Natural Caffeine Market Size & Share

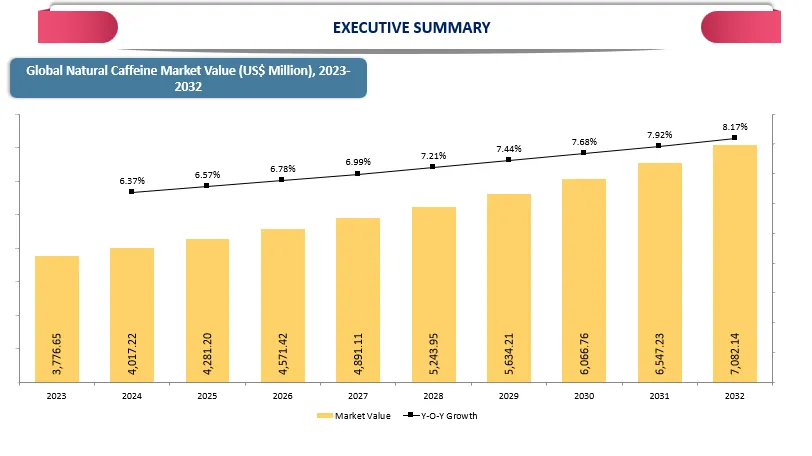

Global Natural Caffeine Market reached US$ 4,281.20 million in 2025 and is expected to reach US$ 7,082.14 million by 2032, growing with a CAGR of 7.5% during the forecast period 2026-2032.

The natural caffeine market is experiencing steady growth, driven by rising consumer demand for clean-label organic and health-focused products. Natural caffeine, derived from plant-based sources such as coffee beans, tea leaves, guarana and yerba mate, has gained popularity due to its perceived health benefits and safer profile compared to synthetic caffeine. The market is heavily influenced by the booming functional beverage industry, including energy drinks, ready-to-drink teas and fitness-centric beverages, which increasingly incorporate natural caffeine to cater to health-conscious consumers.

Moreover, the growing preference for organic and eco-friendly products has spurred demand for natural caffeine in regions like North America and Europe, where consumers prioritize transparency and ethical sourcing. The Asia-Pacific region, driven by countries like China, Japan and India, is emerging as a significant market due to increasing health awareness and urbanization.

For instance, according to UN-HABITAT, urbanization continues to be a defining megatrend in Asia-Pacific. Fifty-four per cent of the global urban population, more than 2.2 billion people, live in Asia. By 2050, the urban population in Asia is expected to grow by 50% - an additional 1.2 billion people. Additionally, despite challenges like high production costs and competition from synthetic caffeine, the natural caffeine market shows robust potential, fueled by innovations in product development and growing consumer demand for sustainable and health-oriented solutions.

Natural Caffeine Market Scope

| Metrics | Details |

| CAGR | 7.5% |

| Size Available for Years | 2023-2032 |

| Forecast Period | 2026-2032 |

| Data Availability | Value (US$) |

| Segments Covered | Type, Form, Application, Distribution Channel and Region |

| Regions Covered | North America, Europe, Asia-Pacific, South America and Middle East & Africa |

| Fastest Growing Region | North America |

| Largest Region | Asia-Pacific |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth, Demand, Recent Developments, Mergers and Acquisitions, New Product Launches, Growth Strategies, Revenue Analysis, Porter’s Analysis, Pricing Analysis, Regulatory Analysis, Supply-Chain Analysis and Other key Insights. |

Natural Caffeine Market Dynamics

Rising Popularity of Clean Label Products

The rising popularity of clean label products is a major driver for the natural caffeine market as consumers increasingly prioritize transparency and natural ingredients in their purchases. Clean label products emphasize minimal processing, no artificial additives and clear ingredient sourcing, aligning perfectly with the attributes of natural caffeine. Thus, rise of clean-labels helps to boost the market growth.

For instance, in 2024, consumers demand more clean-label products those with natural ingredients and fewer additives as they perceive them to be better for their health. Most (83%) shoppers are knowledgeable about clean-label products or have heard the term, according to a survey of more than 1,200 US consumers from earlier this year conducted by The Acosta Group.

