Busway Market Size

The global busway market reached US$ 14.75 billion in 2025 and is expected to reach US$ 27.54 billion by 2035, growing at a CAGR of 6.4% during 2026 to 2035. Demand is being reshaped by data centers, industrial electrification, high-rise commercial buildings, EV charging hubs and brownfield factory upgrades. Busway systems are gaining stronger relevance because users need compact, modular and safer power distribution that can be expanded or reconfigured faster than conventional cable-heavy systems. Data center operators value tap-off flexibility and metered distribution, while industrial users value faster installation, better load balancing and reduced shutdown time during expansion.

Asia-Pacific will remain the largest and fastest-growing region as China, India, Japan and South Korea expand data centers, electronics factories, commercial buildings, metro infrastructure and advanced manufacturing clusters. North America will continue to hold a high-value position through AI data center construction and manufacturing reshoring. Supplier differentiation will depend on short-circuit performance, fire safety, conductor selection, installation speed, digital monitoring, local fabrication capability and service support.

Market Scope

| Metrics | Details | |

| Market Size In 2025 | US$ 14.75 Billion | |

| Market Size By 2035 | US$ 27.54 Billion | |

| CAGR During 2026 To 2035 | 6.4% | |

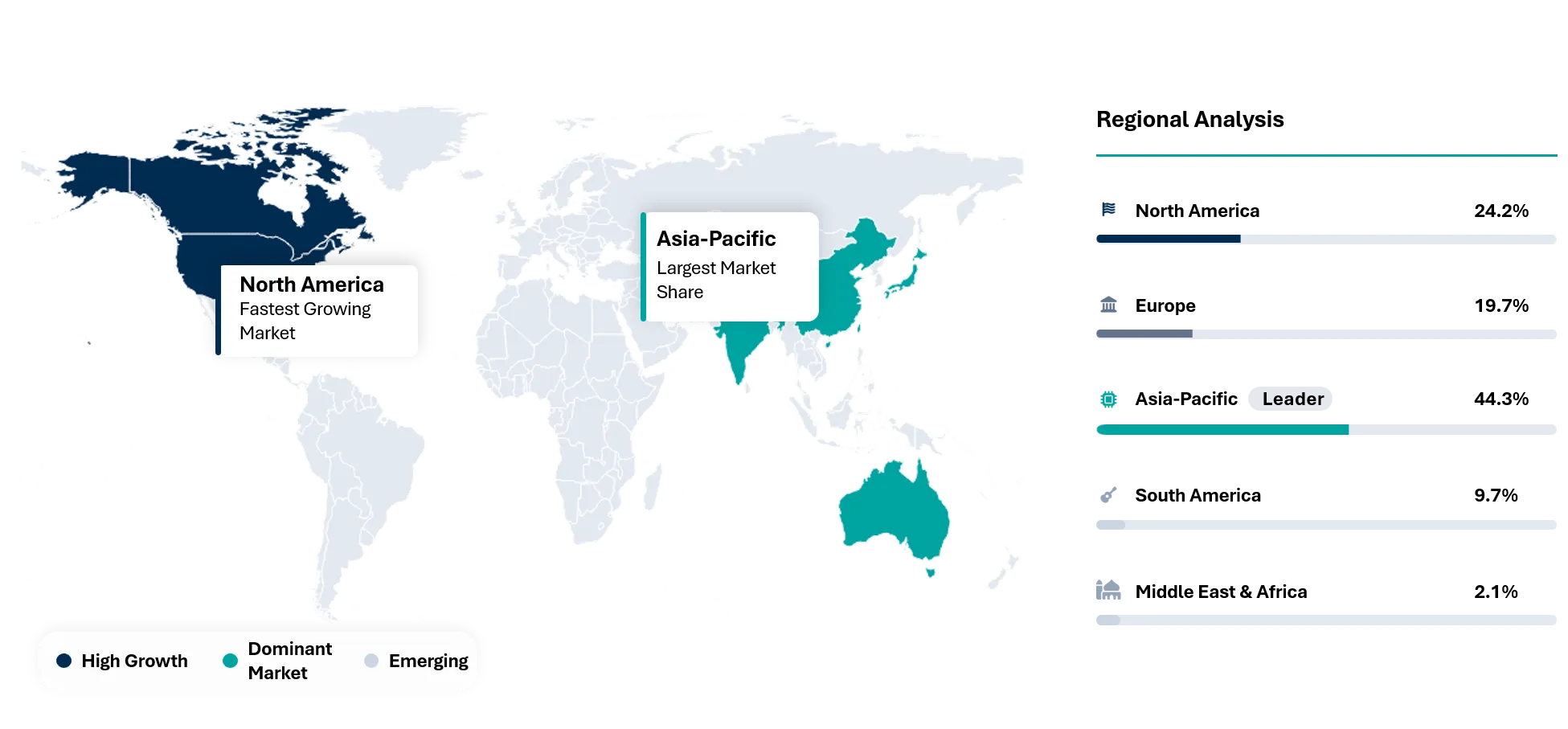

| Largest Region In 2025 | Asia-Pacific, 44.3% market share in 2025 | |

| Fastest Growing Region | Asia-Pacific, 7.2% CAGR between 2026 and 2035 | |

| Key Regional Shift | Asia-Pacific is expected to increase from 44.3% market share in 2025 to 46.7% market share by 2035 | |

