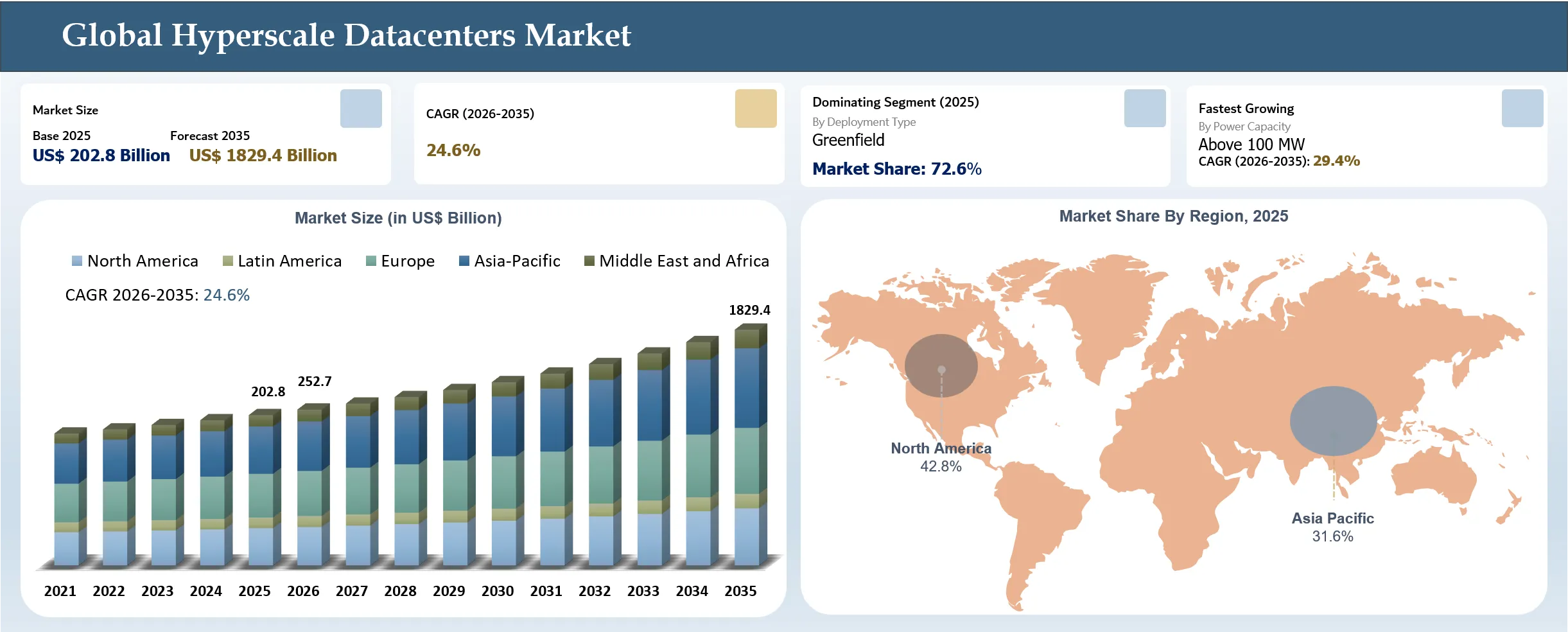

Hyperscale Datacenters Market Size

The global hyperscale data center market reached US$ 202.8 billion in 2025 and is expected to reach US$ 1829.4 billion by 2035, growing with a CAGR of 24.6% during the forecast period 2026-2035, due to the rapid expansion of unprecedented increases in cloud computing load, training of artificial intelligence models, usage of generative AI applications, and the requirement for large-scale data processing. There is a growing trend towards developing hyperscale data centers, which enable high-density computing, storage capabilities at the exabyte level, and low-latency delivery of digital services globally. Significant investment in advanced server infrastructure, liquid cooling, fast interconnect technology, and campuses powered by renewable energy is propelling market growth even more. Major companies such as Amazon Web Services, Microsoft, Google, and Meta Platforms are continuing to scale up their hyperscale data centers in order to cater to the increased computing needs. However, significant investment needs, power availability issues, and grid strain are key factors impacting market growth.

Hyperscale Datacenters Market Key Takeaways

- Greenfield developments make dominate the segment, contributing to about 74.5% of the total capacity increase in hyperscale data centers in 2025 owing to the need for AI ready and cloud native infrastructure.

