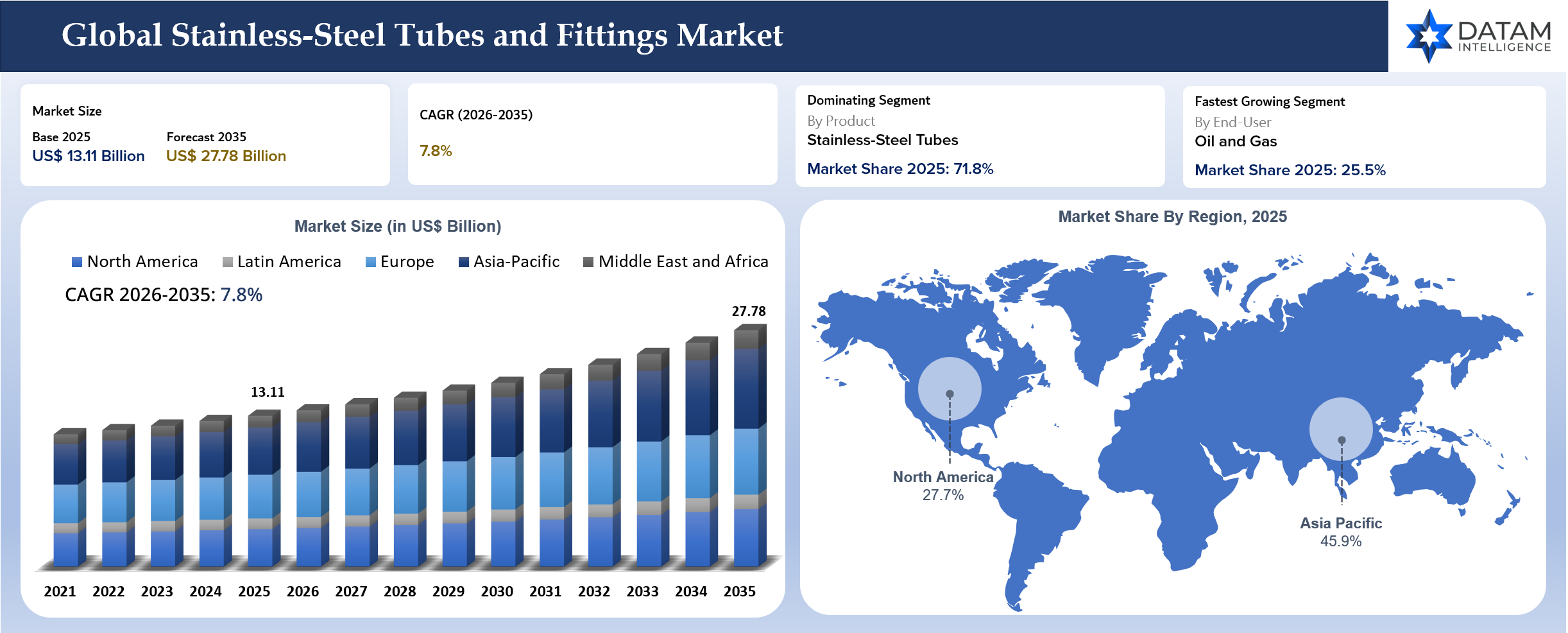

Stainless-Steel Tubes and Fittings Market Size

The global stainless-steel tubes and fittings market reached US$ 13.11 billion in 2025 and is expected to reach US$ 27.78 billion by 2035, growing with a CAGR of 7.8% during the forecast period 2026-2035. The global stainless steel tubes and fittings market is shaped by reliability-critical fluid handling, hygienic processing, high-purity gas distribution and corrosion-resistant industrial infrastructure. Demand is strongest where system failure creates production loss, contamination risk, safety exposure or expensive maintenance. Chemical plants, refineries, semiconductor fabs, pharmaceutical facilities, food and beverage plants, hydrogen systems, offshore energy assets and industrial utilities are therefore the most important demand pockets.

Fittings demand is driven by the need for leak-tight connections, faster installation, reliable reassembly and compliance with pressure, vibration and media compatibility requirements. Swagelok positions tube fittings and adapters around leak reduction, downtime avoidance, tube grip, vibration resistance and material availability across industrial fluid systems. Its product range includes tube fittings, tube adapters, unions, reducers, socket weld fittings, caps, plugs and pipe fittings with stainless steel and alloy options.

High-purity tubing is witnessing strong growth because semiconductor fabs, pharmaceutical plants and biotech facilities need cleaner internal surfaces, controlled documentation and better traceability. According to Dockweiler, stainless steel tubes and fittings are used in microelectronics, life science, energy and industrial processes and offers surface finishes from 0.8 µm to 0.13 µm for demanding purity requirements.

Raw material exposure remains a core commercial issue. Nickel and chromium influence grade selection, surcharge mechanisms and procurement timing. As per USGS, stainless and alloy steel and nickel-containing alloys typically account for more than 85% of U.S. nickel consumption while nickel recovered from scrap accounted for around 54% of U.S. apparent consumption in 2024.

Stainless-Steel Tubes and Fittings Key Takeaways

- Stainless steel tubes dominated the market with 71.8% share in 2025, supported by demand across heat exchangers, process piping, instrumentation lines, hydraulic systems, semiconductor gas distribution, pharmaceutical utilities and precision mechanical assemblies.

- Stainless steel fittings are gaining strategic value as buyers focus on leak prevention, installation speed, reassembly performance, documentation and system downtime reduction rather than only fitting cost.

- Oil and gas was the fastest-growing end user with 25.5% market share in 2025 and is forecast to grow at 9.0% CAGR during 2026-2035, driven by LNG infrastructure, offshore projects, refinery upgrades, subsea systems, high-pressure instrumentation and corrosion-resistant process lines.

- Semiconductor and pharmaceutical facilities are creating a premium demand layer for electropolished tubes, high-purity fittings, cleanroom packaging, ASME BPE-aligned components and documented material traceability.

- Austenitic stainless steel remains the core material family because 304, 304L, 316 and 316L grades are widely accepted across process industries, construction, food processing and hygienic applications.

- Duplex and super duplex stainless steel are gaining importance in offshore energy, chemical processing, desalination, marine systems and high-chloride environments where buyers need higher strength and stronger pitting resistance.

- Nickel and chromium cost exposure will remain a major procurement factor because grade substitution, alloy surcharges, scrap availability and regional import dependence directly affect quoted pricing.

- Supplier differentiation is moving toward documentation, surface finish control, local stock availability, special alloy capability, fast project delivery and technical support for welding, bending, orbital welding and system qualification.

Stainless-Steel Tubes and Fittings Industry Trends and Strategic Insights

- Semiconductor fabs are shifting premium demand toward UHP (Ultra High Purity) tube systems. Stainless steel tubes and fittings used in microelectronics must support ultra-clean gas and liquid transport, lower particle risk and consistent orbital welding outcomes.

