Recycled Steel Market Definition and Overview

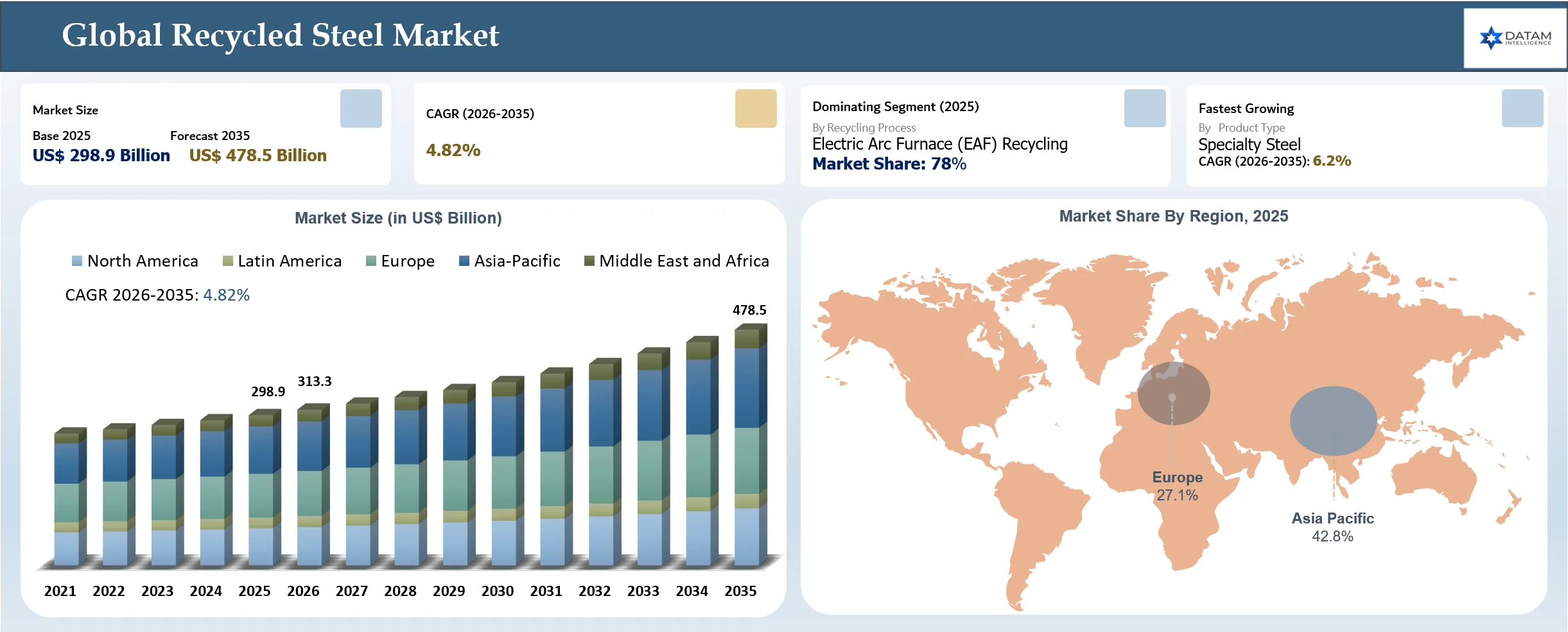

The global Recycled Steel market reached USD 298.9 billion in 2025 and is expected to reach USD 478.5 billion by 2035, growing with a CAGR of 4.82% during the forecast period 2026-2035, due to the increased usage of ferrous scrap by steel manufacturers and quick shifts towards the EAF-based steelmaking process that reduces production emissions and decreases usage of virgin iron ore. According to the World Steel Association, 30.3% of the world’s gross output of crude steel in 2025 was produced using the EAF process. Investment in scrap processing facilities, increasing strictness of decarbonization laws in the industry, and rising demand for low-carbon steel from the construction, automotive, and manufacturing sectors further promote market expansion. However, price volatility of ferrous scrap, low quality of scrap, and lack of its consistency and availability become the most critical issues.

According to the BIR Convention in Bangkok held in October 2025, Statistics Advisor Rolf Willeke indicated that the worldwide production of crude steel reduced by 2.2% to reach 934.3 million tonnes in H1 2025, while the amount of recycled steel in significant nations/regions dropped by 6.9% to 235.96 million tonnes, which accounts for 76% of worldwide steel manufacturing. Even though there was an immediate reduction, BIR predicts that about 630 million tonnes of recycled steel will be utilized each year across the globe and thus reduce nearly 950 million tonnes of CO2 emissions.

