat hunting and containment support.

Mid-market organizations are the strongest MDR adopters. These companies face ransomware risk but may not have a full security operations center. MDR gives them access to analyst expertise and incident response workflows without building everything internally. Endpoint vendors with strong MDR offerings can reach customers that would otherwise remain on basic antivirus.

MDR also affects vendor selection. Buyers evaluate not only the software but also the human response quality. Escalation speed, communication, service-level commitments and response authority matter during incidents. A strong platform with weak service can disappoint customers.

Service-led delivery can improve retention. When an MDR provider becomes part of a customer’s incident response process, switching becomes harder. Vendors that combine endpoint telemetry with skilled analysts and clear remediation playbooks can build stronger long-term relationships.

Mobile Threat Defense Is Becoming More Important For Cloud Workforces

Mobile devices now access email, collaboration tools, customer data and business applications. A compromised smartphone can expose credentials and sensitive information. Mobile threat defense is therefore becoming part of broader endpoint security strategies, especially in regulated industries and field-based workforces.

Healthcare, financial services, government and logistics organizations are strong use cases. Employees rely on mobile devices for communication, approvals and customer interactions. Risk increases when bring-your-own-device policies are used. Buyers need protection that respects privacy while enforcing security posture.

Mobile threat defense works best when integrated with identity and device management. A risky device should influence application access decisions. Conditional access can reduce exposure when a mobile device shows suspicious behavior. Endpoint platforms that connect mobile signals with identity controls will gain relevance.

Adoption remains slower than laptop and server protection because privacy and user experience concerns are higher. Vendors need clear policy controls, transparent data handling and low-friction deployment. Mobile security must protect without becoming intrusive.

Market Segmentation

- By Component

- Solution

- Services

- By Solution Type

- EPP (Endpoint Protection Platform)

- EDR (Endpoint Detection and Response)

- XDR (Extended Detection and Response)

- MDR (Managed Detection and Response)

- NGAV (Next-Generation Antivirus)

- Endpoint Firewall

- Device Control

- Application Control

- Endpoint Encryption

- Patch and Vulnerability Management

- Mobile Threat Defense

- Browser Isolation and Browser Security

- Others

- By Deployment Mode

- Cloud

- On Premises

- Hybrid

- By Endpoint Type

- Workstations and Laptops

- Servers

- Mobile Devices

- POS Terminals

- OT Endpoints

- IoT Endpoints

- Virtual Desktops

- Others

- By End-User

- BFSI

- Healthcare and Life Sciences

- IT and Telecom

- Government and Public Sector

- Manufacturing

- Retail and E-Commerce

- Energy and Utilities

- Education

- Transportation and Logistics

- Others

Geographical Penetration

North America Endpoint Security Market Trends

North America led the endpoint security market with 40.1% market share in 2025. The region has mature enterprise cybersecurity budgets and a high concentration of vendors, managed security providers and advanced buyers. U.S. enterprises in BFSI, healthcare, technology, retail and government agencies are early adopters of EDR, XDR and MDR.

Ransomware exposure remains a key purchase driver. Healthcare systems, municipalities, schools and financial institutions have faced operational disruption from endpoint-led attacks. Buyers increasingly view endpoint security as a business continuity control rather than an IT tool. Cyber insurance requirements also push organizations toward stronger endpoint detection, patching and response evidence.

U.S. buyers are also consolidating platforms. Large enterprises want fewer tools and better security operations outcomes. Microsoft benefits from enterprise bundling, while CrowdStrike and SentinelOne compete through endpoint-native detection and response depth. Palo Alto Networks, Cisco, Fortinet and Trend Micro compete through broader security platform integration.

Canada and Mexico show different maturity levels but follow similar direction. Canadian organizations emphasize data protection, compliance and managed detection. Mexican enterprises are increasing security investment as banking, manufacturing and retail digitization expand. Channel partners and managed service providers remain important across both markets.

