Rare Earth Elements Market Companies Research Insight

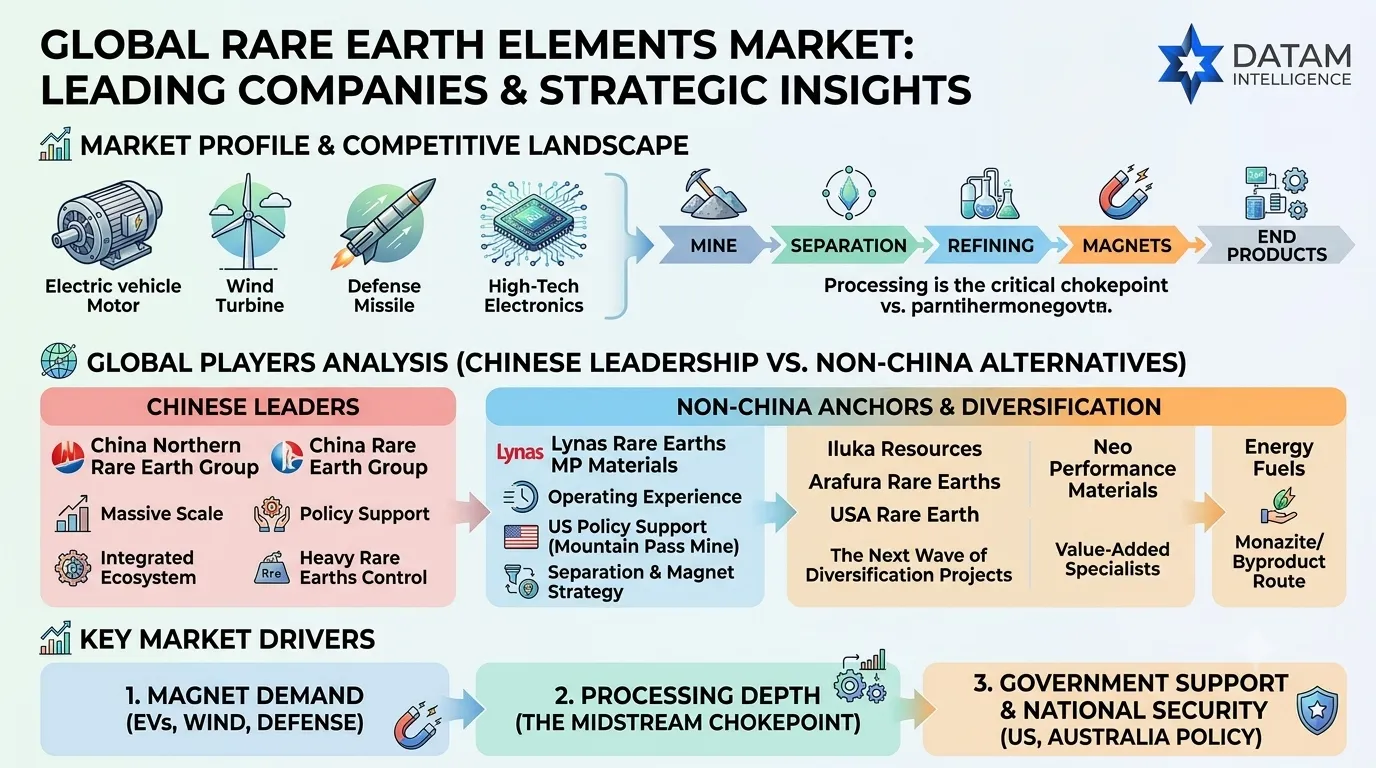

The rare earth elements market has an odd profile. It is not large in the way copper, steel or aluminum markets are large. Yet it carries an industrial weight that is difficult to ignore. A small volume of rare earth material can sit inside an electric vehicle motor, a wind turbine generator, a defense system, a robotics platform or a precision electronics component and become the part that makes performance possible.

According to DataM Intelligence, the Rare Earth Elements Market reached US$ 3.76 billion in 2025 and is expected to reach US$ 8.34 billion by 2035, growing at a CAGR of 8.3% during 2026 to 2035. North America is identified as the largest market, while Asia Pacific is expected to be the fastest growing region. The market covers metals and compounds sourced from bastnäsite, monazite, xenotime, rare earth laterite and other mineral sources, with applications across magnets, catalysts, metal alloys, polishing, ceramics, glass and additives.

Explore the Future of the Rare Earth Elements Market

Request for Rare Earth Elements Market free sample report and discover market trends, demand drivers, segmentation analysis, and strategic insights to support your business decisions.

The competitive landscape is shaped less by mine ownership alone and more by what happens after mining. That is the part people sometimes underestimate. Rare earth ore needs separation. Separated oxides need refining. Magnet materials require alloying, metal making and customer qualification. A mining project may sound strategic, but if it cannot connect to separation and magnet production, its commercial influence is more limited.

China remains the central force. Its position is strongest in processing, refining and magnet materials, which gives Chinese groups a structural advantage that cannot be unwound quickly. A 2025 rare earth processing analysis estimated China’s refining share at nearly 90%, while the IEA’s 2025 critical minerals work highlighted that China leads refining for 19 of the 20 strategic minerals it tracks.