Key Takeaways

- The electric arc furnace recycling segment captured a dominant 78% of the global market share in 2025. This aligns with data from the World Steel Association showing that 30.3% of the world’s gross crude steel output was produced via EAF in 2025.

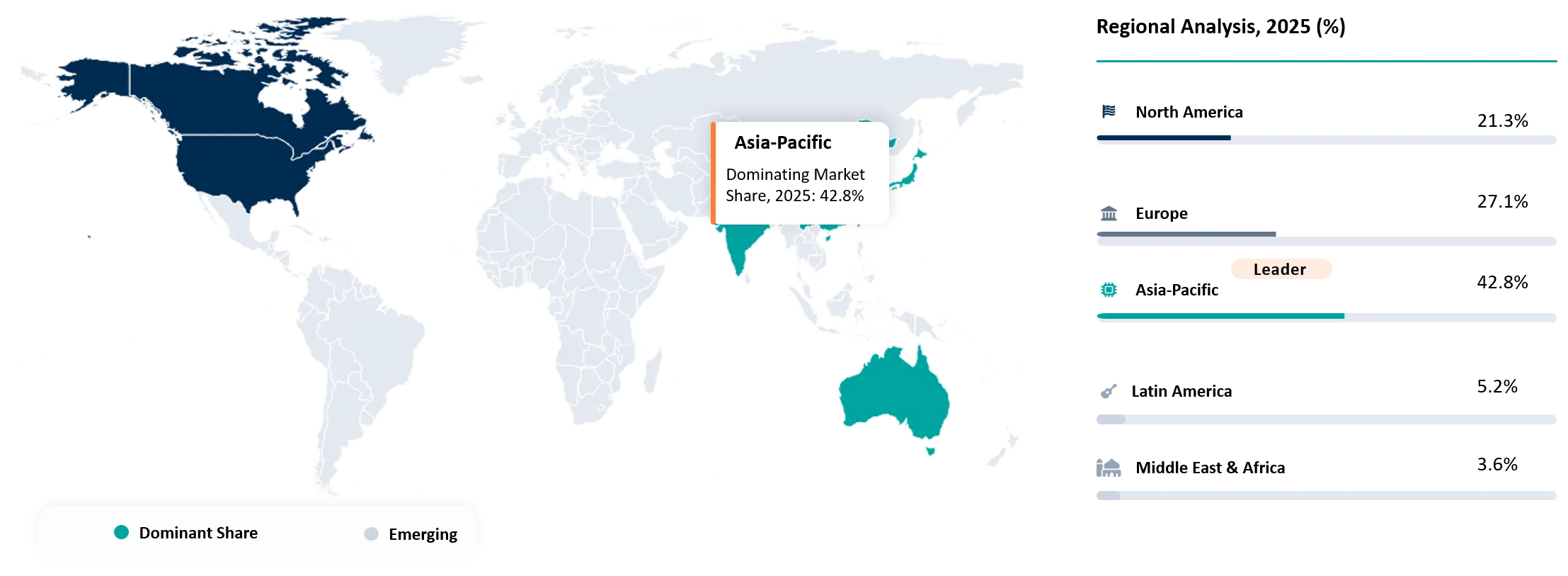

- The Asia-Pacific region emerged as the largest market center, accounting for an estimated 42.8% share of the global recycled steel market in 2025. The region's significant footprint is highlighted by China alone exporting a record-breaking 131 million tonnes of steel during the same year.

- The Bureau of International Recycling predicts that approximately 630 million tonnes of recycled steel will eventually be utilized annually worldwide. This massive level of recycling is expected to substantially lower carbon emissions by eliminating nearly 950 million tonnes of CO2 each year.

- Global exports and imports of ferrous scrap experienced growth, rising to 456.5 million tonnes in 2025. This represents a notable increase compared to the 449.2 million tonnes recorded in the previous year of 2024.

Recycled Steel Market Industry Trends and Strategic Insight

- Increase in capacity of Electric Arc Furnaces (EAFs) will determine demand for recycled steel in the coming years. The steel producers are making efforts to increase production from the EAF-based steelmaking process.

