Smart Hospitals Market Size & Industry Outlook

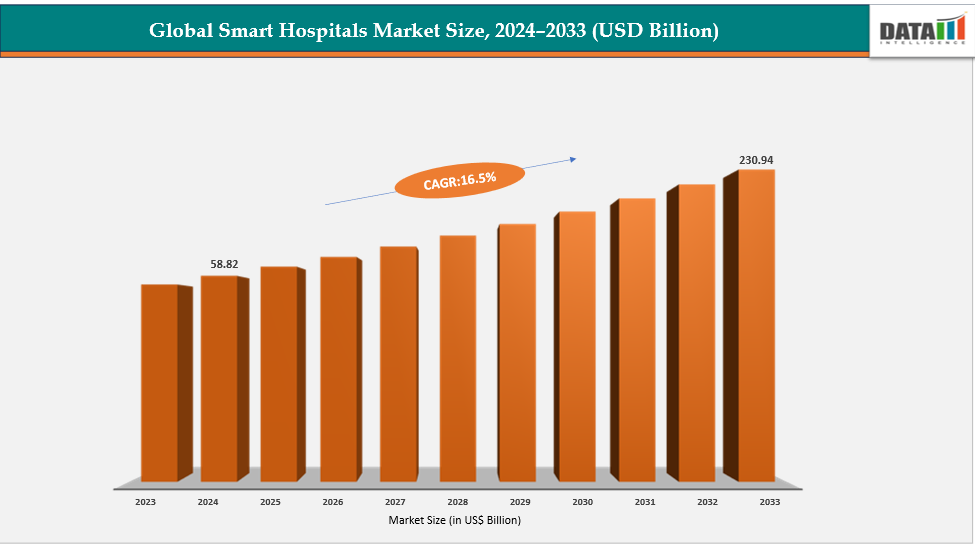

As per DMI analysis, the global smart hospitals market was US$58,247.59 million in 2024 and expected to reach up to US$363,954.84 million in 2032, growing at a CAGR of 26.2% during the forecasting period (2026-2033)

- The global smart hospitals market is advancing at a pace as providers adopt AI, automation, and wireless-first infrastructure to improve capacity, productivity, and care quality. By 2025, more than 350 hospitals across 30 countries had achieved recognized digital excellence, reflecting strong global momentum toward intelligent care delivery. Proven performance gains, AI tools saving over 15,000 documentation hours annually, 74% of leaders viewing virtual nursing as essential, and Wi-Fi 6E/5G reducing network bottlenecks and enabling real-time clinical applications, are accelerating investment, positioning smart hospitals as a critical enabler of efficient, scalable, and high-quality healthcare.

- For instance, in August 2024, PAHO introduced the Digitally Smart Health Facilities (DSHF) framework, signaling a transformational shift in the Americas. By embedding IoT, AI, blockchain, mobile platforms, and telehealth into facility design, DSHFs aim to strengthen system resilience and enable continuity of care during emergencies. This aligns with broader demand trends, with 94% of patients preferring digital or hybrid care models and governments prioritizing long-term infrastructure modernization.

- In December 2025, ECU Health partnered with Artisight to deploy an AI-driven Smart Hospital Platform across rural North Carolina, supporting Tele-Neuro, Tele-ICU, virtual nursing, and real-time behavior detection. This transformation enables patients in remote areas to access specialized care locally, aligning with industry trends showing that 84% of clinicians report improved communication when AI tools are integrated into workflows and 82% report higher job satisfaction.

- The IMA AMR Smart Hospital Project, launched in December 2024, reflects India’s national emphasis on antimicrobial stewardship and infection control. Through a certification framework rolled out to 1,700+ IMA branches, the pilot proved effective in strengthening surveillance and reducing inappropriate antimicrobial use. With AMR projected to cause 10 million annual deaths by 2050, the initiative positions AMR-focused smart hospital practices as a critical component of safety and quality transformation.

