Therapeutic Hypothermia Market Size& Industry Outlook

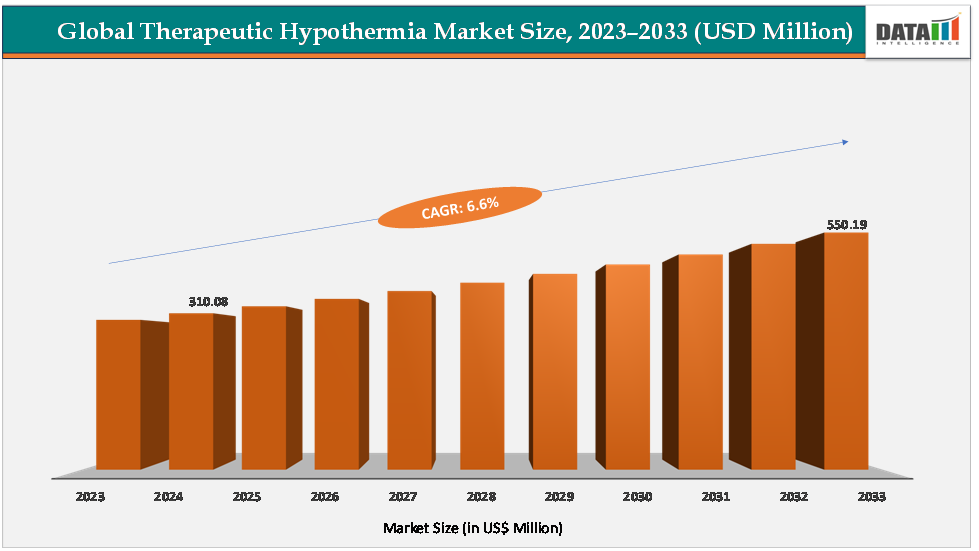

The global therapeutic hypothermia market size reached US $310.08Million in 2024 and is expected to reach US$ 550.19Million by 2033, growing at a CAGR of 6.6%during the forecast period 2025-2033.

The therapeutic hypothermia market is witnessing strong expansion driven by the rising incidence of cardiac arrest, neonatal hypoxic-ischemic encephalopathy, and neurotrauma, alongside stronger clinical guideline adoption. Hospitals are increasingly deploying endovascular cooling systems for precise, rapid temperature control, while surface cooling pads and blankets (offered by Stryker and Gentherm) are gaining traction for their non-invasive ease of use. The neonatal segment, where devices like whole-body cooling blankets are standard in NICUs, is a particularly fast-growing niche. In parallel, demand for recurring consumables such as catheters, probes, and disposable cooling pads ensures recurring revenue streams, reinforcing the market’s growth trajectory.

Key Market Highlights

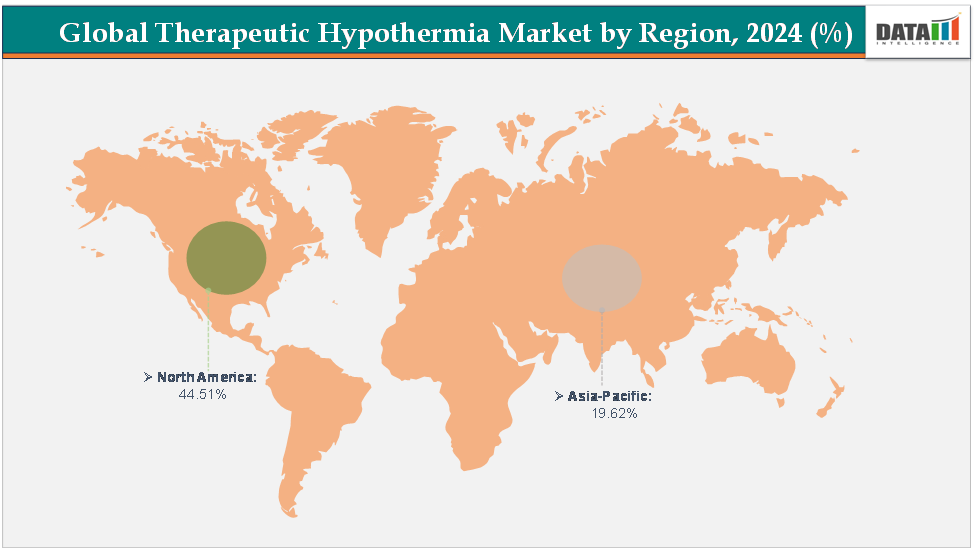

- North America dominates the therapeutic hypothermia market with the largest revenue share of 44.51% in 2024.