- Hygienic processing is becoming a stronger purchasing driver. Pharmaceutical, biotech and food plants are not only buying corrosion-resistant components. Buyers also need cleanability, surface finish consistency, documentation and standardized dimensions.

- Procurement teams are separating commodity stainless tubes from application-critical tubing. Standard welded tubes face price competition. Heat exchanger tubes, high-pressure tubes, subsea tubes, steam generator tubes, semiconductor tubes and pharmaceutical tubes require tighter qualification and supplier trust.

Stainless-Steel Tubes and Fittings Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 13.11 Billion | |

| 2035 Projected Market Size | US$ 27.78 Billion | |

| CAGR (2026-2035) | 7.8% | |

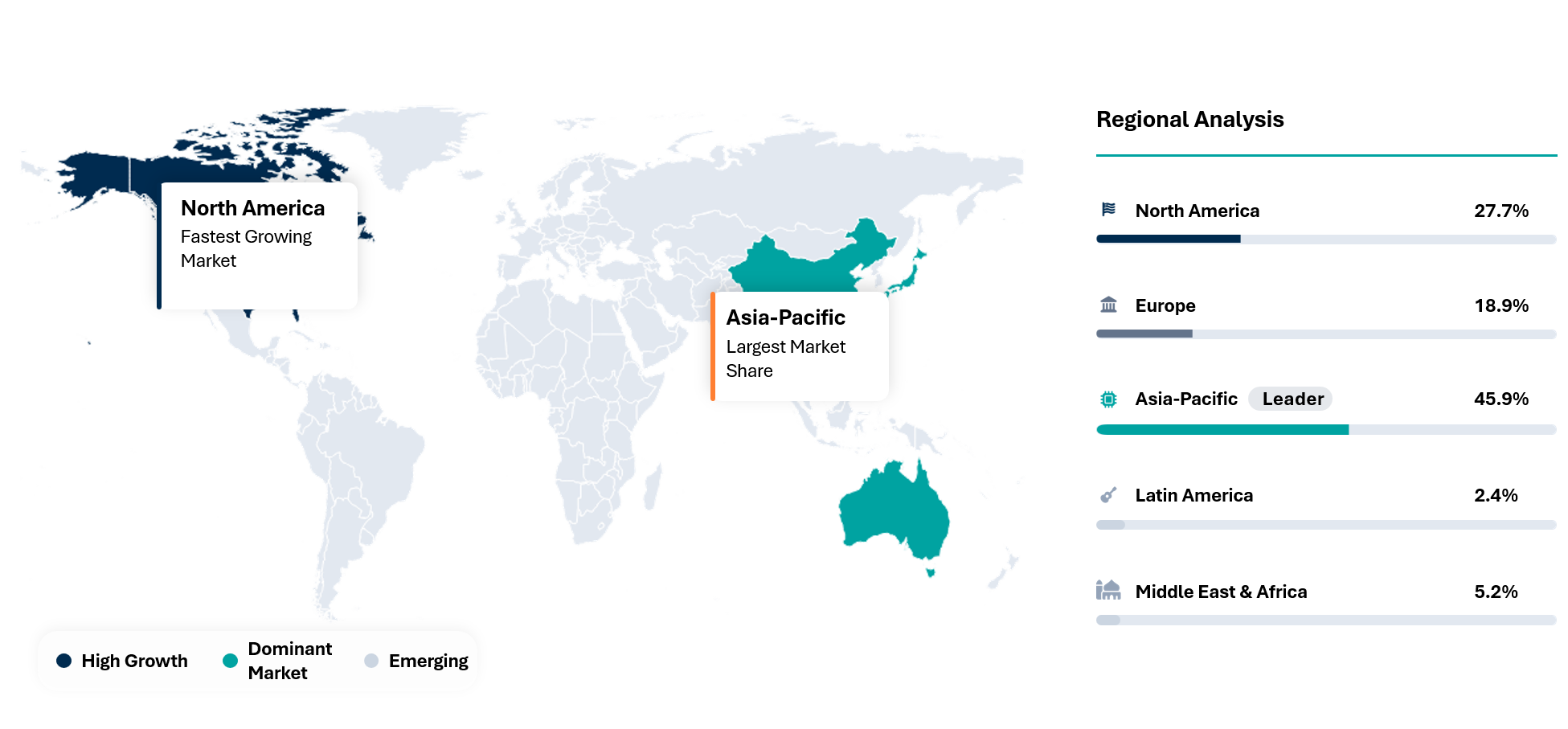

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Product | Stainless-Steel Tubes, Stainless-Steel Fittings | |

| By Steel Grade | Austenitic Stainless-Steel, Ferritic Stainless-Steel, Duplex Stainless-Steel, Super Duplex Stainless-Steel, Martensitic Stainless-Steel, PH (Precipitation Hardening) Stainless-Steel, Others | |

| By Size | Small Diameter, Medium Diameter, Large Diameter | |

| By End-User | Oil and Gas, Chemical and Petrochemical, Power Generation, Food and Beverage, Pharmaceutical and Biotechnology, Semiconductor and Electronics, Water and Wastewater, Automotive and Transportation, Construction and Architecture, Marine and Shipbuilding, Medical Devices, Industrial Machinery, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Why does this report matter in 2026?

Stainless steel tube and fitting buyers enter 2026 with a more complicated sourcing environment. Project owners want shorter lead times, tighter documentation and stronger corrosion performance while suppliers are still managing nickel, chromium, energy, freight and alloy surcharge movement. Low-cost buying creates risk when tubing enters high-purity gas lines, process piping, pressure systems or hygienic utilities where failure can stop production.

The decisive shift is the move from material supply to system assurance. Semiconductor fabs require high-purity tube systems with documented surface quality. Pharmaceutical and biotech facilities need hygienic tubing that supports cleaning, sterilization and validation. Energy and chemical plants need materials that can survive chloride, pressure, heat and sour service exposure. Supplier selection is therefore becoming more technical and documentation-led.

Decision-makers need a report that connects grade selection, product form, end-use conditions, regional supply, alloy pricing and supplier capability. A commodity view of stainless steel tubes and fittings misses the real buying logic in 2026. The strongest opportunities sit where material quality, surface finish, joining method and traceability influence plant uptime and regulatory confidence.

Strategic Indicators For Stainless-Steel Tubes and Fittings

High Regulation Impact

The market is experiencing intensified regulatory pressure driven by carbon-border taxation, traceability mandates, and industrial compliance reforms. The European Union’s Carbon Border Adjustment Mechanism (CBAM) is increasing compliance costs for exporters from India, China, and Southeast Asia supplying stainless process tubes into Europe, forcing mills to invest in low-emission melting and digital emissions reporting. The United States continues tightening ASTM, ASME, and Buy America requirements for energy and infrastructure projects, benefiting domestic manufacturers. India’s Quality Control Orders (QCOs) and BIS certification enforcement are restricting low-grade imports, while Saudi Arabia and the UAE are strengthening local-content rules for oil and gas procurement, reshaping global supplier qualification strategies.