- Advanced scrap sorting techniques are improving recycled steels such as, Machine learning, computer vision, X-ray fluorescence (XRF), and Laser-Induced Breakdown Spectroscopy (LIBS) have been implemented for sorting alloy grades and minimizing residual contamination.

- The purchase of green steel is fueling the need for recycled material certifications. The need for EPDs, verification of recycled content, and lifecycle carbon emissions reports is on the rise among infrastructure builders, automotive original equipment manufacturers (OEMs), and industry manufacturers.

- Hybrid EAF-DRI technology production routes are expanding recycled steel utilization. Manufacturers are mixing recycled steel scrap with Direct Reduced Iron (DRI).

- Technology is improving the recycled steel supply chains through digital traceability. The traceability of materials has been made possible through material traceability technology, digital scrap inventory systems, blockchain-enabled systems, and lifecycle data management systems.

Recycled Steel Market Scope

| Metrics | Details | |

| 2025 Market Size | USD 298.9 Billion | |

| 2035 Projected Market Size | USD 478.5 Billion | |

| CAGR (2026-2035) | 4.82% | |

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Scrap Type | Ferrous Scrap, Obsolete (Old) Scrap, Prompt (Industrial) Scrap, Others | |

| By Recycling Process | Electric Arc Furnace (EAF) Recycling, Basic Oxygen Furnace (BOF) Recycling, Others | |

| By Product Type | Flat Steel, Hot Rolled Coil (HRC), Cold Rolled Coil (CRC), Steel Plates, Sheets, Galvanized Steel, Tinplate, Long Steel, Rebar, Wire Rod, Structural Sections, Rails, Merchant Bars, Stainless Steel, Alloy Steel, Specialty Steel | |

| By End-Use | Building & Construction, Automotive & Transportation, Industrial Machinery & Equipment, Energy & Power, Packaging, Shipbuilding, Consumer Appliances, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Türkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Recycled Steel Market Disruption Analysis

Rapid Expansion of Electric Arc Furnace (EAF) Steelmaking Reshaping the Global Recycled Steel Value Chain

The primary disruption in the Recycled Steel Market is the accelerating adoption of electric arc furnace (EAF) steelmaking, which is fundamentally changing global steel production by increasing dependence on recycling ferrous scrap instead of virgin iron ore. This is affecting sourcing policies where steel producers are now investing in the processing capacity of ferrous scrap and gaining access to good-quality raw materials required to manufacture green steel. According to a recent report published by the International Energy Agency (IEA), the pipeline of announced green steel projects across the globe had surpassed 400 million tons per annum (Mtpa) by the beginning of 2026, and most of the new projects are through the EAF and DRI-EAF route, requiring much larger volumes of recycled steel.

In addition, government bodies and large steel manufacturers are giving preference to circular manufacturing and industrial decarbonization by means of green steel projects, which has led to the acquisition of more scrap processing companies, renovation of recycling plants, and digitalization of the scrap processing industry. With the growing demand for low-carbon steel in automotive, construction, renewable energy, and engineering sectors, scrap steel is now becoming an important resource rather than just a secondary material source, thus fostering competition for quality ferrous scrap around the world.

