Battery Chemicals vs Battery Components: Why the Distinction Matters in 2026

Battery chemicals and battery components are often discussed together, but they represent different opportunity pools.

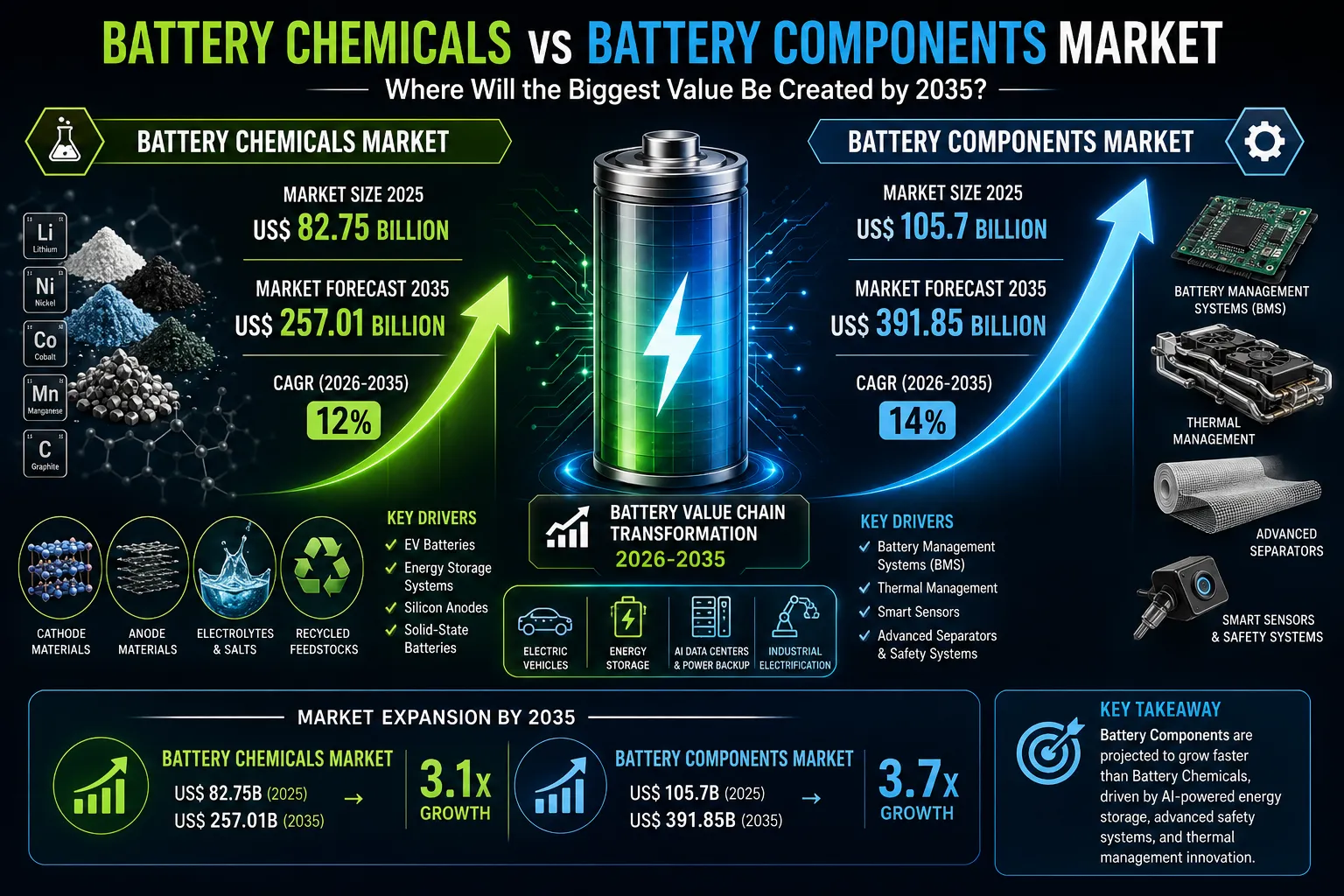

Battery chemicals include cathode materials, anode materials, electrolytes, salts, binders, conductive additives, silicon materials, lithium compounds, graphite, manganese, nickel, cobalt, and recycled feedstocks. These inputs determine energy density, cycle life, safety, charging speed, cost structure, and chemistry roadmap.