| Leading Product | Sandwich Busway | |

| Fastest Growing Product | Data Center Busway | |

| Leading Application | Power Distribution | |

| Fastest Growing Application | Data Center Power Distribution | |

| Market Maturity | Growth Stage | |

| Key Buying Question | Which busway system can reduce installation time, copper exposure and future load expansion risk? | |

| By Product | Sandwich Busway, Air-Insulated Busway, Plug-In Busway, Feeder Busway, Lighting Busway, Data Center Busway, Trolley Busway, Others | |

| By Conductor Material | Copper, Aluminum, Hybrid Conductor | |

| By Power Rating | Below 400 A, 400 A To 800 A, 801 A To 1600 A, 1601 A To 3200 A, Above 3200 A | |

| By Application | Power Distribution, Data Center Power Distribution, Industrial Production Lines, Commercial Building Distribution, Lighting Distribution, Renewable Energy Facilities, EV Charging Infrastructure, Others | |

| By End-User | Data Centers, Industrial Manufacturing, Commercial Real Estate, Utilities, Oil and Gas, Healthcare Facilities, Transportation Infrastructure, Retail and Warehousing, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| South America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Key Takeaways

- Asia-Pacific is the fastest-growing region with 7.2% CAGR between 2026 and 2035 because China, India, Japan and South Korea are expanding high-load electrical infrastructure.

- Sandwich busway remains the leading product because of compact design; lower voltage drops and high short-circuit strength support industrial and commercial power distribution.

- Data center busway is expected to be the fastest-growing product as AI clusters, high-density racks and scalable colocation halls require flexible overhead power distribution.

- Copper conductor busway remains preferred in high-performance projects where compact size, conductivity and thermal performance matter, while aluminum busway supports cost-sensitive projects.

- Industrial manufacturing remains a major customer because production lines need modular distribution that can be modified during layout changes, capacity expansion and automation upgrades.

- Supplier differentiation is moving toward certified assemblies, tested short-circuit performance, digital metering, fast engineering support, local fabrication and installation partner strength.

Why Does This Report Matter In 2026?

Busway demand matters in 2026 because electrical distribution is becoming a constraint in data centers, factories, hospitals, logistics parks and high-rise buildings. Traditional cable routes are often slower to install, harder to modify and more labor-intensive in dense electrical rooms. Busway systems reduce installation complexity by using prefabricated sections that can be installed, extended and reconfigured with more predictable site work.

AI data centers are creating a major shift in customer requirements. Higher rack density increases the need for scalable overhead power distribution and branch-level visibility. Operators want systems that can support future tap-off changes without major shutdowns. Smart metered busway is becoming more relevant because facility teams need to monitor load balance, capacity use and heat risk across halls.

Industrial customers also need busway for flexible manufacturing. EV battery plants, semiconductor fabs, electronics factories, food processing units and automated warehouses frequently change line layouts. Busway allows production areas to expand or change equipment loads without heavy rewiring. A strong report must therefore evaluate power density, conductor cost, regional construction cycles and procurement risk rather than treating busway as a basic electrical accessory.

Strategic Indicators For Busway

High Regulation Impact

Busway systems are shaped by electrical safety standards, fire performance requirements, short-circuit ratings, grounding rules and local installation codes. Customers in data centers, hospitals, factories and public infrastructure require certified assemblies that can withstand fault conditions and operate safely under continuous load. Certification is not a minor purchase requirement because failure can create fire risk, shutdown exposure and legal liability.

Fire-rated routing is becoming more important in high-rise buildings, tunnels, hospitals and data centers. Electrical distribution paths must protect life safety systems and critical loads during emergencies. Busway suppliers need to provide test evidence, technical documentation and engineering support for code compliance. Installers must also follow torque, jointing and route spacing requirements carefully.

Data centers and critical facilities create higher documentation demand. Owners need records on short-circuit withstand, IP ratings, conductor material, temperature rise, tap-off safety and maintenance procedures. Suppliers with stronger compliance documentation can move faster through consultant and owner approval.

High Investment Activity

Investment is strongest in data centers, semiconductor fab, EV plants, battery factories, industrial automation and commercial real estate. Data center capital spending is particularly important because busway systems help operators add or adjust loads across halls. AI workloads increase power density and make flexible electrical distribution more valuable.

Manufacturing investment also supports busway growth. New factories require high-load power distribution, while brownfield plants need retrofit solutions that minimize downtime. Modular busways can reduce installation labor and improve future flexibility. Suppliers with local fabrication and engineering teams can capture projects where speed matters.

Commercial buildings support additional demand. Hospitals, airports, retail complexes, office towers and logistics facilities use busways where power distribution needs to be compact and reliable. Energy efficiency upgrades and electrification programs can also trigger replacement or expansion of existing systems.

Supply Chain Disruption

Busway supply risk is tied to copper, aluminum, insulating materials, steel enclosures, joints, tap-off boxes, meters and factory fabrication slots. Copper and aluminum availability can affect lead times and quoted pricing. Customers working on data center and industrial projects often need firm delivery schedules because electrical distribution delays can hold up commissioning.

Customization adds another supply challenge. Busway systems are engineered to project layout, rating, route and tap-off requirements. Late design changes can create rework and delay fabrication. Engineering coordination between consultants, electrical contractor, equipment supplier and owner is therefore critical.