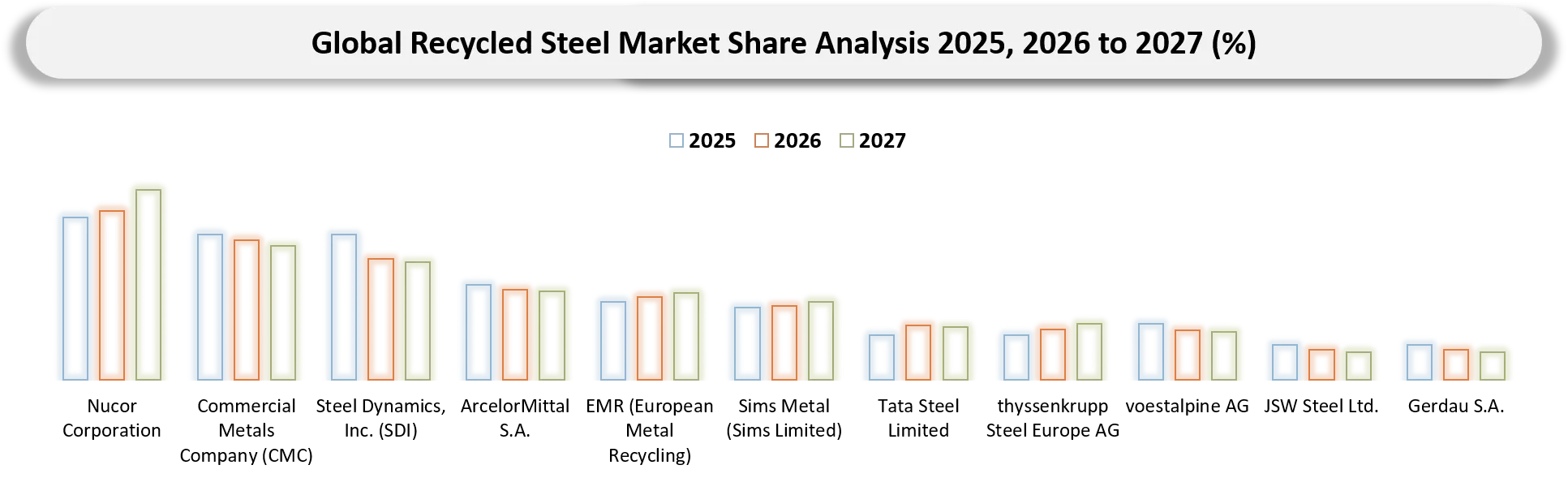

Recycled Steel Market BCG Matrix: Company Evaluation

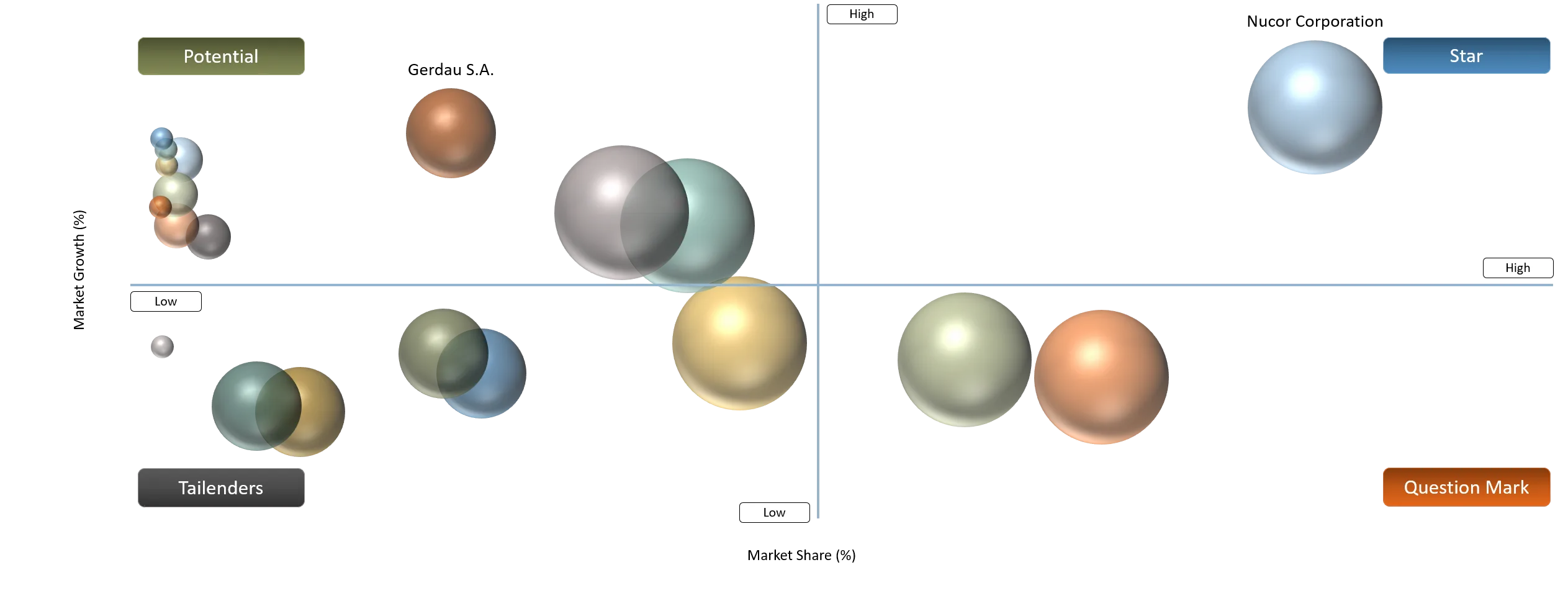

Stars include Nucor Corporation, Steel Dynamics, Inc. (SDI), and ArcelorMittal S.A., since they have strong capabilities in scrap-based steel manufacturing, large EAF plants, and recycled steel as part of their decarbonization strategy. The Question Marks include CMC, Tata Steel Limited, and JSW Steel Ltd., which are fast becoming the leaders in recycled steel production due to investments made by them in EAFs, steel scrap recycling plants, and circular economy projects.

