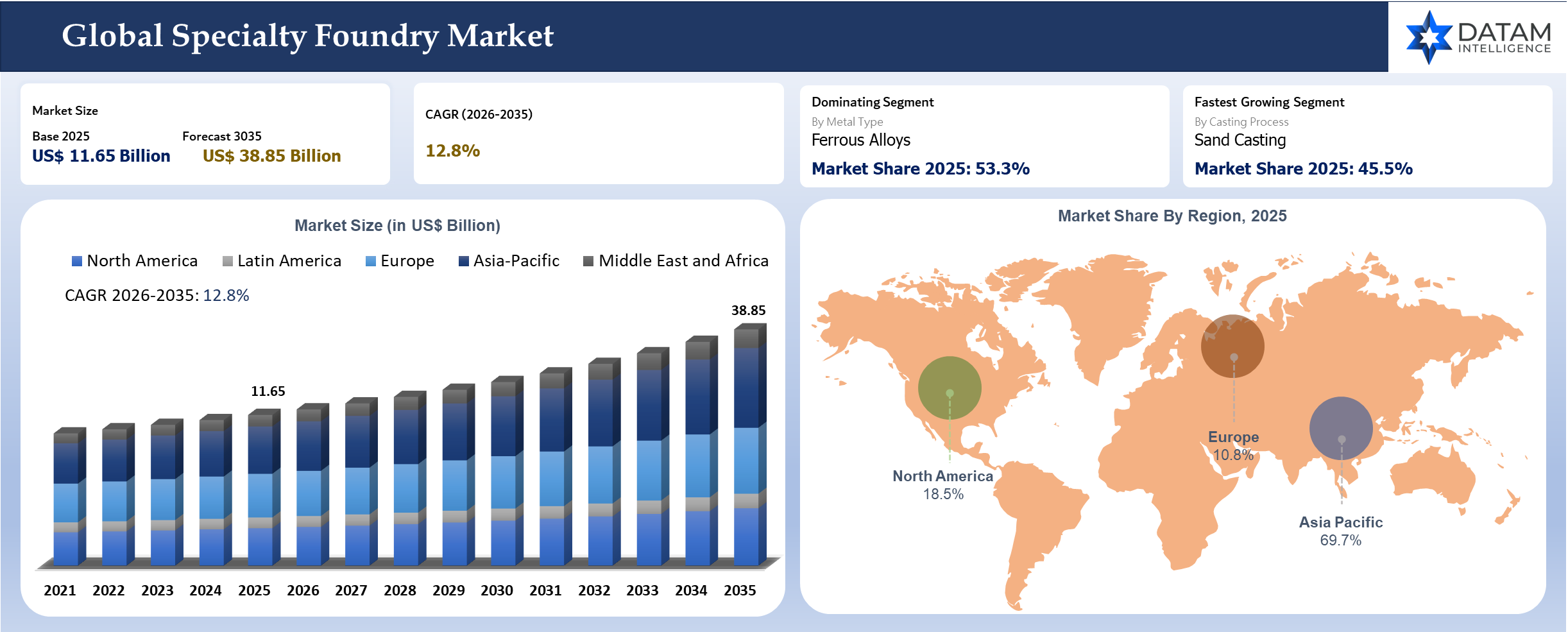

Specialty Foundry Market Size

The global specialty foundry market size reached US$ 11.65 billion in 2025 and is expected to reach US$ 38.85 billion by 2035, growing with a CAGR of 12.8% during the forecast period 2026-2035. Specialty foundries operate in mature process technologies like analog, mixed signal, radio frequency (RF), power semiconductors, micro-electromechanical systems (MEMS) and embedded non-volatile memories. Specialty foundries have a crucial role because of the demand for reliable and customized products with a high lifecycle. Electric vehicles, 5G and Internet of Things (IoT) applications will increase the need for power semiconductors and sensors.

The specialty foundry industry is likely to grow due to increased demand from IDMs and fabless players, looking for flexible production partners for legacy and specialty technologies. Innovations in compound semiconductors (like gallium nitride (GaN) and silicon carbide (SiC)) and MEMS sensors and innovations in RF front-end modules underscore the need for specialty fabrication environments. Increasingly, industries have begun focusing on energy efficiency and miniaturization, which makes specialty foundries an integral part of the electronics industry.