High Investment Activity

Investment momentum accelerated during 2025 as manufacturers expanded high-value corrosion-resistant alloy tube capacity linked to hydrogen, LNG, desalination, and energy-transition projects. Spain-based Tubacex expanded advanced tubular manufacturing capabilities across the Middle East and North America to support CCS and hydrogen infrastructure demand, while Italy-based Marcegaglia increased welded stainless-steel tube production capacity in the UK market. India and Saudi Arabia emerged as strategic investment destinations due to refinery expansion, petrochemical localization, and lower operating costs. Japanese and Korean producers are simultaneously investing in nickel-alloy and duplex stainless tube technologies to capture offshore energy and semiconductor-grade process piping demand.

Supply Chain Disruption

The stainless-steel tubes and fittings supply chain remains exposed to nickel price instability, Red Sea shipping disruptions, and geopolitical fragmentation affecting raw material sourcing. European manufacturers continue facing elevated energy costs and longer alloy procurement cycles, while Chinese exports are encountering stricter anti-dumping scrutiny in North America and Europe. India gained sourcing preference among EPC contractors due to lower-cost welded tube manufacturing and faster delivery cycles. Meanwhile, Middle Eastern refinery expansion projects are tightening availability of corrosion-resistant alloy tubes globally. Logistics bottlenecks at Asian ports and vessel rerouting through the Cape of Good Hope increased lead times for duplex and seamless stainless tubes used in LNG, offshore, and chemical-processing applications.

Pricing Volatility

Pricing volatility is being driven primarily by fluctuating nickel, molybdenum, and ferrochrome input costs alongside unstable freight and energy expenses. European producers experienced higher production costs because of electricity and carbon-related charges, while Chinese mills increased export competitiveness through aggressive pricing strategies. Indian manufacturers maintained relatively stable pricing due to domestic steel integration and lower operating costs, improving export competitiveness in the Middle East and Africa. High-specification duplex and super-austenitic tubes continue commanding premium pricing due to constrained supply availability. EPC contractors are increasingly shifting toward quarterly indexed procurement contracts to mitigate exposure to raw-material and shipping-cost fluctuations.

Procurement Pressure

Procurement teams across oil and gas, power generation, semiconductor, and chemical-processing sectors are facing rising pressure to secure certified stainless-steel tubes with shorter lead times and full traceability compliance. Buyers in the United States and Europe are prioritizing ASME-certified suppliers with documented emissions transparency and localized inventories. Saudi Arabia, the UAE, and Qatar increasingly require local-content participation for refinery and hydrogen infrastructure projects, pressuring international suppliers to establish regional partnerships. Indian manufacturers are benefiting from competitive pricing and integrated production models, while Japanese and European producers retain advantages in high-corrosion-resistant alloy applications. Strategic procurement increasingly emphasizes lifecycle durability, welding consistency, and compliance-driven sourcing rather than lowest-cost purchasing.

New Technology Adoption

The market is rapidly adopting automation, AI-enabled quality inspection, smart pilger mills, and digital twin manufacturing to improve dimensional precision and reduce material wastage. European and Japanese manufacturers are investing heavily in predictive maintenance systems and automated ultrasonic testing for seamless stainless tubes used in nuclear, LNG, and semiconductor applications. India and China are accelerating adoption of robotic welding and Industry 4.0-enabled tube finishing lines to improve export competitiveness. Advanced corrosion-resistant alloys for hydrogen transportation, CCS infrastructure, and offshore energy systems are gaining commercial traction. Digital machining technologies integrated with CAM platforms are also improving precision fittings manufacturing and reducing rejection rates across high-specification industrial applications.

Regional Expansion Opportunity

Asia-Pacific remains the strongest expansion region due to refinery additions, semiconductor investments, and industrial infrastructure growth across India, China, South Korea, and Southeast Asia. India is increasingly emerging as a preferred export hub for welded and seamless stainless tubes due to competitive operating costs, regulatory tightening on imports, and strong EPC-linked demand.

The Middle East is witnessing accelerated demand from hydrogen, desalination, LNG, and petrochemical megaprojects in Saudi Arabia and the UAE. Regional localization mandates and industrial diversification programs are creating long-term opportunities for corrosion-resistant stainless-steel tube manufacturers and fittings suppliers supporting energy-transition infrastructure.

Government Policy Support

Government-backed industrial policies are significantly influencing the stainless-steel tubes and fittings market globally. India’s Production Linked Incentive initiatives, BIS quality mandates, and infrastructure expansion programs are supporting domestic stainless manufacturing competitiveness. The European Union is incentivizing low-carbon steel production and traceability investments through green-transition frameworks, while the United States continues supporting domestic industrial procurement under Buy America policies. Saudi Arabia and the UAE are integrating local manufacturing participation into refinery, hydrogen, and energy-transition projects under Vision 2030 industrial diversification strategies. China is simultaneously prioritizing high-value stainless exports and advanced alloy manufacturing capabilities linked to clean-energy and semiconductor supply-chain development.

Import, Export and Pricing Intelligence

Global stainless-steel tube trade flows are increasingly shifting toward India, Vietnam, and the Middle East as buyers diversify sourcing away from overdependence on China. European importers are prioritizing certified low-carbon suppliers, while GCC countries are increasing imports of corrosion-resistant alloy tubes for hydrogen and petrochemical infrastructure developments.

Pricing behavior remains heavily linked to nickel surcharges, freight volatility, and regional energy costs. European suppliers maintain premium pricing for specialized seamless tubes, while Indian and Chinese manufacturers compete aggressively in welded industrial tube categories serving construction, automotive, and process-industry applications.

| HS Code | Reporter | Trade Flow | 2025 Trade Value | Interpretation |

| HS 730640 | China | Export | USD 5.8 Billion | China continues to dominate global welded stainless-steel tube exports through scale manufacturing and aggressive pricing strategies. |

| HS 730640 | India | Export | USD 1.9 Billion | India strengthened export competitiveness through lower-cost manufacturing and refinery-linked stainless demand. |

| HS 730640 | United States | Import | USD 2.6 Billion | Strong infrastructure, LNG, and industrial retrofit demand continue driving stainless tube imports. |

| HS 730449 | Germany | Import | USD 1.7 Billion | Germany remains dependent on imported high-performance seamless stainless tubes for industrial processing sectors |

| HS 730449 | Saudi Arabia | Import | USD 1.2 Billion | Refinery expansion, hydrogen investments, and desalination projects accelerated imports of corrosion-resistant alloy tubes. |

Company Coverage Preview

Tubacex remains one of the most strategically positioned companies in the global stainless-steel tubes and fittings market due to its vertically integrated manufacturing footprint, advanced corrosion-resistant alloy expertise, and expanding presence in hydrogen, CCS, LNG, and mobility applications. The company operates production facilities across Europe, North America, the Middle East, and Asia while increasingly focusing on high-margin seamless stainless and nickel-alloy tubular systems. Its NT2 strategic transformation plan is reducing dependency on traditional oil-and-gas applications and expanding exposure to energy-transition infrastructure. Strong investments in automation, advanced pilger technologies, and regional service centers continue to strengthen global competitiveness.

