Silicon Carbide Power Semiconductor Market Size & Share:

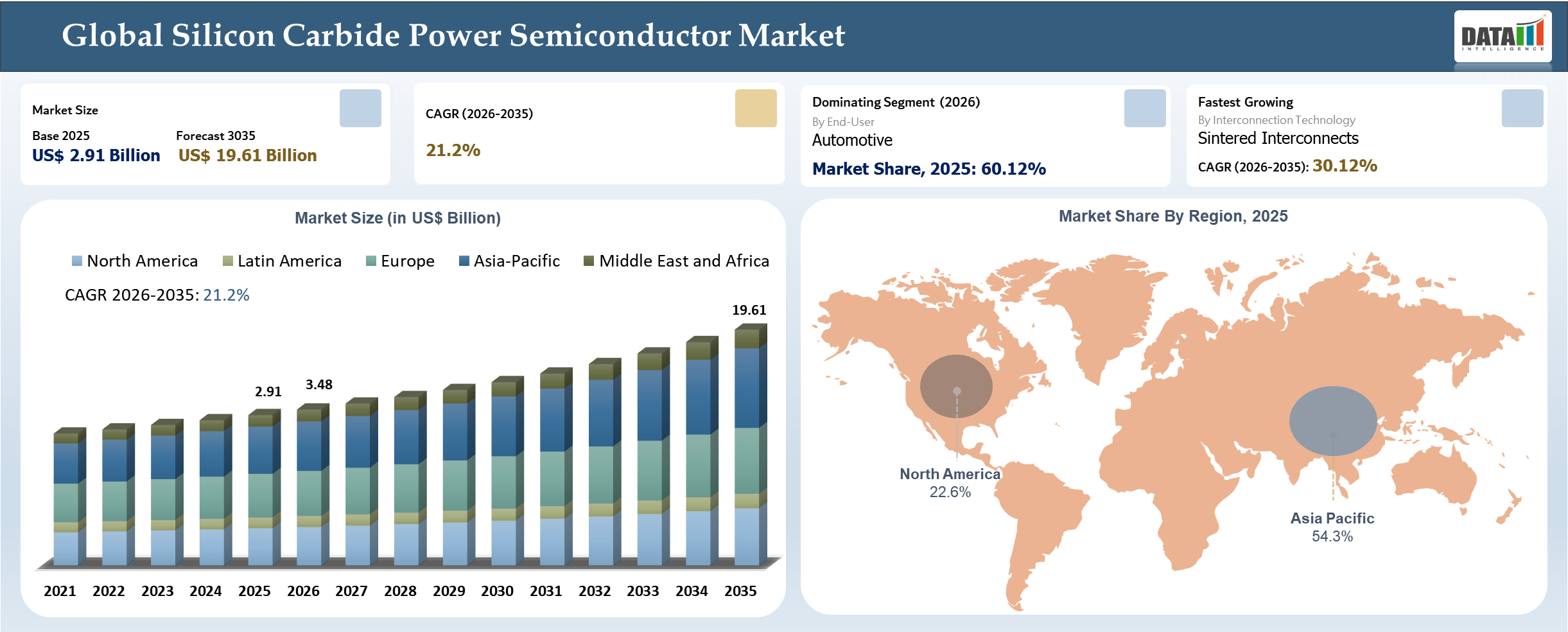

The global silicon carbide power semiconductor market reached US$ 2.91 billion in 2025 and is expected to reach US$ 19.16 billion by 2035, growing with a CAGR of 21.2% during the forecast period 2026-2035.

Moving from a capex-intensive growth phase to an efficiency-focused optimization phase, the sector currently faces issues of overcapacity and underutilization in the near term owing to the fast pace of capacity expansion from 2019 to 2024. The market has shifted to efficiency gains, cost savings, and scaling up the production of 200 mm wafers, along with innovations in MOSFET design and power module technology. Competition is being witnessed as a result of rising vertical integration and participation by Chinese companies throughout the supply chain.

Silicon Carbide Power Semiconductor Industry Trends and Strategic Insights

- The move towards high-efficiency, high-voltage power electronics has been spurred by the shift to the adoption of 800V architectures for EVs and high-speed charging stations, with players such as STMicroelectronics and Infineon Technologies developing new products and expanding capacity in silicon carbide power electronics.

