Global Space Robotics Market Size

The Global Space Robotics Market reached US$ 5.65 billion in 2025 and is expected to reach US$ 12.99 billion by 2035, growing with a CAGR of 8.7% during the forecast period 2026-2035. Space project complexity and ambition drive deep space robotics industry demand. Governments and private companies heavily invest in missions to the Moon, Mars and beyond, which demand robots to perform planetary surface exploration, sample gathering and infrastructure building. Robots need to function autonomously in hostile, uncontrolled environments, driving innovation in AI, machine learning and robotic mobility.

For example, NASA's Artemis mission and ESA's lunar missions rely on robots to land on the moon and erect habitats. Furthermore, growing interest in asteroid mining and space resource exploitation fuels the demand for specialist robotics. As exploration missions reach further into space, the dependence on robots to accomplish the too dangerous or too impractical for human endeavors will continue to increase, solidifying the role of robotics in deep space exploration.

Space Robotics Industry Trends and Strategic Insights

North America dominates the market in the market, capturing the largest revenue share of 39.3% in 2025.

By end-user, the government segment is projected to experience the largest market, registering a significant 28.7% in 2025.

Market Size and Future Outlook

2025 Market Size: US$ 5.65 Billion

2035 Projected Market Size: US$ 12.99 Billion

CAGR (2026-2033): 8.7%

Largest Market: North America

Fastest Market: Asia-Pacific

Key Takeaways

- Space robotics spending is projected to more than double between 2025 and 2035, creating substantial opportunities across exploration, servicing, and orbital logistics applications.

- North America accounted for 39.3% of global revenue in 2025, supported by NASA programs, defense investments, and private sector innovation.

- Government organizations remain the largest buyers of space robotics systems, supported by growing budgets for lunar exploration, Mars missions, and national space programs.

- Asia-Pacific represents the fastest-growing regional opportunity as China, India, Japan, South Korea, and Australia expand robotic exploration capabilities.

- Satellite servicing is emerging as one of the most commercially attractive use cases, creating recurring service revenue opportunities through life-extension missions.

- AI-enabled autonomy is becoming a critical differentiator, allowing robots to navigate, inspect, repair, and construct assets with minimal human intervention.

- High development costs remain a significant barrier, favoring companies with proven spaceflight heritage, robust engineering capabilities, and long-term government partnerships.

Market Scope

| Metrics | Details |

| Market Size (2025) | US$ 5.65 Billion |

| Market Size (2035) | US$ 12.99 Billion (Calculated) |

| CAGR (2026-2035) | 8.70% |

| Historic Years | 2023-2024 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Segments Covered | Solution, Application, End User, Region |

| Leading Region | North America |

| Fastest Growing Region | Asia-Pacific |

Market Dynamics

Diver-Rising Adoption of Advanced Technologies

New technologies, like Artificial Intelligence (AI) and Deep Learning (DL), are being extensively implemented in the field of robotics. Some organizations are designing AI-enabled deep space robots that offer improved exploration advantages and increased mobility within space. Robots are able to work with minimum human intervention and carry out very intricate tasks for a longer time.

For example, in June 2023, the International Space Station (ISS) began to use a new device called Int-Ball, which was created by the Japan Aerospace Exploration Agency and operated & managed by a crew of JAXA ground controllers. The major aim of Int-Ball is to minimize photographing time; JAXA has created the JEM Internal Ball Camera ("Int-Ball") which autonomously travels to the target spatial position and takes videos/pictures of the target, with the goal of achieving zero photographing time by the crew.

Restraints-High Cost of Development and Deployment

One of the main constraints in the international deep space robotics industry is the excessive cost involved in the development, testing and deployment of space-grade robotic systems. Designing robots that are capable of withstanding hostile extraterrestrial environments-severe temperatures, radiation and delayed communications-calls for customized materials, high-precision engineering and stringent testing procedures.

The expenses are further augmented by launch costs, which can cost tens of millions of dollars per mission. The high capital costs restrict participation to well-funded government agencies and a handful of private companies, resulting in high barriers to entry for startups and new entrants. The financial burden tends to retard innovation cycles and limit wider adoption among international or commercial players.

Segmentation Analysis

The global space robotics market is segmented based on solution, application, end-user and region.

