Preventive Vaccine Market Size

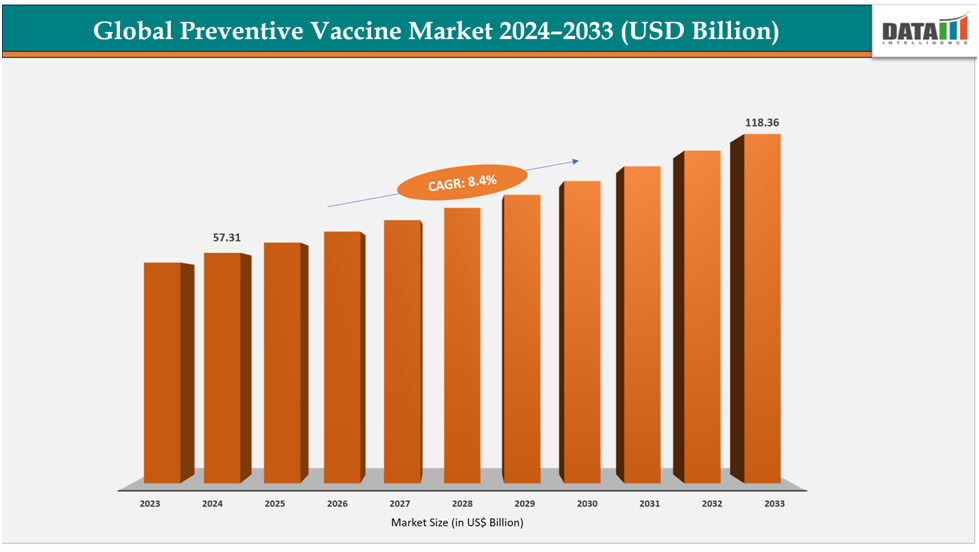

The global preventive vaccine market size reached in US$ 62.12 billion 2025 and is expected to reach US$118.36 billion by 2033, growing at a CAGR of 8.4%during the forecast period 2026-2033.

Innovations in vaccine research and development, including mRNA, protein subunit, and conjugate technologies, are speeding up the creation of safer, more efficient, and quicker-to-produce vaccinations. New developments make it possible to target newly developing infectious diseases and enhance immune responses across all age groups. Around the world, robust government vaccination programs are increasing vaccine accessibility at the same time by providing financing, launching awareness campaigns, and enforcing vaccination laws. When combined, these elements raise demand, lower the burden of disease, and boost vaccine coverage.

Market Dynamics

The preventive vaccine market is experiencing steady growth driven by the rising prevalence of infectious diseases such as influenza, dengue, HPV, and pneumonia, along with the continued emergence of new viral threats. Increasing global immunization programs, supported by governments and international organizations, are playing a crucial role in expanding vaccine coverage and ensuring consistent demand. Growing awareness about disease prevention, rising healthcare expenditure, and strong investments in vaccine research and development are further accelerating market expansion. Technological advancements, including mRNA platforms, recombinant vaccines, and faster development cycles, are improving vaccine efficacy and accessibility. Additionally, the expansion of vaccination programs beyond pediatrics to include adult and elderly populations is significantly broadening the market scope.

However, the market faces several challenges, including high development and production costs, complex regulatory requirements, and the need for robust cold chain infrastructure for vaccine storage and distribution. Vaccine hesitancy and misinformation in certain regions can also limit adoption rates. Dependence on government funding and procurement programs creates pricing pressures for manufacturers, while competition from alternative preventive therapies and shifting healthcare priorities may impact investment flows. Despite these challenges, significant opportunities exist in the development of advanced and combination vaccines, expansion into emerging markets, and increasing demand for life-cycle immunization strategies. Continuous innovation, strategic partnerships, and advancements in delivery technologies are expected to drive long-term growth, even as evolving regulatory and public health dynamics continue to shape the market.