Regional supply chains are becoming more important. Customers increasingly prefer suppliers with local assembly, regional inventory and installation support. Import delays, tariffs and long ocean shipping routes can affect project schedules. Localized production is becoming a competitive advantage.

Pricing Volatility

Busway pricing is strongly affected by copper and aluminum costs. Copper-based systems can be more compact and electrically efficient, but they expose projects to higher material cost. Aluminum systems may reduce initial cost but require careful evaluation of size, temperature performance and connection quality. Procurement teams increasingly ask for conductor comparisons during bid review.

Project pricing also depends on rating, IP protection, fault withstand, metering, plug-in density, enclosure material, tap-off box count and installation conditions. Data center busway may carry higher pricing because smart metering, overhead routing, flexibility and fast deployment matter. Industrial projects may focus more on ruggedness, safety and long service life.

Price competition is stronger in commercial buildings and lower-rating projects. Premium suppliers defend pricing through tested performance, documentation, warranty support and engineering capability. Low-cost suppliers can win in less demanding applications but may struggle in critical facilities where approval risk is high.

Procurement Pressure

Procurement teams must balance price, lead time, compliance and installation risk. A low-cost busway can become expensive if it causes site rework, fails consultant approval or delays commissioning. Data centers and factories often value certainty more than lowest quoted price. Customers are increasingly comparing total installed cost rather than product price alone.

Electrical contractors influence supplier selection. Contractors prefer systems that are easy to assemble, clearly labeled, supported by technical drawings and backed by local field support. Joint integrity, tap-off handling and route tolerance can affect installation labor. Suppliers with strong contractor relationships can win repeat projects.

Owner priorities are changing. Data center operators want monitoring and load flexibility. Industrial plants want low downtime and expansion readiness. Commercial buildings want safety and maintainability. Procurement decisions now require alignment between owner, consultant and contractor.

New Technology Adoption

Smart metered busway is gaining adoption in data centers and critical facilities. Operators need visibility into power usage, load balance and capacity planning. Integrated metering allows facility teams to identify hotspots, avoid overloads and plan rack changes more accurately. Data center busway is increasingly judged by digital visibility as much as conductor rating.

Prefabrication and digital engineering are also changing project delivery. Busway routes can be modeled in building information platforms to reduce clashes and speed installation. Digital drawings, factory-built sections and modular tap-off boxes reduce site labor. Suppliers that support design coordination can capture complex projects.

Higher protection ratings and fire-rated systems are gaining attention in infrastructure and critical buildings. Customers need safe operation in demanding environments such as tunnels, hospitals, industrial process areas and outdoor service routes. Product innovation is focused on safety, durability and easier maintenance.

Regional Expansion Opportunity

Asia-Pacific offers the strongest expansion opportunity because construction, manufacturing and data center capacity are growing together. China remains a large demand base across industry and infrastructure, while India is expanding through data centers, metro systems, hospitals, commercial towers and manufacturing corridors. Japan and South Korea support premium demand in electronics, semiconductors and high-quality industrial facilities.

North America is attractive because data center and manufacturing reshoring activity are strong. AI infrastructure, semiconductor investment, EV plants and logistics automation support high-value busway demand. Customers place strong emphasis on safety, certification and local support.

Europe remains steady because energy efficiency upgrades, industrial modernization, EV infrastructure and commercial refurbishment support demand. European customers prioritize certification, sustainability and system reliability. Growth is moderate but premium applications remain attractive.

Government Policy Support

Government support for manufacturing, data centers, electrification and infrastructure indirectly supports busway demand. Industrial policies that encourage semiconductor fabs, EV battery plants and advanced manufacturing create new electrical distribution needs. Infrastructure programs for airports, metros, hospitals and public buildings also support demand.

Energy transition policies increase electrical load in buildings and facilities. EV charging hubs, heat pump adoption, renewable integration and electrified industrial processes require stronger internal power distribution. Busways can support these upgrades where cable installations become difficult or space constrained.

Data localization and digital infrastructure policies also matter. Countries building cloud regions and AI data centers require fast power infrastructure deployment. Busway suppliers positioned near data center construction hubs can benefit from repeat projects.

AI Impact Analysis

AI affects the busway market primarily through data center demand. AI training and inference workloads require high-density computing halls with significant power distribution needs. Rack density growth changes how operators plan overhead busway, tap-off density and metering. Busway demand will rise where operators need fast deployment and future capacity changes. AI can also improve busway design and facility planning. Electrical engineers can use design tools to optimize routes, reduce clashes, estimate load distribution and improve installation sequencing. Digital twin and building information modeling workflows help identify conflicts before site installation. Such planning is valuable in data centers and large industrial projects where delays are expensive.

Smart busway data can feed AI-enabled facility management. Metered busway can provide load, temperature and branch usage data. Analytics can help identify abnormal load patterns, capacity constraints and maintenance risks. Data centers and critical facilities are the strongest adopters because downtime risk is high. AI will not replace electrical engineering judgment. Busway systems must still meet safety standards, short-circuit ratings, grounding requirements and local codes. AI will improve design productivity and monitoring, but certified product performance and skilled installation will remain central.

Disruption Analysis

Data center power density is disrupting busway demand. Older power distribution designs may not support rapid rack changes, high-density zones or AI cluster expansion. Overhead busway allows operators to add or move tap-offs with less disruption than cable-heavy systems. This makes busway a strategic infrastructure component in hyperscale and colocation halls. Factory electrification is another disruption. EV production, battery manufacturing, robotics, automated warehouses and electronics assembly require flexible power layouts. Production lines change faster than older fixed wiring systems were designed for. Busway supports reconfigurable power distribution across dynamic facilities.