Battery components include separators, current collectors, battery management systems, thermal management systems, cell packaging, busbars, sensors, insulation materials, safety vents, module structures, pack enclosures, and manufacturing equipment components. These determine how the battery performs in real-world systems.

The difference is important because the strategic logic is changing. Battery chemicals are exposed to raw material volatility, qualification timelines, regional sourcing requirements, and chemistry shifts. Battery components are exposed to platform design, safety regulation, pack architecture, manufacturing automation, and system-level integration.

In 2026, the most attractive opportunities are not simply in “battery materials” or “battery parts.” They are in bottleneck areas that solve performance, localization, safety, or cost problems.

Request Exclusive Sample

- Battery Chemicals Market: https://www.datamintelligence.com/download-sample/battery-chemicals-market

- Battery Components Market: https://www.datamintelligence.com/download-sample/battery-components-market

The Global Battery Market in 2026: From Volume Growth to Supply Chain Strategy

Battery demand is expanding across electric vehicles, grid storage, data centers, industrial electrification, and backup power systems. However, the market is no longer moving in a straight line. Regional policy, capital cost, commodity prices, and end-market demand are creating different growth speeds across geographies.

Electric vehicles remain the largest demand driver, but the sector has become more price-sensitive. Lower-cost chemistries such as lithium iron phosphate are gaining share because they support affordability, safety, and simpler supply chains. Premium vehicle platforms still require higher energy-density chemistries, but mass-market growth increasingly favors cost discipline.

Energy storage is becoming a second major pillar. Grid operators, utilities, renewable energy developers, and large power users are adopting battery storage for peak shaving, renewable integration, frequency response, and reliability. This matters because stationary storage changes the chemistry mix. Energy storage systems do not always require the highest energy density. They prioritize cost, safety, cycle life, thermal stability, and long operating duration.

Data center power demand is also becoming relevant. AI infrastructure is increasing demand for reliable, flexible, and fast-response power systems. This creates new opportunities for stationary batteries, power electronics, thermal components, battery management systems, and sodium-ion or LFP-based storage architectures.

Government incentives are reshaping the competitive map. The United States, Europe, India, China, Japan, South Korea, and Southeast Asia are using industrial policy to localize battery manufacturing and reduce dependence on concentrated supply chains. This is creating opportunities for regional chemical processing, graphite production, recycling, separators, pack components, and energy storage manufacturing.

The market is therefore shifting from “who can build the most capacity?” to “who can build bankable, localized, cost-competitive, and technology-relevant capacity?”

2026 Innovation Landscape: Technologies That Are Moving from Lab to Strategy

Solid-State Batteries: Commercial Reality Is Getting Closer, but Selectively

Solid-state batteries remain one of the most watched technologies because they promise improved safety, higher energy density, and potentially faster charging. The strategic question is no longer whether solid-state batteries are attractive. The real question is where they can scale first.

The 2026 market is showing that solid-state commercialization will likely be selective. Premium mobility, aerospace, defense, robotics, high-performance vehicles, and specialized industrial systems may adopt solid-state technologies before mass-market vehicles. Manufacturing complexity, material interfaces, cost, and durability remain key barriers.

The Suzuki acquisition of Kanadevia’s all-solid-state lithium-ion battery business is a clear signal. It shows that established mobility players are not waiting for technology to become fully commoditized. They are acquiring process knowledge, intellectual property, and development capability early.

Silicon-Rich Anodes: The Near-Term Performance Upgrade

Silicon-rich anode technology is one of the most strategically important battery chemical opportunities in 2026. Silicon can store more lithium than graphite, supporting higher energy density and faster charging. The challenge is expansion during cycling, which can reduce durability.

The market is now moving beyond basic science. Companies are developing silicon oxide materials, silicon-carbon composites, advanced binders, electrolyte additives, and engineered particles to control swelling and improve cycle life.

Monomyth Materials’ acquisition of NanoGraf assets is important because it connects synthetic graphite capability with silicon oxide anode expertise. This reflects a larger trend: the future anode supply chain will not be graphite-only or silicon-only. It will likely be a hybrid performance stack where graphite, silicon, binders, additives, and cell design are optimized together.

Sodium-Ion Batteries: A Supply Chain Diversification Play

Sodium-ion batteries are gaining commercial attention because they reduce dependence on lithium and can support lower-cost applications. They generally have lower energy density than lithium-ion batteries, but that is not a deal-breaker for stationary storage, two-wheelers, light mobility, backup power, and some industrial uses.