For more details on this report, see Request for Sample

Segmentation Analysis

The global preventive vaccine market is segmented based ontype, disease indication, route of administration, distribution channel, and region

By Disease Indication:

By Type:

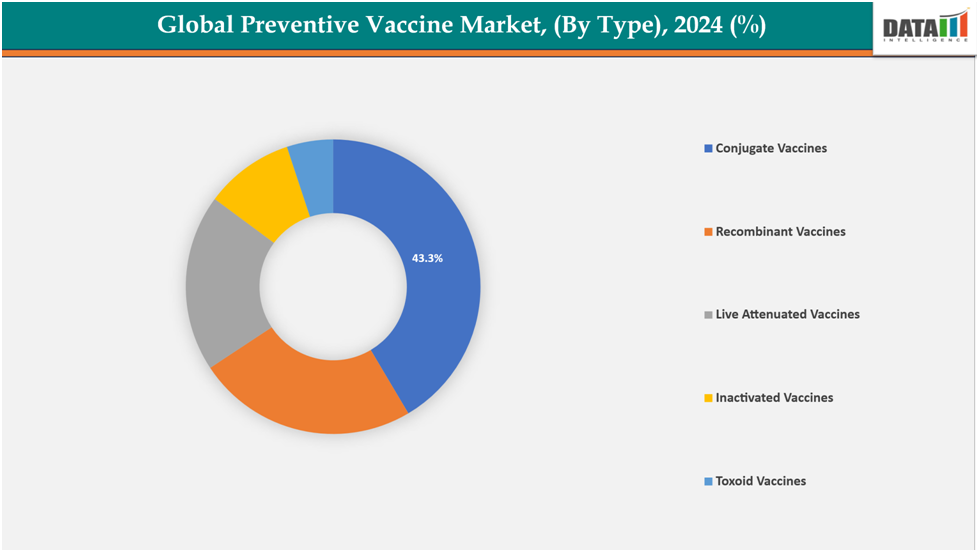

The conjugate vaccines segment from type is dominating the preventive vaccine market with a 43.3% share in 2024

Conjugate vaccines dominate the preventive vaccine market primarily because they effectively protect infants and young children, the most vulnerable populations. Unlike plain polysaccharide vaccines, conjugate vaccine links the bacterial sugar coat to a carrier protein, powerfully engaging the immature immune system to trigger a robust, long-lasting response with immunological memory.

Moreover, scientific advantage, continuousinvestments in research and development, and higher-valent vaccines expand coverage, allowing protection against multiple strains, reducing severe diseases like invasive pneumococcal and meningococcalinfections. For instance, in July 2025, the FDA approved MenQuadfi, a meningococcal conjugate vaccine developed by Sanofi Pasteur, for active immunization against invasive disease caused by Neisseria meningitidis serogroups A, C, W, and Y. It was authorized for use in individuals six weeks of age and older, marking a significant advancement in pediatric and adult protection.

The Pneumococcal disease segment disease indication is dominating the preventive vaccine market with a 25.5% share in 2024

The pneumococcal vaccine segment dominates the preventive vaccine market due to the high global burden of pneumococcal disease, which causes pneumonia, meningitis, and bloodstream infections, particularly in children under five and the elderly. The broad acceptance of effective vaccinations, such as PCV and PPSV, is fueled by their inclusion in numerous national immunization programs. Vaccines become more accessible through government programs and international partnerships that fund them. Additionally, the cost-effectiveness of immunization over therapy and growing awareness of preventative healthcare are driving demand.

Moreover, innovation in vaccines covering more serotypes strengthens their appeal.In June 2024, the U.S. FDA approved Merck’s CAPVAXIVE (Pneumococcal 21-valent Conjugate Vaccine) for adults aged 18 and older. The vaccine was designed to provide active immunization against 21 Streptococcus pneumoniae serotypes, targeting those responsible for the majority of invasive pneumococcal disease and pneumonia cases in adults.

