Supply Chain Cybersecurity Market Size

Cybersecurity risk is no longer limited to internal enterprise systems. Vendors, contract manufacturers, logistics partners, software suppliers, IoT assets and third-party service providers have become major entry points for cyberattacks. As a result, organizations are shifting from enterprise-only protection to supply chain-wide cyber resilience.

Supply Chain Cybersecurity Market is valued at US$ 803 million in 2025 and is projected to reach US$ 2,913.66 million by 2035, growing at a CAGR of 13.70% during 2026–2035.

The market matters now because cyber incidents increasingly originate through third-party access points. With over 90% of critical infrastructure breaches linked to vendors in recent years, supply chain cybersecurity is moving from a compliance checklist to a board-level investment priority. Procurement teams are embedding cyber requirements into supplier contracts, regulators are expanding third-party compliance rules and CIOs are extending zero-trust architectures beyond enterprise perimeters.

Supply Chain Cybersecurity Market Scope

| Metric | Details |

| Market Size in 2025 | US$803 million |

| Market Size by 2035 | US$2,913.66 million |

| CAGR | 13.70% during 2026 to 2035 |

| Historic Years | 2023 to 2024 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Segments Covered | Component, Deployment, Organization Size, Application and End-User |

| Leading Region | North America |

| Fastest Growing Region | Asia-Pacific |

Key Takeaways

- The Supply Chain Cybersecurity Market is projected to grow from US$803 million in 2025 to US$2,913.66 million by 2035.

- The Supply Chain Cybersecurity Market Size in 2026 is estimated at US$913.01 million, supported by regulatory enforcement and vendor risk visibility needs.

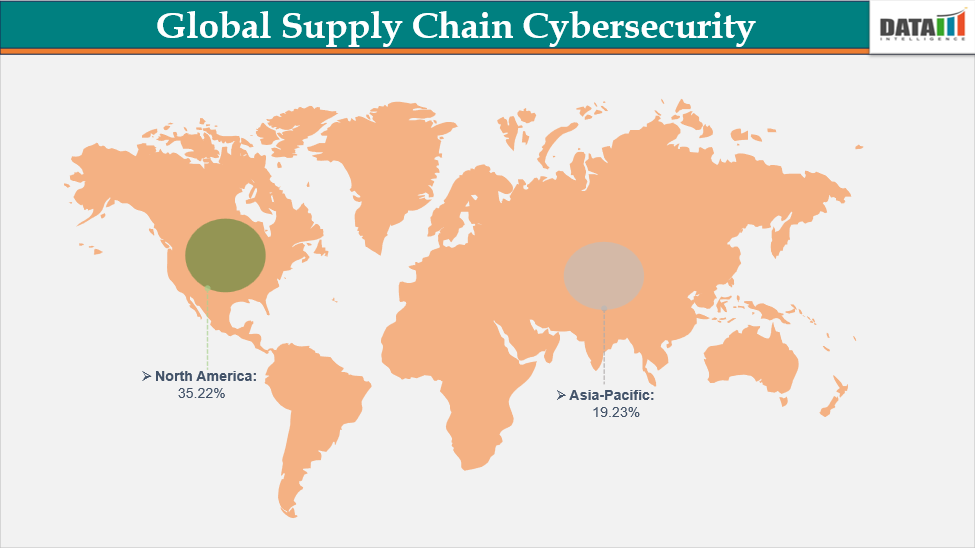

- North America accounted for 35.22% of the Supply Chain Cybersecurity Market Share in 2025, driven by CMMC and NIST-related compliance demand.

- Asia-Pacific held 19.23% share in 2025 and is the fastest-growing region, supported by cybersecurity frameworks in Japan, South Korea and Singapore.

- Hardware solutions hold 42.7% market share, reflecting the need to secure IoT devices, RFID systems, logistics assets and physical supply chain infrastructure.

- Over 66% of suppliers lack standardized cybersecurity protocols, creating a large compliance and risk management gap for enterprises.

- Compliance cost remains a barrier for smaller vendors, with expenses ranging from US$1,000 to US$50,000, slowing adoption across lower-tier suppliers.