The sodium-ion opportunity is less about replacing lithium-ion everywhere and more about expanding the battery market into applications where lithium cost, availability, or safety concerns create limitations.

For battery chemicals, sodium-ion creates demand for alternative cathode materials, hard carbon anodes, sodium salts, and new electrolyte systems. For battery components, it creates opportunities in pack design, thermal systems, BMS calibration, and manufacturing adaptation.

Dry Electrode Manufacturing: Cost and Factory Productivity Matter

Dry electrode manufacturing is becoming a critical production innovation. Traditional electrode manufacturing requires solvent coating, drying, and solvent recovery. These steps consume energy, increase factory footprint, and add cost.

Dry electrode processes can reduce energy consumption, shorten production time, and simplify manufacturing. The strategic value is significant: even modest improvements in yield, energy use, and throughput can reshape battery economics at scale.

This technology matters for both battery chemicals and components. Chemical formulations must work with dry processing, while manufacturing equipment suppliers must redesign coating, calendaring, handling, and inspection systems for new production methods.

AI-Driven Battery Development: From Material Discovery to Quality Control

AI is becoming a practical tool across the battery value chain. It is being used for material screening, electrolyte design, process optimization, defect detection, state-of-health prediction, and recycling sorting.

The Holyvolt acquisition of Wildcat Discovery Technologies reflects this trend. Wildcat’s high-throughput battery materials discovery platform gives Holyvolt a faster pathway from chemistry screening to pilot-scale development. The deal matters because battery innovation is increasingly becoming a data problem as much as a chemistry problem.

Battery companies that combine laboratory capability, pilot production, manufacturing data, and AI-based optimization will have a stronger chance of reducing development cycles.

M&A and Strategic Deals Reshaping the Battery Market

The 2026 deal environment is not random. It reveals where the battery industry believes future value will be created: regional manufacturing, anode materials, recycling, solid-state technology, BESS integration, and upstream lithium access.

Lyten Acquires Northvolt Assets: Europe’s Battery Reset

Lyten completed the acquisition of Northvolt’s Swedish battery assets, including Northvolt Ett and Northvolt Labs, and later moved to acquire the Revolt battery recycling plant. This is one of the most consequential battery transactions of 2026.

The impact is strategic on several levels.

First, it keeps significant European battery manufacturing infrastructure alive after Northvolt’s financial distress. Second, it gives Lyten a pathway to combine lithium-ion production, lithium-sulfur development, R&D infrastructure, and recycling capability. Third, it demonstrates that distressed battery assets can become platforms for new technology strategies rather than simply being written off.

For the future battery supply chain, this transaction highlights a major lesson: manufacturing assets with skilled labor, permitting, infrastructure, and customer relevance remain valuable even when original business models fail.

LG Energy Solution Takes Full Ownership of NextStar Energy

LG Energy Solution’s decision to acquire Stellantis’ 49% stake in NextStar Energy gives LG full control of Canada’s first commercial-scale battery manufacturing facility in Windsor, Ontario.

This deal reflects a wider recalibration in battery joint ventures. As EV demand patterns shift and stationary storage demand grows, battery manufacturers want more flexibility over customer mix, production strategy, and technology deployment.

The implication is important. Battery plants are no longer being designed only around one vehicle platform or one automaker relationship. Facilities must be flexible enough to serve EVs, energy storage systems, and broader electrification demand.

Suzuki Acquires Kanadevia’s Solid-State Battery Business

Suzuki’s acquisition of Kanadevia’s all-solid-state lithium-ion battery business is a technology-driven transaction rather than a capacity-driven one.

The deal gives Suzuki access to solid-state battery technology developed over many years, including dry-process know-how and intellectual property. It signals that solid-state batteries are becoming strategically important enough for automakers and mobility companies to internalize capability.

For the industry, the message is clear: the next battery technology race will not be won only by buying cells. It will be shaped by control over materials, process knowledge, patents, and manufacturability.

Holyvolt Acquires Wildcat Discovery Technologies

Holyvolt’s acquisition of Wildcat Discovery Technologies is a major example of battery innovation moving toward integrated discovery-to-manufacturing platforms.

Wildcat brings high-throughput materials discovery. Holyvolt brings manufacturing ambition around cleaner and more scalable battery production. The strategic value lies in shortening the distance between lab results and commercial production.