Geographical Analysis

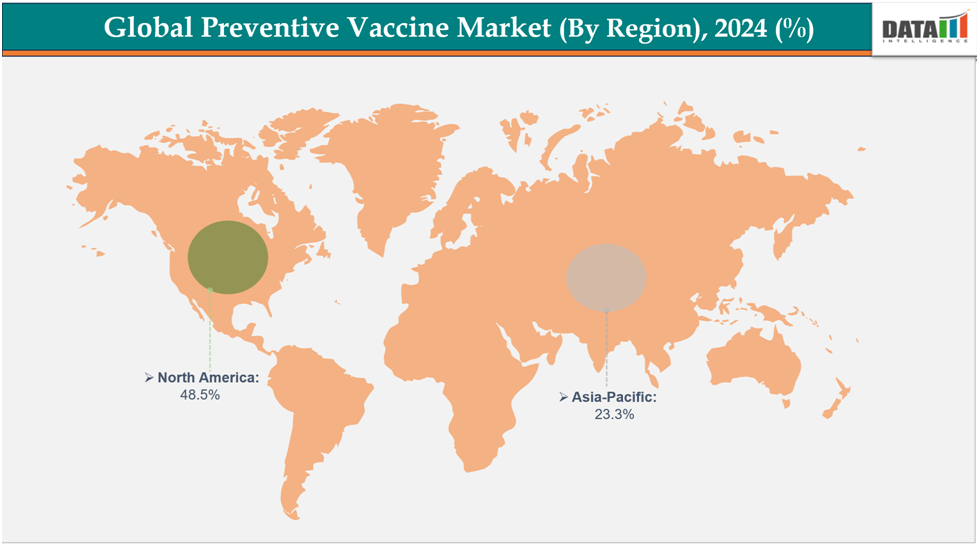

North America is dominating the global preventive vaccine market with a 48.5% in 2024

North America has a well-developed market for preventive vaccines because of its high immunization rate and robust public health programs that target at-risk groups, adults, and children. Conjugate and mRNA vaccines are the most popular preventative vaccinations in North America because of their great efficacy, safety, and wide range of protection against many infectious disease strains. According to CDC guidelines, vaccinations against influenza, COVID-19, meningococcal disease, and pneumococcal disease are frequently given to people of all ages. Strong intellectual property protection, high vaccination costs, and FDA regulations that promote significant R&D investment are the main drivers of the region's market supremacy.

The dominance of the U.S. is further reinforced by recent regulatory and market development. For instance, in September 2024, the FDA approved FluMist, AstraZeneca’s needle-free influenza vaccine, for self- or caregiver-administration at home. Adults up to 49 years old could self-administer, while parents or caregivers could vaccinate children aged 2–17. Approval was supported by usability studies demonstrating safe and effective administration across eligible age groups.

Europe's the second region after North America which is expected to dominate the global preventive vaccine market with a 34.5% in 2024

Europe’s preventive vaccine market growth is driven by high public awareness of immunization and well-established healthcare systems. Widespread access to hospitals, clinics, pharmacies, and online platforms, combined with cross-border collaborations and public health campaigns, has increased vaccine adoption across the region. Favorable government policies and national immunization programs promote routine and seasonal vaccination for children, adults, and at-risk populations. For example, in October 2024, the European Union promoted the European Immunization Agenda 2030 (EIA2030) across all 53 member states, aiming to strengthen immunization systems, improve vaccine coverage, and combat vaccine hesitancy through public health campaigns.

Germany’s preventive vaccine market is driven by advanced healthcare infrastructure, supportive regulations, and high public awareness. Hospitals, clinics, pharmacies, and digital platforms provide widespread access, while national immunization programs, public health campaigns, and strong government and private support promote vaccine adoption, ensuring robust coverage and sustained market growth nationwide.

The Asia Pacific region is the fastest-growing region in the global preventive vaccine market, with a CAGR of 7.5% in 2024

The Asia-Pacific preventive vaccine market, including Japan, China, India, and South Korea, is expanding due to rising health awareness, urbanization, and improved healthcare access. Advancement in research and developments by biological companies, government initiatives, public health programs, and educational campaigns promote immunization, encourage vaccine adoption, and strengthen disease prevention efforts across the region.