- AI and Generative AI Workloads are the biggest growth engine with a 35% market growth impact, and this means that AI training clusters, Large Language Models, and AI Inference are the main drivers of hyperscale demand.

- High-Performance Computing (HPC) applications contribute 14% market growth contributions through the increased adoption of hyperscale technology in scientific research, healthcare, manufacturing, military/defense, and financial industries.

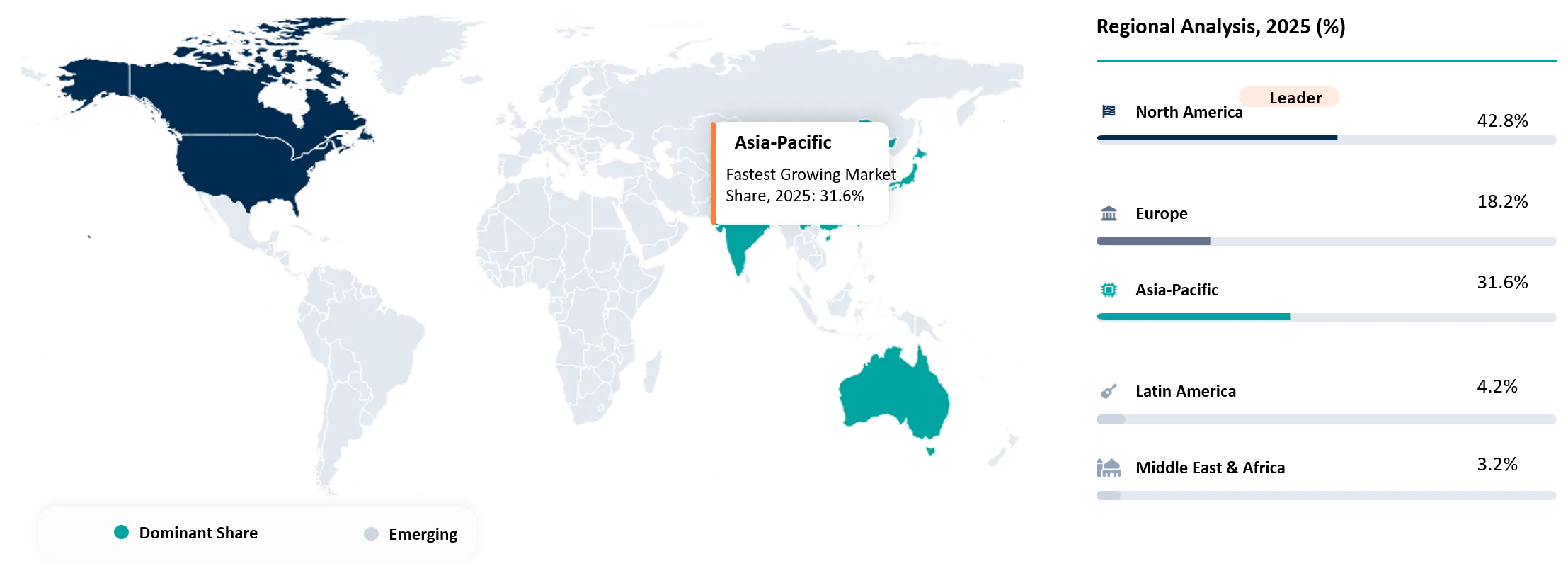

- North America is a dominate region for the hyperscale datacenter market with a share of around 42.9% of global hyperscale data center revenues in 2025 on account of significant investments in AI infrastructure, cloud computing, and hyperscale campus.

Hyperscale Datacenters Industry Trends and Strategic Insight

- Hyperscale data center physical layer and network layer are being radically redesigned to support GPU-dense configurations, due to AI accelerators require significantly higher rack densities, deployments now driving data center location decisions, power purchasing decisions, and innovations in cooling solutions moving away from a commoditized model of capacity planning towards one that is based on workload optimization.

- Accelerated deployment of optical networking technologies due to growing east-west traffic from AI and distributed cloud workloads is driving the adoption of advanced hyperscale datacenters to distribute computing environments.

- Emerging Geographies for Strategic Data Center Growth, hyperscale data centers are gradually venturing into secondary and frontier geographies rather than sticking to conventional hub geographies owing to better power availability, government policy inducements, and lower total cost of ownership, which is a smart way of managing risks and strengthening grid robustness.

- The operators with secured long-term capacity of power and renewable energy shall have an edge over others in future hyperscale rollouts.

- Liquid cooling, custom silicon, and networking technology seem to be some key differentiators shaping efficiency and performance of the workload.