Specialty Foundry Industry Trends and Strategic Insights

- The value-demand for castings is increasingly favoring those that depend more on alloy control, dimensional consistency and certification than volume of metal melted.

- The aerospace, defense, medical and severe service industrial sectors have kept specialty foundries alive despite buyers' attempts to reduce order lead times.

- Process digitalization through control, simulation and traceability is now a commercial advantage, not internal efficiencies.

Specialty Foundry Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 11.65 Billion | |

| 2035 Projected Market Size | US$ 38.85 Billion | |

| CAGR (2026-2035) | 12.8% | |

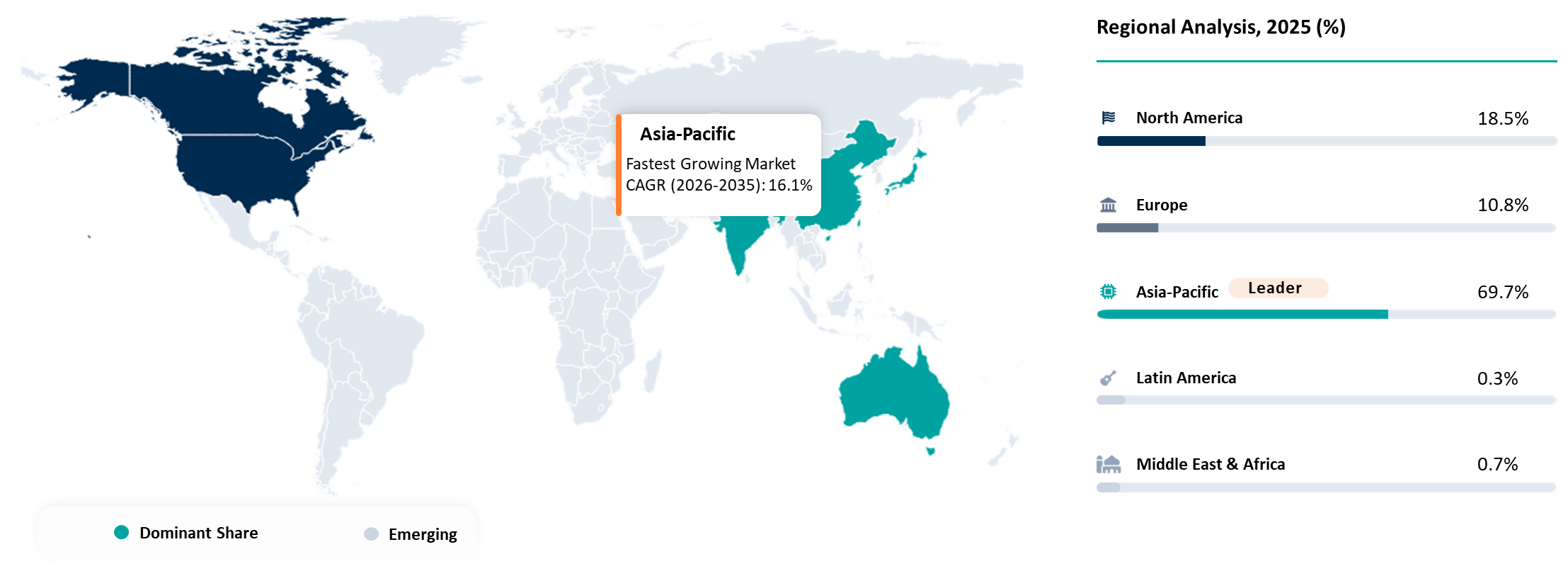

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Metal Type | Ferrous Alloys, Non-Ferrous Alloys, High Performance Alloys | |

| By Casting Process | Investment Casting, Sand Casting, Shell Molding, Lost Foam Casting, Centrifugal Casting, Vacuum Casting | |

| By Production Mode | Prototype and Short Run, Low Volume High Mix, Serial Production for Critical Components | |

| By Component Focus | Turbine and Hot Section Components, Pump and Valve Bodies, Wear Parts and Mill Liners, Medical and Dental Castings, Defense and Ammunition Components, Precision Industrial Components | |

| By Quality and Compliance | NADCAP Or Aerospace Qualified, Nuclear Qualified, Medical Grade, General Industrial Certified | |

| By Region | North America | USA, Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Specialty Foundry Market : Key Takeaways