Rising Investments in Government Sector to Drive the Segment Growth

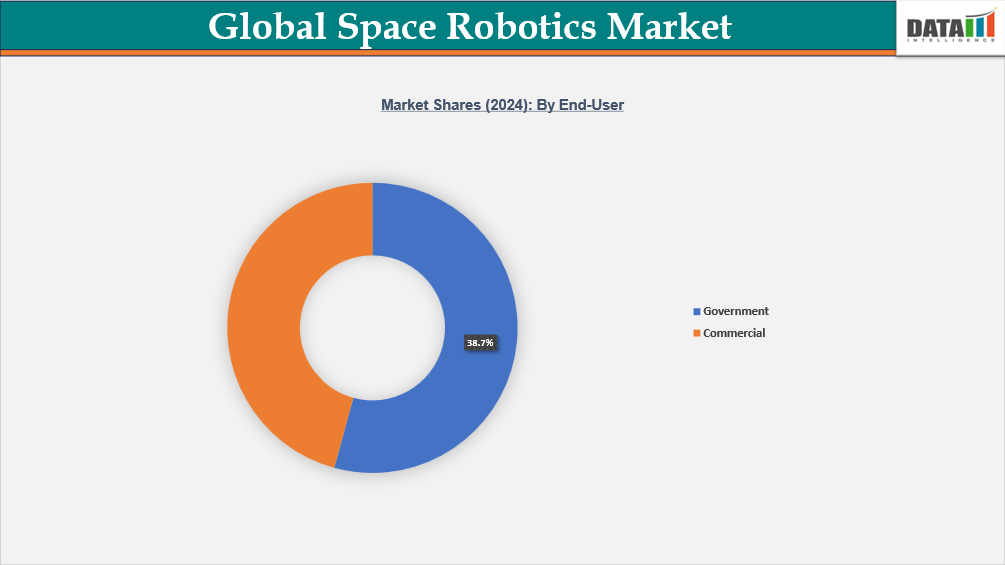

Government end-user is expected to hold about 38.7% of the global market in 2024. Government remains at the forefront of the industry as it is national space agencies such as NASA, ESA, Roscosmos, CNSA and ISRO that are the biggest spenders on space missions into the universe. Governments allocate large sums of money to interplanetary research; space station upkeep and planetary exploration and they demand the use of cutting-edge robotic technologies. Government investment in deep space robotics is further established by the growing focus on Mars exploration and asteroid mining due to growing interest in space security.

Additionally, governments are funding research and development in the fields of robotics and space. For example, in February 2023, India's union budget for 2023-2024 provisioned US$ 151.48 million for the Department of Space (DoS). It will aid the development of India's space program by initiating projects from launch vehicles and satellites to other development and operational ones.

Commercial Sector Has a Significant Growth Rate Due to the Expanding Private Companies

The commercial space robotics sector is quickly growing as private companies look for robotic solutions to cut costs, extend satellite lifecycles and enable new business models in space. One of the most obvious applications is satellite servicing, which employs robotic equipment for in-orbit inspection, refueling and repositioning. For example, Northrop Grumman's Mission Extension Vehicle (MEV-1 and MEV-2) successfully docked with Intelsat satellites, extending their operational lifetimes by more than 5 years and saving operators the expense of launching totally new spacecraft. This commercial proof-of-concept opens the door to service-based contracts in GEO and LEO, establishing recurrent income streams for robotic service providers.

Geographical Penetration

Rising Investments and Adoption of Technology in Asia-Pacific

Asia-Pacific is the fastest-growing region for space robotics, with strong contributions from China, India, Japan and other regional players. China leads the market, having demonstrated cutting-edge robotics in its Chang’e lunar exploration program, Tianwen-1 Mars rover and robotic arms on the Tiangong space station. China’s roadmap for lunar bases and deep-space exploration ensures long-term investments in autonomous robotics for construction, servicing and planetary mobility.

Beyond the big players, South Korea and Australia are entering the space robotics market. South Korea is using robotics for planned lunar exploration missions and Australia's collaboration with NASA under the Artemis Accords includes the development of a semi-autonomous lunar rover by the mid-2020s. With increasing government financing, regional collaboration and the arrival of commercial entrepreneurs, the Asia-Pacific space robotics market is predicted to become one of the most competitive, contributing not just to national projects but also to global commercial missions.

India Space Robotics Market Outlook

India's space robotics sector is expanding rapidly, fuelled by ISRO's emphasis on lunar and planetary exploration. Robotic technologies were tried in missions such as Chandrayaan-2 and Chandrayaan-3, where autonomous landing and rover systems demonstrated India's expanding capabilities. Looking ahead, ISRO plans to invest in robotic arms and humanoid robots (such as Vyommitra) for the future Gaganyaan human spaceflight mission. The government's effort for commercialization and private sector participation is also projected to create chances for robotics firms meeting satellite servicing and manufacturing needs.