Additionally, this trend has spurred innovations in the beverage and snack industries, where manufacturers prominently highlight "naturally sourced caffeine" to cater to this growing demand. For instance, energy drinks like Runa and Guayaki Yerba Mate have gained traction for their commitment to clean labels, emphasizing organic and sustainably sourced ingredients.

Similarly, startups producing caffeine-infused waters and teas have found success by marketing their products as free from synthetic additives and artificial sweeteners. This consumer shift toward clean-label preferences has solidified natural caffeine as a key ingredient in a wide range of food and beverage offerings, driving its market expansion.

Expanding Applications in Diverse Industries

Natural caffeine’s versatility is driving its adoption across multiple industries, including beverages, personal care and pharmaceuticals. In the beverage industry, natural caffeine is a critical component of energy drinks and ready-to-drink teas, which are seeing increasing demand.

In the cosmetics industry, natural caffeine is utilized for its antioxidant and anti-inflammatory properties, aiding in skin rejuvenation and reduction of cellulite.

The U.S. National Institutes of Health (NIH) highlights caffeine’s efficacy in enhancing skincare products, leading to increased demand in this sector. Pharmaceuticals are another growing application area. Natural caffeine is included in pain relief and respiratory stimulant formulations, benefiting from its natural origin and minimal side effects. The Indian Ministry of Health and Family Welfare reports a 15% annual growth in the herbal pharmaceuticals market, with natural caffeine being a prominent ingredient.

High Production Costs

High production costs significantly restrain the natural caffeine market by making products derived from natural sources more expensive than those using synthetic caffeine. The extraction of natural caffeine from raw materials like coffee beans, tea leaves, guarana and yerba mate involves labor-intensive processes, sustainable farming practices and certifications such as organic or fair-trade. These factors drive up the cost of natural caffeine, which is typically priced between US$ 25 to US$ 35 per kilogram, compared to synthetic caffeine, which costs around US$ 10 to US$ 15 per kilogram.

This cost disparity makes it challenging for manufacturers to price natural caffeine-based products competitively, particularly in price-sensitive markets. For instance, natural caffeine energy drinks such as Guayaki Yerba Mate retail at a premium of US$ 3–US$ 4 per bottle, while mainstream synthetic caffeine-based energy drinks like Monster Energy or Red Bull are priced around US$ 2–US$ 3 per can. Similarly organic green coffee bean extracts used in natural caffeine supplements are significantly costlier due to the need for sustainable sourcing.

The higher costs often lead to limited adoption of natural caffeine-based products, especially in emerging markets where affordability is a major concern. Thus, high production costs pose a significant barrier to the growth of the natural caffeine market by creating a substantial price gap between natural and synthetic caffeine. This cost disparity, driven by labor-intensive extraction processes, sustainable farming practices and certification requirements, limits the affordability and accessibility of natural caffeine-based products, particularly in emerging markets.

Natural Caffeine Market Trends

The growing trend of health consciousness is transforming consumer preferences in the beverage and nutrition markets. More people are seeking products that provide energy, focus, and wellness benefits naturally, avoiding synthetic additives and sugar-laden alternatives. This shift positions natural caffeine as a key ingredient for brands targeting health-conscious lifestyles. As consumers integrate wellness into daily routines, demand for functional, clean-label products continues to rise.

Natural caffeine sources like green tea, guarana, and yerba mate are increasingly used in energy drinks, supplements, and functional beverages. These ingredients provide balanced stimulation and mental clarity without the negative side effects of synthetic caffeine. Combining caffeine with complementary ingredients like L-Theanine allows brands to offer enhanced focus and sustained energy. This aligns perfectly with consumers’ desire for health-conscious, functional solutions that support overall well-being.Real-world examples like KEY, an all-natural, sugar-free energy drink with 80 mg of natural caffeine from green tea, demonstrate this trend. By expanding to over 420 Sprouts Farmers Market stores nationwide, KEY targets health-conscious consumers seeking sustained energy without jitters. Its formulation, combining caffeine with L-Theanine, positions it as a functional, wellness-focused beverage. Such success stories illustrate the potential for natural caffeine products to capture market share by leveraging health-conscious consumer behavior.Market Segment Analysis

The global natural caffeine market is segmented based on by type, by form, by application, by distribution channel and by region.