AI Impact Analysis

Artificial intelligence is transforming stainless-steel tube manufacturing through predictive quality control, automated defect detection, demand forecasting, and production optimization. Manufacturers are deploying AI-enabled ultrasonic inspection and machine-vision systems to identify dimensional deviations and welding inconsistencies in real time, significantly reducing rejection rates. European and Japanese producers are integrating AI-driven predictive maintenance across pilger mills and heat-treatment lines to improve operational efficiency and minimize downtime. Procurement and inventory management are also benefiting from AI-assisted raw-material forecasting linked to nickel and ferroalloy price movements. In high-specification applications such as hydrogen transport and semiconductor processing, AI-supported manufacturing analytics are improving reliability, traceability, and compliance performance.

Disruption Analysis

Rapid expansion of hydrogen transportation networks, carbon capture systems, desalination plants, semiconductor fabs, and pharmaceutical manufacturing facilities is reshaping demand patterns toward high-purity, corrosion-resistant, and pressure-resistant stainless-steel tubing solutions. Simultaneously, fluctuating nickel and molybdenum prices are forcing manufacturers to optimize alloy compositions and adopt leaner procurement strategies to preserve margins. The market is also experiencing disruption from increasing competition between Asian low-cost producers and premium European specialty manufacturers, intensifying pricing pressure globally.

Automation and digital manufacturing technologies, including robotic welding, AI-driven quality inspection, laser cutting, and Industry 4.0-enabled production systems, are transforming operational efficiency and reducing defect rates across the value chain. Sustainability regulations in Europe and North America are accelerating adoption of recycled stainless steel, low-carbon melting technologies, and environmentally compliant production practices, creating a competitive divide between technologically advanced producers and conventional manufacturers. Geopolitical trade tensions, anti-dumping duties, and regional localization policies are shifting global supply networks and encouraging localized production hubs in India, Southeast Asia, and the Middle East. Additionally, emerging substitute materials such as composite piping systems and advanced polymer-based industrial fittings are challenging stainless-steel adoption in selected low-pressure applications. However, stainless steel continues to maintain strong long-term relevance due to its durability, recyclability, temperature resistance, and suitability for critical industrial environments.

BCG Matrix: Company Evaluation

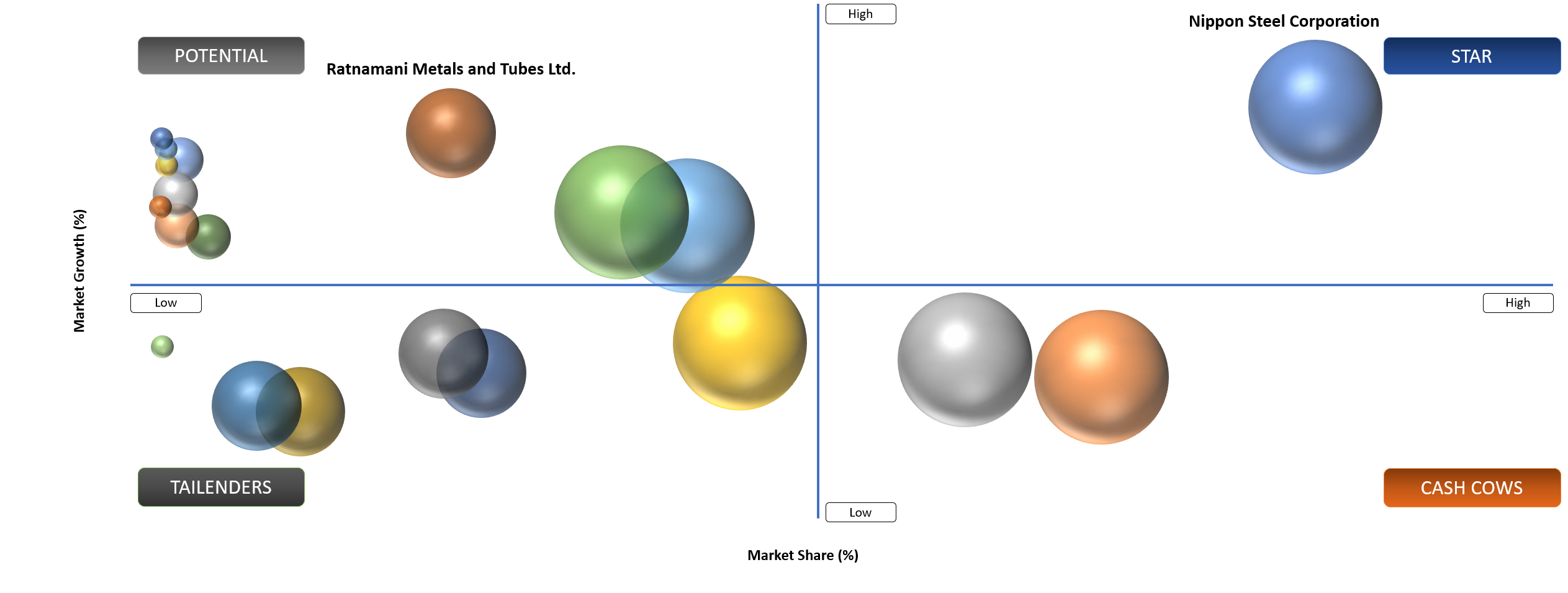

STAR

The stars segment in the global stainless-steel tubes and fittings market is dominated by globally integrated manufacturers with strong technological capabilities, diversified end-user penetration, and extensive distribution networks. Companies such as Nippon Steel Corporation, Sandvik AB, Tubacex, and Outokumpu maintain leadership due to their advanced corrosion-resistant alloy portfolios, precision tube manufacturing expertise, and strong positioning in energy, chemical processing, desalination, and hydrogen infrastructure projects. The companies benefit from rising demand for high-performance seamless stainless-steel tubing in offshore oil & gas, semiconductor manufacturing, and clean energy systems. The competitive advantage is strengthened through automation investments, vertically integrated steel production, long-term EPC partnerships, and compliance with stringent international certifications, including ASTM, ASME, and PED standards.

POTENTIAL

Potential players in the global stainless-steel tubes and fittings market consist primarily of regional manufacturers and emerging specialty alloy producers expanding aggressively into high-growth industrial applications. Companies including Ratnamani Metals & Tubes Ltd., Venus Pipes & Tubes Ltd., Pennar Industries, and Tsingshan Holding Group are increasingly strengthening their global competitiveness through capacity expansion, export-focused strategies, and investments in precision tubing technologies. The firms are gaining traction in pharmaceutical processing, food-grade piping, green hydrogen transportation, and industrial automation applications where demand for customized stainless-steel solutions is accelerating. Relatively lower production costs, expanding domestic infrastructure opportunities, and rapid adoption of automated welding and finishing technologies create significant growth potential.