- Energy and industrial firms such as Siemens AG and Schneider Electric have begun implementing power electronics based on SiC technology to boost energy efficiency and grid reliability as well as deliver top-of-the-line motor drives.

- Semiconductor companies such as onsemi and ROHM Semiconductor are focusing on new architectures within power electronic devices, such as trench MOSFETs and power modules, to improve switching efficiency and enable more compact system designs.

Silicon Carbide Power Semiconductor Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 2.91 Billion | |

| 2035 Projected Market Size | US$ 19.61 Billion | |

| CAGR (2026-2035) | 21.2% | |

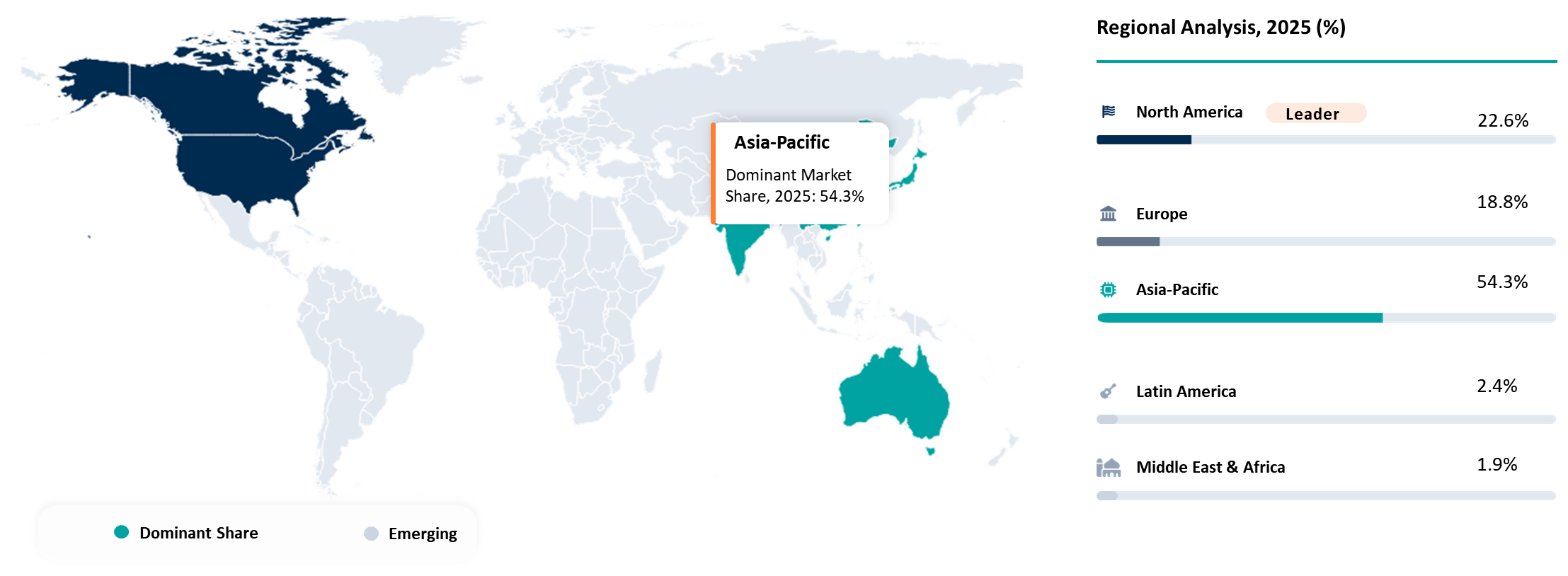

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | North America | |

| By Product Type | Discrete Devices, Power Modules, and Bare Die / Unpackaged Chips | |

| By Voltage Rating | Low Voltage (<650V), Mid Voltage (650-1200V), High Voltage (1200-1700V), Very High Voltage (1.7kV-3.3kV), and Ultra High Voltage (>3.3kV) | |

| By Wafer Size | 1-4 inch, 6 inch, 8 inch and 10 inch & above | |

| By Substrate Technology | DBC (Direct Bonded Copper), AMB (Active Metal Brazed) and IMS (Insulated Metal Substrate) | |

| By Interconnection Technology | Wire Bonding, Ribbon Bonding, Sintered Interconnects, Flip-Chip / Direct Bonding and Embedded Die Interconnect | |

| By Electrical Function | Switching Devices, Rectification Devices and Integrated Power Conversion | |

| By End-User | Automotive, Energy & Power, IT & Telecom, Consumer Electronics, Aerospace & Defense, Medical Devices and Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Disruption Analysis