- AI-infrastructure demand is expected to contribute a more significant proportion of the hyperscale CAPEX spend than conventional cloud scale-up in the coming decade.

Hyperscale Datacenters Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 202.8 Billion | |

| 2035 Projected Market Size | US$ 1829.4 Billion | |

| CAGR (2026-2035) | 24.6% | |

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Type | Cloud Data Centers, Colocation Data Centers, Enterprise Data Centers | |

| By Component | Hardware, Software, Services | |

| By Power Capacity | 10 MW–50 MW, 50 MW–100 MW, Above 100 MW | |

| By End User | IT & Telecommunications, Cloud Service Providers, BFSI, Government & Defense, Healthcare & Life Sciences, Media & Entertainment, Retail & E-Commerce, Manufacturing, Others | |

| By Deployment Type | Greenfield, Brownfield | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

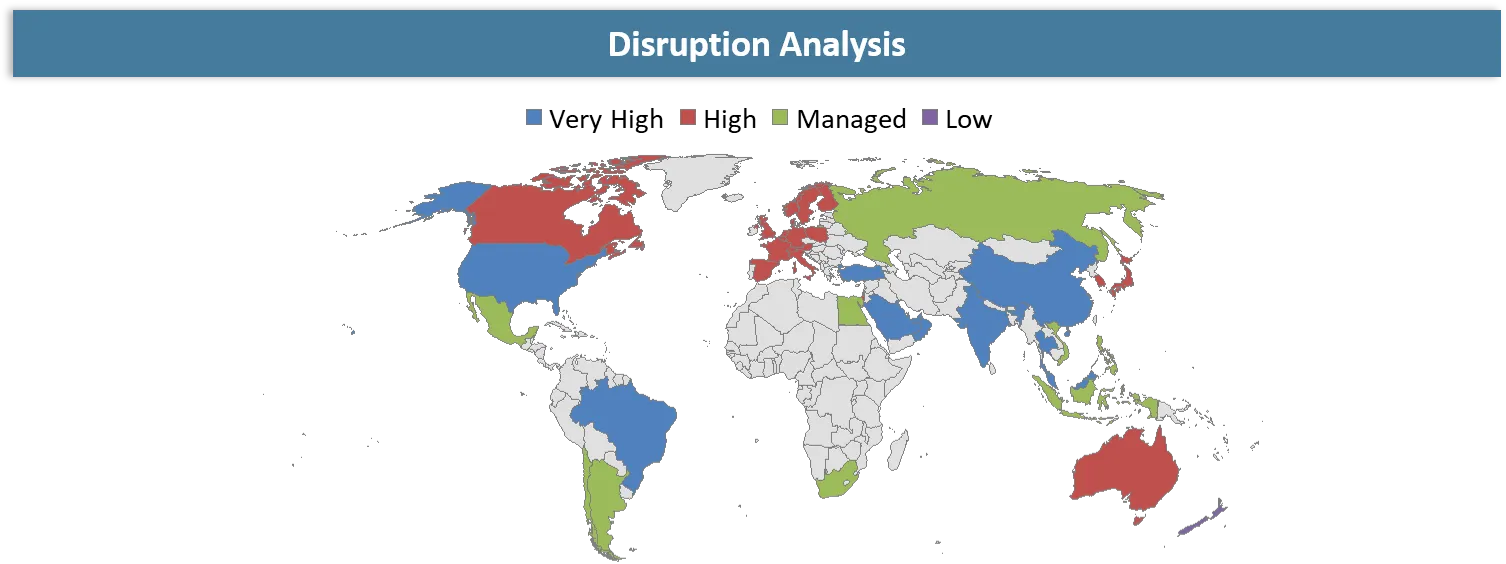

Disruption Analysis

Grid Power Constraints and Utility Connection Delays Reshaping Hyperscale Datacenter Expansion Strategies

The most significant disturbance that has affected the Hyperscale Datacenters Market is the gap that has started to form between the development of hyperscale infrastructure and the expansion of the electrical grid. The increased number of AI-driven computing clusters, cloud systems, and intensive data processing centers has resulted in the need for more electricity that is surpassing the ability of transmission networks and interconnection capabilities of utilities. Consequently, the power availability has become a more crucial element than land availability for the development of hyperscale data centers in some of the biggest data center markets. In accordance with the International Energy Agency (IEA), in 2024 the global data center electricity consumption amounted to about 415 TWh while the growth has been reaching 12% annually and was driven mainly by the expansion of AI infrastructure. In addition, electricity production for the purpose of data centers will be above 1,300 TWh in 2035.