Market Scope

| Metric | Details |

| Market Size (2025) | US$ 803 Million |

| Market Size (2035 Forecast) | US$ 2,913.66 Million |

| CAGR (2026–2035) | 13.70% |

| Historic Years | 2023–2024 |

| Base Year | 2025 |

| Forecast Period | 2026–2035 |

| Segments Covered | Component, Deployment, Organization Size, Application, End-User |

| Leading Region | North America |

| Fastest Growing Region | Asia-Pacific |

For more details on this report, Request for Sample

Threat Landscape and Demand Signals

Multi-Tier Supplier Networks Are Expanding the Attack Surface

The Supply Chain Cybersecurity Market Growth is being shaped by indirect cyberattacks. Cybercriminals increasingly target smaller vendors, logistics software, IoT devices and software suppliers to access larger enterprises. This creates major blind spots across multi-tier supplier ecosystems, especially in manufacturing, defense, transportation, logistics and critical infrastructure.

Enterprises are responding by investing in supplier risk scoring, continuous monitoring, identity verification, threat intelligence and contract-level cybersecurity controls. Visibility across the supplier base is becoming as important as internal network protection.

Compliance Is Becoming a Purchasing Trigger

Regulation is converting supply chain cybersecurity from discretionary IT spending into a mandatory operational requirement. Key compliance drivers include the U.S. Cybersecurity Maturity Model Certification, NIST supply chain risk management standards, Japan’s METI cybersecurity evaluation system rollout by 2026, South Korea’s national cybersecurity mandates across 14 sectors and EU-driven supplier security standardization initiatives.

These requirements are changing procurement behavior. Vendors increasingly need to prove cyber readiness before qualifying for contracts, especially in defense, government, critical infrastructure and regulated manufacturing supply chains.

Market Dynamics

Zero-Trust Architecture Across Vendor Ecosystems

Enterprises are replacing perimeter-based security models with zero-trust frameworks that continuously verify users, devices, applications and third-party access points. Government mandates such as the U.S. OMB directive for federal zero-trust adoption are accelerating this shift.

For suppliers, zero-trust compliance is becoming a contract requirement. This creates a cascading demand effect across large enterprises, prime contractors, tier-one suppliers and lower-tier vendors.

Sector-Level Adoption Maturity

Adoption varies widely by industry. Defense and aerospace show the highest maturity because strict compliance mandates require suppliers to meet defined security standards. Manufacturing is growing rapidly due to industrial IoT vulnerabilities and connected production networks. Retail and e-commerce are focusing on data protection, payment security and vendor access risk. Healthcare adoption is rising due to sensitive data exposure and third-party service dependencies.

This uneven maturity creates different opportunity pools. Regulated industries are investing faster, while SMEs often need lower-cost managed services and compliance support.

Multi-Tier Vendor Complexity

The biggest operational challenge is securing hundreds or thousands of suppliers across multiple tiers. Lack of standardized controls, fragmented documentation, limited cyber expertise and weak visibility increase implementation complexity. SMEs are particularly exposed because many cannot afford enterprise-grade cybersecurity programs.

Market Opportunities

Vendor Risk Standardization

Technology providers that simplify supplier onboarding, risk scoring, compliance tracking and continuous monitoring are well positioned. Enterprises need repeatable frameworks that can be applied across large supplier bases without creating excessive procurement delays.

Hardware-Embedded Security

Hardware accounts for 42.7% of the market, creating opportunities in secure chips, tamper-proof devices, IoT tracking systems, RFID security and logistics asset protection. Manufacturing and logistics companies are increasingly combining physical asset security with digital risk management.

Managed Security Services

SMEs are turning to managed security providers because internal cybersecurity resources are limited. Compliance-as-a-service, continuous monitoring, third-party risk audits and managed detection services can help smaller suppliers meet enterprise and regulatory requirements.

Asia-Pacific Regulatory Adoption

Japan, South Korea and Singapore are creating structured demand through government-led cybersecurity frameworks. Vendors entering these markets early can benefit from compliance-driven purchasing cycles and industrial digitalization.

Economic and Investment Analysis

Macroeconomic pressure on supply chains is increasing the need for resilience. Cyberattacks can disrupt production, logistics, customer data, procurement systems and critical infrastructure operations. As a result, cybersecurity is becoming part of supply chain risk management, not only IT budgeting.