Shift from Silicon-Based Power Devices to Wide Bandgap Architectures Reshaping Power Electronics Efficiency

A transformation in the silicon carbide power semiconductors market is currently taking place with wide bandgap semiconductor devices increasingly replacing silicon power devices by setting new benchmarks for efficiencies and performance. With SiC, high switching efficiency, high performance, and ability to support high-voltage architectures, including 800V electric vehicle platforms, have emerged. Technology is being increasingly adopted in electric cars, renewables, and industrial sectors.

Also, a shift in manufacturing practices, with greater emphasis on scaling up production processes, utilizing more complex MOSFET designs, and implementing power modules. Vertical integration and growing Chinese involvement in the sector add to increasing competition. Overproduction in the near term is leading companies to concentrate on improving yield rates.

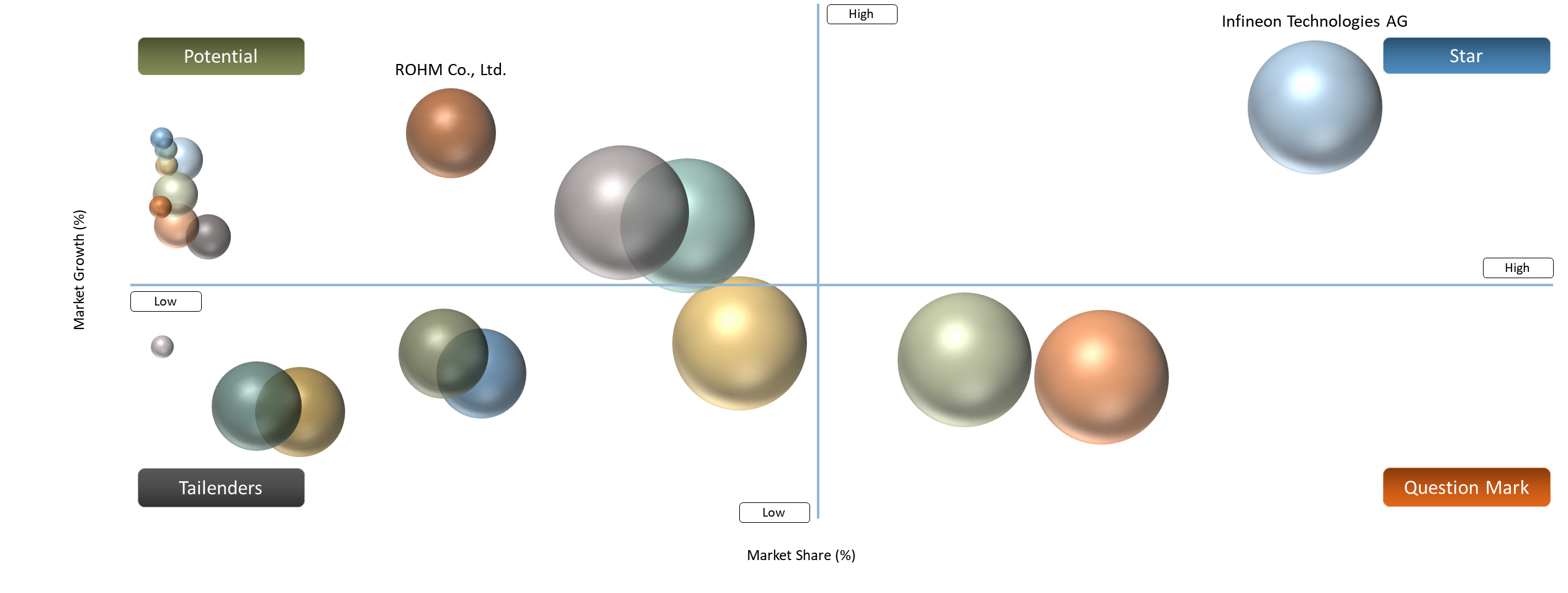

BCG Matrix: Company Evaluation

Major firms such as STMicroelectronics, Infineon Technologies, and Semiconductor Components Industries, LLC (Onsemi) fall under the category of Stars because they have high market share, strong presence in automobiles, and consistent investments in the production capacity of 200 mm SiC. Companies such as Wolfspeed, Inc. and ROHM Co., Ltd. can be categorized as Question Marks since they possess outstanding technological capabilities and growth opportunities in terms of substrates and devices; however, their global presence is increasing gradually.

Companies like Mitsubishi Electric Corporation and Fuji Electric Co., Ltd. are identified as Potential because of their existing knowledge of power electronics and growing involvement in SiC applications. Companies such as TOSHIBA ELECTRONIC DEVICES & STORAGE CORPORATION, Microchip Technology Inc., Hitachi, Ltd., and Littelfuse, Inc. are considered Tailenders because of their minor involvement in SiC technologies.

Silicon Carbide Power Semiconductor Market Dynamics

EV Powertrain Electrification Driving SiC Substitution

The quick rise of electrification for power-hungry applications in automobiles, energy generation, and industry is resulting in a more widespread use of silicon carbide power semiconductors. The use of silicon carbide components in electric vehicle engines, solar energy converters, and industrial motor drives allows for more efficient energy consumption, better heat management, and less power loss, allowing for real-time energy optimization and efficiency. In addition to increasing operational effectiveness, this approach can also cut down on overall expenses by reducing cooling needs and power usage. STMicroelectronics and Infineon Technologies are increasing their offerings of silicon carbide products and manufacturing capacity to keep up with growing demand.