This disruption is necessitating fundamental changes to the site selection process, infrastructure planning models, and capital allocations by hyperscale providers. Although the time to build a hyperscale data center is generally 1-3 years, the time for the development of power infrastructure could be up to 5-15 years. This results in the bottleneck of the power infrastructure development that causes delays to commissioning of facilities and cash flow generation. Major hyperscale regions including Northern Virginia, Texas, Dublin, Frankfurt, and Singapore see more and more investments in direct renewables purchasing, power generation assets, and geographies as a way to overcome the issue of limited grid access. Thus, power infrastructure availability becomes the competitive advantage changing the investment patterns globally.

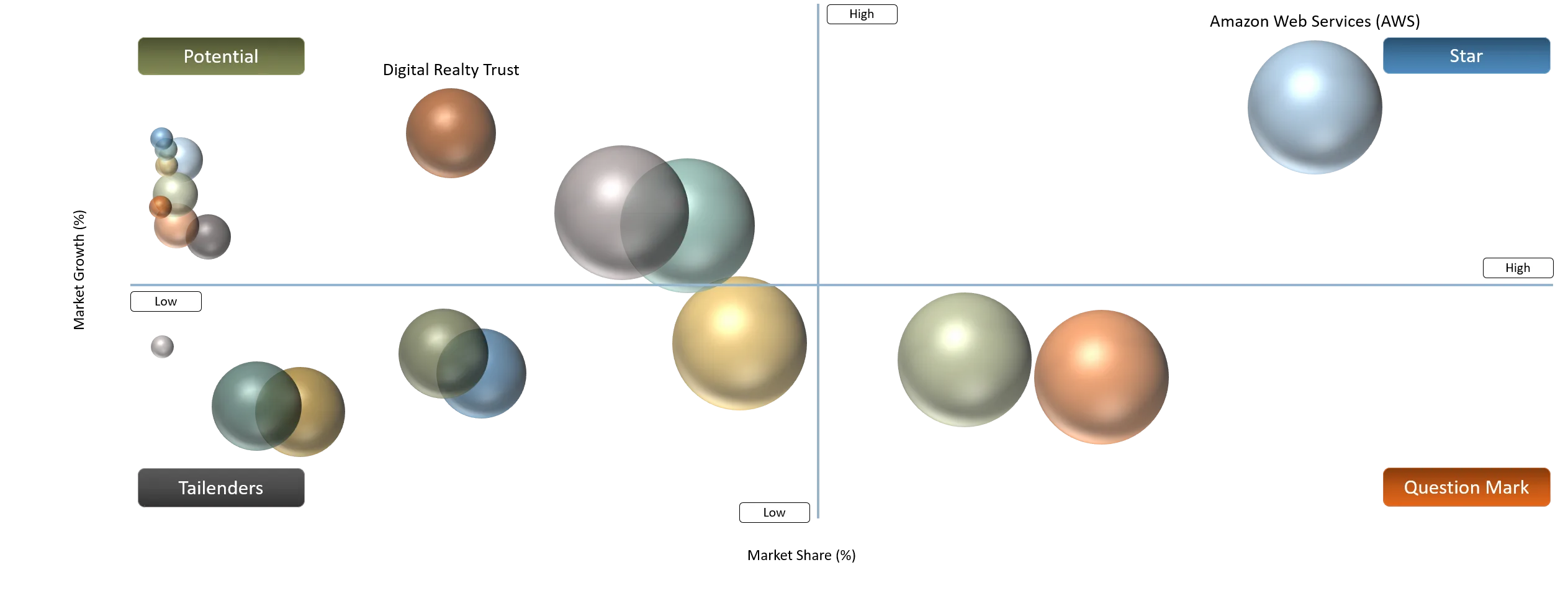

BCG Matrix: Company Evaluation

Stars are Amazon Web Services (AWS), Microsoft, Google, and Meta Platforms because they dominate the market for the deployment of hyperscale infrastructure, cloud computing, and AI-powered datacenters. This quartet is responsible for deploying most of the world’s hyperscale infrastructure and is actively investing in next-generation AI clusters, proprietary silicon, liquid cooling, and multi-gigawatt datacenters. Where, Question Marks include Oracle Corporation, Alibaba Group, and Tencent Holdings as they are still growing in terms of hyperscale infrastructure and cloud services despite facing stiff competition from large-scale cloud service providers. They have been investing heavily in infrastructure used for artificial intelligence computations and growth of regional data centers and cloud native services.