Potential classification encompasses companies such as Gerdau S.A., voestalpine AG, and thyssenkrupp Steel Europe AG, which are gradually adopting recycled steel by way of green steel initiatives and advanced scrap recycling technology. Tailenders include EMR (European Metal Recycling), Sims Metal (Sims Limited), and Cleveland-Cliffs Inc. EMR and Sims Metal are amongst the world’s best ferrous scrap processors and providers, though their steel production is minimal in comparison to integrated steel producers.

Recycled Steel Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

Rapid deployment of electric arc furnace (EAF) technology is the primary driver of the recycled steel market, as EAFs utilize predominantly ferrous scrap instead of virgin iron ore. | 32% | High | Scrap-based steel production, long products, flat steel, construction steel | Accelerates transition toward low-carbon steelmaking, increases ferrous scrap demand, and drives investmentsin EAF capacity and scrap processing infrastructure. |

Steel manufacturers are increasing recycled steel consumption to reduce greenhouse gas emissions and meet corporate net-zero targets. | 26% | High | Green steel production, automotive, infrastructure, industrial manufacturing | Strengthens adoption of recycled steel in decarbonization strategies, improves ESG compliance, and expands demand for certified low-carbon steel. |

Government Policies encouraging steel recycling, landfill diversion, and recycled-content utilization are accelerating investments in scrap collection, processing, and recycling infrastructure across major steel-producing economies. | 22% | Medium–High | Municipal recycling, construction, public infrastructure, steel manufacturing | Expands recycling capacity, improves scrap recovery rates, and strengthens domestic circular steel supply chains through regulatory support.18% |

Growth in Automotive Lightweighting and Sustainable Manufacturing are using recycled steel to lower vehicle lifecycle emissions while complying with stringent environmental regulations and sustainability targets. | 18% | Medium | Automotive components, EV manufacturing, transportation equipment | Increases OEM procurement of recycled steel, supports lightweight vehicle production, and drives long-term supply agreements with recyclers. |

Deployment of AI-enabled sorting systems, sensor-based metal identification, robotic scrap handling technologies is improving scrap purity, recovery efficiency of recycled steel suitable for high-value applications. | 14% | Medium | Advanced scrap processing, specialty steel, engineering-grade steel | Enhances recycled steel quality, reduces contamination, increases recovery efficiency, and enables premium-grade recycled steel production. |

Rapid deployment of electric arc furnace (EAF) technology is the primary driver of the recycled steel market, as EAFs utilize predominantly ferrous scrap instead of virgin iron ore

The rapid adoption of Electric Arc Furnace (EAF) technology serves as one of the important factors driving the growth of the Recycled Steel Market because EAF uses recycled ferrous scrap rather than primary iron ore and metallurgical coal. Increased investments in green steel production have prompted companies to upgrade their existing plants as well as build new capacity for production based on scrap. As per the data published by the World Steel Association – World Steel in Figures 2026, the global exports/imports of ferrous scrap were recorded at 456.5 million tonnes in 2025 compared to 449.2 million tonnes in 2024.

For instance, in June 2026, Mysteel reported that the production of the 87 independent EAF steelmakers in China recovered and the utilization of EAF was 77.36% in June 2026 due to the increasing number of mills returning to operation after maintenance.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

Growing demand for premium-grade recycled steel is outpacing the availability of clean, low-residual ferrous scrap. | 22% | Raw Material Availability | Automotive steel, electrical steel, high-strength structural steel | Intensifies competition for premium scrap, limits production of high-grade recycled steel, and increases procurement costs. |

Inconsistent Scrap Collection and Recycling Infrastructure. | 18% | Scrap Collection & Processing | Construction steel, industrial manufacturing, regional recycling operations | Reduces scrap recovery efficiency, creates regional supply gaps, and limits expansion of circular steel supply chains. |