That concentration is pushing Western governments and manufacturers to support companies that can build alternative supply chains. Some will succeed. Some probably will not. Rare earth projects are technically demanding, capital hungry and slow to qualify with customers. The market rewards patience, which is not always what investors want to hear.

Top 10 Rare Earch Elements Market Companies Analysis

China Northern Rare Earth Group

China Northern Rare Earth Group is one of the most important rare earth companies globally. Its position is tied to China’s deep rare earth ecosystem, including mining, separation, refining and downstream material supply. The company benefits from scale, policy support and proximity to China’s magnet and advanced manufacturing base.

Its advantage is not just resource access. It operates inside a system where processing capability, customer demand and industrial policy are already connected. That is difficult for new entrants to match. For global buyers, China Northern Rare Earth remains a benchmark for cost, volume and supply chain integration.

China Rare Earth Group

China Rare Earth Group is another major Chinese rare earth player formed through industry consolidation. Its role matters because consolidation gives China stronger coordination across rare earth mining, separation and processing.

The company is especially important in the context of heavy rare earths, where supply concentration is more sensitive. Dysprosium and terbium matter for high performance magnets, especially where heat resistance and reliability are required. China Rare Earth Group’s influence sits in precisely the part of the market where global buyers feel most exposed.

Lynas Rare Earths

Lynas Rare Earths is the most important non China rare earth producer. That alone gives it strategic weight. The company operates mining and processing assets across Australia and Malaysia, and it is often seen as the clearest alternative to China controlled rare earth supply chains.

Lynas benefits from credibility. It has operating experience, customer relationships and a real supply base rather than only a project pipeline. That matters in rare earths, where many companies look promising for years before proving commercial scale. Still, Lynas faces the same pressure as everyone else outside China. Processing costs, environmental approvals and customer requirements all remain demanding.

MP Materials

MP Materials operates the Mountain Pass rare earth mine in California and is the leading rare earth company in the United States. Its strategic importance increased sharply as the US government placed more focus on domestic rare earth supply chains.

The company is trying to move beyond concentrate production into separation and magnet related activity. That is the right direction because the value in rare earths rises as companies move closer to usable magnet materials. In 2025, the US Defense Department made a major investment in MP Materials to support domestic rare earth processing and magnet supply, showing how closely rare earths are now tied to national security planning.

MP Materials has a strong story. It also has a difficult task. Building a full mine to magnet chain outside China takes capital, technical execution and customer qualification. The market will not reward ambition alone.

Iluka Resources

Iluka Resources is important because of its rare earth refinery strategy in Australia. The company has long experience in mineral sands, and rare earths are becoming a more strategic part of its future positioning.

Iluka’s appeal comes from its location and downstream processing ambition. Australia wants to move beyond exporting raw minerals and build more refining capacity. Iluka sits inside that national strategy. The challenge is that refining is hard. It requires capital, technical control and stable demand from customers willing to support non China supply.

Arafura Rare Earths

Arafura Rare Earths is developing the Nolans rare earth project in Australia. The project is strategically relevant because it is focused on neodymium and praseodymium, which are central to permanent magnets.

Arafura is a good example of the opportunity and the tension in the market. It has strong policy relevance and exposure to magnet demand, but it still needs to move through financing, construction and commercial ramp up. Australia’s support for rare earth projects, including discussion around floor prices and financing support, has helped improve the investment case for companies like Arafura.

USA Rare Earth

USA Rare Earth is trying to build a domestic mine to magnet rare earth supply chain in the United States. Its positioning is attractive because US customers want local sources for defense, EVs and advanced manufacturing.

The company’s value lies in downstream ambition. Mining alone is not enough, and USA Rare Earth has been associated with magnet manufacturing plans as part of its broader strategy. The difficult part will be proving that a domestic US chain can compete on cost, quality and timing. The strategic need is obvious. Commercial execution is still the real test.

Shenghe Resources

Shenghe Resources is a major Chinese rare earth company with influence across rare earth mining, processing and trading. It has also had international relevance through partnerships and involvement in rare earth supply flows outside China.

Shenghe’s strength is market reach. It understands both resource access and downstream demand. In a market where pricing, export rules and supply routes can shift quickly, that commercial flexibility matters. For non Chinese competitors, Shenghe is part of the reason the global market remains difficult to displace.

Neo Performance Materials

Neo Performance Materials is important because it sits closer to value added rare earth materials rather than raw mining alone. The company produces rare earth and rare metal based materials used in magnets, electronics, automotive systems and industrial applications.

Neo’s advantage is technical capability and customer intimacy. It operates in the part of the market where material quality, formulation and qualification matter. That may be less visible than mining assets, but it is often more commercially sticky. Customers do not casually switch suppliers when a material is built into a qualified component.

Energy Fuels

Energy Fuels is better known for uranium, but it has become relevant in rare earths through monazite processing and rare earth carbonate production in the United States. That gives it an unusual position in the market.