Investment is moving toward zero-trust platforms, supplier risk management software, AI-driven threat detection, hardware security, cloud-based monitoring and managed security services. Large enterprises are likely to continue investing in integrated platforms, while SMEs may adopt tiered pricing and subscription-based models.

ROI is linked to breach avoidance, compliance readiness, reduced vendor risk, faster supplier qualification and lower disruption exposure. Key economic risks include high compliance costs for small vendors, fragmented supplier maturity and rising implementation complexity across multi-tier ecosystems.

Segmentation Analysis

Segmented by component (hardware, software, services), by deployment (cloud, on-premises), by organization size (SMEs, large enterprises), by application (data protection, data visibility and governance, others), by end-user (automotive, FMCG, healthcare, manufacturing, retail and e-commerce, transportation and logistics), and by Region - Share, Trends, and Forecast to 2035.

By component, hardware dominates with 42.7% market share. Demand is driven by the need to secure IoT devices, RFID systems, connected production equipment and logistics assets. Enterprises are investing in embedded security features such as cryptographic chips, tamper detection and secure device authentication.

Software and services are gaining traction as companies need integrated platforms for vendor risk assessment, compliance tracking, identity verification, threat detection and incident response.

By deployment, cloud-based solutions are growing due to scalability, faster integration and multi-vendor monitoring capabilities. On-premises deployment remains relevant in highly regulated sectors where sensitive supplier and infrastructure data must remain under direct enterprise control.

By organization size, large enterprises lead adoption due to compliance exposure and complex supplier ecosystems. SMEs remain a major opportunity for managed security services because cost and skill constraints limit internal implementation.

Regional Analysis

North America

North America leads the Supply Chain Cybersecurity Market, accounting for 35.22% share in 2025. The U.S. is the primary growth engine, supported by federal mandates such as CMMC and NIST supply chain risk management guidelines. CMMC impacts over 300,000 contractors, creating a large compliance-driven market across defense and federal supplier ecosystems.

The region also benefits from major cybersecurity vendor presence, high enterprise awareness and growing adoption of zero-trust security. SMEs remain a vulnerability across the supplier base, creating strong opportunities for managed security providers and compliance automation platforms.

Asia-Pacific

Asia-Pacific held 19.23% market share in 2025 and is the fastest-growing region. Japan, South Korea and Singapore are driving adoption through government-led compliance frameworks and national cybersecurity programs.

Industrial IoT expansion, smart manufacturing and connected logistics are increasing the attack surface. Enterprises in the region are investing in supplier security platforms, hardware safeguards and compliance-focused monitoring tools to reduce operational and regulatory risk.

Europe

Europe’s market is shaped by regulatory pressure, supplier security standardization and rising enterprise awareness of third-party cyber exposure. Companies are prioritizing vendor risk management because many suppliers still lack standardized cybersecurity protocols.

Demand is expected to grow around supplier compliance platforms, data protection, cloud security, risk scoring and standardized onboarding processes. Europe’s focus on governance and risk controls supports steady adoption across manufacturing, healthcare, logistics and retail supply chains.

Competitive Landscape and Vendor Strategy

The major companies in the Supply Chain Cybersecurity Market include IBM Corporation, Cisco Systems, Inc., Palo Alto Networks, Inc., Check Point Software Technologies Ltd., Fortinet, Inc., Trellix Corporation, CrowdStrike Holdings, Inc., Broadcom Inc. (Symantec Enterprise Division), Trend Micro Incorporated and Kaspersky Lab JSC.

Leading vendors are expanding zero-trust capabilities, AI-driven threat detection, hybrid cloud security and third-party risk management. IBM leverages AI-driven security platforms and SIEM capabilities to provide visibility across vendor ecosystems. Cisco and Palo Alto Networks are embedding security into network and cloud infrastructure. CrowdStrike focuses on endpoint security, identity protection and threat intelligence. Fortinet, Trend Micro, Check Point and Trellix are strengthening integrated security platforms for distributed enterprise and supplier environments.

The competitive landscape is shifting toward platform consolidation. Buyers increasingly prefer solutions that combine hardware protection, software risk management, compliance automation, managed services and real-time threat intelligence.