Metal price volatility is disrupting procurement strategy. Customers compare copper and aluminum options more carefully. Some projects prioritize copper for compactness and performance, while others select aluminum to control cost. Suppliers need transparent engineering guidance to prevent cost decisions from creating future thermal or space constraints. Digital monitoring is also disrupting product selection. Basic busway is no longer enough for some critical sites. Data centers and high-reliability facilities increasingly value metered tap-offs, communication integration and load visibility. Suppliers with smart busway capability can defend premium pricing.

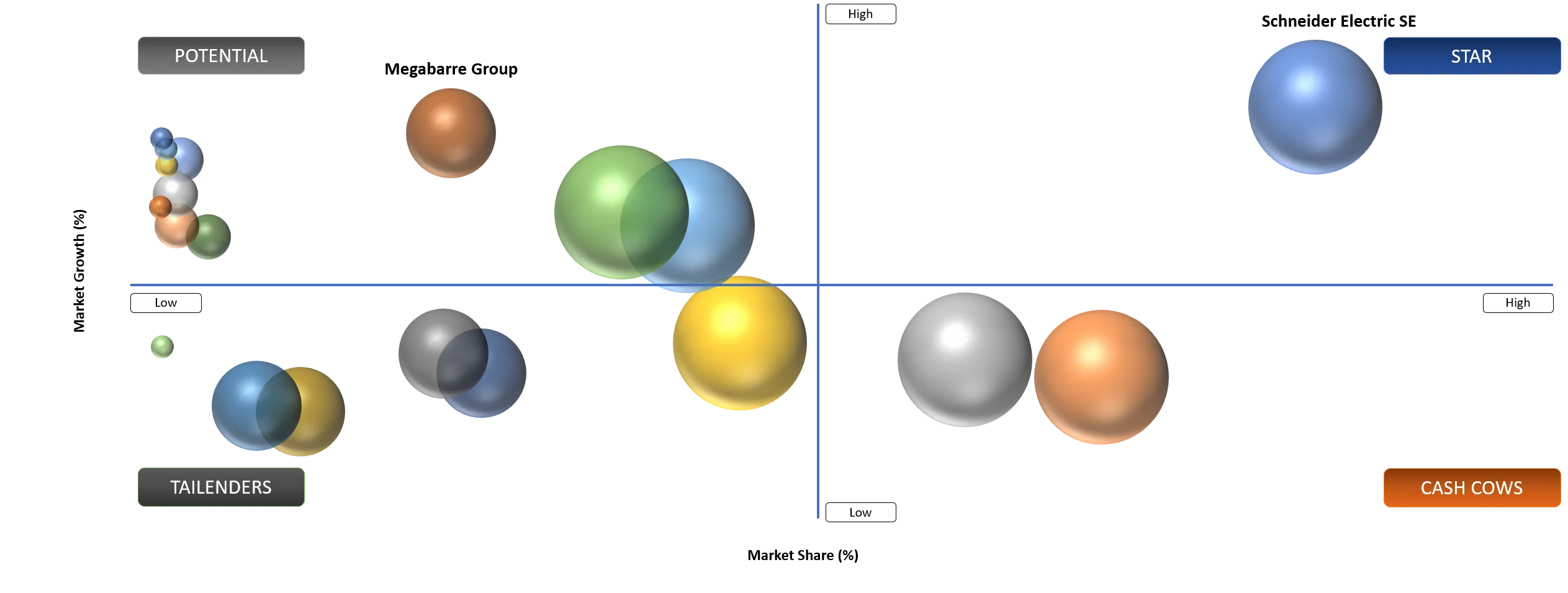

BCG Matrix: Company Evaluation

Star

Star players include Schneider Electric SE, Siemens AG, ABB Ltd., Eaton Corporation plc, Legrand SA, Vertiv Holdings Co, EAE Elektrik A S, C and S Electric Limited and Larsen and Toubro Limited. Companies have strong power distribution portfolios, recognized brands, installation ecosystems and access to data centers, industrial plants, commercial buildings and infrastructure projects. The strongest advantage comes from combining busway systems with switchgear, monitoring, design support and field service.

Potential

Potential companies include Godrej and Boyce Manufacturing Company Limited, Megabarre Group and DBTS Industries Sdn Bhd. Godrej and Boyce can gain share through India’s industrial, commercial and data center infrastructure growth. Megabarre Group can grow in premium project applications where compact busbar trunking and engineering flexibility matter. DBTS Industries can expand through regional manufacturing, price competitiveness and Southeast Asian construction growth.

Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact | Demand Concentration | Impacted Use Case | Strategic Impact |

Data Center Power Density Requires Modular Distribution | High | North America and Asia-Pacific | Data Center Busway | Drives smart metered and plug-in busway demand |

Factory Electrification Increases High-Ampere Distribution Demand | High | Asia-Pacific, Europe and North America | Industrial Power Distribution | Supports sandwich and feeder busway adoption |

Commercial Buildings Shift From Cable Runs To Plug-In Power Ways | Medium | Urban Construction Markets | Commercial Distribution | Reduces installation time and improves flexibility |

Retrofitting Projects Need Faster Installation With Lower Downtime | Medium | Industrial Brownfield Sites | Retrofit Power Distribution | Supports modular busway replacement projects |

Driver: Data Center Power Density Requires Modular Distribution

Data center operators are facing higher power density as AI, cloud computing and high-performance workloads expand. Electrical distribution must support dense equipment zones, changing rack layouts and strict uptime targets. Busway systems help operators add or reposition tap-off units without large cable rerouting, which improves flexibility during expansion. Metered busway is gaining importance because operators need power visibility at room, row and rack levels. Load monitoring supports capacity planning, energy management and risk reduction. Operators can identify imbalance, unused capacity and possible overload conditions more quickly. Smart busway therefore becomes part of data center operations, not just electrical infrastructure.

Colocation providers also value speed. Customer deployments can change quickly and power availability affects leasing. Busway systems support faster fit-outs because tap-offs can be configured as customers add racks. Such flexibility is valuable in competitive colocation markets where speed to revenue matters. The strongest opportunity will be in AI-ready and high-density halls. Conventional cable distribution can become bulky and difficult to modify. Busway provides a cleaner overhead distribution route and allows future expansion. Suppliers that combine busway, metering, integration and data center service support will benefit.

Restraint Impact Analysis

| Restraint | Drag On Market Growth | Primary Impact Area | Impacted Use Case | Strategic Impact |

Copper and Aluminum Price Volatility Pressures Project Cost | High | Conductors and Assemblies | Data Centers and Industrial Facilities | Raises bid uncertainty and substitution pressure |

Poor Installation Planning Raises Thermal and Joint Failure Risk | Medium To High | Site Execution | All Busway Systems | Increases in need for trained installers |

Long Approval Cycles Slow Industrial Replacement Projects | Medium | Industrial Plants | Retrofit Projects | Delays order conversion |

Fire-Rated Route Requirements Increase Engineering Complexity | Medium | Critical Buildings | Hospitals, Tunnels and Data Centers | Raise documentation and testing requirements |

Restraint: Copper and Aluminum Price Volatility Pressures Project Cost

Copper and aluminum price volatility can change project economics between design and procurement. Busway systems use significant conductor material, so quoted cost can move with metal markets. Electrical contractors and owners often need price validity windows, escalation clauses or alternative conductor options to manage risk. Copper remains attractive where compactness and conductivity matter, but it raises cost exposure. Aluminum can reduce material cost but may require larger dimensions and careful joint design. Customers need engineering guidance because the cheapest conductor option may not be the best long-term choice for space-constrained or high-load projects.

Material volatility also affects supplier margins. Manufacturers that quote long-lead projects without strong pass-through terms can face margin pressure. Large projects may require hedging or indexed pricing. Procurement teams increasingly review metal exposure as part of bid evaluation. Project delays can worsen pricing risk. If approvals take months, material prices and production slots can change. Suppliers with clear quotation terms, local sourcing and design alternatives can reduce friction. Customers with early design finalization can also lower cost uncertainty.

Segment Analysis

By Product

Sandwich Busway Will Continue To Lead High-Performance Demand

Sandwich busway will continue to lead because compact design and strong electrical performance suit high-load buildings and industrial facilities. The enclosed structure keeps conductors closely arranged, reducing reactance and supporting efficient power transfer. Customers use sandwich busways where floor space, shaft space and installation efficiency are important. Data centers increasingly prefer compact busway designs because electrical rooms and overhead spaces are under pressure. AI-ready halls need scalable power paths without excessive cable congestion. Sandwich busway supports dense layouts and future tap-off flexibility when designed correctly. Smart metering adds further value to critical facilities.

Industrial facilities also use sandwich busways for production line power. Automotive, electronics, food processing and battery plants need reliable high-current distribution. A compact busway route can reduce cable trays and simplify future expansion. Line changes can be managed with less disruption when plug-in points are planned. Specification of quality matters. A sandwich busway must meet temperature rise, short-circuit withstand and insulation requirements. Joint design and installation torque are critical. Suppliers with tested products, strong documentation and contractor training will maintain an advantage.

Data Center Busway Is The Fastest-Growing Product Opportunity

Data center busway is the fastest-growing opportunity because power distribution has become a strategic constraint in AI and cloud infrastructure. Operators need flexible overhead systems that can support changing rack loads and high-density deployments. Busway allows faster modification compared with fixed cable routes. Metering is becoming a key differentiator. Operators need branch-level load visibility to manage capacity. Smart tap-offs and integrated monitoring can help facility teams avoid overloads and plan future equipment installation. This supports better utilization of electrical infrastructure.

Colocation providers also use busways to improve tenant flexibility. Customers may need different power densities and deployment schedules. Plug-in busway allows operators to serve different layouts without extensive rewiring. Faster installation supports revenue growth. Heat and safety need careful design. High current distribution must avoid hot joints, improper installation and overload. Data center customers prioritize certified systems, maintenance access and reliable monitoring. Suppliers that can provide complete engineering support will capture premium projects.

By End-User

Industrial Manufacturing Will Remain A Core Customer Base

Industrial manufacturing remains a core customer because plants require reliable and flexible power distribution. Production lines change with automation, new equipment and capacity expansions. Busway gives plant owners the ability to add or relocate power drops with less disruption than traditional cable. EV plants and battery factories are important growth pockets. These facilities use heavy electrical equipment, testing systems, robotics and environmental controls. Power distribution must support high loads and frequent layout refinement. Busway helps reduce installation time and future rework.