Key Highlights

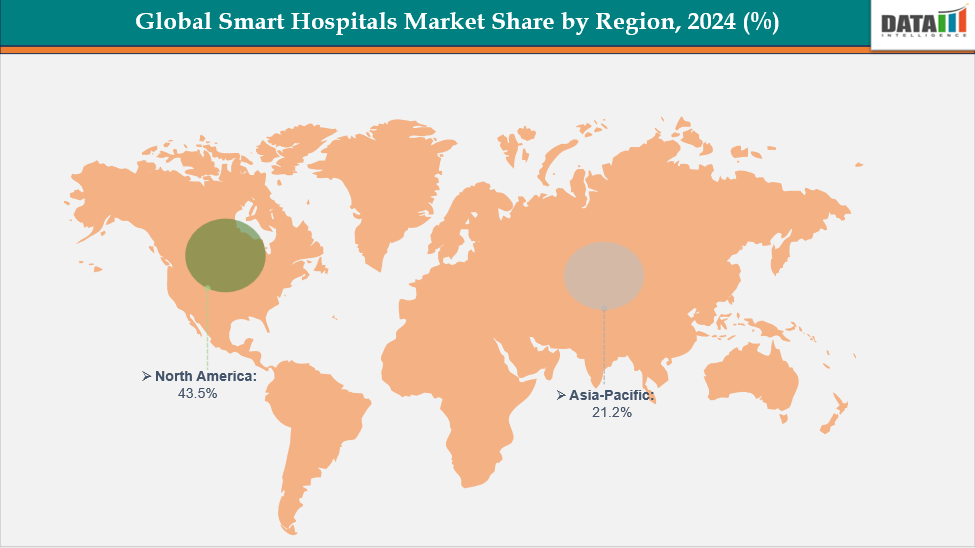

- North America dominates the smart hospitals market with the largest revenue share of 43.5% in 2024.

- The Asia Pacific is the fastest-growing region and is expected to grow at the fastest CAGR of 8.1% over the forecast period.

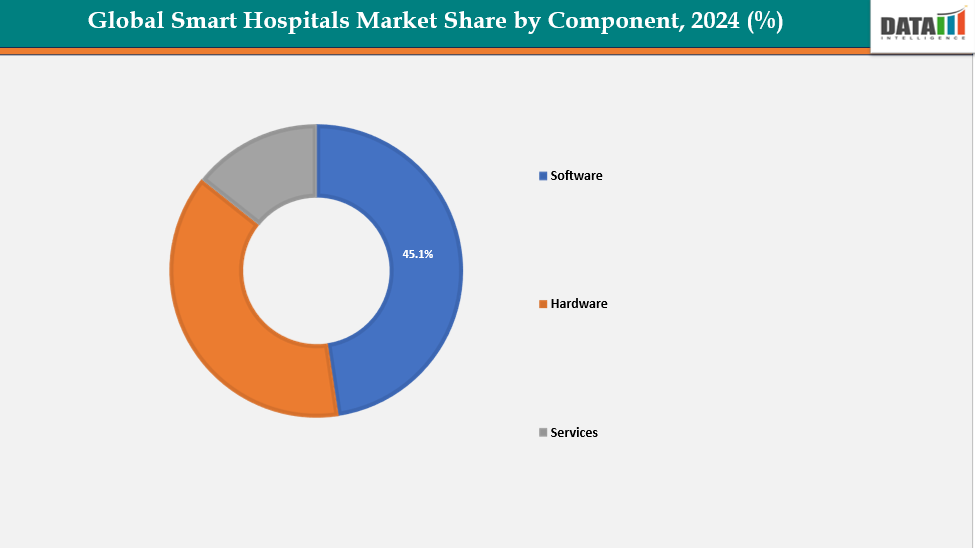

- Based on component, software segment led the market with the largest revenue share of 45.1% in 2024.

- The major market players in the Smart Hospitals market includes eVideon, Artisight, Uniguest, Oneview Healthcare, Diligent Robotics, Andor Health and among others.