Under the category of Potential, Digital Realty Trust and Equinix feature because of the increasing need for hyperscale colocation, artificial intelligence-enabled facilities, and enterprise cloud connectivity. Both firms have large data center footprints across the globe and have great relations with the hyperscale. With more enterprises adopting hybrid clouds and AI-enabled workloads, these firms are developing more power-dense data centers. IBM is among the group of Tailenders since, while IBM possesses a considerable enterprise technology footprint and cloud infrastructure stack, it falls behind when it comes to expanding their hyperscale data center capabilities and market penetration compared to the leaders in this domain.

Hyperscale Datacenters Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

Rise in demand for Data Sovereignty and Regional Cloud Infrastructure Needs

| 15% | Government Cloud, Sovereign Cloud Providers, Regulated Industries (BFSI, Healthcare, Public Sector) | Regional Data Hosting, Sovereign AI Platforms, Localized Cloud Services | Accelerates hyperscale expansion into secondary markets and drives investments in country-specific cloud infrastructure to meet regulatory compliance requirements. |

Rapid growth in AI and Generative AI Workloads is significantly increasing demand for high-density computing infrastructure

| 35% | AI Developers, Hyperscalers, Cloud Service Providers, Research Institutions | AI Training Clusters, LLM Deployment, AI Inference, Generative AI Services | Primary growth catalyst reshaping hyperscale architecture through GPU-dense facilities, liquid cooling adoption, and multi-gigawatt campus development. |

Rapid adoption to Cloud-Native Architecture by Enterprises

| 26% | Large Enterprises, SaaS Providers, Digital Platforms, Cloud Operators | Public Cloud, Hybrid Cloud, Containerized Applications, Multi-Cloud Environments | Drives sustained hyperscale capacity expansion as enterprises migrate mission-critical workloads from on-premises environments to cloud ecosystems. |

Development of advanced Semiconductor Technology and AI Accelerators is driving the need for specialized hyperscale environments

| 18% | Semiconductor Companies, AI Infrastructure Providers, Cloud Operators | GPU Clusters, AI Accelerators, HPC Infrastructure, Advanced Computing Platforms | Increases demand for power-dense facilities, advanced networking fabrics, and next-generation cooling systems optimized for accelerated computing. |

Rise in expansion of High-Performance Computing (HPC) Workloads, applications rely on high-performance computing environments

| 14% | Scientific Research, Financial Services, Healthcare, Defense, Manufacturing | Simulation & Modeling, Drug Discovery, Financial Analytics, Digital Twins | Expands hyperscale adoption beyond cloud computing by supporting compute-intensive workloads requiring large-scale parallel processing capabilities. |

Rapid growth in AI and Generative AI Workloads is significantly increasing demand for high-density computing infrastructure

The rapid commercialization of AI and Generative AI technology is one of the key factors that is leading to investments in hyperscale datacenter infrastructure. With the increased use of LLMs, Generative AI solutions, AI Copilots, autonomous machines, and machine learning platforms, there is a need for high density data center infrastructures that can support GPU clusters and accelerated computing architecture. The International Energy Agency estimates that worldwide data center electricity usage was at 500 TWh in 2025, which is expected to grow above 1300 TWh in 2035, with AI workload being the main contributor to the additional demand.

Parallel to that, the rise of AI adoption in enterprises and the increase in AI capital expenditures are redefining hyperscale development approaches. The global AI market will be valued at about US$ 4.8 trillion by 2033, according to UNCTAD, indicating the magnitude of infrastructural needs for the future. In addition, leading cloud operators and tech companies are pouring hundreds of billions of dollars into AI data centers, AI accelerators, and high-performance computing clusters. For example, in April 2026, the International Energy Agency (IEA) noted that AI-oriented data centers experienced a 50 percent increase in power usage in 2025, whereas AI-specific facilities have grown three times their capacity in just 18 months. This trend has been fueled by the increasing demand for hyperscale data center capacity for AI and cloud computing applications.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

Constraining Factors Regarding Grid Power Availability and Utility Interconnect Development Timeframes are impacting projects' timelines and limiting hyperscale capacity growth

| 12% | Power Infrastructure & Capacity Expansion | AI Training Clusters, Cloud Regions, Hyperscale Campus Development | Delays facility commissioning, restricts AI-driven capacity additions, and shifts investments toward regions with stronger grid availability and renewable energy access. |