High Device Cost vs Silicon Alternatives

The cost of devices continues to be the main challenge when it comes to the use of silicon carbide devices as compared to silicon devices. Silicon carbide devices require complex manufacturing steps such as crystal growth, wafer processing, and defect reduction, hence yielding fewer outputs. It causes the costs of manufacturing to be high, while at the same time, there is a lack of good quality substrates and special equipment required for SiC devices.

The difference in cost creates an impact on adoption, especially in those applications that are very sensitive to price where system efficiency improvements may not be able to outweigh the higher cost at the beginning. In the case of SiC, although it provides advantages in the long term by saving energy, having a smaller system, and requiring less cooling, the cost factor limits its adoption in the consumer market.

Segment Analysis

The global silicon carbide power semiconductor market is segmented based on product type, voltage rating, wafer size, substrate technology, interconnection technology, electrical function, end-user and region.

Rising Adoption of SiC MOSFET-Based Discrete Devices Driving Flexible Power Electronics Integration

Discrete devices, especially the SiC MOSFETs, make up an essential part of the silicon carbide power semiconductor industry due to their versatility, efficiencies, and ease of incorporation into different power electronics applications. Such discrete semiconductors are more efficient when it comes to switching, can handle high voltages, and have superior thermal properties, which makes them ideal for use in various products, including but not limited to onboard chargers, DC-DC converters, industrial motors, and power supplies.

The SiC MOSFET-based discrete components permit the slow transition to wide-bandgap technology without a complete redesign of the systems involved, which makes them very suitable for mid-level power applications that have budget constraints. The discrete components give designers more freedom when designing the system by optimizing the system depending on their own needs. Even though most high-power applications make use of the power modules, the discrete components remain relevant in promoting the adoption of the SiC technology into the market.

Geographical Penetration

Asia-Pacific Dominance Driven by Strong Manufacturing Base and Electrification Demand

The Asia-Pacific region enjoys a prominent market share in the silicon carbide power semiconductor industry owing to an existing semiconductor manufacturing infrastructure and high demand for electric cars, renewable energy, and electrified industries. The region boasts integrated device manufacturers, state-of-the-art fabrication plants, and an established wafer, epitaxial growth, and device manufacturing supply chain.