Stainless-Steel Tubes and Fittings Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

Rising Investments in Industrial Infrastructure and Process Manufacturing Expansion | 5.20% | Asia-Pacific, Middle East, and North America industrial manufacturing hubs | Process piping systems, refinery operations, chemical transportation networks, industrial fluid handling | Accelerates demand for corrosion-resistant stainless-steel tubes and fittings across large-scale industrial projects |

Expanding Oil & Gas, Petrochemical, and Energy Sector Projects | 4.90% | Middle East, U.S., China, and offshore energy production regions | Pipeline systems, offshore platforms, LNG infrastructure, and high-pressure fluid transfer | Strengthens long-term consumption of high-grade stainless-steel tubing solutions for harsh operating environments |

Increasing Adoption in Food Processing, Pharmaceuticals, and Water Treatment Industries | 4.40% | Europe, North America, and rapidly urbanizing Asian economies | Hygienic fluid transfer systems, sanitary processing lines, purified water distribution | Enhances demand for precision-engineered stainless-steel fittings compliant with stringent hygiene and safety standards |

Growing Construction of Commercial Buildings

and Smart Urban Infrastructure | 4.10% | India, Southeast Asia, GCC countries, and urban redevelopment clusters | HVAC systems, plumbing networks, fire protection systems, structural piping applications | Supports higher penetration of durable and low-maintenance stainless-steel piping solutions in modern infrastructure projects |

Growing Investments in Energy and Process Industries

The stainless-steel tubes and fittings market is expanding rapidly because global energy and process industries are undergoing large-scale capacity additions and modernization programs. Oil & gas companies, petrochemical operators, LNG developers, and chemical manufacturers are investing heavily in high-temperature and high-pressure piping systems where stainless steel provides superior operational reliability. According to the International Gas Union, global LNG trade surpassed 401 million tonnes in 2023, while multiple LNG export terminals and regasification projects are under construction across the United States, Qatar, and Southeast Asia, significantly boosting demand for cryogenic-grade stainless-steel tubes and fittings.

The global refining and petrochemical industry are also increasing capital expenditures on facility upgrades to comply with stricter environmental regulations and improve operational efficiency. Stainless-steel tubing systems are increasingly replacing traditional alloy materials in refinery heat exchangers, instrumentation systems, process pipelines, and offshore drilling operations because they reduce maintenance costs and improve lifecycle performance under corrosive operating conditions.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

Volatility in Nickel and Chromium Raw Material Prices | 4.30% | Manufacturing cost structure and procurement stability | Industrial piping systems, construction-grade fittings and process equipment manufacturing | Increases pricing pressure across the supply chain and reduces profit margins for manufacturers and distributors |

Intense Competition from Low-Cost Carbon Steel and Plastic Alternatives | 3.90% | Product substitution in cost-sensitive industries | Water distribution systems, low-pressure industrial applications and residential plumbing | Limits stainless-steel penetration in price-driven markets and slows volume expansion in emerging economies |

High Energy Consumption and Production Costs in Stainless-Steel Manufacturing | 4.10% | Operational expenditure and production scalability | Seamless tube manufacturing, heavy industrial fittings production and refinery-grade applications | Reduces manufacturing competitiveness and creates pricing challenges amid fluctuating energy markets |

Supply Chain Disruptions and Limited Availability of High-Grade Stainless-Steel Alloys | 3.70% | Raw material sourcing and delivery timelines | Oil & gas infrastructure, chemical processing plants and offshore installations | Delays project execution timelines and increase dependency on regional alloy suppliers and imports. |

Raw Material Price Volatility and Energy-Intensive Production Challenges

A major challenge impacting the global stainless-steel tubes and fittings market is the volatility in nickel, chromium, and molybdenum prices, which directly affects production costs and profit margins for manufacturers. Stainless-steel production remains highly energy-intensive, and fluctuations in electricity and natural gas prices continue to pressure operating economics, particularly in Europe and Asia. According to the World Bank commodity outlook, nickel prices experienced significant fluctuations between 2022 and 2024 due to geopolitical disruptions, export restrictions, and changing battery-sector demand dynamics.

Manufacturers are also facing growing regulatory pressure regarding industrial emissions and carbon intensity. The World Steel Association stated that the steel sector accounts for approximately 7-9% of global direct fossil fuel emissions, forcing stainless-steel producers to invest heavily in electric arc furnaces, recycling systems, low-carbon alloys, and energy-efficiency upgrades. Smaller tubing manufacturers often struggle to absorb these modernization costs, particularly in developing regions where financing availability remains limited. In addition, global trade restrictions, anti-dumping measures, and import tariffs on steel products continue to create supply-chain uncertainties and procurement risks for downstream industrial buyers.

Segmentation Analysis

The global stainless-steel tubes and fittings market is segmented based on the Product, Steel Grade, Size, End-User and region.

Oil and Gas Industry Leads Market Demand

The oil and gas industry remains one of the largest consumers of stainless-steel tubes and fittings globally due to the sector’s requirement for high-strength, corrosion-resistant, and temperature-resistant piping systems. Stainless-steel tubes are extensively used in offshore platforms, subsea pipelines, refineries, gas processing plants, LNG facilities, and instrumentation systems exposed to highly corrosive environments. According to the U.S. Energy Information Administration (EIA), global liquid fuels consumption exceeded 102 million barrels per day in 2024, supporting continued investments in upstream and midstream infrastructure that require advanced stainless-steel piping solutions.

Offshore developments are further strengthening demand for duplex and super duplex stainless-steel fittings because these materials provide excellent resistance to seawater corrosion and chloride stress cracking. Brazil, Guyana, Norway, and the Gulf region continue expanding offshore exploration and production activities, increasing the installation of stainless-steel flowlines, heat exchangers, and hydraulic control tubing systems. In addition, carbon capture and storage (CCS) projects linked to oil and gas decarbonization initiatives are creating new opportunities for specialized stainless-steel process piping capable of handling high-pressure CO₂ transport systems.

Water Treatment and Desalination Applications Gain Momentum

The growing need for safe water infrastructure and wastewater management is significantly accelerating the use of stainless-steel tubes and fittings in municipal and industrial treatment systems. Stainless steel is increasingly preferred in desalination facilities, filtration plants, chemical dosing systems, and wastewater recycling projects because of its durability and resistance to corrosion in saline and chemically aggressive environments. According to the United Nations World Water Development Report, global water demand is projected to increase by nearly 30% by 2050, encouraging governments to invest aggressively in resilient water infrastructure.

The Middle East remains a major growth center for desalination investments. Saudi Arabia, the UAE, and other Gulf countries are expanding large-scale seawater desalination capacity to support urbanization and industrial growth. The International Desalination Association reported that over 21,000 desalination plants are operational globally, with many next-generation facilities utilizing stainless-steel piping networks to improve operational reliability and reduce maintenance requirements. India is also expanding wastewater recycling and industrial water reuse projects under national urban development programs, increasing demand for stainless-steel fittings across municipal treatment infrastructure.