Frequent fluctuations in ferrous scrap prices. | 20% | Raw Material Procurement Costs | Electric Arc Furnace (EAF) steelmaking, long products, flat steel production | Increases production cost volatility, compresses operating margins, and encourages long-term procurement contracts and vertical integration. |

Stringent Environmental and Operational Compliance Costs. | 14% | Regulatory Compliance & Operations | Scrap processing facilities, steel recycling plants, EAF operations | Raises capital and operating expenditures for recyclers, delays capacity expansion, and accelerates investment in cleaner processing technologies. |

Frequent fluctuations in ferrous scrap prices

One of the key restraints limiting the growth of the Recycled Steel Market is the consistent fluctuations in the price of ferrous scrap, which have an impact on the cost of raw materials procurement and production processes for steel producers that use scrap as input material. The prices of ferrous scrap are very volatile, and the main factors affecting the volatility include the demand for steel globally, industrial production, trade regulations, freight rates, and supply of scrap. As per the Bureau of International Recycling (BIR), there have been many price fluctuations in the global ferrous scrap market in 2025 due to low demand for steel in China, import policy changes in Türkiye, and purchase activities in Europe and Asia.

For instance, in April 2026, S&P Global Commodity Insights reported that the Indian ferrous scrap market was slow due to the rising costs of importing caused by geopolitical issues in the Middle East. The prices of imported shredded scrap increased to US$369.32 per metric ton CFR Nhava Sheva in March 2026 compared to US$345.95 per metric ton in December 2025, while the price of HMS 1/2 (80:20) scrap increased from US$320-345 to US$345-370 per metric ton.

Recycled Steel Market Segment Analysis

The global recycled steel market is segmented based on scrap type, recycling process, product type, end-use, and region.

Electric Arc Furnace (EAF) Recycling Dominates the Market as Steelmakers Accelerate the Transition Toward Low-Carbon Production

The electric arc furnace (EAF) recycling segment dominated the Recycled Steel Market, capturing about 78% of the market share in 2025. This is because of the rising use of the process of making steel using scrap metal, as EAF uses mostly scrap material rather than raw materials such as iron ore, hence saving on energy. Producers of steel in regions including North America, Europe, and Asia-Pacific have been increasing capacities of electric arc furnaces as a measure of meeting industrial decarbonization targets and the increasing demand for eco-friendly steel. The rising availability of steel scrap contributes greatly to this domination.

In parallel, industry investments in new EAF plants and modernization works in 2025 and 2026.

According to the OECD Steel Outlook 2026, total global steelmaking capacity stood at around 2.5 billion tonnes in 2025, and the majority of announced increases in capacity were for low-emission steelmaking processes, especially electric arc furnace-based steelmaking. With the introduction of carbon reduction policies by governments and steel producers' replacement of their outdated blast furnace capacities, EAF recycling would remain the most important form of recycling in the future.

Recycled Steel Market Geographical Penetration

Asia-Pacific Leads the Recycled Steel Market Through Expanding Scrap-Based Steel Production and Circular Economy Investments

The Asia-Pacific emerged as a dominating region in the Recycled Steel Market, taking up an approximate 42.8% share of the global market in 2025. These factors include the presence of the largest steel-producing center in the world, the creation of ferrous scrap, rising EAF steel production, and growing interest in circular manufacturing in the region. Some of the leading countries of the region, namely China, India, Japan, and South Korea, are fast adopting recycled steel as it helps decrease reliance on raw materials, at the same time helping in achieving industrial carbon emission targets. Growing infrastructure developments, automobile manufacturing, renewable energy initiatives, and manufacturing activities are the key factors fueling the demand for recycled steel. According to the OECD Steel Outlook 2026, India added 41.4 million tonnes (Mt) of steelmaking capacity between 2021 and 2025 and plans to add up to 31.8 Mt of additional capacity by 2028, while China exported a record 131 Mt of steel in 2025, highlighting the region's significant influence on global steel supply chains.

For instance, in May 2025, Nippon Steel announced a basic agreement with Nakayama Steel Works to set up a joint venture aimed at establishing an Electric Arc Furnace (EAF) in Japan. The project involves about ¥95 billion (more than $650 million) investment in setting up a new steel production facility with EAF and about ¥50 billion in joint venture investment, where Nakayama Steel will own 51% while Nippon Steel owns 49%.