- The Asia Pacific is the fastest-growing region and is expected to grow at the fastest CAGR of6.7% over the forecast period.

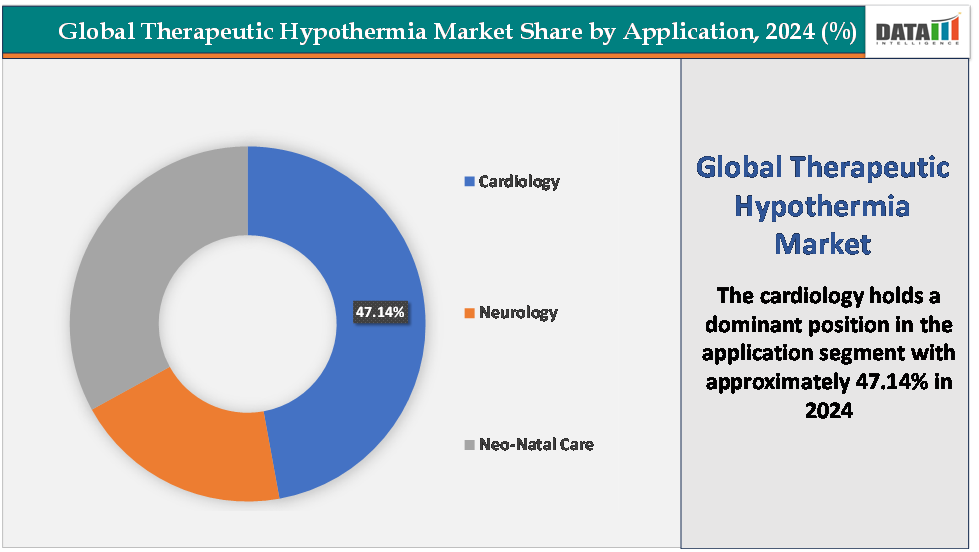

- Based on application, the cardiology segment led the market with the largest revenue share of 47.14% in 2024.

- The major market players in the therapeutic hypothermia market are BD, Terumo Cardiovascular Systems Corporation, Stryker, Shenzhen Comen Medical Instruments Co., Ltd., Phoenix Medical Systems, Geotherm, International Biomedical Ltd., Asahi Kasei Corporation, Global Healthcare SG, and Aspen Systems, among others

Market Dynamics

Drivers:

High burden of cardiac arrest and neurological emergencies is significantly driving the therapeutic hypothermia market growth

The large and growing clinical burden of cardiac arrest and neurological emergencies is a primary engine behind demand for therapeutic hypothermia (targeted temperature management) devices, every year roughly 350,000–450,000 out-of-hospital cardiac arrests occur in the United States alone, producing a large population of survivors who are candidates for controlled temperature management to reduce brain injury and improve neurologic recovery. Equally, traumatic brain injury (TBI) remains a huge global problem that create continuous ICU demand for neuroprotective strategies.

Together these high-volume indications translate directly into market demand: hospitals need reliable, fast, and protocol-compatible cooling systems to implement guideline-based post-resuscitation care and neuroprotection. Clinical guidelines and registry data showing improved outcomes with high-quality TTM have increased protocol adoption in cardiac arrest pathways, which pulls sales for both surface cooling systems and intravascular catheters.

Manufacturers have responded with both established and newer platforms for instance BD/Mediante's Arctic Sun family and ZOLL’s Thermogram (Thermogram XP / Thermogram HQ and IQool surface systems) remain widely used for precise surface and intravascular temperature control while focused solutions such as the Thermoset rapid-immersion system and ongoing stroke/HIE device studies reflect continued product innovation.

Restraints:

Limited awareness in emerging markets is hampering the growth of the market

Limited awareness and training among healthcare professionals in emerging markets remain major barriers to the growth of the therapeutic hypothermia market. In countries across Asia, Africa, and Latin America, many hospitals and emergency departments still lack standardized post-cardiac arrest or neuroprotective temperature management protocols, leading to underutilization despite clinical evidence.

In neonatal care, while therapeutic hypothermia is the standard of care for hypoxic-ischemic encephalopathy in developed nations, many low- and middle-income regions rely on improvised cooling methods or do not offer it at all, owing to equipment shortages and insufficient staff training. Moreover, high upfront device costs and low reimbursement incentives discourage hospital investments where awareness of long-term benefits remains low. This knowledge gap not only slows clinical adoption but also restricts market penetration for major device manufacturers seeking to expand into high-population, high-need regions.

For more details on this report – Request for Sample

Therapeutic Hypothermia Market, Segmentation Analysis

The global therapeutic hypothermia market is segmented based on product type, application, end-user and region.