This deal matters because the battery industry has historically struggled with the “pilot line gap.” Many promising materials fail because they cannot be manufactured consistently or economically. Combining discovery, data, testing, and pilot-scale capability can reduce that risk.

Monomyth Materials Acquires NanoGraf Assets

Monomyth Materials’ acquisition of substantially all NanoGraf assets is one of the most relevant 2026 deals in the anode materials segment.

NanoGraf’s silicon oxide technology adds a performance layer to Monomyth’s synthetic graphite platform. This strengthens the case for domestic anode supply chains and reduces reliance on imported active anode materials.

The broader impact is that anode strategy is becoming more sophisticated. Future supply chains will need both volume graphite production and advanced silicon-enhanced materials. Companies that can integrate both may become more attractive to cell manufacturers seeking higher energy density and regional supply security.

Huayou Cobalt Moves to Acquire Atlantic Lithium

Zhejiang Huayou Cobalt’s proposed acquisition of Atlantic Lithium is a clear upstream battery chemicals move. The deal centers on the Ewoyaa lithium project in Ghana and reflects the continuing importance of hard-rock lithium assets despite weaker lithium prices in recent years.

This transaction shows that strategic buyers are still willing to acquire upstream assets when they support long-term feedstock security. It also reinforces Africa’s growing role in global battery mineral supply chains.

The implication for battery chemical markets is direct: companies with integrated mining, refining, precursor, and cathode material strategies can better manage margin volatility than companies dependent on spot-market feedstock.

T1 Energy to Acquire KORE Power

T1 Energy’s planned acquisition of KORE Power for approximately $32 million gives it an entry point into battery energy storage systems and data center infrastructure markets.

This is important because energy storage is no longer a secondary battery application. It is becoming a core demand center. KORE’s engineering and BESS capabilities give T1 a path to combine solar manufacturing, storage integration, and power infrastructure offerings.

The deal also reflects growing demand from AI data centers and industrial power users that need scalable energy storage solutions.

AESC Sells Majority Stake in Tennessee Battery Plant to Fixx Energy

AESC’s sale of a majority stake in its Tennessee LFP battery cell manufacturing facility to Fixx Energy reflects a different kind of strategic shift: regulatory restructuring.

The U.S. market is increasingly focused on domestic content, foreign entity of concern rules, and bankable supply chains. By shifting ownership while maintaining technology relationships, the deal shows how battery assets may be restructured to preserve access to customers, incentives, and financing.

This is likely to become a recurring theme. Battery manufacturing is no longer evaluated only on cost and capacity. Ownership structure, supply origin, compliance status, and policy eligibility are becoming commercial factors.

Battery Industry Funding Trends in 2026

Battery funding is becoming more selective, but not weaker. Capital is moving toward technologies and assets that solve defined bottlenecks.

Solid-state battery funding remains active because the potential upside is high, especially for safety and energy density. However, investors are increasingly looking for credible manufacturing pathways rather than laboratory claims.

Silicon anode funding is strong because it offers a near-term performance upgrade for lithium-ion batteries. Companies that can demonstrate cycle life, manufacturability, and customer qualification are attracting attention.

Battery recycling continues to attract capital because it supports local supply chains and future recovered-material availability. The strategic value of recycling increases as more batteries reach end-of-life and as regional content rules become stricter.

Battery manufacturing automation is also gaining momentum. Coating, drying, formation, testing, inspection, data systems, and factory software are all becoming important because yield is now a major determinant of profitability.

Strategic Opportunities in Battery Chemicals

Battery chemicals remain one of the highest-value areas of the battery supply chain. However, opportunities are becoming more specialized.

Cathode materials remain central. LFP is gaining share due to cost and safety, while high-nickel materials remain relevant for long-range and premium applications. Manganese-rich chemistries and sodium-ion cathodes may create future diversification.

Anode materials are entering a major transition. Graphite localization, synthetic graphite production, natural graphite processing, and silicon-enhanced materials are all becoming strategic priorities.

Electrolyte innovation is gaining importance as fast charging, high-voltage cathodes, silicon anodes, and solid-state systems require more advanced formulations.

Conductive additives are moving from commodity inputs to performance enablers. Conductive carbons, dispersions, nanotubes, and graphene-based systems can improve electrode conductivity and cell efficiency.