China Recycled Steel Market Trends

China holds the dominant position in the Asia-Pacific Recycled Steel Market, due to the country’s substantial capacity for steel production, developed collection system for ferrous scrap, and rapid transformation towards low-carbon steel production. China's high-level policies aimed at decarbonizing industries, developing a circular economy, and increasing the capacity of EAFs have contributed greatly to the use of recycled steel in such industries as construction, automobiles, machines, and infrastructure. Major Chinese integrated steel companies like China Baowu Steel Group, HBIS Group, and Ansteel Group maintain their dominance in the region's recycled steel market value chain through the purchase of domestic scrap and steelmaking using EAFs. Furthermore, the OECD Steel Outlook 2026 reported that China exported a record 131 million tonnes of steel in 2025, underscoring its significant influence on global steel supply chains.

For example, in August 2025, Zhejiang Resources Recycling Co., Ltd., a China-based recycling company, agreed to acquire a 51% stake in Zhejiang New Century Renewable Resources Development Co., Ltd. and Zhejiang Deqing Hanggang Fuchun Regeneration Technology Co., Ltd. for approximately CNY 510 million (US$71 million).

India Recycled Steel Market Outlook

India is the fastest-growing country in the Asia-Pacific Recycled Steel market due to growth in the installation capacity of steel-making plants, increased usage of scrap steel, and a focus on sustainable manufacturing by the Indian government. Increased investments in electric arc furnaces, scrap collection, and recycling facilities in the nation have improved the recycled steel industry in India. Moreover, high demand from construction, automotive, infrastructure, railway, and engineering industries is prompting the use of recycled steel by steel manufacturers. According to the OECD Steel Outlook 2026, India added 41.4 million tonnes (Mt) of steelmaking capacity between 2021 and 2025, the largest net capacity increase globally, and is projected to increase total steelmaking capacity to 191.3–217.1 Mt by 2028.

For example, in July 2025, Manbro Industries announced three strategic acquisitions to strengthen its presence in value-added steel products, vehicle scrappage, and metal recycling in India. The company acquired a 26% stake in KD Ecosystem, the first registered vehicle scrappage facility in Eastern India with the capacity to dismantle 42,500 end-of-life vehicles annually, a 51% stake in Shivam Pipe Industries with a production capacity of 3,000 metric tons per month, and a 99.90% stake in K D Infrastructures.

Recycled Steel Market Competitive Landscape

- The market consists of three main groups of players: fully integrated steel manufacturers who operate large scale scrap-based steel production facilities, international metal recyclers and processors of scrap material, as well as regional steel manufacturers who increase their EAF capacity. The Nucor Corporation, SDI (Steel Dynamics, Inc.), CMC (Commercial Metals Company), Gerdau S.A., JSW Steel Ltd., Tata Steel Limited, ArcelorMittal S.A., Cleveland-Cliffs Inc., thyssenkrupp Steel Europe AG, and voestalpine AG benefit from using EAF technology, integrated approach to scrap sourcing, as well as existing steel production capacities to increase their competitive position on the market. At the same time, EMR (European Metal Recycling) and Sims Metal (Sims Limited) provide an important contribution to global ferrous scrap supply and processing, providing good quality scrap materials to steel manufacturers in North America, Europe, and Asia-Pacific regions.

- Key players are Nucor Corporation, Commercial Metals Company (CMC), Steel Dynamics Inc. (SDI), ArcelorMittal S.A., European Metal Recycling (EMR), Sims Metal (Sims Limited), Tata Steel Limited, thyssenkrupp Steel Europe AG, voestalpine AG, JSW Steel Ltd., Gerdau S.A. and Cleveland-Cliffs Inc.

Key Developments

- In April 2025: Sev. en Global Investments completed the acquisition of Celsa Steel UK and Celsa Nordic, rebranding them as 7 Steel UK and 7 Steel Nordic, with a combined annual capacity of around 2 million tonnes of steel production.

- In May 2026: Derichebourg announced the acquisition of the Scholz Group, one of Europe’s largest metal and steel scrap recycling companies, significantly expanding its European recycling footprint. The Scholz Group processes millions of tonnes of ferrous and non-ferrous scrap annually, strengthening supply chains for recycled steel production via electric arc furnace (EAF) routes, and supporting the growing demand for low-carbon steel and circular economy initiatives across Europe.

