hy functional beverages are becoming the front line of innovation

Functional beverages are moving from a niche wellness shelf into the center of beverage product development. Consumers are expanding their expectations beyond refreshment. They are looking for products that can support hydration, digestion, clean energy, immunity, recovery, focus and daily wellness. This shift is turning every bottle, can and ready to drink format into a claim platform where ingredients, taste, convenience and credibility decide market success.

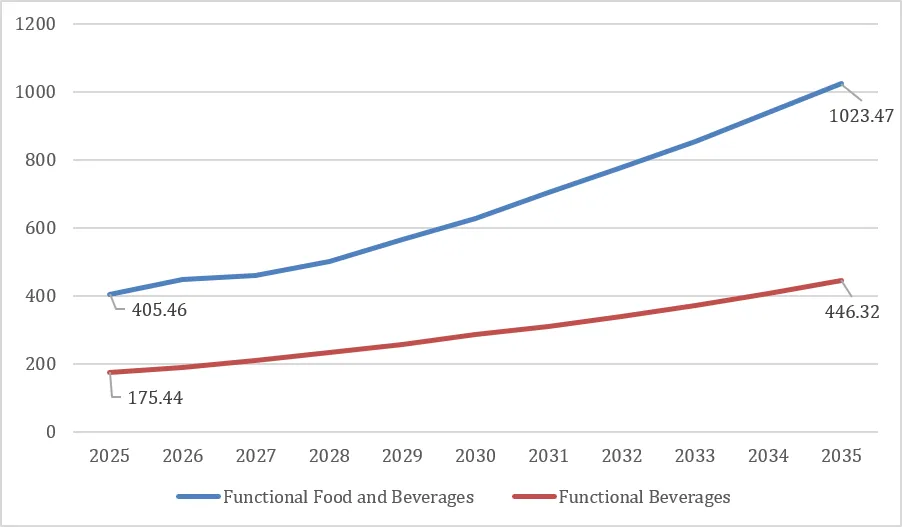

The scale of the opportunity explains why the category has become so competitive. DataM Intelligence estimates that the functional food and beverage market reached US$ 405.46 billion in 2025 and is expected to reach US$ 1023.47 billion by 2033, growing at 11.09% during 2026 to 2035. Within beverages, DataM Intelligence also reports that the functional beverages market reached US$ 175.44 billion in 2025 and is expected to reach US$ 446.32 billion by 2035. This is creating pressure on beverage companies to move faster from flavor extensions toward benefit-led product architecture.

For a full category baseline, explore the DataM Intelligence Functional Food and Beverage Market report and the Functional Beverages Market report.

Chart 1. Functional food and beverage market growth shows why brands are prioritizing wellness led beverage portfolios.

The battleground is shifting from refreshment to specific consumer outcomes

The functional beverage market is being shaped by a simple commercial reality. Consumers want specific benefits without adding complexity to daily routines. A drink is easier to adopt than a capsule, powder or supplement stack because it fits into existing occasions such as morning energy, commute hydration, post workout recovery and evening relaxation. This gives beverage companies a strong route to convert wellness demand into repeat consumption.