Limiting Factors Regarding Water Consumption and Advanced Cooling Infrastructure

| 7% | Thermal Management & Sustainability Compliance | High-Density AI Computing, GPU Clusters, HPC Workloads | Increases operational complexity and infrastructure costs while accelerating adoption of liquid cooling, immersion cooling, and water-efficient datacenter designs. |

Challenges With Critical Component Supply Chains, the hyperscale sector experiences difficulties

| 8% | Server Deployment, Networking Expansion, AI Accelerator Integration | Extends project lead times and capital expenditure due to shortages of transformers, switchgear, generators, cooling systems, optical networking equipment, and AI hardware. | |

Regulatory Complexities Associated With Data Sovereignty, the growth of data sovereignty regulations as well as cybersecurity regulations poses certain complexities to hyperscale’s

| 6% | Regulatory Compliance & Geographic Expansion | Sovereign Cloud, Cross-Border Data Processing, Government Cloud Services | Requires region-specific infrastructure investments, increases compliance costs, and influences hyperscale site-selection and regional expansion strategies. |

Limiting Factors Regarding Water Consumption and Advanced Cooling Infrastructure

One of the most significant challenges limiting the growth of the hyperscale datacenter industry is the rising strain related to water use and installation of cooling technology. The fast proliferation of technologies like artificial intelligence and high-performance computing and even more so GPU-heavy workloads have led to denser rack power densities and thus created unprecedented demands for cooling in hyperscale datacenters, especially those powered by AI-based computing clusters, which have much higher thermal densities than other cloud workloads. In response to these growing demands, hyperscale operators need to deploy advanced liquid cooling solutions, chilled water, and massive cooling capabilities.

Also, water availability has become one of the most important considerations in selecting sites for hyperscale deployments. Industry figures have shown that a hyperscale data center may require up to millions of gallons of water each year for cooling purposes, especially in locations where evaporative cooling techniques are employed. Such cooling techniques increase complexities and costs associated with projects along with deployment delays. For example, in 2026, a United Nations-supported report highlighted the increasing environmental and resource stress caused by the exponential growth of AI data centers. It was estimated that by 2030, the world’s data centers would use up to 9.3 trillion liters of water, cover an area of 14,500 square kilometers, and produce up to 2.5 million metric tons of electronic waste.

Segmentation Analysis

The global hyperscale datacenter market is segmented based on type, component, power capacity, end user, deployment type and region.

Large-Scale Greenfield Developments Supporting the Expansion of AI-Ready Hyperscale Infrastructure

The Greenfield segment remains dominant in the deployment scenario of the Hyperscale Datacenters Market because of the increasing demand for purpose-built facilities that can accommodate next-generation computing, including cloud computing, artificial intelligence, and high-performance computing applications. The flexibility that greenfield sites allow in the design of the power distribution architecture, site selection, cooling systems, and connectivity cannot be achieved by brownfield sites. As estimated by market players, greenfield sites will be responsible for about 74.5% of all the capacity additions in global hyperscale datacenters in 2025.

Hyperscale campuses launched in 2025 and 2026 are likely to have capacities higher than 100 MW each, and several campuses have the potential for megawatts worth of power capacity expansion over the years. The capital expenditure on datacenters globally is forecasted to cross US$ 400 billion in 2025, out of which a substantial amount will be allocated to the greenfield hyperscale data centers, AI-ready power solutions, cooling systems, and renewable energy sources. The potential to build a facility of custom design that has scalable power availability, high-speed connectivity, and expansion potential makes it the most profitable model of the market.

Geographical Penetration

Massive AI Infrastructure Investments and Multi-Gigawatt Campus Development Strengthening North America's Leadership

North America region is dominating the hyperscale datacenters market, which is attributed to its presence of the top hyperscale cloud service providers, advanced digital connectivity infrastructure, and heavy investments in artificial intelligence computational capabilities. The region enjoys the presence of top hyperscale players such as Amazon Web Services (AWS), Microsoft, Google, Meta, and Oracle, who keep on building more data centers in the United States and Canada. By 2025, North America was generating about 42.9% of the world’s hyperscale data center revenues, driven by the rapid installation of AI training clusters, cloud computing services, and high-performance computing facilities.