Geographical Penetration

U.S. Stainless-Steel Tubes and Fittings Market Landscape

The United States stainless-steel tubes and fittings market is being driven by rising investments in energy infrastructure modernization, semiconductor manufacturing expansion, pharmaceutical processing capacity, and industrial reshoring initiatives. Demand for corrosion-resistant stainless-steel piping systems has accelerated across LNG terminals, hydrogen infrastructure, chemical processing facilities, and high-purity food and beverage production plants. According to the U.S. Department of Energy, more than USD 70 billion has been allocated toward grid modernization, clean hydrogen hubs, carbon capture infrastructure, and industrial decarbonization programs under recent federal energy transition initiatives, creating strong demand for stainless-steel tubing systems capable of operating under high pressure and corrosive conditions. The U.S. Environmental Protection Agency has also tightened industrial water treatment and emissions standards, increasing the use of stainless-steel fittings in wastewater treatment facilities and chemical handling systems. Stainless-steel tube manufacturers are also benefiting from the expansion of pharmaceutical manufacturing and biotechnology investments, particularly in aseptic processing and sterile fluid transfer systems where 316L stainless steel remains a preferred material standard.

Oil and gas pipeline replacement projects across Texas, Louisiana, and the Gulf Coast are expanding the use of stainless-steel fittings for sour gas handling, offshore processing, and LNG export terminals. According to the U.S. Energy Information Administration, U.S. LNG export capacity continues to expand through multiple Gulf Coast terminal developments, many of which require large-scale deployment of corrosion-resistant piping systems. The food processing industry is also contributing significantly to market demand, as the U.S. Department of Agriculture reported continued investments in hygienic food manufacturing facilities and automated processing lines. The rise of hydrogen transportation infrastructure and carbon capture projects is increasing adoption of duplex and super duplex stainless-steel tubes due to their superior pressure resistance and durability. Domestic producers are increasingly investing in automation, laser welding, and precision forming technologies to improve dimensional accuracy and meet stringent ASME and ASTM industrial standards.

Japan Stainless-Steel Tubes and Fittings Market Outlook

Japan’s stainless-steel tubes and fittings market is expanding steadily due to advanced industrial manufacturing, hydrogen energy development, semiconductor fabrication growth, and modernization of chemical processing facilities. Japan remains one of the world’s leading stainless-steel producing nations, supported by strong industrial groups and high-value engineering sectors. According to the Japan Iron and Steel Federation, Japan produced over 84 million metric tons of crude steel in 2024, while specialty stainless-steel production remained essential for automotive, electronics, and industrial fluid handling applications.

The country’s focus on hydrogen adoption is significantly strengthening demand for high-performance stainless-steel tubing systems capable of handling high-pressure hydrogen transport and storage. Japan’s Ministry of Economy, Trade and Industry has continued to invest heavily in hydrogen supply chain projects, fuel-cell systems, and ammonia co-firing infrastructure, all of which require corrosion-resistant stainless-steel piping solutions. In semiconductor manufacturing, Japan has also increased investments in advanced chip production and materials processing. The Japanese government announced multi-billion-dollar support packages for semiconductor fabrication and supply-chain resilience, accelerating installation of ultra-high purity stainless-steel process tubes and fittings in cleanroom manufacturing environments.

Another major trend influencing the market is Japan’s aging industrial infrastructure replacement cycle and growing emphasis on disaster-resilient engineering systems. Stainless-steel tubes are increasingly being deployed in seismic-resistant piping systems, high-rise buildings, industrial automation plants, and advanced wastewater treatment facilities. According to Japan’s Ministry of Land, Infrastructure, Transport and Tourism, substantial public infrastructure spending continues to target industrial water systems, transportation upgrades, and resilient urban utilities.

Japan’s chemical processing and pharmaceutical sectors are also adopting advanced stainless-steel sanitary fittings to comply with stricter contamination-control requirements and precision manufacturing standards. Additionally, Japanese automakers are expanding hydrogen fuel-cell vehicle development, increasing demand for seamless stainless-steel tubing in fuel delivery systems and thermal management applications. The market is also benefiting from Japan’s technological leadership in precision metallurgy and high-grade alloy manufacturing, particularly in duplex stainless steel and heat-resistant stainless alloys. Manufacturers are integrating robotic welding, automated inspection systems, and digitally monitored production lines to enhance product quality, reduce defects, and support high-performance industrial applications across energy, marine, and electronics industries.

China Stainless-Steel Tubes and Fittings Market Trends

China remains one of the most influential markets for stainless-steel tubes and fittings due to its enormous industrial manufacturing base, infrastructure expansion, petrochemical investments, and clean energy deployment. According to the World Stainless Association, China accounts for the majority of global stainless-steel production and consumption, supported by large-scale industrialization and continuous infrastructure development. The country’s petrochemical, refining, and chemical processing sectors continue to invest heavily in high-capacity production facilities requiring corrosion-resistant stainless-steel piping systems.

China’s National Development and Reform Commission has also accelerated investments in hydrogen energy infrastructure, LNG terminals, and industrial decarbonization projects, all of which require advanced stainless-steel tubes capable of operating under high-pressure and temperature conditions. In addition, China’s rapid semiconductor manufacturing expansion is increasing demand for ultra-high purity stainless-steel tubing used in cleanroom fabrication environments. The government’s strategic focus on domestic semiconductor self-sufficiency has resulted in large-scale investments in advanced manufacturing facilities, significantly supporting industrial stainless-steel consumption.

China continues to invest aggressively in municipal wastewater treatment, desalination facilities, and district heating networks where stainless-steel fittings provide superior durability and corrosion resistance. The country’s renewable energy sector is also supporting market growth, particularly through offshore wind projects, solar manufacturing facilities, and battery production plants. According to the International Energy Agency, China remains the world’s largest investor in clean energy infrastructure, creating sustained demand for industrial-grade stainless-steel components across energy supply chains.

China’s shipbuilding and marine engineering sectors are increasingly adopting duplex stainless-steel tubes for offshore platforms and marine transport systems exposed to harsh saline environments. Domestic manufacturers are heavily investing in automated rolling mills, precision welding technologies, and advanced alloy development to improve export competitiveness and product quality. The integration of digital manufacturing systems and smart factory technologies is also strengthening production efficiency and supporting the country’s leadership in global stainless-steel industrial supply chains.

Competitive Landscape

- The global stainless-steel tubes and fittings market is highly competitive and characterized by the presence of integrated steel manufacturers, specialty alloy producers, precision tubing companies, and industrial piping solution providers.

- Companies compete based on product quality, alloy specialization, corrosion resistance performance, pressure-handling capability, fabrication precision, and global supply-chain capabilities.