Asia-Pacific Endpoint Security Market Outlook

Asia-Pacific is the fastest-growing region with 14.1% CAGR between 2026 and 2035. The region is expected to increase from 38.3% market share in 2025 to 42.5% market share by 2035. Growth is supported by cloud adoption, digital banking, healthcare modernization, government cybersecurity programs and manufacturing digitization.

India is a major growth market. Banks, IT services firms, healthcare providers, digital platforms and public-sector agencies are expanding endpoint protection beyond basic antivirus. Cost sensitivity remains important, but ransomware risk and regulatory pressure are pushing adoption of EDR and MDR. Managed security providers will play a large role because many organizations need operational support.

Japan is a high-value market where reliability, vendor trust and documentation matter. Enterprises prefer stable deployment, strong support and low operational disruption. Manufacturing, financial services, healthcare and public-sector buyers are increasing endpoint security investment as remote work, cloud use and supply-chain risk expand.

South Korea, Australia, Singapore and Southeast Asia contribute additional demand. Digital government initiatives, fintech expansion, smart manufacturing and regional cloud adoption raise endpoint exposure. Buyers often need localized support, data residency options and partner-led deployment.

U.S. Endpoint Security Market Landscape

The U.S. remains the single most important country market because enterprise buyers have advanced security operations maturity and large endpoint estates. Organizations often operate across hybrid work, cloud applications, mobile devices and contractor environments, creating complex endpoint exposure. Endpoint security spending is also supported by board-level concern around ransomware and breach disclosure.

Financial institutions prioritize endpoint visibility, fraud prevention, privileged user monitoring and incident response evidence. Healthcare providers prioritize clinical uptime and patient data protection. Government agencies require auditability and endpoint control across distributed departments. Each sector has different procurement criteria, but all demand stronger detection and response.

MDR adoption is growing in the U.S. mid-market because many organizations cannot hire enough analysts. Endpoint vendors and service providers compete by offering 24-hour monitoring, threat hunting and response guidance. Service quality is increasingly as important as product capability.

Agent performance and user disruption remain major concerns. U.S. enterprises often run large application environments with legacy systems and specialized software. Endpoint platforms must deliver strong protection without slowing business operations. Vendors with reliable agents and phased deployment support will win more migrations.

India Endpoint Security Market Analysis

India’s endpoint security demand is expanding quickly because digital banking, IT services, public-sector systems, healthcare, telecom and manufacturing are becoming more connected. Large IT services companies already operate mature endpoint programs, while mid-sized firms are upgrading from antivirus to EDR and MDR. Demand is strongest where customer data and operational uptime are critical.

Banking and fintech are important demand centers. Digital payments and online banking increase fraud and credential attack exposure. Endpoint platforms support device compliance, incident investigation and user activity analysis. Regulatory expectations around cyber resilience are also pushing security modernization.

Healthcare is another growth area. Hospitals, diagnostic chains and health technology companies manage sensitive patient data and connected devices. Ransomware can disrupt care delivery, which raises urgency for stronger endpoint protection. MDR and managed security services will be important because many healthcare organizations lack internal security depth.

Price sensitivity remains high, especially among SMEs. Vendors need flexible packaging, local partner support and managed service options. Cloud-managed endpoint security can reduce deployment burden, but buyers still need proof that the product is effective and affordable.

Japan Endpoint Security Market Growth Outlook

Japan’s endpoint security market is shaped by quality expectations, reliability and long-term vendor trust. Enterprises are cautious with security changes because business disruption is unacceptable. Endpoint vendors must provide stable agents, detailed documentation and strong local support.

Manufacturing is a major demand base. Japanese manufacturers operate complex IT and OT environments with global supply chains. Endpoint protection must support engineering workstations, plant systems, remote access and supplier collaboration. Low disruption is essential because production downtime carries high cost.

Financial services and public-sector buyers prioritize compliance, audit evidence and incident readiness. Endpoint telemetry helps prove control during security reviews. XDR and MDR adoption will rise as organizations seek better correlation and response capability without expanding internal teams too quickly.