- USD 38.85 billion is the 2035 market opportunity. The specialty foundry market is projected to expand from USD 11.65 billion in 2025, driven by rising demand for precision-engineered castings across aerospace, defense, medical, energy and industrial applications.

- Asia-Pacific remains the largest and fastest-growing market. Strong manufacturing ecosystems across China, India, Japan and South Korea, coupled with expanding aerospace, automotive and industrial production, continue to position the region as the global hub for specialty foundry operations.

- Investment casting is becoming the benchmark for high-value manufacturing. Demand is shifting toward processes that deliver complex geometries, thin-wall structures, tight dimensional tolerances and minimal post-machining for mission-critical components.

- Process digitalization is redefining competitive advantage. Simulation software, real-time process monitoring, digital work instructions and traceability systems are improving repeatability, quality assurance and production efficiency across specialty foundries.

- Advanced alloys are driving premium foundry demand. Growing adoption of high-performance ferrous, non-ferrous and specialty alloys is supporting applications that require superior heat resistance, corrosion protection, lightweight performance and long operational lifecycles.

- Reshoring and supply chain resilience are influencing sourcing strategies. Manufacturers are increasingly prioritizing domestic and allied-country foundry capacity to reduce geopolitical risks, shorten lead times and secure reliable supply for critical industries.

- Certification and engineering expertise are becoming key differentiators. Aerospace, medical, nuclear and defense customers increasingly value foundries with advanced metallurgical capabilities, regulatory certifications and consistent dimensional accuracy over high-volume production alone.