China Space Robotics Market Trends

China's Space Robotics market prognosis remains positive, as it is one of the most advanced countries in space robotics, accounting for more than 40% of the regional market. It has successfully deployed robotic arms on the Tiangong space station, as well as surface rovers on the Moon and Mars. The country's space robotics industry is inextricably connected to its long-term goal of establishing permanent lunar outposts and improving on-orbit servicing capabilities. Chinese enterprises and CASC subsidiaries are developing autonomous satellite servicing and debris removal technologies that are consistent with both national security and commercial purposes. With strong state backing and swift execution, China is poised to be a global leader in robotic applications for human spaceflight, exploration and in-orbit operations.

Presence of Major Companies in North America

North America is expected to be dominant region of the global market holding about 40% of the market in 2024. The region’s strong space exploration programs, sophisticated technological infrastructure and significant R&D expenditures are expected to make it the market leader in the worldwide deep space robotics market. Presence of leading space agencies like NASA and premier private space companies such as SpaceX, Blue Origin and Lockheed Martin gives a competitive advantage in this region. Also, government assistance in policies, financing deep space missions and partnerships with commercial players support North America's market leadership.

Space agencies and companies are building deep space robots that may operate in extreme conditions. An example is NASA, which is currently building its new space-exploring robot, the Shapeshifter. The Shapeshifter is an amphibious aerial robot capable of rolling, flying, floating and swimming. The NASA Innovative Advanced Concepts research program is constructing the robots. When complete, the robots will be able to explore Saturn's moon, Titan, which has liquid (in the form of seas of methane) on its surface.

US Space Robotics Market Insights

US currently dominates the commercial space robotics business, thanks to NASA's legacy and private sector innovation. NASA's contributions include Canadarm2 (on the International Space Station), Mars rovers Curiosity and Perseverance and planned robotic systems for the Artemis lunar program and Lunar Gateway station. Commercially, US businesses are pioneering new uses, including Northrop Grumman's MEV spacecraft for satellite life extension, Redwire's in-space manufacturing robotics and Astrobotic's lunar surface robots for cargo delivery. With billions funded annually through NASA and the Department of Defense, together with a robust commercial sector, US is the largest market and engine of innovation in space robotics globally.

Canada Space Robotics Industry Growth

Canada holds a unique global position as a specialist in space robotics, largely through its legacy of the Canadarm series. The Canadarm and Canadarm2 have been critical to Shuttle missions and ISS operations, while the upcoming Canadarm3 will play a central role on NASA’s Lunar Gateway. Canadian company MDA leads this sector, developing robotic arms, manipulators and autonomous servicing systems for both government and commercial clients. Beyond government contracts, Canada is increasingly targeting the commercial servicing market, leveraging its decades of expertise to expand into robotic satellite repair, inspection and orbital logistics services.

Technology Analysis

Advancements in space robotics are focused on enhanced autonomy, resiliency and accuracy. Artificial Intelligence (AI) and Machine Learning (ML) have been one of the significant advances, which allows robots to make decisions in real-time while on missions with very little human intervention.

For example, NASA's Mars rovers now have autonomous navigation systems that enable them to move across new terrain without repeated Earth-based instructions. This is important due to the communication delay in communication with deep space objects, which varies from 5 to 20 minutes one way.

Why Space Robotics Is Becoming Mission Critical

Space missions are becoming increasingly complex. Future lunar bases, Mars exploration programs, asteroid resource extraction projects, and orbital infrastructure initiatives require robotic systems capable of operating independently in environments characterized by radiation, communication delays, and extreme temperatures.

Programs such as NASA's Artemis initiative, future lunar habitat projects, and robotic exploration missions are increasing demand for advanced mobility systems, robotic manipulators, autonomous navigation software, and intelligent servicing platforms. As human presence expands beyond low-Earth orbit, robotics will serve as the primary workforce supporting construction, maintenance, inspection, and scientific operations.

Technology Evolution and Autonomy Trends

Artificial intelligence, machine learning, computer vision, and autonomous navigation systems are becoming central components of modern space robotics platforms.

The hardware-software stack increasingly consists of robotic arms, mobility platforms, sensors, machine vision systems, AI processing modules, autonomous navigation software, and communication systems designed for delayed-response environments.

Recent examples include JAXA's Int-Ball system aboard the International Space Station, which autonomously captures images and videos while reducing astronaut workload. Similar technologies are being integrated into future robotic explorers, servicing spacecraft, and orbital infrastructure systems.

The market is progressing through several autonomy levels:

- Assisted robotic operations with human oversight

- Semi-autonomous mission execution

- Autonomous navigation and inspection

- Fully autonomous servicing and exploration systems

Higher autonomy levels are expected to become essential for deep-space missions where communication delays make real-time control impractical.

Market Opportunities Through 2035

The most attractive opportunities are emerging where robotics intersects with long-term space infrastructure development.

For manufacturers, demand is growing for robotic manipulators, mobility systems, autonomous navigation technologies, and AI-enabled mission software.