Japan will also value AI-assisted investigation, but trust and governance will matter. Buyers will adopt AI features when they are explainable and auditable. Vendors that present AI as analyst support rather than uncontrolled automation will have stronger acceptance.

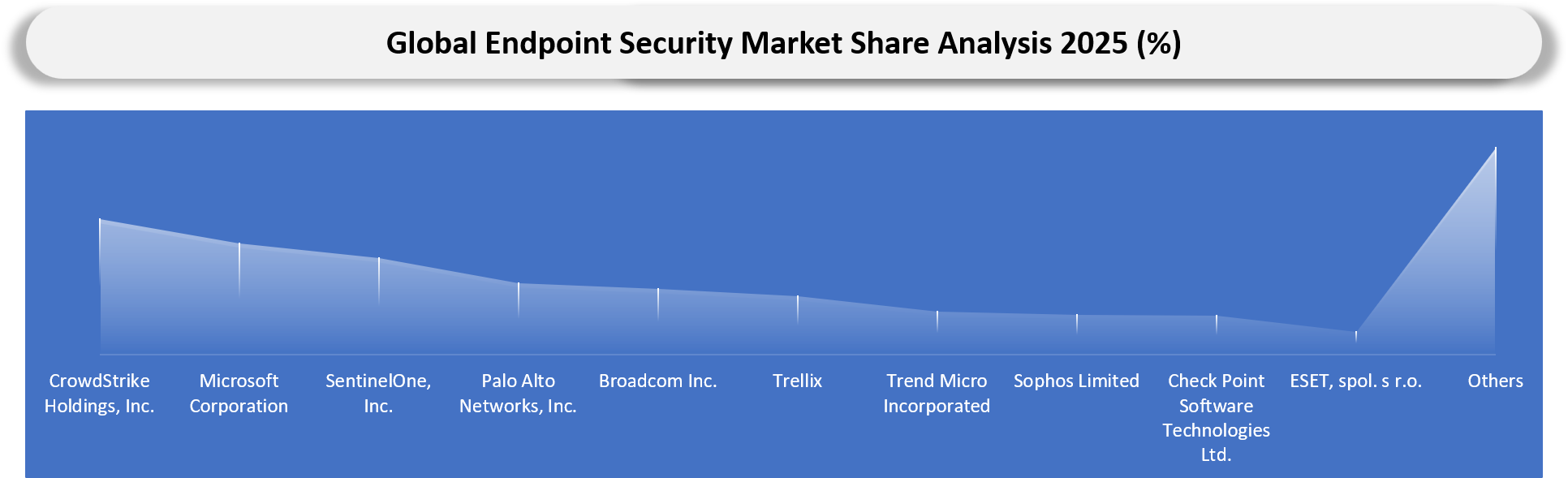

Competitive Landscape

- Competition is split between endpoint-native vendors, cloud platform vendors, network security vendors, MDR providers and identity security companies moving closer to endpoint protection. CrowdStrike, Microsoft and SentinelOne remain highly visible in enterprise endpoint and XDR buying discussions.

- CrowdStrike competes through endpoint-native telemetry, adversary intelligence, managed response and AI-assisted investigation. Microsoft competes through ecosystem bundling, Defender XDR, Intune, Entra and Microsoft 365 reach. SentinelOne competes through autonomous endpoint response, AI analytics and Singularity Platform expansion.

- Palo Alto Networks, Cisco, Fortinet, Trend Micro, Sophos, Trellix, Check Point and Bitdefender compete through broader security platforms. Some buyers prefer integrated security stacks that connect endpoint, network, cloud and operations workflows. This creates pressure on standalone endpoint vendors to prove superior detection and response value.

- MDR providers and channel partners influence mid-market adoption. Endpoint technology alone is not enough when customers lack analysts. Service-led delivery can help vendors reach healthcare, education, local government and SMEs. Partner quality will therefore influence vendor share.

- Competitive benchmarking should track detection efficacy, false positives, agent performance, operating system coverage, MDR quality, identity integration, browser protection, telemetry pricing, response automation, data residency and migration support.

Key Companies

- CrowdStrike Holdings, Inc.