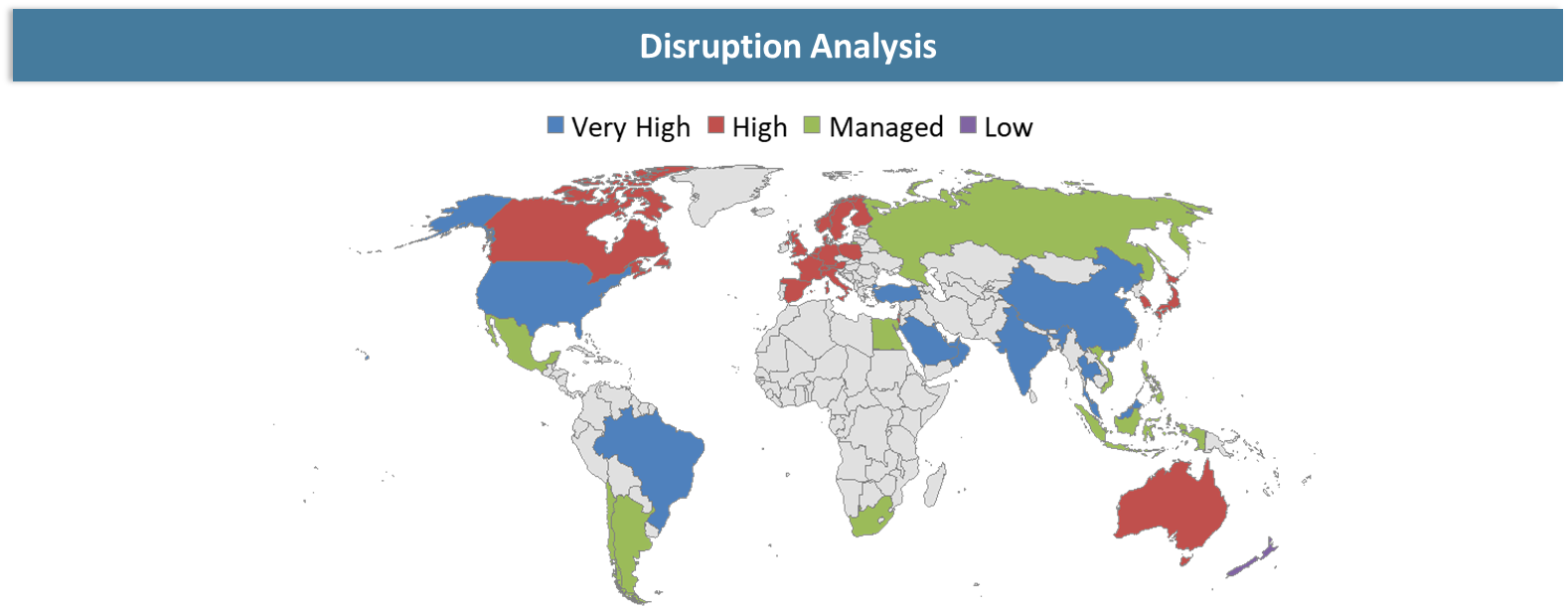

Disruption Analysis

While specialty foundries have always operated with skilled labor, purchasers now require repeatability that can weather retirements, night shifts and relocation between facilities. It alters strategic investments. Foundries are investing in simulations, process controls, data acquisition and digital work instructions since there is less consumer patience for non-quantifiable process variances. Supply chain disruptions and national security-driven reshoring have made the availability of domestic or partner-country casting capacity increasingly critical for selecting casting applications. Consumers desire near-net-shape parts that minimize material waste and machining time in subsequent processes. It benefits foundries with a greater engineering focus and greater certainty in dimensioning repeatability. Casting bids are also impacted, since their economic benefit no longer stops at the foundry gate but is extended into the consumer’s post-processing and assembly efficiency.