Brownfield factories represent another opportunity. Older plants often face crowded cable trays and limited electrical room space. Retrofitting with busway can improve safety and maintainability. However, shutdown planning is critical because production downtime is expensive. Industrial customers prioritize reliability and service. Price matters, but failure, risk and downtime matter more. Suppliers with field support, spare tap-offs, fast delivery and local installation partners will be favored.

Market Segmentation

- By Product

- Sandwich Busway

- Air-Insulated Busway

- Plug-In Busway

- Feeder Busway

- Lighting Busway

- Data Center Busway

- Trolley Busway

- Others

- By Conductor Material

- Copper

- Aluminum

- Hybrid Conductor

- By Power Rating

- Below 400 A

- 400 A To 800 A

- 801 A To 1600 A

- 1601 A To 3200 A

- Above 3200 A

- By Application

- Power Distribution

- Data Center Power Distribution

- Industrial Production Lines

- Commercial Building Distribution

- Lighting Distribution

- Renewable Energy Facilities

- EV Charging Infrastructure

- Others

- By End-User

- Data Centers

- Industrial Manufacturing

- Commercial Real Estate

- Utilities

- Oil and Gas

- Healthcare Facilities

- Transportation Infrastructure

- Retail and Warehousing

- Others

Geographical Penetration

Asia-Pacific Busway Market Trends

Asia-Pacific dominated the busway market with 44.3% market share in 2025 and is expected to reach 46.7% market share by 2035. The region is also the fastest growing with 7.2% CAGR between 2026 and 2035. Growth is supported by data center expansion, electronics manufacturing, EV battery plants, commercial towers, metro projects and industrial electrification. China remains the largest regional demand base. Industrial plants, data centers, transport infrastructure and commercial buildings support busway use. Competition is intense because local manufacturers compete strongly on price, but premium projects still value certified performance and engineering support.

India is becoming a major growth market. Data centers, metro rail, airports, hospitals, high-rise buildings, electronics manufacturing and EV plants are expanding. Busway adoption is increasing where cable congestion and installation time create practical problems. Local manufacturing and project support are important. Japan and South Korea remain high-value markets. Semiconductor fabs, electronics plants, data centers and advanced manufacturing facilities require reliable electrical distribution. Customers emphasize quality, documentation and long-term supplier trust. Premium busway systems are well positioned where downtime risk is high.

U.S. Busway Market Landscape

The U.S. is a high-value busway market due to AI data centers, semiconductor fabs, manufacturing reshoring, EV plants and logistics automation. Data center operators need scalable overhead power distribution, metering and fast installation. Industrial users need reliable busway systems for high-load production environments. Data centers are the strongest U.S. demand pocket. AI infrastructure raises power density and accelerates construction timelines. Busway suppliers that can support fast engineering, factory-built assemblies and smart monitoring are well positioned. Electrical contractors also influence supplier selection because installation ease matters.

Manufacturing investment supports additional demand. Semiconductor, battery, automotive and industrial automation projects require high-current distribution. Busways can reduce cable runs and support future layout changes. Brownfield upgrades also create opportunities when plants expand without major building redesign. U.S. customers prioritize certification, safety and service. Local inventory, field support and installation guidance can influence vendor choice. Suppliers that combine strong products with engineering responsiveness will defend share.

India Busway Market Landscape

India is one of the fastest-growing country markets for busway because infrastructure, commercial construction and manufacturing are expanding together. Data centers in Mumbai, Chennai, Hyderabad, Bengaluru and Delhi NCR are increasing demand for modular electrical distribution. Metro projects, airports, hospitals and premium commercial buildings also support adoption. Manufacturing corridors are creating industrial demand. EV plants, battery facilities, electronics production and food processing sites require flexible power distribution. Busway helps reduce installation time and supports future equipment changes. Plant owners are increasingly comparing total installed cost rather than only material price.

India remains price-sensitive, so aluminum busway and locally manufactured systems can be attractive. However, critical facilities such as data centers and hospitals often prioritize certification and reliability over lowest price. Customers need strong technical support to avoid installation failures. Local companies such as C and S Electric, Godrej and Boyce and Larsen and Toubro compete with global suppliers. Project access, contractor relationships and after-sales support matter. International suppliers can win premium projects through technology and documentation.

Japan Busway Market Outlook

Japan is a quality-focused busway market where reliability and documentation matter. Semiconductor facilities, electronics manufacturing, commercial buildings and data centers require robust electrical distribution. Customers prefer proven systems with strong installation control. Data center demand is rising as cloud and AI infrastructure expands. Space constraints in urban sites make compact power distribution valuable. Busways can support overhead routing and future flexibility, especially in colocation facilities.

Industrial users value low downtime. Production facilities often have complex electrical layouts and limited shutdown windows. Busway retrofits must be carefully planned. Suppliers with strong engineering and installation partner networks are better positioned. Japan’s demand growth is moderate but premium. Customers are less likely to switch suppliers based only on price. Technical quality, safety documentation and long-term service support define competitiveness.