Recycled feedstocks will become increasingly important. Recovered lithium, nickel, cobalt, manganese, copper, and graphite can reduce dependence on primary mining and support local content strategies.

Localized material production is a major opportunity. Battery chemical suppliers that can produce near cell manufacturing hubs will gain advantages in logistics, compliance, customer collaboration, and qualification speed.

For deeper forecasts, supplier benchmarking, and market sizing, link here: Battery Chemicals Market Report

Strategic Opportunities in Battery Components

Battery components are becoming more valuable as battery systems become safer, smarter, and more application-specific.

Battery management systems are critical because battery packs now require more precise monitoring of voltage, temperature, state of charge, state of health, and safety risk.

Thermal management systems are gaining importance as fast charging, high-energy cells, and dense battery packs increase heat control requirements. Liquid cooling, advanced heat exchangers, thermal interface materials, and phase-change materials will remain important areas of innovation.

Separators are becoming more advanced. Ceramic-coated separators, thinner films, higher thermal stability, and chemistry-specific separator designs will be important for safety and performance.

Cell packaging and structural components are becoming more complex as battery packs become part of vehicle structures, energy storage enclosures, and industrial systems.

Smart sensors are emerging as a high-value component category. Gas, pressure, temperature, strain, and current sensors can improve safety monitoring and predictive maintenance.

Manufacturing equipment components are also strategic. Rollers, coating systems, inspection modules, formation equipment, and automation parts directly influence factory yield and production cost.

For detailed forecasts and supplier opportunities, link here: Battery Components Market Report

Risk Radar: What Could Reshape Battery Supply Chains by 2030

Critical mineral volatility remains a central risk. Lithium, graphite, nickel, cobalt, manganese, and copper markets can change quickly due to supply disruptions, export controls, permitting delays, or demand shocks.

Technology obsolescence is another risk. Companies tied too heavily to one chemistry or format may face margin pressure if the market shifts faster than expected.

Manufacturing overcapacity is emerging in some regions. Battery plants require high utilization, and underused capacity can trigger pricing pressure, impairments, or asset sales.

Geopolitical risk is intensifying. Battery supply chains are exposed to tariffs, local content rules, foreign ownership restrictions, and strategic mineral policy.

ESG compliance is becoming more demanding. Carbon footprint, water use, labor practices, recycling content, traceability, and responsible sourcing will affect customer qualification.

Execution risk remains high. Battery projects require technical yield, stable customers, financing, utility access, workforce training, and supply agreements. Weakness in any of these areas can delay commercialization.

Strategic Playbook for 2026–2030

The next five years will reward companies that treat the battery value chain as an integrated system.

Battery chemical suppliers should secure long-term feedstock, invest in recycling partnerships, localize production, and develop next-generation chemistries such as silicon materials, sodium-ion inputs, advanced electrolytes, and manganese-rich cathodes.

Battery component suppliers should focus on smart, safety-critical, and chemistry-flexible components. BMS, thermal management, advanced separators, sensors, structural parts, and manufacturing equipment components are likely to capture higher-value demand.

Battery manufacturers should design facilities for flexibility. Plants that can serve EVs, stationary storage, and industrial applications will be better positioned than facilities dependent on one end market.

Investors should focus on bottleneck technologies rather than headline capacity. The most attractive opportunities may sit in anode materials, recycling feedstocks, electrolyte additives, separators, thermal systems, inspection technology, and manufacturing automation.

Strategic buyers should monitor distressed but valuable assets. The Lyten-Northvolt transaction shows that failed business models can still contain valuable infrastructure, talent, IP, and regional manufacturing capacity.

Outlook: Where the Biggest Value Will Be Created

The battery industry in 2026 is entering a more mature but more competitive phase. Growth remains strong, but value creation is shifting away from broad capacity expansion toward technology relevance, supply chain resilience, cost control, and regional alignment.

Battery chemicals will create value through advanced materials, localized processing, recycling integration, and chemistry diversification. Battery components will create value through safety, intelligence, thermal control, manufacturability, and system-level performance.

The biggest winners will be companies positioned at the intersection of technology and execution. Innovation alone will not be enough. Capacity alone will not be enough. The strongest positions will combine materials expertise, component integration, manufacturing discipline, customer qualification, and supply chain control.

The future battery supply chain will not be built around isolated products. It will be built around connected ecosystems where chemicals, components, cells, packs, recycling, and software reinforce each other.