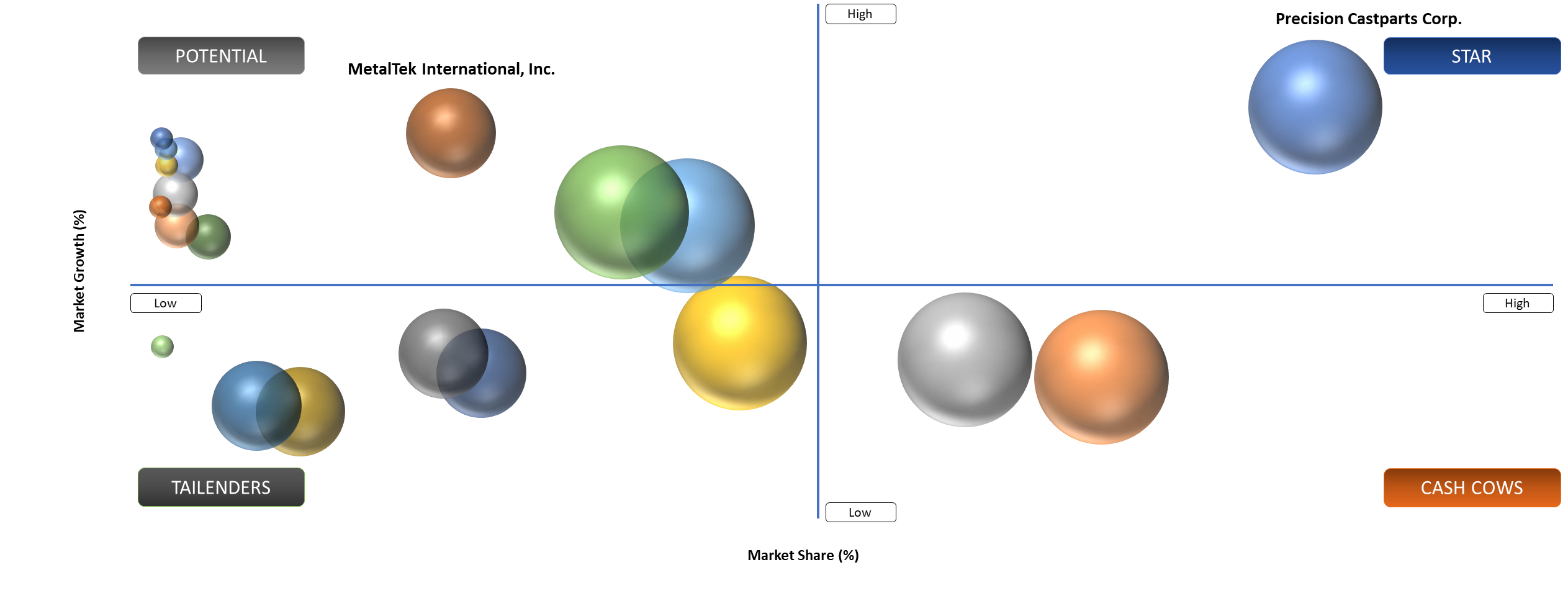

BCG Matrix: Company Evaluation

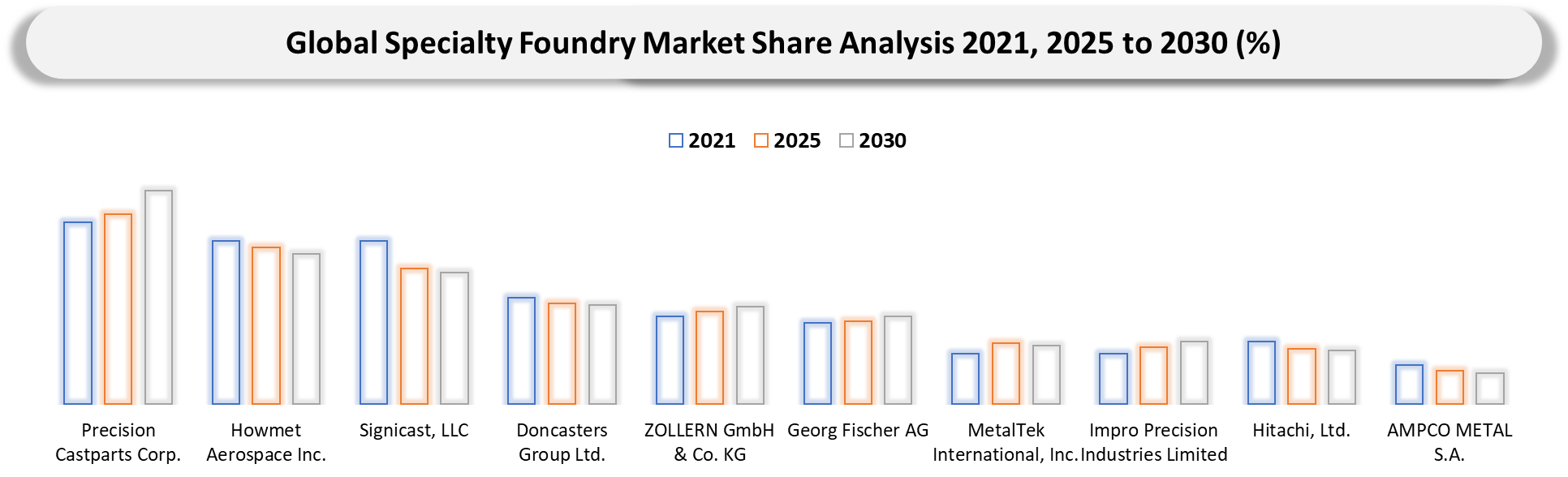

Precision Castparts Corp., Howmet Aerospace Inc. and Impro Precision Industries Limited stand out as the most credible Stars because they combine technical capabilities with the ability to provide access to lucrative programs and efficient manufacturing processes. The Stars are the most apparent at places where there are challenges related to technical complexity, customer qualification and repetitive capability requirements. The Potentials are resilient against market conditions since the companies benefit from repeat business through existing customer relationships, despite uneven growth in new programs. The Question Marks are technically credible and can capitalize on material strengths or forging-related capabilities, but they require better positioning within the foundries in premium casting programs.

Specialty Foundry Market Dynamics

Qualification-heavy industries are consolidating demand around foundries that can prove repeatability on difficult alloys.