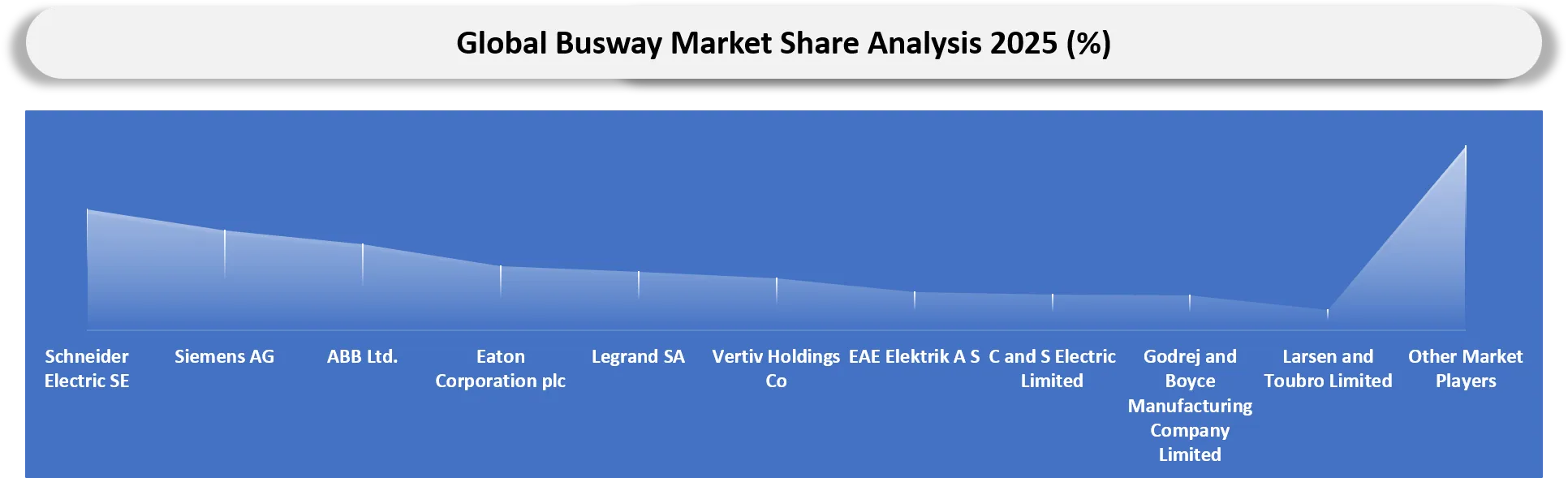

Competitive Landscape

- Competition is led by global electrical distribution companies, regional busway manufacturers, data center infrastructure vendors and local electrical equipment suppliers. Schneider Electric, Siemens, ABB, Eaton and Legrand compete through broad power distribution portfolios and strong consultant relationships.

- Data center competition is becoming more specialized. Schneider Electric, Vertiv, Legrand and Eaton are strong where busway connects with rack power, monitoring and critical infrastructure. Smart metering and integration with power management systems are increasingly important differentiators.

- Regional companies compete strongly on lead time, customization and price. EAE Elektrik, C and S Electric, Godrej and Boyce, Larsen and Toubro, Megabarre, DBTS Industries and Gersan can win projects where local support and cost competitiveness matter.

- Product differentiation depends on conductor material, temperature rise, short-circuit withstand, tap-off safety, enclosure rating, fire resistance, metering capability and installation speed.

- Competitive benchmarking should track certification coverage, data center references, delivery time, local fabrication, contractor support, digital monitoring, warranty terms and metal price exposure.

Key Companies

- Schneider Electric SE

- Siemens AG

- ABB Ltd.

- Eaton Corporation plc

- Legrand SA

- Vertiv Holdings Co

- EAE Elektrik A S

- C and S Electric Limited

- Godrej and Boyce Manufacturing Company Limited

- Larsen and Toubro Limited

- Pogliano BusBar S.r.l.

- Megabarre Group

- Naxso S.r.l.

- DBTS Industries Sdn Bhd

- Vass Electrical Industries Pty Ltd.

- Delta Group

- Rittal GmbH and Co. KG

- LS ELECTRIC Co., Ltd.

- NHP Electrical Engineering Products Pty Ltd.

- Gersan Elektrik Ticaret ve Sanayi A S

Company Coverage Preview

Schneider Electric SE remains one of the strongest busway suppliers through Canalis and its broader low-voltage power distribution portfolio. The company benefits from strong access to data centers, commercial buildings, industrial facilities and electrical contractors. Its advantage comes from system-level capability across switchgear, energy monitoring, automation and power distribution.

Siemens AG competes through SIVACON busbar trunking systems and its broader electrification portfolio. The company is relevant in industrial facilities, buildings and infrastructure projects where engineering depth and reliability matter. Siemens benefits from strong relationships with consultants, contractors and industrial customers.

ABB Ltd., Eaton Corporation plc, Legrand SA, Vertiv Holdings Co, EAE Elektrik A S, C and S Electric Limited, Godrej and Boyce Manufacturing Company Limited and Larsen and Toubro Limited compete across regions and application layers. Competition depends on rating range, certification, local engineering support, manufacturing footprint and project delivery speed.

Data center-focused suppliers and electrical infrastructure companies are becoming more important as AI power density grows. Vertiv, Legrand and Schneider Electric are especially relevant where busway connects with rack power, monitoring and critical power infrastructure. Regional companies can win where local price, short lead time and installation support matter.

Major Pain Points

- Copper and aluminum price swings can change project economics after design approval.