For instance, in October 2024, SK bioscience’s SkyCellflu Quadrivalent, the first Korean-developed cell-cultured influenza vaccine, received final market authorization from Indonesia’s BPOM. This approval marked a significant milestone as the first Korean flu vaccine approved for use in Indonesia, expanding access to advanced influenza prevention in Southeast Asia’s largest pharmaceutical market.

China and India are witnessing growing demand for preventive vaccines due to increased health awareness, expanding healthcare infrastructure, and government immunization programs. Enhanced access through hospitals, clinics, pharmacies, and online platforms, combined with educational campaigns, is driving vaccine adoption, supporting the growth of both routine and new preventive immunization options.

Competitive Landscape

Top companies in the preventive vaccine marketincludeGSK plc, Biological E Limited,HIPRA, Bharat Biotech, GSK plc, Sanofi, Bavarian Nordic, Merck Inc., Valneva SE, Pfizer Inc., andTakeda Pharmaceutical Company Limited,among others.

GSK plc: GlaxoSmithKline (GSK), a UK-based pharmaceutical leader, holds one of the world’s largest preventive vaccine portfolios. Its offerings include vaccines for influenza, HPV, shingles, and meningococcal diseases. GSK focuses on global immunization, with strong R&D in next-generation vaccines, targeting both developed and emerging markets to address public health needs worldwide.

Key Developments:

February 2026: Across North America, Europe, and Asia Pacific, rising prevalence of cancer, cardiovascular, and neurological diseases significantly accelerated demand for microRNA-based diagnostics and therapeutics, driving strong market growth.

January 2026: Advancements in next-generation sequencing (NGS), qPCR-based assays, and AI-driven bioinformatics tools enhanced miRNA profiling accuracy, enabling early disease detection and precision medicine applications.

December 2025: Leading companies such as Thermo Fisher Scientific, QIAGEN, Merck KGaA, NanoString Technologies, and Takara Bio expanded miRNA assay kits, sequencing platforms, and research solutions to strengthen global market presence.

November 2025: Increasing adoption of microRNA as non-invasive biomarkers in liquid biopsy significantly improved early cancer detection, disease monitoring, and treatment response analysis.

October 2025: Growing investments in miRNA-based therapeutics, including mimics and inhibitors, accelerated drug discovery for oncology, metabolic, and rare genetic disorders.

September 2025: In the United States, strong R&D funding, presence of leading biotech firms, and advanced genomic infrastructure significantly supported market expansion.

August 2025: In China, India, and Japan, increasing investments in genomics research, expanding biotechnology sectors, and rising demand for early diagnostic solutions accelerated regional growth.

July 2025: Expanding clinical trials, growing applications in infectious diseases and personalized medicine, and continuous innovation in miRNA delivery systems supported long-term global growth of the microRNA market.

Market Scope

| Metrics | Details | |

| CAGR | 8.4% | |

| Market Size Available for Years | 2022-2033 | |

| Estimation Forecast Period | 2026-2033 | |

| Revenue Units | Value (US$ Bn) | |

| Segments Covered | By Type | Conjugate Vaccines, Recombinant Vaccines, Live Attenuated Vaccines, Inactivated Vaccines, Toxoid Vaccines |

| By Disease Indication | Pneumococcal Disease, DTP (Diphtheria, Tetanus, Pertussis), Meningococcal Disease, MMR (Measles, Mumps, Rubella), Varicella, Influenza, Rotavirus, Polio, Human Papilloma Virus, Hepatitis, Dengue and Others | |

| By Route of Administration | Oral, Intramuscular, Subcutaneous and Others | |

| By Distribution Channel | Hospital Pharmacies, Retail Pharmacies | |

| Regions Covered | North America, Europe, Asia-Pacific, South America and the Middle East & Africa | |

The Global Preventive Vaccine Market report delivers a detailed analysis with 62 key tables, more than 52visually impactful figures, and 159 pages of expert insights, providing a complete view of the market landscape.

Suggestions for Related Report

For more biotechnology-related reports, please click here