The company matters because rare earths can sometimes come from mineral sands and byproduct routes, not only conventional rare earth mines. Energy Fuels is trying to use existing processing infrastructure to enter the rare earth supply chain. It is still early compared with established rare earth companies, but the approach is interesting because it may support supply diversification without relying entirely on new greenfield rare earth mines.

Competitor Analysis: Top Rare Earth Elements Market Players

| Company | Core Position | Strategic Focus | Main Demand Exposure | Competitive Strength |

| China Northern Rare Earth Group | Large scale rare earth mining, separation and processing | Integrated Chinese rare earth supply | Magnets, catalysts, polishing, industrial materials | Scale, cost position and domestic ecosystem |

| China Rare Earth Group | Consolidated Chinese rare earth mining and processing | Heavy rare earth and strategic supply control | Magnets, defense, electronics and advanced materials | Policy backing and processing influence |

| Lynas Rare Earths | Non China rare earth mining and processing | Diversified rare earth supply outside China | Magnets, EVs, wind, defense and electronics | Operating credibility and non China supply position |

| MP Materials | US rare earth mining, separation and magnet chain development | Domestic US mine to magnet supply | Defense, EVs, electronics and advanced manufacturing | Mountain Pass asset and US policy support |

| Iluka Resources | Australian rare earth refining and mineral sands base | Downstream rare earth processing | Magnets, industrial materials and strategic supply | Refinery strategy and Australian resource position |

| Arafura Rare Earths | Australian rare earth project development | NdPr supply for permanent magnets | EV motors, wind turbines and industrial magnets | Magnet focused resource exposure |

| USA Rare Earth | US rare earth and magnet supply chain development | Domestic mine to magnet integration | Defense, EVs and advanced manufacturing | US localization strategy |

| Shenghe Resources | Rare earth processing, trading and resource partnerships | Global rare earth supply flows | Magnets, industrial users and processors | Commercial reach and China market integration |

| Neo Performance Materials | Rare earth materials and value added products | Advanced magnetic and specialty materials | Automotive, electronics, industrial and energy systems | Technical materials expertise and customer links |

| Energy Fuels | Monazite processing and rare earth carbonate production | US rare earth supply diversification | Separation feedstock, magnets and strategic materials | Existing processing base and byproduct route |

The table shows the split clearly. Chinese companies have scale and processing depth. Lynas and MP Materials are the clearest non China anchors. Iluka, Arafura and USA Rare Earth represent the next wave of diversification projects. Neo Performance Materials sits closer to customers and engineered materials. Energy Fuels is the wildcard, using a different feedstock and processing route.

Who Are Other Companies Influencing the Market?

Several other companies shape the rare earth market, even if they are not always in the first group investors mention. Australian Strategic Materials is relevant because of its mine to metals strategy. Hastings Technology Metals and Northern Minerals are watched because they add to Australia’s rare earth project pipeline. Rainbow Rare Earths is important because of its focus on rare earth recovery from phosphogypsum, which gives it a more unconventional supply route.

Pensana is another company that often appears in rare earth supply diversification discussions, particularly in relation to Europe and magnet supply chains. Mkango Resources has relevance through rare earth development and recycling related initiatives. Solvay remains important because rare earth processing chemistry and separation expertise matter more than the market sometimes admits.

Japan linked players also influence the market. Companies involved in magnet manufacturing, electronics and advanced materials help shape demand standards and qualification expectations. The same is true for South Korean and European advanced materials companies that depend on rare earth magnets but may not mine rare earths themselves.

What Is Driving Competition in the Market?

Competition is being driven by magnets first. That is the cleanest way to understand the market. Neodymium, praseodymium, dysprosium and terbium are central to high performance permanent magnets used in electric vehicles, wind turbines, robotics, aerospace systems and defense applications. DataM Intelligence identifies permanent magnets as one of the most important demand areas for rare earth elements.

Processing is the second force, and arguably the harder one. Rare earth supply chains do not end at the mine gate. Separation, refining, alloying and magnet production determine who has real influence. A 2025 academic analysis of rare earth trade risk found that vulnerabilities are often higher in upstream and intermediate input products, including magnets, advanced ceramics and phosphors, which supports the view that midstream chokepoints matter as much as raw materials.

Government support is the third force. The US Defense Department’s investment in MP Materials showed that rare earth supply is no longer being treated as a normal market problem. Australia has also moved toward stronger support mechanisms for rare earth and critical mineral producers, including floor price discussions.

There is also a sustainability layer. Rare earth production can carry environmental and social concerns, especially around processing waste, chemical use and radioactive byproducts from some ores. A 2025 review on sustainable rare earth production highlighted the uncertainty around techno economic assessment, life cycle impacts and social assessment, especially for new production routes and unconventional feedstocks.

The market is attractive, but not forgiving. Demand is improving. Policy support is stronger. Buyers want alternatives. Still, rare earth projects need technical execution, financing, environmental control and customer qualification. In this market, a company does not win by owning a deposit. It wins by turning that deposit into separated, refined, qualified material that customers can trust.