Growing commercialization of generative AI has only helped strengthen the dominance of the region even more. During 2025-2026, leading technology firms declared investment plans that totaled US$ 300 billion in AI-related infrastructure, hyperscale campuses, high-speed networks, and future data center facilities in North America. Some of the recently planned facilities have a capacity greater than 100 MW while multi-gigawatt scale campuses are becoming a norm in places like Virginia, Texas, Arizona, and Ohio. For instance, in September 2025, Energy Capital Partners (ECP) and KKR, two US-based investment companies, that they have embarked on the construction of a hyperscale data center campus in Texas. The hyperscale data center project aims to deliver massive power generation and digital infrastructure for cloud computing services, AI operations, and high-performance computing applications.

U.S. Hyperscale Datacenters Market Trends

The United States is the leading market in terms of the global Hyperscale Datacenters Market owing to the presence of a high concentration of hyperscale cloud service providers, state-of-the-art digital infrastructure, and extensive investments in AI computation infrastructure. The United States has the world's biggest hyperscale ecosystem with companies like AWS, Microsoft, Google, Meta, Oracle, and a number of colocation service providers taking part in it. As per industry reports, in 2025, the United States has held more than 55% share of the total hyperscale datacenter capacity in North America and was leading in the share of global hyperscale installations. Northern Virginia, Texas, Arizona, Ohio, and Oregon data centers continue to be heavily invested in due to fiber optic connections, power supply systems, and closeness to the major cloud and enterprise customers.

For instance, in 2025, Apollo Funds, a U.S.-based private equity firm, has successfully acquired Stream Data Centers, a developer and operator of hyperscale data center campuses. This acquisition was made with the aim of enhancing Apollo’s portfolio in terms of digital infrastructure and taking advantage of increased demands for hyperscale facilities due to cloud computing, AI, and HPC.

Canada Hyperscale Datacenters Market Outlook

Canada is shaping up as an increasingly strategic market within the Hyperscale Datacenters sector owing to the presence of an abundance of renewable energy sources, good climate for energy-efficient cooling of IT infrastructure, advanced digital network infrastructure, and investment by international hyperscalers. Leading cloud computing companies such as Amazon Web Services, Microsoft, Google, and Oracle are expanding their presence in Canada to meet the rising needs of cloud computing and artificial intelligence solutions. Low-cost access to renewable sources of electricity such as hydroelectricity has helped Canada become a suitable location for hyperscaler expansion. In the period between 2025 and 2026, provinces like Ontario, Quebec, and Alberta have seen rising hyperscaler investments.

For example, in the year 2025, CPP Investments, which is a Canada-based investment organization, announced an investment of $225 million in the construction of the Ontario Data Centre. This investment will be done to construct digital infrastructure that can satisfy increasing demands by the cloud computing and artificial intelligence sectors.

Hyperscale Datacenters Market Competitive Landscape

- Characteristically, there are three main groups of players involved in the Hyperscale Datacenters Market. They include the hyperscale cloud service providers, wholesale and colocation infrastructure providers, and hyperscale campus developers. The key players among the first group of companies include Amazon Web Services (AWS), Microsoft, Google, Meta Platforms, Oracle Corporation, Alibaba Group, Tencent Holdings, and IBM due to their huge investments in AI computing, cloud computing infrastructure, and dense data centers. Digital Realty Trust, Equinix, NTT Ltd., and CyrusOne represent the second group of players who provide the necessary infrastructure for hyperscale computing through the provision of colocation facilities, interconnections, and carrier-neutral ecosystems. In the third category are QTS Realty Trust, Vantage Data Centers, and STACK Infrastructure who are into the development of large-scale AI-ready campuses and high-density data center facilities to meet growing hyperscale demands. According to Synergy Group, the global total of hyperscale data centers among the biggest operators of the world reached more than 1,100 hyperscale data centers in the year 2025. The cloud service providers hold almost 68.9% share of global infrastructure demands in terms of hyperscale.

- Key Players include AWS, Microsoft, Google, Meta Platforms, Oracle Corporation, Alibaba Group, Tencent Holdings, IBM, Digital Realty Trust, Equinix, NTT Limited, CyrusOne, QTS Realty Trust, Vantage Data Centers, and STACK Infrastructure.

Key Developments

- March 2026: La Caisse committed CAD 240 million towards the development of Cologix’s AI-ready MTL8 data center located in Montréal, Canada. This was intended to help increase the density of the data center infrastructure that could support AI, cloud computing, and HPC loads amid increasing demand for hyperscale-class data center facilities in North America.

- April 2025: Hypertec Cloud acquired 5C Data Centers, which gave rise to the creation of 5C Group. This became one of the biggest AI digital infrastructure service companies in North America, as it leveraged massive data center infrastructure together with cloud and AI computation to cater to the increasing demand for artificial intelligence (AI), cloud computing, and HPC services.