Application:

The cardiology segment is dominating the therapeutic hypothermia market with a 47.14% share in 2024

The cardiology segment holds the dominant share of the global therapeutic hypothermia market, primarily driven by the widespread adoption of targeted temperature management (TTM) in post–cardiac arrest care and the high global incidence of cardiovascular emergencies. Each year, an estimated 350,000–450,000 out-of-hospital cardiac arrests occur in the United States alone, and millions more worldwide, making cardiac patients the largest pool eligible for temperature management therapy.

Leading approved devices have further strengthened this dominance by providing rapid, precise, and user-friendly cooling solutions specifically designed for cardiac patients. Key products include BD’s Arctic Sun 5000 (a surface cooling system that automates temperature control with advanced feedback mechanisms) and ZOLL Medical’s Thermogard XP and Thermogard HQ systems (FDA-cleared intravascular catheters offering direct core cooling for critically ill cardiac patients). Other FDA-approved systems such as The ICECAP and ThermoSuit System have enhanced flexibility and reduced induction times, improving feasibility in acute settings.

Hospitals favor these technologies due to their ability to achieve target temperature quickly and maintain it accurately during critical care, aligning with outcome-driven quality metrics. In contrast, neurological and neonatal applications face lower adoption due to limited protocol standardization and smaller patient bases. Overall, the combination of a high patient burden, clear clinical guidelines, robust reimbursement frameworks, and multiple FDA-cleared device options firmly positions cardiology as the largest and most rapidly advancing segment in the therapeutic hypothermia systems market.

The neo-natal care segment is fastest-growing in the therapeutic hypothermia market with a 31.32% share in 2024

The neonatal care segment is emerging as the fastest-growing area within the therapeutic hypothermia market, primarily due to increasing global awareness and adoption of hypothermia therapy for hypoxic-ischemic encephalopathy (HIE) in newborns. HIE affects an estimated 1–1.2 million infants annually worldwide, with the highest burden in low- and middle-income countries, where birth asphyxia remains a leading cause of neonatal mortality and neurodevelopmental disability. Clinical studies have demonstrated that controlled cooling within six hours of birth can significantly reduce mortality and long-term neurological impairment, prompting organizations such as the World Health Organization (WHO) and American Academy of Pediatrics (AAP) to endorse therapeutic hypothermia as the standard of care for moderate-to-severe HIE.

As a result, hospitals and neonatal intensive care units (NICUs) in both developed and developing regions are increasingly investing in dedicated neonatal cooling technologies. Several FDA-approved and CE-marked systemssuch as GE Healthcare’s Lullaby Hypotherm Pro, Inspiration Healthcare’s Tecotherm Neo, and ZOLL’s Blanketrol IIIoffer precise, servo-controlled temperature regulation tailored for infants, ensuring safe and consistent hypothermia treatment. Additionally, the introduction of portable, cost-effective cooling devices in resource-limited settings has expanded accessibility.

Geographical Analysis

North America is dominating the global therapeutic hypothermia market with a 44.51% in 2024

North America dominates the global therapeutic hypothermia market due to its advanced healthcare infrastructure, high prevalence of cardiac arrest and neurological emergencies, and widespread implementation of targeted temperature management (TTM) protocols in hospitals. Strong support from organizations such as the American Heart Association (AHA), coupled with favorable reimbursement policies and early regulatory approvals for devices like BD’s Arctic Sun and ZOLL’s Thermogard XP, have accelerated adoption across cardiac and neurocritical care units. Additionally, the region’s strong R&D ecosystem and presence of leading manufacturers further consolidate its market leadership.

US Therapeutic Hypothermia Market Trends

The United States is the largest and most dominant market for therapeutic hypothermia systems globally, owing to its advanced healthcare infrastructure, strong clinical adoption, and favorable regulatory environment. The country reports approximately 350,000–450,000 out-of-hospital cardiac arrests annually, making it the single largest pool of potential candidates for targeted temperature management (TTM). Clinical guidelines from the American Heart Association (AHA) and American Stroke Association (ASA) formally recommend TTM for comatose post–cardiac arrest patients, which has driven nationwide adoption in emergency departments and intensive care units.

The U.S. Food and Drug Administration (FDA) has played a key role in facilitating innovation through 510(k) clearances for several leading TTM systems, including BD’s Arctic Sun 5000, ZOLL Medical’s Thermogard XP and Thermogard HQ, and Stryker’s Altrix Temperature Management System, all widely used across major U.S. hospitals. In the neonatal space, the FDA-cleared Inspiration Healthcare Tecotherm Neo and GE Healthcare’s Lullaby Hypotherm Pro are increasingly deployed for treating hypoxic-ischemic encephalopathy (HIE). The presence of major manufacturers and innovators such as Becton, Dickinson and Company (BD), ZOLL Medical (Asahi Kasei Group), Stryker Corporation, and Medtronic plc strengthens domestic supply, R&D, and training ecosystems.