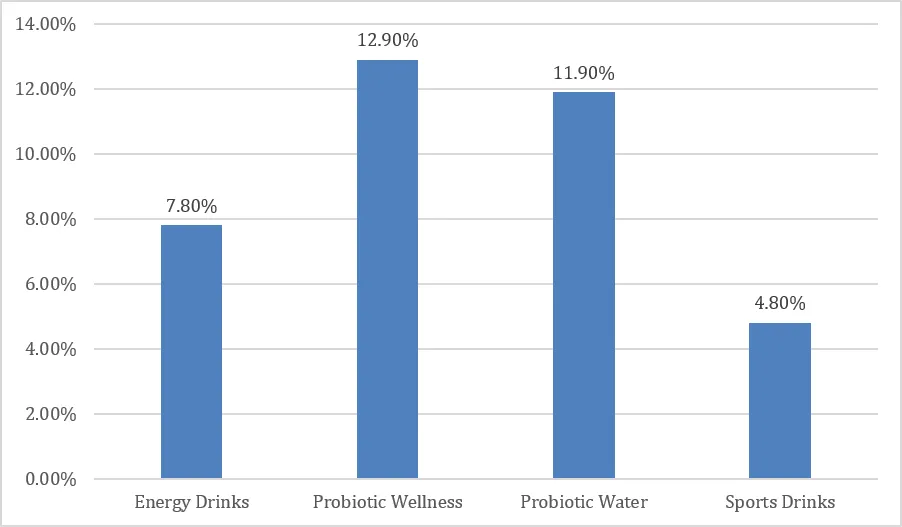

Gut health has become one of the strongest entry points. Probiotic drinks, prebiotic sodas, kombucha style beverages and fiber added sparkling drinks are gaining momentum because digestive health now connects to immunity, skin wellness, energy and mood in consumer perception. DataM Intelligence estimates that the probiotic wellness drinks market is valued at about US$ 1.04 billion in 2025 and is projected to reach US$ 3.09 billion by 2035, growing at 12.9% during 2026 to 2035.

Hydration is becoming a broader lifestyle category. Sports drinks were historically built around athletic performance. Hydration brands are now targeting office workers, frequent travelers, outdoor consumers and everyday wellness users. Recent market coverage notes that daily use buyers form a large share of sports drink consumption, while major beverage companies are repositioning hydration around science backed electrolyte formulas. This shift is expanding the addressable market for electrolyte drinks, functional water and sugar reduced hydration formats.

For companies tracking hydration led innovation, the DataM Intelligence Functional Water Market report and the Electrolyte Drinks Market report provide relevant demand and channel analysis.

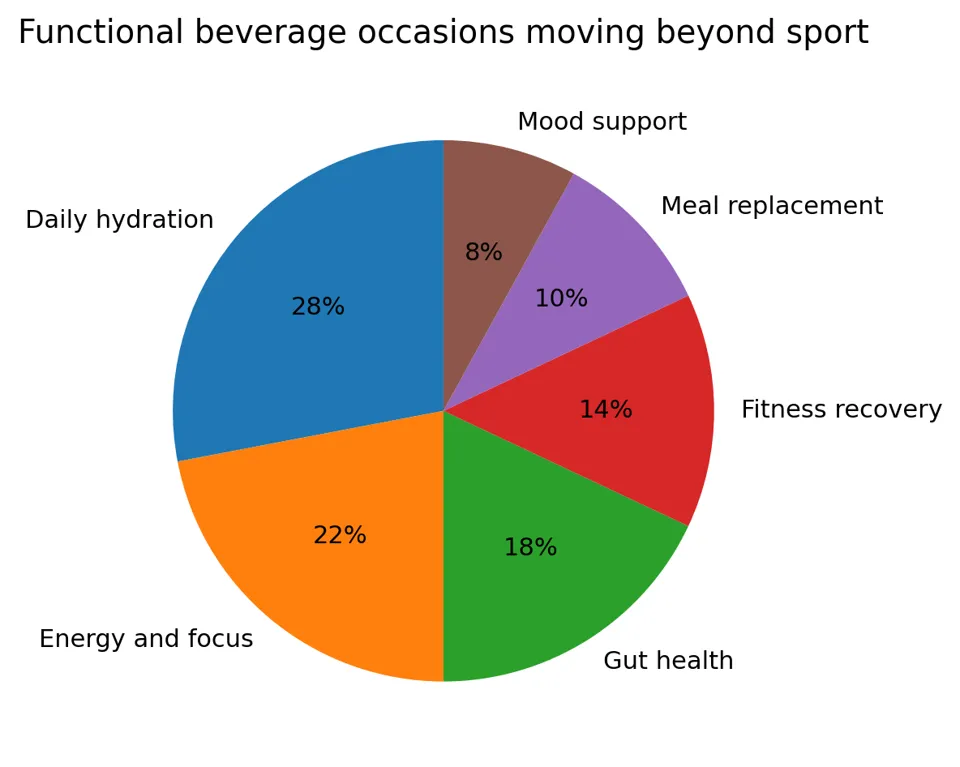

Chart 2. Functional beverage occasions are expanding beyond sport into everyday wellness routines.

Energy drinks are being rebuilt around cleaner stimulation

Energy is another major innovation arena. Traditional energy drinks built the category around caffeine, sugar and performance cues. The next wave is moving toward natural caffeine, yerba mate, matcha, B vitamins, adaptogens and nootropics. Consumers still want alertness and focus, but more buyers are looking for smoother energy, lower sugar and cleaner ingredient labels.