Aerospace turbines, defense products, castings for severe service pumps and valves, medical devices and precision wear components all have metallurgical consistency requirements and process traceability. In such cases, when the foundry gets approved, it becomes a permanent fixture within their production process. It generates a high level of stickiness because changing suppliers is costly. The buyer will need new first article approval, destructive testing, metallurgy tests and revised machining assumptions if he decides to switch his specialty casting supplier. Such foundries have an upper hand compared to general job shops. The good thing is that foundries that get placed into such programs will have volumes even in industrial recessions. Specialty alloy castings like nickel-based superalloys, titanium castings and stainless and bronze castings with tight tolerances require knowledge that is not quickly acquired. It makes customers ready to favor capability over cost.

Skilled labor tightness and alloy yield losses continue to cap profitable expansion.

Burdens of shortages in skilled foundry personnel and costliness of process waste. The casting of specialty parts does not follow a simple rule of more time in the furnace producing more parts. The process requires skill in pattern making, shell handling, metal processing, inspection procedures and problem-solving skills that cannot be easily duplicated. If the skilled labor pool is too shallow, yields may fall and deliveries may be less reliable. Super-alloys, specialty stainless steels, titanium and precise tooling use up a lot of cash flow at the very beginning of the manufacturing process. Waste of scrap and rework on these types of projects will eliminate profit margins fast.

Specialty Foundry Market Segmentation Analysis

The global specialty foundry market is segmented based on the metal type, casting process, production mode, component focus, quality, compliance and region.

Process Selection Drives Precision Value Creation in the Specialty Foundry Market

Process choice is the most informative framework in analyzing this market because it determines all of the factors involved, including tolerance capacity, alloy compatibility, tooling cost-efficiency, production lead-time and machining requirements further down the line. Investment Casting claims top billing whenever a client demands intricate geometry, thin walls, high tolerances and reduced machinability. It delivers the highest value for aerospace hardware, medical device components, valve internal parts, instruments and instrumentation assemblies and engineering industrial products. The benefit is not only geometrical; it lies in the fact that these parts can be supplied with minimal machining in expensive-to-machine alloys. After the validation of the tooling set and process conditions, the buyer acquires assurance in the reproducibility of these parameters. In regulated programs, this makes the choice very compelling. Foundries targeting this market compete in shell performance, gating, ceramic material properties and heat treat behavior rather than mere melting technology.

Geographical Penetration

Europe Specialty Foundry Market Driven by Precision Engineering, Sustainability Mandates and Industrial Decarbonization Initiatives

The specialty foundry market in Europe has several distinguishing features, such as emphasis on high precision engineering, sustainability and metallurgy, owing to its mature industrial sector comprising the automobile, aerospace and energy industries. The European specialty foundry market is known for emphasizing high precision engineering, sustainability and metallurgy, owing to its mature industrial sector comprising the automobile, aerospace and energy industries. In addition, regulations resulting from the decarbonization efforts of the EU, along with increased costs of energy, have driven growth in energy-efficient melting processes and the adoption of circular manufacturing processes. In this regard, the European Commission has been investing in industrial decarbonization and manufacturing innovation initiatives.

Germany Specialty Foundry Market Trends

Germany continues to be an important player in specialized foundries within Europe because of its strong automobile and engineering industry sectors. According to the German Foundry Institute, over 600 foundries are currently operating in Germany and are engaged in the production of top-quality cast products of iron, steel and non-ferrous materials. The shift towards electric vehicles and other energy-saving modes of transport is resulting in a greater demand for lightweight cast products made from aluminum and magnesium. The Fraunhofer Society, on the other hand, has been funding several research projects related to modern casting techniques, such as hybrid casting and 3D sand printing, at millions of euros per annum.

Italy Specialty Foundry Market Trends

Italian specialty foundries have become an integral part of automotive, machinery and industrial equipment supply chains, with special attention being paid to aluminum and lightweight alloys due to electric vehicles. Another characteristic feature of Italy’s foundry industry is its technical progress and export orientation. Clusters operating in regions such as Lombardy and Emilia-Romagna are introducing innovations such as automation, robotics and computer-controlled processes to improve accuracy and minimize production flaws. Collaboration with research centers and support from the European Union in terms of innovative programs aimed at applying new technologies, including 3D sand printing and hybrid manufacturing systems, is promoting further development within the sector.