The rapid pace of electrification in important economies is playing an important role in market growth, especially in the automotive and energy sectors. With more use of EV charging stations, renewable energy, and automation in industry, the demand for efficient power semiconductors continues to grow, with SiC having an advantage over other materials.

Moreover, constant efforts towards capacity enhancement and technology advancement, which include shifting to 200 mm wafer manufacturing, are making the process scalable and efficient. Consequently, Asia-Pacific is not just the biggest consumer of semiconductors but is also emerging as a key source for innovations and future growth of the market.

China Accelerating Market Growth Through EV Leadership and Supply Chain Localization

Key factors responsible for promoting the growth of the silicon carbide power semiconductor market include China’s prominent position in terms of electric vehicle manufacturing and usage. As far as electric vehicles are concerned, the huge market potential of China, along with the high requirement of quick charging systems, is expected to fuel their growth.

Government-led programs aimed at silicon carbide self-reliance and electrification have spurred substantial investment in SiC wafer fabrication, epitaxial growth, and device production. The result has been quick establishment of a local value chain, minimizing dependence on foreign sources and enhancing indigenous expertise in the entire value chain.

The country is also experiencing new entrants and more competition, especially in the upstream sectors like substrates and equipment. The development is improving cost efficiency and innovation, making China a major player in international market trends.

Japan Strengthening Market Position Through Advanced Power Electronics Innovation

Japan possesses a dominant position in the field of SiC power semiconductor due to its robust semiconductor manufacturing facility and experience in power electronics. There exist several leading firms in Japan who are making heavy investments in silicon carbide semiconductors in order to improve their performance.

Ongoing shift by Japanese firms in developing innovative ideas related to devices architectures, manufacturing technologies, and materials, such as improvements in the field of SiC MOSFETs and power modules. Such innovations would result in increased performance and efficiency as well as reduced losses.

Moreover, because of its focus on quality, precision manufacturing, and innovation through research and development, Japan is seen as a technological leader within the international SiC industry. Future alliances and advancements in new technologies will only enhance Japan’s competitive standing within the market environment.

Silicon Carbide Power Semiconductor Market Competitive Landscape

- The market is defined of three major layers that include IDM companies, SiC-only firms, and diversification in power electronics and components companies, making it highly dependent on ecosystems. The leading IDMs like STMicroelectronics, Infineon Technologies, and Semiconductor Components Industries, LLC (Onsemi) have a strong market position due to their vertical integration strategy involving substrates, devices, and modules, as well as their involvement with automobile OEMs. Their capability to produce 200 mm wafers, obtain long-term supply contracts, and provide integrated power solutions increases their competitive edge in fast-growing industries like electric vehicles and renewables.

- The technology-oriented companies like Wolfspeed, Inc. and ROHM Co., Ltd. are very crucial for developing substrate technology and innovations in devices especially SiC MOSFETs and epitaxy. In addition to the technology-oriented firms, the traditional power electronics and industrial companies such as Mitsubishi Electric Corporation, TOSHIBA ELECTRONIC DEVICES & STORAGE CORPORATION, Fuji Electric Co., Ltd., Hitachi, Ltd., Microchip Technology Inc., and Littelfuse, Inc. have been contributing to the development of applications through application-oriented products.

- Key players include Infineon Technologies AG, STMicroelectronics, Wolfspeed, Inc., ROHM Co., Ltd., Mitsubishi Electric Corporation, TOSHIBA ELECTRONIC DEVICES & STORAGE CORPORATION, Microchip Technology Inc., Hitachi, Ltd., Semiconductor Components Industries, LLC (Onsemi), Fuji Electric Co., Ltd., Littelfuse, Inc.

Silicon Carbide Power Semiconductor Market Recent Developments

- Mar 2026 - Wolfspeed introduced the industry’s first commercially available 10 kV SiC MOSFET, marking a significant advancement in ultra-high-voltage power devices. The innovation expands SiC applications into grid infrastructure, industrial electrification, and data center power systems, enabling higher efficiency, improved durability, and next-generation power conversion architectures.