Rising Adoption of Natural Caffeine in Food & Baverages

The food and beverages segment dominates the natural caffeine market, primarily due to its widespread use in energy drinks, ready-to-drink teas, coffee and functional beverages. Consumers increasingly prefer beverages that provide a natural energy boost, aligning with the global trend toward clean-label and health-conscious products.

Energy drinks and sports beverages, in particular, rely heavily on natural caffeine sourced from coffee beans, guarana and green tea to deliver sustained energy and improved performance. For instance, brands like Red Bull Organics and Guayaki Yerba Mate have captured significant market share by promoting their use of naturally sourced caffeine.

Additionally, the growing popularity of cold brew coffee and green tea-based drinks has further propelled the demand for natural caffeine in this segment. Companies like Starbucks have expanded their offerings with natural caffeine-infused beverages, such as cold brew with guarana or green coffee extract, to cater to health-conscious millennials and Gen Z consumers.

The inclusion of natural caffeine in functional foods like protein bars and caffeinated snacks is also rising, offering consumers convenient energy solutions beyond traditional drinks. This strong consumer preference for natural, functional and clean-label food and beverage options ensures the segment's continued dominance in the natural caffeine market.Top of Form

Market Geographical Share

North America Natural Caffeine Market

In North America, the natural caffeine market is primarily driven by the US, Canada, and Mexico, where consumption of coffee and caffeinated beverages is significant. In the US, the FDA regulates caffeine-containing products, while the National Coffee Association (NCAUSA) provides industry guidance and USDA statistics track production and imports. The North American natural caffeine landscape presents a mature, yet dynamically evolving marketplace characterized by sophisticated consumer behavior and regulatory frameworks that distinguish it as a global benchmark for caffeine consumption patterns. This market demonstrates remarkable population-level penetration, with approximately 69% of the US population consuming at least one caffeinated beverage daily.Demographically, caffeine consumption peaks among consumers aged 50-64 years at 246 milligrams daily, while the youngest cohort children aged 2-5 years consuming 42 milligrams daily establishes habitual patterns from early developmental stages. This high engagement is further evidenced by North America recording the highest average annual caffeine-containing beverage volume sales per capita at 348 liters, substantially exceeding other global regions.This volumetric leadership translates into 89% of the adult US population consuming caffeine with equal prevalence between men and women; however, gender-differentiated patterns emerge at higher intake levels, where men consume 240 milligrams daily versus 183 milligrams for women among regular consumers. The category is dominated by coffee, which represents 69% of total caffeine intake across all US age groups, followed by carbonated soft drinks at 15.4% and tea at 8.8%Europe Natural Caffeine Market

European natural caffeine market was valued at US$ 1,280.29 million in 2024 and is estimated to reach US$ 2,196.43 million by 2032, growing at a CAGR of 7.1% during the forecast period from 2026-2032.In Europe, the natural caffeine market is governed by a highly structured and harmonized regulatory framework led by the European Food Safety Authority (EFSA) and the European Commission. EFSA evaluates the safety of caffeine intake and provides scientific opinions that shape regulations for foods, beverages, and supplements.The European natural caffeine market is a sophisticated and growing ecosystem, anchored by the rigorous standards of the European Food Safety Authority (EFSA). Since its foundational 2015 scientific opinion, the market has operated under a clear regulatory ceiling: habitual consumption of up to 400 milligrams per day is considered safe for healthy adults, while a 200-milligram threshold is maintained for pregnant women and acute single doses. This evidence-based structure derived from 39 surveys across 22 countries establishes 3 milligrams per kilogram of body weight as a conservative safety threshold, providing a predictable environment for ingredient developers targeting everyone from children to the elderly.While the average European adult consumes between 37 and 319 milligrams of caffeine daily, the sources of this intake reveal a continent divided by tradition. Coffee dominates the mainland, contributing between 40% and 94% of adult caffeine intake. However, a "Tea Belt" exists in Ireland and the United Kingdom, where tea accounts for 59% and 57% of intake respectively. Currently, Europe records 200 liters per capita in annual caffeine-containing beverage sales. While this trails North America’s 348 liters, it significantly outpaces the Asia-Pacific region’s 126 liters, signaling a mature market that still possesses significant headroom for growth in novel delivery formats.Major Global Players

The major global players in the market include SHRI AHIMSA NATURALS LIMITED, Applied Food Sciences (AFS), Botanic Healthcare, Natura Vitalis, Prinova Group LLC, Nutriventia, UL LLC, Herbochem, Cerata Pharmaceuticals LLP and Stabilimento.