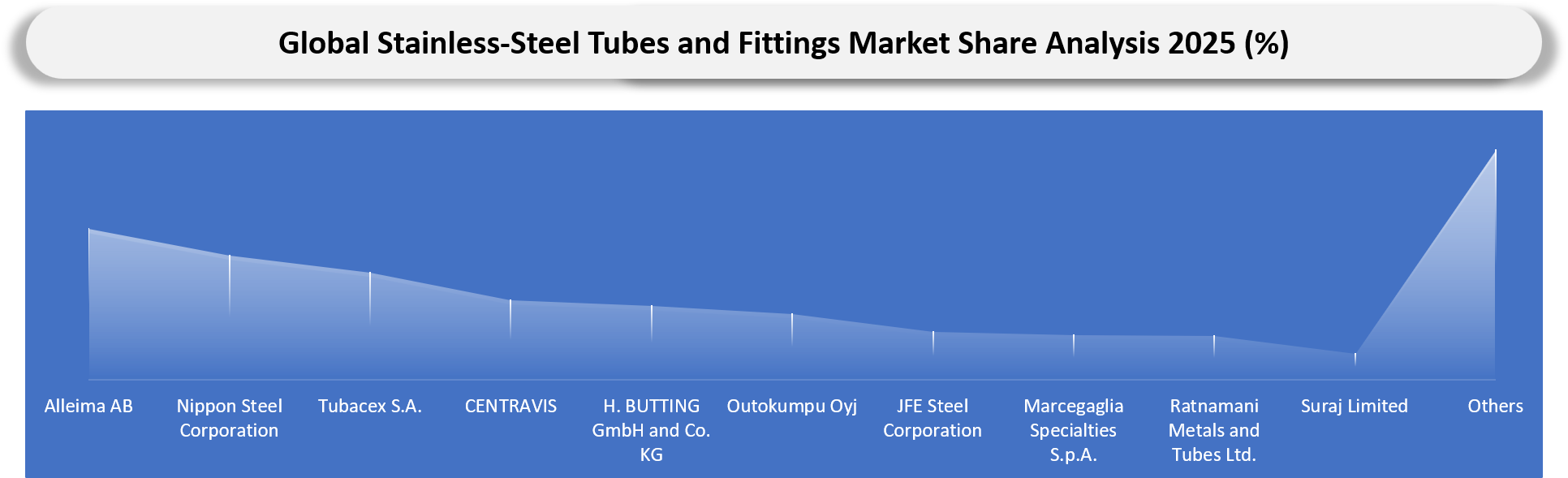

- Key players include Outokumpu, Acerinox, Nippon Steel Corporation, Sandvik, Tubacex, Tenaris, Ratnamani Metals & Tubes Ltd., Jindal Stainless, Plymouth Tube Company, Vallourec, and Alleima.

- Manufacturers are increasingly investing in low-carbon stainless-steel production, precision seamless tubing technologies, digital quality-control systems, and high-performance alloys designed for hydrogen, offshore, pharmaceutical, and semiconductor applications.

- Strategic focus areas include recycled stainless-steel utilization, electric arc furnace expansion, advanced welding technologies, and development of high-purity tubing systems capable of meeting stringent industrial safety and environmental standards.

Growing investments in hydrogen-ready infrastructure, offshore renewable energy systems, and industrial decarbonization technologies are expected to further intensify innovation and competition across the stainless-steel tubes and fittings industry over the coming decade.

MAJOR PAIN POINTS

- Volatility in nickel, chromium, and molybdenum prices is creating unpredictable raw material procurement costs and reducing profit margins for stainless-steel tube and fitting manufacturers.

- Intense pricing competition from low-cost Asian manufacturers, particularly from China and Southeast Asia, is pressuring global suppliers to reduce pricing and compress operating margins.

- High energy consumption during stainless-steel melting, extrusion, welding, and finishing processes is increasing production costs amid rising global electricity and gas tariffs.

- Supply chain disruptions affecting steel billets, scrap stainless steel, alloying materials, and logistics networks are causing delays in project execution and contract fulfillment.

- Stringent environmental regulations related to carbon emissions, wastewater discharge, and industrial waste management are increasing compliance costs for manufacturers across Europe and North America.

- Counterfeit and substandard stainless-steel fittings in developing markets are negatively impacting brand reputation, operational safety, and customer trust across industrial applications.

- Slower capital expenditure in oil & gas, petrochemical, and construction sectors during economic downturns is reducing large-volume demand for industrial-grade stainless-steel tubes and fittings.

- Technical challenges associated with corrosion resistance, high-pressure tolerance, and weld integrity in harsh industrial environments are increasing quality assurance and testing expenses.

- Growing substitution from composite pipes, plastic piping systems, and advanced alloy materials in selected applications is limiting market penetration in cost-sensitive industries.

Trade restrictions, anti-dumping duties, and geopolitical tensions affecting global steel trade flows are creating uncertainty in international procurement and export operations for manufacturers.

RECENT DEVELOPMENTS

- April 2026: Alleima AB reported Q1 2026 resilience, despite weaker demand, maintaining advanced stainless-steel tubing deliveries across energy and aerospace sectors.

- January 2026: Nippon Steel Corporation emphasized strengthening premium steelmaking capabilities amid global tariff pressures and declining Japanese crude-steel demand environment.

- February 2026: Tubacex S.A. confirmed Abu Dhabi plant commercialization, despite geopolitical project delays impacting 2025 earnings and stainless-tube contract execution globally.

- December 2025: Alleima AB expanded Mehsana manufacturing operations, introducing SAF 2906 and SAF 3006 high-performance stainless-steel grades locally in India.

- September 2025: Tubacex S.A. leveraged seven U.S. facilities to offset tariff risks while supporting nuclear, hydrogen, and carbon-capture projects growth.

- July 2025: Tubacex S.A. showcased Alloy 699 XA and Uremium 29 downstream solutions during Mumbai’s NextGen Conference 2025 industrial event.

- July 2025: Tubacex S.A. achieved €61 million EBITDA during first-half 2025, supported by premium stainless-tube backlog exceeding €1.4 billion globally.

April 2025: Tubacex S.A. recorded historic 17% EBITDA margin, maintaining €1.5 billion premium stainless-tubing order backlog across diversified industrial sectors.

ANALYST VIEW / OPINION

- Rising investments in industrial infrastructure modernization and process manufacturing expansion are accelerating demand for corrosion-resistant stainless-steel tubes and fittings across energy, chemicals, and water treatment sectors.

- Oil & gas pipeline upgrades and refinery capacity expansions in Asia-Pacific and the Middle East are strengthening long-term consumption of seamless and welded stainless-steel tubing solutions.

- Food processing, pharmaceutical, and biotechnology industries are increasingly adopting hygienic stainless-steel fittings due to stricter sanitation standards and contamination-control requirements.

- Demand for duplex and super duplex stainless-steel grades is growing rapidly because of their superior strength, pressure resistance, and durability in harsh industrial environments.