- June 2026: The CPP Investments, a globally oriented Canadian investment firm, entered into a partnership with the CtrlS, an Indian data center company, in order to help in developing the large data centers in India. This partnership was entered into due to the need for meeting the demands of the growing needs of cloud computing, artificial intelligence (AI), and high-performance computing (HPC).

- September 2025: Cologix, a network-neutral interconnection and data centre company operating in North America, made further investments in Toronto by acquiring CIM Group’s stake in the TOR4 Data Centre and the 105 Clegg property. This acquisition was carried out to enhance the capability of digital infrastructure and cater to the increasing requirements of cloud connectivity, artificial intelligence (AI), and HPC.

- January 2026: LightHouse Data Centers and Wharton Digital have launched their hyperscale data center platform strategy, which has been designed keeping in mind a development pipeline that will exceed 2 GW of capacity in North America.

- July 2025: Pennsylvania Data Center Partners and PowerHouse Data Centers have formed a partnership to build a 1.35 GW hyperscale data center campus located in Carlisle, Pennsylvania.

- April 2026: AirTrunk, which is a hyperscale data center provider in the Asia-Pacific region, acquired Lumina CloudInfra in order to increase its capabilities in digital infrastructure and to hasten its expansion into hyperscale data center capabilities in the regions that matter.

Key Procurement Priorities and Buyer Evaluation Criteria

- Organizations that are placing their bets on the Hyperscale Datacenters Market, there is an ever-increasing need for vendors who can provide computing facilities that are highly scalable, ready to be used with AI applications, and with a high degree of computational density along with dependable energy provision and low-latency network connectivity.

- The process of procurement decision-making is increasingly impacted by the rapid emergence of generative AI, LLMs, cloud native, HPC, and big data-intensive applications. The consequence of this is that the buyers are now preferring the infrastructure vendors who are capable of delivering GPU-dense, liquid cooling, renewable energy use, and multigigawatt scale-up services with high availability.

- These include issues related to power sourcing, power purchasing strategy, network interconnection density, infrastructure scalability, energy efficiency, sustainability, cooling capabilities, uptime, security, and even data sovereignty compliance. The capability of delivering long-term power purchasing and high-density AI workloads has become a significant factor that distinguishes the vendors from each other.

- The buyer is very keen on the knowledge of building hyper-scale facilities, AI-based data center architecture, innovative thermal management technologies, use of renewable energy, disaster recovery features, and worldwide experience when choosing partners for infrastructure.

Why Choose DataM?

- Technological Innovations: Explores advancements in Hyperscale Datacenters Market including high-density RDL, panel-level packaging, and heterogeneous integration, enabling improved performance, reduced power consumption, and smaller form factors for AI, 5G, and high-performance computing applications.

- Product Performance & Market Positioning: Evaluates how different players deliver packaging solutions based on I/O density, thermal performance, miniaturization, and cost efficiency, highlighting how leading companies differentiate through advanced integration and scalability across consumer electronics and automotive applications.

- Real-World Evidence: Highlights adoption of FOWLP in smartphones, wearables, automotive electronics, and AI chips, demonstrating benefits such as enhanced processing speed, reduced footprint, improved energy efficiency, and optimized system-level performance.

- Market Updates & Industry Changes: Tracks key developments such as capacity expansions, new packaging platforms, panel-level innovations, and regional semiconductor investments across Asia-Pacific, North America, and Europe, supporting the shift toward advanced packaging ecosystems.

- Competitive Strategies: Analyzes how leading companies expand through capacity scaling, technology innovation, strategic partnerships, and integration of advanced packaging with chip design to address rising demand from AI and high-performance computing markets.

- Pricing & Market Access: Explains pricing variations based on complexity, wafer size, and integration level, along with access through OSAT providers, foundries, and integrated device manufacturers supporting global supply chains.

- Market Entry & Expansion: Identifies growth opportunities driven by AI, 5G, automotive electronics, and data centers, while outlining strategies such as regional capacity expansion, technology differentiation, and ecosystem partnerships to scale globally.

Target Audience

- Hyperscale Cloud Service Providers

- Public Cloud Infrastructure Operators

- Colocation Data Center Providers

- Data Center Developers and Investors

- Artificial Intelligence (AI) Infrastructure Providers

- High-Performance Computing (HPC) Organizations

- Enterprise IT and Digital Transformation Leaders