- Microsoft Corporation

- SentinelOne, Inc.

- Palo Alto Networks, Inc.

- Broadcom Inc.

- Trellix

- Trend Micro Incorporated

- Sophos Limited

- Check Point Software Technologies Ltd.

- ESET, spol. s r.o.

- Bitdefender SRL

- Kaspersky Lab

- WithSecure Corporation

- Fortinet, Inc.

- Cisco Systems, Inc.

- Malwarebytes Inc.

- BlackBerry Limited

- VMware LLC

- Tanium Inc.

- WatchGuard Technologies, Inc.

Company Coverage Preview

CrowdStrike Holdings, Inc. is one of the most influential companies in endpoint security because Falcon is positioned around AI-powered protection, detection and response backed by adversary intelligence. Its strength lies in endpoint-native telemetry, threat intelligence, lightweight agent deployment and managed response capability. CrowdStrike benefits from buyer demand for ransomware defense, cross-domain visibility and agentic AI workflows that reduce analyst burden.

Microsoft Corporation competes strongly because Defender for Endpoint is integrated with Microsoft Defender XDR, Microsoft Intune, Microsoft Entra and the broader Microsoft enterprise ecosystem. Its advantage comes from enterprise licensing reach, Windows endpoint presence, identity integration and security operations integration. Microsoft is especially strong among organizations seeking platform consolidation across endpoint, identity, email and cloud workloads.

SentinelOne, Palo Alto Networks, Trend Micro, Sophos, Trellix, Bitdefender, ESET, Check Point, Fortinet and Cisco compete through different combinations of endpoint protection, EDR, XDR, MDR, cloud security and network security integration. The market is increasingly judged by operational outcomes. Buyers compare how quickly a vendor detects suspicious activity, correlate’s identity risk, contains devices and supports response during active incidents.

Major Pain Points

- Alert fatigue slows incident investigation and reduces analyst productivity.

- Endpoint agents can create performance concerns on business-critical devices.

- Telemetry storage and retention costs can increase XDR spending.

- Legacy antivirus contracts and internal migration effort delay platform switching.

- Remote work expands unmanaged device and home network exposure.

- Identity-led attacks can bypass device-only controls.

- Healthcare and public-sector buyers often lack enough security analysts.

- False positives can disrupt users and increase help desk workload.

- Mobile and bring-your-own-device security creates privacy and policy challenges.

- MDR service quality varies widely across providers and regions.

Recent Developments

- January 2026: CrowdStrike agreed to acquire SGNL, strengthening its identity security capability for human, non-human and AI identity use cases.

- January 2026: CrowdStrike agreed to acquire Seraphic Security, expanding browser runtime security coverage for enterprise users and SaaS-heavy workforces.

- August 2025: SentinelOne announced an agreement to acquire Prompt Security, strengthening generative AI security, agent security and data leakage protection.

- September 2025: SentinelOne announced an agreement to acquire Observo AI, strengthening real-time telemetry pipeline capability for AI-native security operations.

- July 2025: Palo Alto Networks announced a US$ 25 billion agreement to acquire CyberArk, strengthening identity security as part of its broader cybersecurity platform strategy.

Analyst View and Opinion

- Endpoint security will remain one of the most durable cybersecurity budget categories because every user, device and workload still creates a practical attack path.

- EDR will remain the foundation of enterprise endpoint security, while XDR will grow faster as buyers seek cross-domain detection and response.

- MDR will continue gaining share in mid-market and resource-constrained organizations because analyst shortages remain a structural problem.

- Identity integration will become a required endpoint capability because attackers increasingly use valid credentials and legitimate tools.

- AI-assisted investigation will become a competitive differentiator, but buyers will demand explainability and governance before allowing high-impact automated actions.

- Microsoft will remain strong where customers prefer platform bundling, while CrowdStrike and SentinelOne will defend premium share through endpoint-native depth and AI-led response.

- Browser security will become more important as SaaS workflows replace local applications and attackers target sessions and extensions.