Recent Developments

- In June 2026, Cisco expanded AI-powered security for enterprise supply chains through enhanced capabilities across its Hybrid Mesh Firewall and Cisco Security Cloud platforms, strengthening threat detection, third-party risk management and zero-trust protection.

- In June 2026, Palo Alto Networks enhanced Prisma AIRS for AI and software supply chain security, adding advanced protections for AI applications, software supply chains and cloud-native environments.

- In May 2026, CrowdStrike expanded its Falcon platform to strengthen supply chain resilience, adding capabilities for identity protection, cloud security and real-time threat intelligence.

- In May 2026, Fortinet enhanced its AI-powered Security Fabric platform with new threat detection, automated incident response and integrated network security capabilities.

- In April 2026, Trend Micro advanced its Cyber Risk Exposure Management platform with expanded attack surface visibility, vulnerability prioritization and AI-assisted threat intelligence.

- In March 2026, Check Point Software strengthened its Infinity Platform with AI-powered threat prevention, automated security operations and enhanced cloud protection.

- In February 2026, Trellix expanded its XDR platform for supply chain threat detection, adding advanced threat intelligence and automation for faster investigation and response.

Regulatory and Policy Analysis

Regulatory pressure is one of the most important drivers of the Supply Chain Cybersecurity Market Forecast. CMMC, NIST supply chain risk management standards, Japan METI cybersecurity evaluation requirements, South Korea’s national mandates and EU supplier security initiatives are reshaping enterprise procurement.

Government programs are pushing organizations to verify supplier security maturity before contract award. This is increasing demand for compliance evidence, continuous monitoring, cyber audits, vendor scoring and third-party risk documentation.

Expected regulatory changes are likely to raise the cost of non-compliance. Enterprises that standardize supplier cybersecurity early may reduce future remediation costs, procurement delays and operational disruption risk.

Impact Analysis

Supply chain cybersecurity affects procurement, vendor qualification, logistics continuity, manufacturing resilience and enterprise risk governance. Cybersecurity is now embedded into supplier selection and contract management, particularly in defense, critical infrastructure, healthcare and manufacturing.

Policy impact is visible through compliance-driven spending. Supplier ecosystems that fail to meet minimum cybersecurity standards may lose contract eligibility or face higher onboarding costs. Hardware security also has direct operational impact because connected assets, IoT devices and tracking systems are now part of the cyber risk surface.

Strategic Insights and Analyst Perspective

The Supply Chain Cybersecurity Market Trends point toward continuous supplier monitoring, zero-trust access, AI-driven threat detection and standardized compliance workflows. Enterprises should treat supply chain cybersecurity as a cross-functional program involving procurement, IT, legal, risk and operations.

Vendors should prioritize ease of supplier onboarding, automated risk scoring, regulatory mapping and flexible pricing for SMEs. Investors should track platforms that combine compliance automation with threat intelligence and managed services.

Risk mitigation should focus on supplier segmentation, minimum security baselines, contract-level cyber clauses, continuous monitoring and incident response coordination across vendors.

Report Benefits

This Supply Chain Cybersecurity Market Report helps cybersecurity vendors identify demand across hardware, software and managed services. Enterprises can use the report to benchmark supplier risk priorities, compliance requirements and regional adoption trends.

Investors can assess high-growth opportunities in zero-trust platforms, vendor risk management, hardware security and managed security services. Procurement teams can understand supplier qualification requirements, cost barriers and contract-level cybersecurity expectations. Strategy teams can evaluate regional expansion, compliance-led demand and competitive positioning.

Target Audience

- Cybersecurity vendors

- Managed Security Service Providers (MSSPs)

- Hardware security companies

- Cloud security firms

- Procurement heads

- Chief Information Officers (CIOs)

- Chief Information Security Officers (CISOs)

- Compliance officers

- Supply chain leaders

- Defense contractors

- Manufacturing companies

- Logistics providers

- Healthcare organizations

- Retailers and retail chains

- Investors in cybersecurity sector

- Private equity firms

- Corporate strategy teams

The global supply chain cybersecurity market report delivers a detailed analysis with 78 key tables, more than 74 visually impactful figures, and 239 pages of expert insights, providing a complete view of the market landscape.