This creates a product development challenge. Brands need enough functional intensity to be credible, but they must also manage taste, aftertaste, regulatory claims and price points. Energy beverage innovation is therefore moving toward layered formulations where caffeine is combined with ingredients positioned for focus, mood or endurance. DataM Intelligence estimates that the global energy drinks market reached US$ 98.5 billion in 2025 and is projected to reach US$ 174.8 billion by 2033, growing at 7.8% during 2026 to 2033.

To evaluate the category and ingredient opportunity, review the DataM Intelligence Energy Drinks Market report and the Natural Caffeine Market report.

Functional Beverage Category Growth Signals

Chart 3. Gut health and hydration categories show strong growth signals alongside energy and sports drink demand.

Product teams are competing on claims, texture and formulation credibility

Functional beverages are difficult to build because the product must perform on multiple fronts. A beverage needs a clear claim, a familiar taste profile, stable ingredients, attractive packaging and the right retail price. Product teams also need to avoid overloading formulas with too many benefits because broad wellness language can reduce trust. The strongest launches are likely to focus on one primary benefit, then support it with one secondary benefit that fits the usage occasion.

Protein beverages show this clearly. Ready to drink protein is gaining traction because consumers want convenient satiety, muscle support and meal replacement options. However, brands must manage mouthfeel, sweetness, shelf stability and ingredient cost. A protein drink can win if it tastes like a mainstream beverage, while still offering nutritional value that feels measurable and credible.

Mood and focus beverages face a different challenge. Adaptogens, magnesium, L theanine and botanical ingredients can support differentiated positioning, but they require careful claims management. The opportunity is strong, especially among younger consumers seeking stress support and mental clarity, but the winning products will need transparent dosing, regulatory discipline and repeatable sensory quality.

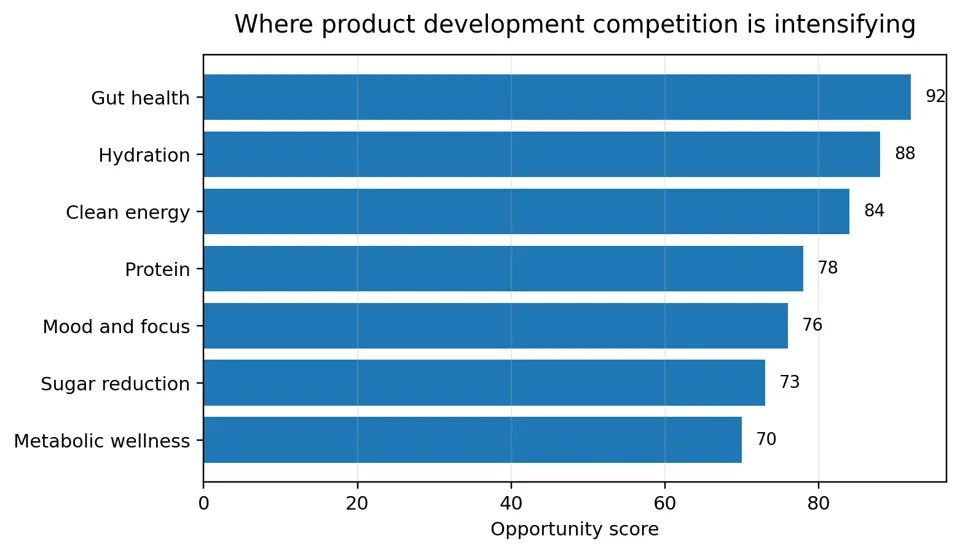

Chart 4. Gut health, hydration and clean energy are among the most competitive product development arenas.