Market Dynamics

Drivers: Rising adoption of IoT, AI, and automation in healthcare driving the smart hospitals market growth

The integration of Internet of Things (IoT), Artificial Intelligence (AI), and automation technologies is one of the most transformative drivers of the global smart hospitals market. These technologies enable hospitals to move beyond traditional, reactive models of care toward predictive, data-driven, and highly efficient systems. By connecting medical devices, sensors, and hospital infrastructure, IoT creates an intelligent network that continuously gathers and analyzes patient data in real time. This helps clinicians make faster, more accurate decisions, reduces human error, and streamlines workflows across departments.

| IoT Application | Benefits | Implementation Cost |

| Patient Monitoring | 24/7 vital tracking, early warning systems | Medium |

| Asset Tracking | Equipment location, utilization analytics | Low |

| Environmental Control | Energy savings, optimal patient comfort | High |

| Security Systems | Access control, patient safety | Medium |

Restraints: High implementation and integration costs are hampering the growth of the smart hospitals market

One of the most significant barriers limiting the widespread adoption of smart hospital solutions is the high cost of implementation and system integration. Building a smart hospital requires substantial investment in digital infrastructure, including IoT sensors, connected medical devices, data management platforms, cybersecurity systems, and AI-powered software. For many healthcare providers—especially mid-sized and public hospitals—the financial burden of transitioning from legacy systems to fully digital environments remain prohibitive.

On average, the initial setup cost for a mid-sized smart hospital can range between USD 10 million and USD 50 million, depending on the scale of automation, interoperability requirements, and the complexity of existing hospital IT systems. Beyond hardware and software procurement, a large portion of expenditure goes toward system integration and staff training, which can account for up to 30–40% of total project costs.

For more details on this report – Request for Sample

Smart Hospitals Market, Segment Analysis

The global smart hospitals market is segmented based on component, technology, application, connectivity, end user and region.

Component: The software segment from component segment to dominate the smart hospitals market with a 45.1% share in 2024

The software segment is a key growth driver in the smart hospitals market, enabling integration of clinical, operational, and patient engagement systems. Hospitals are increasingly adopting AI-based analytics, workflow automation, EHRs, and virtual engagement platforms to enhance efficiency and decision-making. Platforms like Artisight’s Smart Hospital, ThinkAndor, and Vibe Health by eVideon demonstrate how intelligent software optimizes workflows and improves patient experiences.

The rise of cloud-based and interoperable solutions further supports scalability and cost efficiency. As healthcare shifts toward digital-first models, software platforms form the core infrastructure powering automation, connectivity, and real-time data intelligence in modern hospitals.

For instance, in June 2025, King Faisal Specialist Hospital & Research Centre (KFSHRC) is setting new benchmarks in global healthcare through its Smart Hospital initiative, which integrates AI, simulation, and immersive technologies across multiple departments. This digital transformation is enabling KFSHRC to advance clinical excellence, strengthen workforce training, and boost operational efficiency, reinforcing its position as a leader in next-generation healthcare delivery.

Technology: The artificial intelligence (AI) segment is estimated to have a 41.1% of the smart hospitals market share in 2024

The AI segment significantly drives the global smart hospitals market by transforming healthcare systems in patient care delivery, monitoring, and management. It empowers hospitals to analyze extensive clinical data in real time, automate decision-making processes, and predict health outcomes with improved accuracy. The integration of AI into diagnostics, workflow management, and patient engagement leads to marked improvements in clinical efficiency, error reduction, and enhanced patient safety.

For instance, in March 2025, The International Institute of Information Technology Hyderabad (IIITH) has partnered with AIG Hospitals to create the Centre for Digital Technologies in Healthcare (CDiTH). This collaboration enhances AIG Hospitals' status as a premier AI-driven medical facility, focused on the incorporation of artificial intelligence (AI) and digital technologies to advance patient care, optimize operational efficiency, and support medical research.

Smart Hospitals Market, Geographical Analysis

North America

- North America’s smart hospitals market was valued at US$ 22,972.85 million in 2024 and is estimated to reach US$ 100,785.08 million by 2032, growing at a CAGR of 20.7% during the forecast period from 2025-2032.

- The demand for smart hospitals in North America is accelerating rapidly as healthcare systems increasingly face challenges related to rising operational costs, staffing shortages, aging populations and heightened expectations for high-quality, digitally connected care.

- Smart hospitals leverage technologies such as artificial intelligence (AI), the Internet of Things (IoT), telehealth platforms, predictive analytics and integrated digital monitoring to transform both clinical and administrative operations. These solutions enable real-time decision making, automation of routine tasks, improved patient safety and efficient resource utilization.