Natural Caffeine Market Sustainability Analysis

Sustainability is a critical focus in the natural caffeine market, with increasing efforts to minimize the environmental impact of production and packaging. Companies are adopting organic farming practices and reducing reliance on synthetic fertilizers, aligning with the United Nations’ Sustainable Development Goals (SDGs).

Additionally, the use of biodegradable packaging for natural caffeine products is gaining momentum. According to the Global Sustainability Council (GSC), sustainable packaging solutions in the beverage industry could reduce waste by 25% annually. Leading brands are also investing in carbon-neutral manufacturing processes, ensuring minimal environmental footprint and enhanced consumer appeal.

Consumer Behaviour Analysis

Consumers in the global natural caffeine market are increasingly prioritizing clean-label products. Clean labels refer to products that have simple, recognizable ingredients with no artificial additives, preservatives or unnecessary chemicals. This trend is particularly strong among health-conscious consumers, millennials and Gen Z, who are more informed and discerning about the ingredients in their food and beverages. The consumers seek transparency and trust in the brands they choose, with a preference for functional drinks that contain natural organic and non-GMO ingredients.

The demand for clean-label functional drinks is driven by a growing awareness of the potential negative impacts of synthetic chemicals, artificial sweeteners and preservatives on health. Consumers are particularly focused on health benefits like immune support, hydration, energy and mental clarity, but they expect these benefits to come from natural sources like fruits, vegetables, plant extracts and natural sweeteners like stevia or honey.

Emerging Market Players and Strategic Initiatives

Emerging players in the natural caffeine market are adopting innovative strategies to capture market share and meet the growing demand for clean-label organic and health-conscious products. The companies are focusing on sustainability, transparency and product differentiation to appeal to a broader consumer base. One key strategy involves sourcing caffeine from diverse, sustainable plant-based origins like guarana, green coffee and yerba mate, ensuring high quality while supporting environmental sustainability.

For example, Runa, a brand offering guarana-based beverages, emphasizes its commitment to sustainability by sourcing guarana from indigenous communities in the Amazon Rainforest, promoting both fair trade and environmental preservation. Emerging players are also leveraging digital platforms and social media to engage with consumers, particularly Millennials and Gen Z, who seek transparency in ingredients and sustainability practices.

By Type

- Coffee

- Tea

- Cocoa

- Guarana

- Others

By Form

- Powder

- Liquid

- Capsules and Tablets

By Application

- Food and Beverages

- Pharmaceuticals

- Personal Care and Cosmetics

- Others

By Distribution Channel

- Online

- Offline

By Region

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

Key Developments

- March 2026: DSM-Firmenich unveiled a new natural caffeine extract platform derived from green coffee beans, integrating microencapsulation technology to enhance stability in functional beverages. This innovation supports clean-label energy formulations for global markets.

- January 2026: RYZE Coffee expanded internationally with its mushroom-infused natural caffeine beverages, debuting in Europe and Asia. The launch emphasized adaptogenic blends and sustainable sourcing, marking a milestone in functional beverage innovation.

- November 2025: Applied Food Sciences introduced a patented water-soluble natural caffeine ingredient for sports drinks, improving bioavailability and taste neutrality. This advancement enables broader applications in hydration and endurance products.

Why Purchase the Report?

- To visualize the global natural caffeine market segmentation based on type, form, application, distribution channel and region, as well as understand key commercial assets and players.

- Identify commercial opportunities by analyzing trends and co-development.

- Excel data sheet with numerous data points of the natural caffeine market with all segments.

- PDF report consists of a comprehensive analysis after exhaustive qualitative interviews and an in-depth study.

- Product mapping available as excel consisting of key products of all the major players.

The global natural caffeine market report would provide approximately 70 tables, 64 figures and 201 pages.

Target Audience 2026

- Manufacturers/ Buyers

- Industry Investors/Investment Bankers

- Research Professionals

- Emerging Companies