- December 2025 - Fuji Electric and Robert Bosch GmbH collaborated to develop mechanically compatible SiC power modules for EV inverters. Standardized packaging enables interchangeable integration without redesign, reducing development time and enabling dual sourcing, thereby enhancing supply chain resilience and accelerating EV deployment.

- August 2025 - Toshiba Electronic Devices & Storage Corporation and SICC Co., Ltd. signed an MOU to enhance SiC wafer quality and ensure stable supply. The collaboration strengthens the upstream supply chain, supporting improved device yield and scalable growth in the SiC power semiconductor market.

- May 2025- Toshiba Electronic Devices & Storage Corporation introduced 650V 3rd generation SiC MOSFETs in a compact DFN8×8 surface-mount package, targeting industrial power applications. The new devices deliver higher power density and improved efficiency through reduced switching losses and enhanced thermal performance.

- June 2024 - ROHM Co., Ltd. launched the EcoSiC brand to consolidate its SiC product portfolio under a unified, sustainability-focused platform, strengthening its positioning in high-efficiency power semiconductor solutions and supporting growth across automotive, energy, and industrial applications.

Why Choose DataM?

- Technological Innovations: Explores the latest advancements in silicon carbide power Semiconductor design, including improved hydraulic systems, advanced operator controls, telematics integration, electric and hybrid powertrains and enhanced attachment versatility that are driving higher productivity and lower operating costs across construction and industrial applications.

- Product Performance & Market Positioning: Evaluates how different OEMs perform in real-world construction, landscaping, agriculture and municipal environments. The analysis compares lifting capacity, breakout force, fuel efficiency, durability, operator comfort and attachment compatibility, highlighting how leading manufacturers differentiate themselves globally.

- Real-World Evidence: Highlights practical use cases of silicon carbide power semiconductor across infrastructure development, road maintenance, warehouse handling and smart city projects. It demonstrates measurable improvements in jobsite efficiency, reduced labor dependency, faster material handling and optimized equipment utilization.

- Market Updates & Industry Changes: Tracks important industry developments such as new product launches, electrification initiatives, localized manufacturing expansions, tightening emission standards (Stage V, Tier 4 Final) and shifts in construction spending across major regions, including North America, APAC, China and India.

- Competitive Strategies: Analyzes how leading manufacturers are expanding their footprint through dealer network strengthening, localized production, electric model introductions, strategic partnerships and technology-driven differentiation such as AI-enabled monitoring and autonomous-ready platforms.

- Pricing & Market Access: Explains pricing structures across standard, high-capacity and electric skid steer models, including outright purchase, leasing and rental models. It also reviews regional availability, distribution networks and financing strategies that enhance market penetration.

- Market Entry & Expansion: Identifies growth opportunities in emerging economies driven by infrastructure development, urbanization, smart city programs and expanding rental ecosystems. It also outlines strategies for OEMs to scale operations globally through regional manufacturing hubs and after-sales service optimization.

Target Audience 2026

- Automotive OEMs & EV Manufacturers: Electric car manufacturers, tier one suppliers, and mobility solutions companies using SiC semiconductors for traction inverters, battery charging stations, and powertrains.

- Renewable Energy & Power Infrastructure Companies: Solar and wind energy companies, inverter manufacturers, and utilities incorporating SiC semiconductors for superior energy conversion, grid stability, and high-performance capabilities.

- Industrial Automation & Equipment Manufacturers: Organizations that use motors and drive systems, robotics, UPS, and other power supply applications using SiC technology to maximize energy efficiency, minimize footprint, and improve reliability.

- Semiconductor Manufacturers & IDMs: IDMs and fabless organizations specializing in wafer, epitaxial growth, and device manufacturing using SiC for innovation and capacity building.

- Charging Infrastructure Providers: EV charging network operators and equipment manufacturers deploying SiC-based fast-charging systems to enable high-power, efficient, and compact charging solutions.

- Investors & Private Equity Firms: Investment groups tracking growth in construction equipment manufacturing, rental markets and electrification of compact machinery.

- Dealers & Distribution Networks: Authorized distributors, service providers and aftermarket suppliers involved in sales, financing, spare parts and maintenance services.

Suggestions for Related Report