Specialty Foundry Market Competitive Landscape

- Competitive environment centers on foundry groups and engineered castings firms capable of combining alloy expertise with process control, machining capabilities and certification experience. Precision Castparts Corp., Howmet Aerospace Inc., Impro Precision Industries Limited, Signicast, LLC and Doncasters Group Ltd. have an advantage since consumers here do not differentiate between metallurgical skills and paperwork or between quality and delivery efficiency. The competition thus depends as much on reliability and qualification assurance as on price.

- Specialists with regional expertise continue to carry weight if they have special alloy, geometry or application expertise. ZOLLERN GmbH & Co. KG, Georg Fischer AG, MetalTek International, Inc., Hitchiner Manufacturing Co., Inc. and Aubert & Duval S.A. have prominence since their niche relies on credibility in solving problems associated with particular casting families. More specifically, customers favor those who can accurately determine which jobs to pursue and which to shun. Poorly positioned players tend to be those with good foundry jargon but lack technical specialization.

Specialty Foundry Market Key Developments

- April 2026: Bühler Holding AG advanced precision casting technologies supporting industrial processing equipment, emphasizing digitalization and high-efficiency manufacturing solutions.

- March 2026: Bradken Pty Limited expanded mining-focused specialty casting production, enhancing supply of high-durability components for global resource extraction industries.

- March 2026: Bharat Forge Limited expanded casting and forging integration capabilities, targeting defense, automotive and industrial sectors with advanced lightweight and high-strength components.

- March 2026: ATI Inc. expanded specialty materials and casting capabilities, supporting aerospace and defense demand for high-strength, corrosion-resistant advanced alloys.

- March 2026: Georg Fischer AG advanced precision casting capabilities and digital manufacturing integration to improve efficiency and meet growing demand for complex industrial components globally.

- March 2026: Howmet Aerospace Inc. announced investment in advanced casting technologies and automation to enhance aerospace structural components manufacturing efficiency and reduce lead times.

- February 2026: Signicast, LLC enhanced automated precision casting lines, improving micro-component accuracy and supporting medical and electronics sector demand growth globally.

- January 2026: Precision Castparts Corp. expanded aerospace casting capacity for turbine components, strengthening superalloy production amid rising aircraft engine demand globally.

- January 2026: ZOLLERN GmbH & Co. KG focused on innovation in high-performance alloy casting technologies, targeting aerospace and industrial machinery applications requiring lightweight, durable components.

Why Choose DataM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

Target Audience

- Aerospace and Defense OEMs: Engine builders, airframe suppliers, defense platform manufacturers and ammunition program teams sourcing certified castings for critical components where failure risk is low tolerance and qualification history matters.

- Industrial Pump, Valve and Flow Control Companies: Severe-service equipment manufacturers seeking corrosion-resistant, pressure-capable and geometry-sensitive castings with traceable metallurgy and machining support.

- Medical Device and Surgical Instrument Manufacturers: Buyers of precision castings that need clean process control, dimensional consistency and material pedigree for regulated healthcare use.

- Foundry Buyers and Strategic Sourcing Teams: Procurement managers consolidating supplier bases around foundries that can combine design support, quality records and on-time delivery for critical parts.

- Materials Engineers and Casting Designers: Technical teams comparing alloy behavior, casting route selection and near-net-shape possibilities to reduce machining burden and improve part performance.

- Defense Logistics and Reshoring Program Managers: Public and private stakeholders evaluating domestic or allied casting capacity for resilient supply chains in mission-critical metal components.

- Industrial Investors and Private Equity Firms: Investors assessing foundry businesses that can defend margin through certification depth, technical specialization and sticky customer programs.

- Process Technology and Simulation Providers: Companies offering software, inspection systems, sensors and digital foundry tools that help premium foundries reduce defects and control repeatability.