- Telemetry cost will become a larger procurement discussion as XDR platforms ingest more cross-domain data.

- Healthcare, government and education will remain high-risk verticals because endpoint compromise can directly affect public services and sensitive data.

- Platform consolidation will accelerate, but best-of-breed endpoint vendors can still win when they prove stronger detection and lower operational burden.

Target Audience

| Industry | Who Should Buy This Report? | Reason To Buy This Report |

| BFSI | CISOs, Security Operations Leaders, Risk Teams | Evaluate endpoint protection, fraud exposure, ransomware resilience and regulatory readiness |

| Healthcare and Life Sciences | IT Security Teams, Compliance Teams, Hospital Administrators | Understand ransomware defense, patient data protection and endpoint modernization needs |

| Government and Public Sector | Cybersecurity Program Leaders, Procurement Teams | Assess endpoint security demand across public agencies, municipalities and education systems |

| IT and Telecom | Security Architects, Managed Service Providers | Benchmark EDR, XDR and MDR opportunities across large endpoint estates |

| Manufacturing | Plant IT Teams, OT Security Teams | Assess endpoint control across engineering systems, remote access and production support devices |

| Retail and E-Commerce | Fraud Risk Teams, Security Teams | Evaluate endpoint protection across POS systems, e-commerce operations and distributed stores |

| Investors | Cybersecurity Investors, Technology Funds | Identify high-growth vendors and consolidation opportunities |

| Consulting Firms | Cybersecurity Advisory Teams | Support vendor selection, market entry and security transformation projects |

What DataM Uniquely Provides

- DataM maps endpoint security demand by component, solution type, deployment mode, endpoint type, End-User and region.

- DataM benchmarks vendors across EPP, EDR, XDR, MDR, NGAV, mobile threat defense, browser security and endpoint vulnerability management.

- DataM evaluates pricing pressure across endpoint count, telemetry retention, premium modules, MDR services and platform bundling.

- DataM links endpoint security adoption with ransomware exposure, identity abuse, remote work, healthcare disruption and cyber insurance pressure.

- DataM provides procurement guidance covering detection quality, agent performance, false positives, migration effort, integration depth and service quality.

- DataM helps buyers compare specialist endpoint vendors against platform vendors across measurable operational outcomes.

- DataM supports regional opportunity analysis across North America, Europe, Asia-Pacific, Latin America, Middle East and Africa.

- DataM includes trade intelligence indicators for enterprise software media, network-connected infrastructure and security-related computing hardware.

Related Reports

Endpoint security is closely connected to broader cybersecurity initiatives, including Zero Trust architectures, managed security services, threat analytics, vulnerability management, and AI-driven security operations. As organizations face increasingly sophisticated cyber threats and expanding attack surfaces, integrated security strategies are becoming essential for protecting devices, users, networks, and critical business data. Explore the following reports for deeper insights into the technologies shaping the future of enterprise security.

Zero Trust security market has become a foundational framework for modern cybersecurity strategies, requiring continuous verification of users, devices, and applications before granting access to enterprise resources. As organizations adopt hybrid work models and cloud-first architectures, Zero Trust solutions are playing a critical role in reducing cyber risks and preventing unauthorized access across distributed environments.

Managed Security Services Market: Organizations are increasingly partnering with managed security service providers (MSSPs) to strengthen threat detection, incident response, compliance management, and security operations. Growing cybersecurity complexity and a shortage of skilled professionals are driving demand for outsourced security services that deliver continuous monitoring and proactive risk management.

Security analytics market solutions help organizations identify, investigate, and respond to cyber threats through advanced data analysis, threat intelligence, machine learning, and behavioral monitoring. As cyberattacks become more sophisticated, enterprises are investing in security analytics platforms to improve visibility, accelerate threat detection, and enhance overall security posture.

Artificial intelligence is transforming cybersecurity by enabling automated threat detection, predictive risk analysis, anomaly detection, and faster incident response. AI-powered security platforms help organizations identify emerging threats in real time, improve operational efficiency, and strengthen protection across cloud, network, and endpoint environments.