For technology companies, opportunities exist in perception systems, machine learning algorithms, sensor fusion technologies, and autonomous decision-making platforms.

For investors, companies focused on satellite servicing, orbital logistics, in-space manufacturing, and robotic construction systems offer exposure to recurring revenue opportunities rather than one-time mission contracts.

For procurement organizations, robotic solutions provide a path toward reducing mission costs while improving operational reliability and asset longevity.

Competitive Landscape

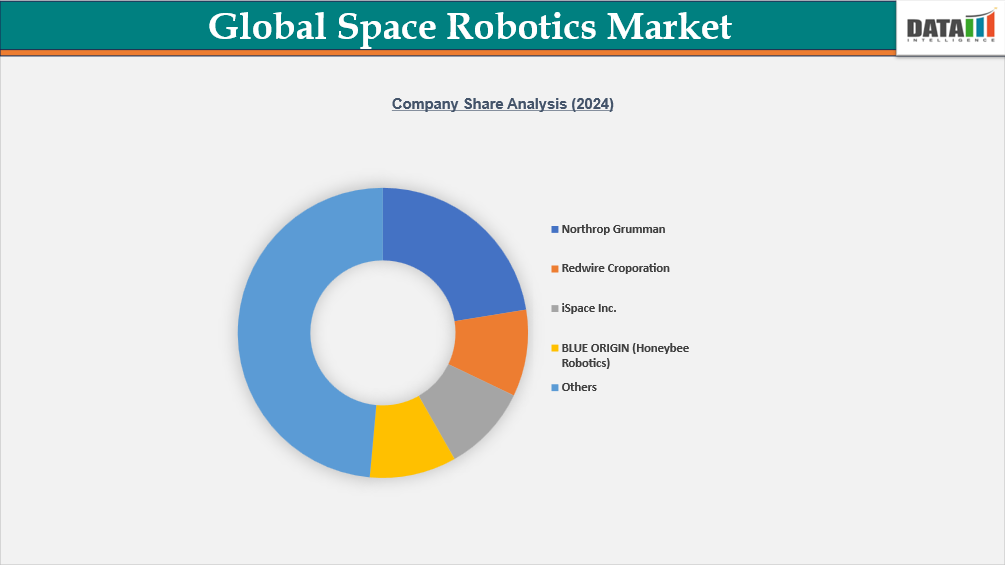

The space robotics market is competitive, driven by a mix of global and regional players striving for technological efficiency and cost leadership.

Key players include Northrop Grumman, Redwire Corporation, iSpace Inc., BLUE ORIGIN (Honeybee Robotics), Motiv Space Systems Inc., Maxar Technologies, Astrobotic Technology, Space Applications Services, Ceres Robotics Inc. and Lunar Resources, Inc.

Players are investing highly in robotics, robotic servicing technologies and seek robotic solutions to reduce costs, extend satellite lifecycles and enable new business models in orbit, to gain an edge.

Key Developments

February 2026: Across North America, Europe, and Asia Pacific, rising investments in space exploration programs, satellite constellations, and commercial space activities significantly accelerated demand for space robotics systems supporting autonomous missions and orbital operations.

January 2026: Globally, advancements in AI-enabled robotics, machine learning, and autonomous navigation systems enhanced the capability of robots to perform complex tasks such as on-orbit servicing, satellite repair, and deep-space exploration.

December 2025: Leading organizations such as NASA, SpaceX, Northrop Grumman, Boeing, and emerging startups expanded investments in robotic arms, planetary rovers, and in-space manufacturing technologies, strengthening innovation across the space robotics ecosystem.

November 2025: Increasing deployment of robotic systems for satellite servicing and on-orbit maintenance significantly improved mission efficiency, extended satellite lifespans, and reduced operational costs in space missions.

October 2025: Rising focus on lunar and planetary exploration missions, along with development of robotic mobility platforms and surface operation systems, accelerated adoption of robotics for extraterrestrial infrastructure development.

September 2025: Across key regions including the United States, China, India, Germany, and Japan, increasing government funding, defense space programs, and public-private partnerships significantly supported market growth and innovation.

The market is rapidly evolving toward autonomous, AI-driven space operations, where robotics, in-space manufacturing, and self-assembling systems are transforming how missions are conducted, enabling safer, cost-efficient, and scalable exploration beyond Earth.

Why Choose DataM?

Data-Driven Insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. This approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. This personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. These insights complement and go beyond what is typically available in generic databases.

Target Audience

- Aerospace and Defense Manufacturers

- Space Agencies and Government Organizations

- Satellite Operators

- Commercial Space Companies

- Robotics Technology Providers

- Component Suppliers

- Investors and Venture Capital Firms

- Research Institutions

- Systems Integrators

- Strategic Consulting Firms