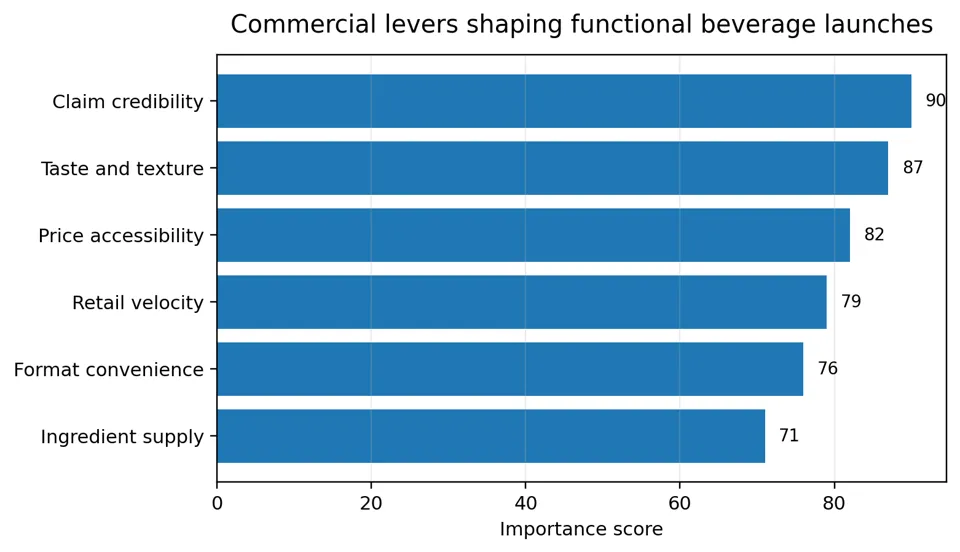

Retailers and distributors are rewarding velocity and clear wellness proof

Functional beverage success depends on more than product concept. Retailers want proof that a product can move quickly, drive repeat purchase and justify shelf space. This gives an advantage to products that connect a clear benefit to a familiar usage moment. Hydration after travel, energy before work, gut health after meals and protein after exercise are easier to understand than vague wellness claims.

The retail battleground is also changing because functional beverage products now compete across convenience stores, supermarkets, gyms, pharmacies, ecommerce and foodservice. Each channel has different pack size, pricing and messaging needs. Convenience stores favor impulse and energy use cases. Pharmacies favor digestive health and clinical credibility. Ecommerce favors education, subscriptions and bundled wellness routines.

The strongest companies are likely to use channel specific launch strategies. A probiotic sparkling drink may use grocery and ecommerce to educate buyers, while an electrolyte drink may use convenience and fitness channels to drive repeat occasions. A protein beverage may require both grocery availability and gym adjacency to reinforce the product use case.

Chart 5. Functional beverage launches need credible claims, strong taste and channel specific commercial execution.

Sugar reduction and GLP 1 behavior are influencing the next formulation cycle

Sugar reduction is becoming a critical formulation theme. Consumers want functional benefits, but they are increasingly sensitive to calories, sweeteners and metabolic health. This is pushing brands toward low sugar hydration, zero sugar energy, fiber enriched sodas and lightly sweetened probiotic drinks. The growth of GLP 1 use is also changing expectations around portion control, satiety and nutrient density, which can support demand for protein, fiber and hydration led beverages.

Indulgence is evolving toward products with a stronger reason to exist. Flavor remains essential because repeat purchase still depends on taste. The next innovation cycle will therefore reward products that can combine enjoyable sensory profiles with credible function, moderate sweetness and a benefit consumers can explain in one sentence.

Ingredient suppliers could become major beneficiaries

The functional beverage battleground creates opportunities beyond finished beverage brands. Ingredient suppliers, formulation houses, packaging companies and contract manufacturers all stand to benefit. Demand is rising for probiotic strains, prebiotic fibers, natural caffeine, electrolytes, plant proteins, botanicals, flavors, clean label sweeteners and stabilizers that can survive processing and shelf life requirements.

Suppliers with beverage application expertise are likely to capture higher value because many functional ingredients behave differently in liquid systems. Stability, solubility, taste masking and heat tolerance are practical barriers. Brands need partners that can shorten development timelines and reduce failed launches. This makes formulation know how as important as ingredient supply.

What the next wave of functional beverage winners will look like

The next winners in functional beverages will be the companies that make benefits easy to understand, easy to trust and easy to repeat. The strongest concepts will connect a specific function to a specific occasion. Hydration for daily energy, probiotics for digestive balance, protein for satiety and natural caffeine for clean focus are clearer than general wellness claims.

Large beverage companies will continue using scale, distribution and marketing to defend their positions. Challenger brands will compete through sharper benefit claims, community building and faster product iteration. Retailers will increasingly decide which concepts survive based on velocity, basket expansion and margin quality. For investors, the opportunity is broad, but the most attractive targets are likely to have strong repeat purchase, defensible formulation capability and a clear route from niche health trend to mainstream consumption.