The Asia Pacific region is the fastest-growing region in the global therapeutic hypothermia market, with a CAGR of 6.7% in 2024

The Asia–Pacific (APAC) region is recognized as the fastest-growing market for therapeutic hypothermia systems, driven by its rapidly improving healthcare infrastructure, growing awareness of targeted temperature management (TTM), and increasing incidence of cardiac arrest, stroke, traumatic brain injury (TBI), and neonatal hypoxic-ischemic encephalopathy (HIE). The region faces a significant disease burden for instance, India and China together report over 700,000 cardiac arrest cases annually, while neonatal HIE remains one of the leading causes of infant mortality in South and Southeast Asia. Governments across the region are expanding access to critical care, with countries such as India, China, Japan, and South Korea investing heavily in intensive care and neonatal facilities.

Regulatory bodies, including Japan’s Pharmaceuticals and Medical Devices Agency (PMDA), China’s National Medical Products Administration (NMPA), and India’s Central Drugs Standard Control Organization (CDSCO), have streamlined device approval pathways, enabling faster market entry for TTM products. Multinational players such as ZOLL Medical, BD (Becton Dickinson), Stryker, and Inspiration Healthcare have increased their presence through partnerships and localized manufacturing to reduce costs and improve accessibility.

Additionally, regional initiatives such as the India Newborn Action Plan and China’s Healthy China 2030 emphasize neonatal survival, indirectly boosting the adoption of hypothermia devices in hospitals. Combined with rising healthcare investments, increased physician training, and supportive reimbursement reforms in advanced markets like Japan and Australia, these developments are fueling double-digit growth rates. As a result, APAC is poised to remain the fastest-growing and most strategically important region in the global therapeutic hypothermia market over the next decade.

Europe Therapeutic Hypothermia Market Trends

The European region represents one of the most mature and steadily expanding markets for therapeutic hypothermia, driven by strong clinical adoption, supportive regulatory frameworks, and continuous technological advancements. Europe records nearly 275,000–300,000 cardiac arrests annually, with countries such as Germany, the U.K., France, and Italy leading in the implementation of targeted temperature management (TTM) protocols across intensive care and emergency settings. The European Resuscitation Council (ERC) has been instrumental in promoting therapeutic hypothermia as a standard of care for comatose cardiac arrest survivors, aligning clinical practice across member states.

Regulatory support from the European Medicines Agency (EMA) and national agencies under the EU Medical Device Regulation (MDR 2017/745) ensures patient safety while accelerating the approval of innovative temperature management devices. Major companies such as ZOLL Medical (Asahi Kasei Group), BD (Becton Dickinson), Stryker Corporation, and Inspiration Healthcare Group maintain strong distribution networks across Europe, with locally manufactured or CE-marked systems such as Arctic Sun 5000, Thermogard XP, Tecotherm Neo, and Blanketrol III widely adopted in hospitals and neonatal intensive care units.

Therapeutic Hypothermia Market Competitive Landscape

Top companies in the therapeutic hypothermia market include BD, Terumo Cardiovascular Systems Corporation, Stryker, Shenzhen Comen Medical Instruments Co., Ltd., Phoenix Medical Systems, Gentherm, International Biomedical Ltd., Asahi Kasei Corporation, Global Healthcare SG, and Aspen Systems, among others.

Therapeutic Hypothermia Market Scope

| Metrics | Details | |

| CAGR | 6.6% | |

| Market Size Available for Years | 2022-2033 | |

| Estimation Forecast Period | 2025-2033 | |

| Revenue Units | Value (US$ Mn) | |

| Segments Covered | Product Type | Surface Cooling Systems, Endovascular (Intravascular) Cooling Systems, Temperature Management Systems, and Others |

| Application | Cardiology, Neurology, and Neo-Natal Care | |

| End-User | Hospitals, Ambulatory Surgical Centers, Specialty Clinics, and Academic Research Institutes | |

| Regions Covered | North America, Europe, Asia-Pacific, South America and the Middle East & Africa | |

The global therapeutic hypothermia market report delivers a detailed analysis with 62 key tables, more than 54visually impactful figures, and 159 pages of expert insights, providing a complete view of the market landscape.

Suggestions for Related Report

For more medical devices-related reports, please click here