- Late route changes can delay busway fabrication and installation.

- Poor joint installation can create thermal risk and reliability problems.

- Data center operators need faster tap-off changes without power disruption.

- Industrial plants need busway retrofits with minimal shutdown time.

- Fire-rated routes and local code approvals can add engineering complexity.

- Low-cost suppliers may lack documentation for critical facilities.

- Contractor familiarity can influence installation quality.

- Imported systems may face long lead times and tariff exposure.

- Smart metering integration can be difficult when facility software systems are not aligned.

Recent Developments

- June 2026: Legrand announced the acquisition of Girtz Industries in the U.S., adding modular power integration and backup/behind-the-meter power capabilities for data centers, industrial facilities and infrastructure customers.

- May 2026: Legrand acquired SRS Power Engineering in Malaysia, a low- and medium-voltage power protection specialist serving data centers and industrial applications, reinforcing its Asia data center power infrastructure presence after its 2025 Linkk Busway acquisition.

- April 2026: Legrand announced two data center acquisitions, including TES, a U.K.-based specialist in power distribution systems, strengthening its critical power and busway-adjacent portfolio for data center infrastructure.

- March 2026: Vertiv expanded its PowerBar Track busway family with a compact double-stack design for AI and hyperscale data centers, enabling higher power density while preserving valuable white space.

- October 2025: Eaton introduced a next-generation 800 VDC power infrastructure architecture for AI factories, incorporating busbar-based power distribution and busway/cable-tray support for high-density data center environments.

- July 2025: Legrand acquired Amperio Project, a Swiss specialist in busbars, further expanding its data center-related busbar and critical power distribution portfolio in Europe.

- June 2025: Legrand acquired Linkk Busway Systems in Malaysia, an Asian specialist in power busbars for data center grey space, directly strengthening Legrand’s busway and busbar position in Asia.

- March 2025: Schneider Electric announced plans to invest more than USD 700 million in U.S. operations through 2027 to support energy infrastructure, AI growth, domestic manufacturing and data center demand, indirectly supporting demand for busway and electrical distribution systems.

- March 2025: Schneider Electric announced a major U.S. investment program supporting energy and AI infrastructure capacity, reinforcing demand for electrical distribution systems used in data centers and advanced facilities.

- February 2025: Legrand continued expanding its data center infrastructure portfolio through acquisitions and product investment, strengthening its position in power distribution and rack-level infrastructure.

- January 2025: Vertiv expanded focus on data center power infrastructure as AI-driven power density increased demand for modular and monitored distribution systems.

- October 2024: Schneider Electric signed an agreement to acquire a controlling interest in Motivair Corporation, strengthening its data center infrastructure positioning around high-density AI environments.

Analyst View and Opinion

- Busway demand will remain closely linked to data centers, industrial electrification and high-load commercial buildings.

- Data center busway will grow faster than standard building busway because AI and colocation facilities need scalable overhead power distribution.

- Sandwich busway will remain the leading product because compactness and electrical performance support critical facilities.

- Copper systems will remain preferred in space-constrained and premium applications, while aluminum systems will gain traction where project cost pressure is stronger.

- Smart metered busway will become a stronger differentiator in data centers and high-reliability facilities.

- Local fabrication will become more important as customers push for shorter lead times and lower import risk.

- Asia-Pacific will remain the main growth engine through manufacturing, construction and data center expansion.

- Installation quality will remain a major market risk because poorly installed joints can create reliability and safety issues.

- Data center owners will increasingly evaluate busway through lifecycle flexibility rather than upfront material cost alone.

- Competition will intensify between global electrical brands and regional manufacturers with faster local delivery.

Target Audience

| Industry | Who Should Buy This Report? | Reason To Buy This Report |

| Data Centers | Power Infrastructure Teams, Colocation Operators, Facility Managers | Evaluate data center busway demand, smart metering and scalable distribution needs |

| Industrial Manufacturing | Plant Engineers, Electrical Managers, Procurement Teams | Assess busway adoption for production lines, automation and facility expansion |

| Commercial Real Estate | Developers, Consultants, Electrical Contractors | Understand busway demand in high-rise buildings, hospitals, malls and mixed-use projects |

| Utilities | Infrastructure Teams, Substation Project Teams | Track internal distribution and facility power routing opportunities |

| Electrical Contractors | Project Managers, Estimation Teams | Benchmark product selection, lead time and installation advantages |

| Investors | Electrical Equipment Investors, Infrastructure Funds | Identify high-growth electrical distribution categories |

| Consulting Firms | Energy and Infrastructure Advisory Teams | Support market entry, partner identification and supplier benchmarking |

What DataM Uniquely Provides

- DataM maps busway demand by product, conductor material, power rating, application, end-user and region.

- DataM separates data center busway from standard building and industrial distribution to identify higher-growth opportunities.

- DataM evaluates copper and aluminum pricing exposure, installation risk and contractor influence.

- DataM benchmarks suppliers across rating range, certification, smart metering, delivery support and regional footprint.

- DataM links demand to AI data centers, EV manufacturing, industrial automation and brownfield retrofit projects.

- DataM provides procurement guidance covering total installed cost, lead time, code compliance and lifecycle flexibility.

- DataM includes trade intelligence indicators for electrical distribution components and conductor inputs.

- DataM supports partner identification across manufacturers, contractors, consultants and data center infrastructure providers.