- A critical factor supporting market demand is the region’s long established digital health foundation, especially the widespread adoption of Electronic Health Records (EHRs). According to the US Office of the National Coordinator for Health Information Technology (ONC), nearly 96% of non-federal acute care hospitals have implemented certified EHR systems. This near-universal adoption creates an essential baseline for more advanced smart hospital features, including predictive AI and automation layers that build on EHR data.

- Government-supported initiatives that promote interoperability, health information exchange and reporting transparency continue to push hospitals toward digital transformation. Between 2023 and 2024, ONC reported that US hospitals’ use of predictive AI tools integrated into clinical workflows rose from 66% to 71%, showing how healthcare providers are shifting from digitization to intelligent optimization. Such policy driven momentum is foundational to North America's leadership in smart hospital adoption.

- Telehealth and remote care integration also play an essential role in fueling the demand for smart hospitals in the region. The pandemic significantly expanded virtual care expectations and many of these usage trends have persisted due to improved access, convenience and cost efficiency. Smart hospital systems embed telehealth directly into clinical and patient monitoring workflows, allowing seamless communication between patients, bedside clinicians and remote specialists.

- A recent example illustrating this trend is ECU Health’s collaboration with Artisight to roll out smart hospital technology across eastern North Carolina in December 2025. The rollout, beginning with five hospitals, Roanoke-Chowan, Bertie, Chowan, North and Duplin, incorporates AI-enabled monitoring, virtual care capabilities and integrated telehealth workflows. The initiative enhances Tele-ICU, Tele-Neuro and continuous virtual patient observation services, enabling specialists at the central medical center to support local facilities and improving care in rural regions. Such deployments show how smart systems close access gaps, boost efficiency and help mitigate rural healthcare staffing shortages, further driving regional demand.

- Demand is also driven by the operational efficiencies that smart hospital systems provide. AI and IoT solutions streamline administrative processes, automate documentation, optimize patient flow, reduce equipment downtime and support predictive maintenance. Hospitals in North America increasingly recognize that these efficiencies translate into measurable financial gains. In March 2022, a notable example is the smart hospital initiative announced by Intuitive MB, highlighted by Realty Trust Group, where real-time IoT sensor networks and AI-driven analytics help predict facility usage patterns, cut maintenance costs and improve environmental sustainability. These improvements extend beyond traditional clinical operations, showing that smart hospital technologies are becoming central to enterprise-wide optimization strategies for modern healthcare systems.

South America

- South America’s smart hospitals market was valued at US$ 3,092.95 million in 2024 and is estimated to reach US$ 21,169.85 million by 2032, growing at a CAGR of 27.5% during the forecast period from 2025-2032.

- South America’s demand for smart hospitals is rising as governments and health institutions confront deep‑rooted systemic challenges including aging populations, rising chronic disease burdens, uneven access to care, workforce shortages and gaps in digital health infrastructure. Public health systems throughout the region have traditionally relied on manual processes and fragmented information systems, leading to inefficiencies, care delays and poor coordination between facilities. These pressures have created momentum for adopting smart hospital frameworks, integrated digital ecosystems that leverage artificial intelligence (AI), the Internet of Things (IoT), robotics, telemedicine and real‑time clinical analytics to improve clinical outcomes, streamline workflows and expand access to high‑quality care.

- Brazil stands at the forefront of this regional transformation due to its expansive public healthcare network and a strategic commitment to digital modernization. Rather than relying on erroneous estimates of patient procedures, it is important to recognize that Brazil’s Unified Health System (SUS) serves millions of users and carries significant operational complexity across primary, secondary and tertiary care, according to official Ministry of Health reports. In July 2025, Brazil secured concept approval for US$ 320 million in financing from the New Development Bank (NDB) to develop the country’s first fully integrated smart hospital under SUS. This 150,000‑square‑meter facility, designed to international standards of safety, sustainability and technological innovation, will deploy AI‑based diagnostics and prognostics, telemedicine platforms, 5G‑enabled emergency services and automated predictive management tools. The initiative aims to enhance workflows in emergency, intensive care and neurology departments and represents a model for future digital health infrastructure in public systems.