- In July 2025: TSR Group signed a long-term supply agreement with voestalpine valid until 2034, ensuring the continuous delivery of recycling raw materials, primarily processed steel scrap, to support industrial steel production.

- In March 2025: ArcelorMittal Nippon Steel India (AM/NS India) commissioned a scrap processing facility in Khopoli, Maharashtra, marking the first of four planned units under its expansion strategy. The facility, with a capacity of 120 kilo tonnes per annum (KTPA) and part of a ₹350 crore investment program, is designed to process ferrous scrap for use in steelmaking, strengthening India’s domestic scrap supply chain and supporting the company’s shift toward recycled steel production and decarbonized steelmaking through electric arc furnace (EAF) routes.

- In June 2025: SSAB and Volvo Cars announced a partnership to advance the use of fossil-free and decarbonized steel, with a focus on integrating recycled and low-carbon steel materials into automotive manufacturing.

Key Procurement Priorities and Buyer Evaluation Criteria

- The procurement decision-making process is increasingly being shaped by global decarbonization mandates, carbon border regulations, and net-zero commitments, with buyers actively favoring recycled steel producers that can demonstrate measurable reductions in CO₂ emissions through electric arc furnace (EAF) operations and high scrap utilization rates.

- Buyers are placing strong emphasis on traceability and transparency across the scrap value chain, evaluating suppliers based on their ability to provide verifiable sourcing data, digital tracking of recycled inputs, and third-party sustainability certifications to ensure compliance with ESG reporting frameworks and green procurement standards.

- Procurement strategies are increasingly influenced by circular economy integration, where buyers prefer suppliers that can support closed-loop recycling systems, industrial scrap recovery partnerships, and end-of-life material reprocessing programs to enhance resource efficiency and reduce dependency on virgin iron ore.

- End-use performance requirements are a key evaluation factor, with buyers assessing recycled steel producers on mechanical strength consistency, corrosion resistance, weldability, and compliance with industry-specific standards, particularly for automotive lightweighting, infrastructure durability, and high-performance engineering applications.

Why Choose DataM?

- Technological Innovations: Explores advancements in recycled steel production, including electric arc furnace (EAF) optimization, scrap sorting automation, digital metallurgy, and low-carbon steelmaking technologies, enabling improved energy efficiency, reduced emissions, and consistent high-quality steel output for automotive, construction, and industrial applications.

- Product Performance & Market Positioning: Evaluates how different producers deliver recycled steel grades based on tensile strength, ductility, corrosion resistance, and alloy consistency, highlighting how leading players differentiate through low-carbon steel portfolios, high scrap utilization rates, and scalable production capabilities across infrastructure and mobility sectors.

- Real-World Evidence: Highlights adoption of recycled steel across automotive lightweighting, rail infrastructure, construction beams, packaging steel, and renewable energy structures, demonstrating benefits such as reduced carbon footprint, lower lifecycle emissions, cost efficiency, and compliance with green building and sustainability standards.

- Market Updates & Industry Changes: Tracks key developments such as green steel plant expansions, hydrogen-ready and EAF capacity additions, circular economy initiatives, scrap supply chain modernization, and regional decarbonization policies across Europe, North America, and Asia-Pacific driving accelerated recycled steel adoption.

- Competitive Strategies: Analyzes how leading steel manufacturers expand through decarbonization investments, strategic scrap sourcing partnerships, renewable energy integration, and advanced recycling technologies to strengthen their position in the low-carbon steel ecosystem and meet ESG-driven procurement demands.

- Pricing & Market Access: Explains pricing variations based on scrap quality, energy costs, alloy complexity, and regional supply-demand dynamics, along with market access through integrated steelmakers, mini-mills, recycling aggregators, and global trading networks supporting circular steel supply chains.

- Market Entry & Expansion: Identifies growth opportunities driven by global net-zero targets, green infrastructure investments, EV manufacturing, and sustainable construction demand, while outlining strategies such as regional recycling capacity expansion, closed-loop partnerships, and technology-driven efficiency improvements to scale recycled steel adoption globally.

Target Audience

- Steel Manufacturers & Producers

- Scrap Metal Suppliers & Recycling Companies

- Automotive OEMs & Tier Suppliers

- Construction & Infrastructure Companies

- Energy & Utilities Sector

- Aerospace, Rail & Heavy Engineering Industries

- Government & Regulatory Bodies