- Volatility in nickel, chromium, and molybdenum prices continues to create pricing pressure for manufacturers and impacts procurement strategies across the supply chain.

- Automation in tube manufacturing, laser welding, CNC bending, and precision fabrication technologies is improving production efficiency and reducing material wastage across the industry.

- Rapid urbanization and smart infrastructure projects are boosting the use of stainless-steel piping systems in commercial construction, HVAC systems, and municipal water distribution networks.

- Sustainability initiatives and increasing preference for recyclable industrial materials are positioning stainless steel as a preferred long-term solution over conventional carbon-steel alternatives.

- Consolidation among regional manufacturers and strategic partnerships with EPC contractors are intensifying competitive dynamics in large-scale industrial and infrastructure projects.

- Asia-Pacific is expected to remain the dominant production and consumption hub due to strong manufacturing activity, export-oriented steel production, and expanding industrial investment across China, India, and Southeast Asia.

TARGET AUDIENCE

| INDUSTRY | WHO SHOULD BUY THIS REPORT? | REASON TO BUY THIS REPORT |

| Stainless-Steel Tube Manufacturers | Production Heads, Plant Managers, Quality Control Teams | Analyze demand trends for seamless and welded stainless-steel tubes across industrial, construction, and process industries |

| Pipe Fittings Manufacturers | Product Development Teams, Operations Managers, Procurement Heads | Evaluate growth opportunities for elbows, tees, reducers, flanges, and customized stainless-steel fitting solutions |

| Oil & Gas Companies | Pipeline Engineering Teams, Reliability Engineers, Sourcing Managers | Assess stainless-steel tube and fitting demand for upstream, midstream, and downstream infrastructure projects |

| Chemical & Petrochemical Companies | Process Engineers, Maintenance Heads, Industrial Procurement Teams | Understand corrosion-resistant tubing and fitting requirements for aggressive chemical processing environments |

| Power Generation & Energy Companies | Plant Engineering Teams, Turbine Operations Managers, EPC Procurement Teams | Analyze high-pressure stainless-steel piping and fitting applications in thermal, nuclear, and renewable energy plants |

| Construction & Infrastructure Companies | Project Management Teams, MEP Engineers, Infrastructure Procurement Departments | Evaluate stainless-steel tube and fitting demand in commercial buildings, metro projects, airports, and smart city infrastructure |

| Food & Beverage Processing Companies | Hygienic Equipment Engineers, Operations Managers, Compliance Teams | Study sanitary-grade stainless-steel tubing and fittings for food processing, dairy, and beverage production systems |

| Pharmaceutical & Biotechnology Companies | Cleanroom Engineering Teams, Validation Managers, Manufacturing Operations Teams | Assess demand for precision stainless-steel tubes and fittings in sterile manufacturing and high-purity fluid transfer systems |

| Automotive & Transportation Manufacturers | Exhaust System Engineers, Manufacturing Teams, Component Sourcing Managers | Analyze stainless-steel tubing applications in exhaust systems, fuel lines, structural components, and EV thermal management systems |

| EPC Contractors & Industrial Fabricators | Project Engineers, Industrial Design Teams, Strategic Procurement Departments | Identify regional demand trends, project-based opportunities, and material sourcing strategies for industrial piping systems |

Economic & Investment Analysis

The Stainless Steel Tubes and Fittings Market represents a strategically significant segment of the global industrial materials ecosystem, underpinned by sustained investments in energy infrastructure, manufacturing capacity expansion, and large-scale industrial modernization. Growing demand for corrosion-resistant, durable, and high-performance piping systems across critical sectors continues to strengthen the market outlook. Industries such as oil & gas, chemical processing, power generation, pharmaceuticals, food & beverage, construction, and water treatment are increasingly prioritizing stainless steel solutions due to their long lifecycle performance, safety compliance, and operational efficiency.

From an investment perspective, the market offers attractive long-term opportunities driven by infrastructure development programs, urbanization, and global energy transition initiatives. The report provides a structured evaluation of market size, growth trajectories, pricing dynamics, supply-demand balance, and regional investment hotspots. It also highlights macroeconomic and industrial factors shaping market performance, enabling stakeholders to make informed strategic decisions.

Key Economic & Investment Insights:

- Increasing global investments in energy, water treatment, and industrial infrastructure projects

- Rising demand for corrosion-resistant and high-durability piping systems across core industries

- Strong growth potential in emerging economies driven by rapid industrialization and urban expansion

- Influence of raw material price volatility (nickel, chromium, and stainless steel alloys) on profitability

- Expansion of downstream industries such as oil & gas, chemicals, pharmaceuticals, and food processing

- Shift toward sustainable and long-life industrial materials supporting replacement demand cycles

- Growing opportunities in EPC contracts, large-scale infrastructure projects, and industrial upgrades

- Regional diversification of manufacturing hubs across Asia-Pacific, particularly India and China

- Increasing adoption of advanced stainless steel grades for high-pressure and critical applications

- Attractive investment potential supported by long-term industrial demand stability and infrastructure spending cycles

Who Should Buy This Report?

This report is designed for decision-makers seeking actionable market intelligence and strategic insights into the Stainless Steel Tubes and Fittings industry, including:

- Manufacturers and producers of stainless steel tubes, pipes, and fittings.

- Raw material suppliers, distributors, and supply chain participants.

- Investment firms, private equity investors, and financial institutions evaluating market opportunities.

- Business development managers and corporate strategists exploring expansion initiatives.

- Procurement and sourcing professionals seeking supplier and pricing intelligence.

- Engineering, procurement, and construction (EPC) companies involved in industrial infrastructure projects.

- Oil & gas, chemical, power generation, water treatment, pharmaceutical, and food processing companies assessing procurement trends.

- Market research professionals, consultants, and industry analysts requiring reliable market forecasts and competitive benchmarking.

- Government agencies, trade associations, and policy-makers monitoring industrial growth and infrastructure development.

The report equips stakeholders with data-driven insights to support investment decisions, market entry strategies, partnership evaluations, capacity expansion planning, and long-term business growth initiatives.

WHY CHOOSE DATAM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

WHAT DATAM UNIQUELY PROVIDES

- Real-time refinery, LNG, hydrogen, and desalination project-linked demand mapping across stainless-steel tube consumption clusters.

- Deep-dive procurement intelligence covering EPC contractor sourcing preferences, alloy specifications, and supplier qualification trends.

- Country-level regulatory benchmarking including CBAM exposure, BIS mandates, ASTM compliance, and localization policy impact analysis.

- Advanced pricing intelligence integrating nickel surcharge behavior, freight volatility, and regional stainless conversion cost trends.

- Competitive benchmarking across seamless, welded, duplex, and corrosion-resistant alloy stainless tube manufacturers globally.

- AI-driven supply-chain disruption tracking covering raw-material bottlenecks, geopolitical shipping risks, and inventory optimization insights.

- Integrated import-export intelligence with HS-code level trade flow evaluation and strategic sourcing opportunity identification.