- Moreover, smart hospitals are intensifying as demographic pressures, increasing chronic disease burdens and digital health reforms converge to reshape healthcare delivery. PAHO and ECLAC project that 22–25% of Latin American and Caribbean residents will be aged 60 or older by 2030. This shift increases demand for continuous care, disease management and acute clinical support. Conditions such as cardiovascular disease, diabetes and cancer account for a majority of regional deaths, driving hospitals to adopt precision diagnostics, predictive analytics, automated alerting systems and real-time clinical decision support tools. These technologies enable clinicians to personalize care pathways and optimize resource allocation across complex patient populations.

- Private partners like Digital Ware provide solutions such as Hosvital-HIS and Davinci-SAR, enabling real-time data exchange, live monitoring and coordinated care, reducing bottlenecks and supporting continuous operations. Private-sector innovation and multinational partnerships accelerate adoption. At Hospitalar São Paulo, companies such as Mindray showcase platforms like M-Connect, unifying medical devices, patient data flows and automated analytics to improve workflow efficiency and situational awareness. Telemedicine and connected care are critical in geographically and socioeconomically diverse regions, where one in five residents lives in underserved areas, with smart hospital systems integrating tele-ICU, remote diagnostics, virtual triage and emergency teleconsultations. Government frameworks further reinforce adoption. Brazil’s ConecteSUS, Colombia’s Digital Health Policy, Chile’s national strategy and Argentina’s telemedicine regulations support interoperable EMRs, data governance and real-time analytics, enabling seamless smart hospital operations. South America is moving decisively toward integrated, patient-centered, data-driven hospital systems, with smart hospitals essential for high-quality, equitable and efficient care.

Europe

- Europe’s smart hospitals market was valued at US$ 16,699.58 million in 2024 and is estimated to reach US$ 96,787.71 million by 2032, growing at a CAGR of 24.9% during the forecast period from 2025-2032.

- The demand for smart hospitals in Europe is emerging as a transformative force in healthcare, driven by structural pressures such as aging populations, rising chronic disease prevalence, workforce shortages and policy commitments to improve quality while controlling costs. Unlike traditional facility upgrades, smart hospitals embed digital technologies like artificial intelligence (AI), the Internet of Things (IoT), robotics, telehealth services and data analytics into clinical, operational and administrative workflows.

- Europe’s aging population is a key driver of this demand. According to Eurostat, by 2050 nearly 30% of the EU’s population will be aged 65 or older, compared to about 21% in 2023, reflecting the fastest demographic shift in the region’s history. This trend is already visible, as the number of adults aged 80+ across the EU increased by 57% between 2001 and 2021, placing growing strain on hospitals to manage chronic diseases, complex diagnostic needs and long-term care services. With these demographic pressures, European policymakers are accelerating smart hospital adoption to ensure sustainable healthcare delivery without proportionate increases in staffing or infrastructure costs.

- A central element pushing smart hospital adoption across Europe is the commitment to interoperability and widespread electronic health records (EHRs). The European Health Data Space (EHDS) initiative is expected to give more than 450 million EU citizens access to cross-border digital health data, strengthening the infrastructure needed for real-time data aggregation, predictive analytics and AI-powered clinical tools, all core components of the smart hospital ecosyste.

- Cultural and organizational shifts within hospitals also influence demand. Patients increasingly expect seamless, data-enabled experiences similar to digital services outside of healthcare. In many European systems, smart hospital technologies reduce waiting times and administrative burden. Dr. Peter Gocke, Head of Digital Transformation at Charité – Universitätsmedizin Berlin, highlights that patients in smart facilities notice efficiency through smoother processes, fewer repeated forms, more seamless data flows and reduced manual tasks. Charité itself exemplifies German and broader EU interest in smart workflows; with over 70 ongoing AI projects, Charité underscores how structured data use, not merely hardware upgrades, propels digital transformation.

- Recognition of European smart hospital excellence also fuels demand by benchmarking performance globally. Karolinska University Hospital in Sweden ranked 13th on the “World’s Best Smart Hospitals 2025” list published by Newsweek, among 350 hospitals in 28 countries. This ranking highlights European leadership in adopting technologies like robotics, digital imaging, AI-assisted diagnosis and 24/7 telehealth communication. Such visibility does not just celebrate individual achievement but encourages peer institutions to pursue similar advancements.

- Technology expectations extend beyond individual hospitals to pan-European initiatives that aim to create shared technology platforms. A prominent example is the EU-funded HosmartAI project, which seeks to establish a common open integration platform for robotics and AI in healthcare settings. The ambition is to validate this platform through eight large-scale pilots across multiple disease areas. These pilots demonstrate how digital integration can measurably improve clinical outcomes, workflow efficiency and the patient experience.

- The European Union’s policy environment has become a major catalyst for the region’s smart hospital expansion, with initiatives like the European Health Data Space (EHDS) designed to enable secure, standardized data sharing across borders. The EU has reinforced this through programs such as EU4Health, which dedicates over €5.3 (US$ 5.8) billion (2021–2027) to digital health modernization. These efforts align with national eHealth strategies across member states, many of which include targets for expanding telehealth, digital prescriptions and real-time clinical data use, foundational components for smart hospitals.

- Operational requirements provide an additional push for adoption. Structured analytics allow hospitals to optimize patient flow, identify delays and reduce bottlenecks. In the UK, Nottingham University Hospitals NHS Trust tested systems that allow patients to control lighting and temperature using voice or bedside terminals, while AI-enabled CCTV supports monitoring of patients with cognitive impairments. These examples highlight how smart hospital technologies combine clinical safety with digital automation. The need to improve patient outcomes is also shaping demand, according to the European Patient Safety Foundation, up to 8–12% of EU hospitalizations involve adverse events, many of which are preventable with better monitoring and automated alerting systems. Financial sustainability further accelerates smart transformation. Public health systems under cost pressure increasingly rely on digital tools to reduce unnecessary admissions, enable virtual care and optimize beds and staff allocation. Europe’s smart hospital demand is reinforced by demographic pressures, the rapid expansion of interoperable health data networks and policy-backed digital transformation. Leadership from institutions like Karolinska and Charité, coupled with EU-funded innovations such as HosmartAI, illustrates a region moving decisively toward efficient, patient-centered, data-driven hospital ecosystems that will define the future of European healthcare.

The Asia Pacific region is the fastest-growing region in the global smart hospitals market, with a CAGR of 8.1% in 2024

- The Asia Pacific region is rapidly growing in smart hospitals due to rising healthcare spending, urbanization, and government modernization initiatives. Countries like India, China, South Korea, and Singapore are investing in digital health ecosystems to address population demands and chronic diseases, adopting IoT devices, AI diagnostics, and telehealth platforms. Strategic partnerships, including collaborations with companies like Samsung and Fujitsu, are enhancing this digital transformation.

- In Japan, an aging population drives the development of smart hospitals, supported by the government's push for Society 5.0, integrating robotics, IoT, and virtual care to address workforce shortages and improve patient management. Collaborations with firms such as Fujifilm and Hitachi are fostering innovation and positioning Japan as a key player in advanced smart hospital solutions in Asia.

Competitive Landscape

Top companies in the smart hospitals market include eVideon, Artisight, Uniguest, Oneview Healthcare, Diligent Robotics, Andor Health and among others.

Artisight:- Artisight plays a pivotal role in advancing the global smart hospitals market through its AI-powered Smart Hospital Platform, which combines computer vision, machine learning, and IoT connectivity to transform hospital operations and patient care. The platform enables real-time monitoring of patient rooms, automates routine clinical workflows, and enhances communication between care teams—all while ensuring data security and compliance.

Market Scope

| Metrics | Details | |

| CAGR | 26.2% | |

| Market Size Available for Years | 2022-2033 | |

| Estimation Forecast Period | 2026-2033 | |

| Revenue Units | Value (US$ Bn) | |

| Segments Covered | Component | Software, Hardware, Services |

| Technology | Artificial Intelligence (AI), Internet of Things (IoT), Cloud Computing, Big Data | |

| Application | Electronic Health Records (EHR) / Clinical Workflow, Medical Connected Imaging, Remote Medicine / Remote Patient Management, Medical Assistance | |

| Connectivity | Wired, Wireless | |

| End User | Hospitals, Home-care / Remote settings, Others | |

| Regions Covered | North America, Europe, Asia-Pacific, South America and the Middle East & Africa | |

The global smart hospitals market report delivers a detailed analysis with 62 key tables, more than 57 visually impactful figures, and 159 pages of expert insights, providing a complete view of the market landscape.

Suggested Reports

For more healthcare it-related reports, please click here